PROGRAM ON HOUSING AND URBAN POLICY

|

|

|

- Marylou Boone

- 5 years ago

- Views:

Transcription

1 Insue of Busness and conomc esearch Fsher Cener for eal sae and Urban conomcs POGAM O OUSIG AD UBA POICY WOKIG PAP SIS WOKIG O. W-7 DGIG OUSIG ISK By Peer nglund Mn wang John M. Qugley December 2 These papers are prelmnary n naure: her purpose s o smulae dscusson and commen. Therefore hey are no o be ced or quoed n any publcaon whou he express permsson of he auhor. UIVSITY OF CAIFOIA BKY

2 edgng ousng sk * Peer nglund Mn wang John M. Qugley ** December 2 Absrac: An unusually rch source of daa on housng prces n Sockholm s used o analyze he nvesmen mplcaons of housng choces. Ths emprcal analyss derves marke-wde prce and reurn seres for housng nvesmen durng a 3-year perod and also provdes esmaes of he ndvdual-specfc dosyncrac varaon n housng reurns. Because he dosyncrac componen follows an auocorrelaed process he analyss of porfolo choce s dependen upon he holdng perod. We analyze he composon of household nvesmen porfolos conanng housng common socks socks n real esae holdng companes bonds and -blls. For shor holdng perods he effcen porfolo conans essenally no housng. For longer perods low rsk porfolos conan 5 o 5 percen housng. These resuls sugges ha here are large poenal gans from polces or nsuons ha would perm households o hedge her lumpy nvesmens n housng. We esmae he poenal value of hedges n reducng rsk o households ye yeldng he same nvesmen reurns. The value s surprsngly large especally o poorer homeowners. Keywords: Porfolo sk ouse Prce Index edgng. J Codes: G2 D6 * A prevous verson of hs paper was presened a he Maasrch-Cambrdge eal sae Fnance and Invesmen Symposum Maasrch eherlands June 2. We are especally graeful for commens of Frans A. de oon whch led o a subsanal mprovemen n he analyss. We also wsh o hank Sefan ydahl for research asssance. ** nglund Sockholm School of conomcs Peer.nglund@hhs.se wang Unversy of Calforna Berkeley mn@econ.berkeley.edu Qugley Unversy of Calforna Berkeley qugley@econ.berkely.edu

3 I. Inroducon ousng s a major componen of household consumpon expendure. The average household n Wesern urope and orh Amerca spends 25 o 35 per cen of s ncome on housng and young homeowners ofen spend even larger proporons. For a varey of reasons mos housng s owner-occuped. Dfferences n ax reamen and cred avalably conrbue o he subsanal dfferences n he fracon of owner-occuped housng across counres. owever apar from hese nsuonal facors here are oher reasons why mos households choose o own her home a leas over a par of her lfe cycles. omeownershp gves he occupans full freedom o alor he house o her specfc ases and needs. omeowners also sand o benef from he consequences of sound decsons abou manenance and renovaon. These offer consderable fnancal advanages (See Sweeney 974 for a dscusson of he manenance cos advanages of homeownershp.) The advanages of homeownershp have o be weghed agans he ransacon coss of changng homes; hese coss are ypcally larger for homeowners. ess frequen movers wll be more lkely o prefer homeownershp whereas households wh shorer expeced duraons may be beer off renng. Choosng o own a home s no only a consumpon decson. I also enals a porfolo choce. In fac mos homeowners have srongly unbalanced porfolos. Ths s llusraed n Table based on mcro daa he PSID for he Uned Saes and he IK daabase for Sweden. Despe dfferen nsuonal envronmens he lfe cycle paern s relavely smlar n hese wo counres. In boh counres he average household nvess well above per cen of ne wealh n s home up unl 5 years of age. The age profle appears o be somewha seeper for he U.S. where households below 3 years of age nves more han hree mes her ne wealh n owner-occuped housng. Ths daa se s based on ax reurns for a random sample of Swedsh households. Asse valuaons made for ax purposes are ranslaed no approxmae marke values.

4 Ths wealh composon does no seem o be he oucome of an unresrced porfolo choce. aher suggess ha curren nsuonal arrangemens do no allow an opmal sharng of he rsks assocaed wh homeownershp. There s some economerc evdence o sugges ha he hgh rsks of homeownershp have real consequences. For example sudes by osen e al. (984) and Turner (2) boh conclude ha house prce volaly dscourages homeownershp. Turner also fnds ha hgh-ncome households presumably hose wh smaller nvesmen shares n housng are less sensve o prce volaly. ecenly dfferen proposals have been pu forh o mprove he possbles o pool and share hese rsks. Case Shller and Wess (993) have proposed a marke n fuures conracs ed o regonal house prce ndexes allowng households o hedge by akng shor posons n hese dervaves conracs. Capln e al. (997) have suggesed seng up housng parnershps ha would allow households o share he rsk of ownng he dwellngs n whch hey lve wh oher nvesors. So far neher of hese proposals for hedgng and rsk sharng has me wh much success n pracce. Ths s undoubedly parly due o legal and praccal problems. Seng up housng parnershps would requre new legslaon and he aracveness of a dervaves marke n prce ndex fuures depends on he qualy and negry of he ndexes. These new markes would ake me o develop and despe her mmedae appeal s no clear o wha exen households are adversely affeced by her unbalanced nvesmen porfolos. Ths paper provdes a dealed assessmen of he poenal gans for homeowners from mproved hedgng opporunes. Specfcally we nvesgae he benefs n mean-varance space whch arse from nroducng opporunes o ake posons n a prce ndex for owneroccuped homes. The nex secon of he paper brefly revews avalable evdence on housng reurns n a porfolo conex. Secon III presens he daa ha our analyss draws on and he mehods we use for esmang house prce ndexes and he reurns o nvesng n an owner- 2

5 occuped home. In order o generae long-erm reurns we esmae a VA model. Ths model and he properes of reurns a dfferen horzons are dscussed n secon IV. Furher deals are repored n Appendx B. In secon V we use he varance-covarance srucure of reurns o derve mean-varance effcen porfolos under a seres of condons. We deal wh hree ssues: he opmal allocaon of nvesmen o housng n effcen porfolos unresrced by consumpon moves; he nheren rsk n housng chosen only for consumpon moves; and he poenal for rsk reducon whch could be afforded by nsrumens o hedge housng nvesmens. ouseholds ha hold a large fracon of her porfolos n her own homes ypcally younger and poorer households pay a hgh cos for hs choce n erms of exra rsk. Inroducng a marke n he housng ndex leads o a consderable reducon of hs rsk. II. vdence on housng reurns and opmal porfolo choce mprcal sudes of he quanave mporance of he porfolo-mbalance problem are scarce. xcepons are papers by Goezmann (993) Flavn and Yamasha (998) chholz e al. (2) and Gazlaff (2). 2 Despe usng dfferen mehods o measure he reurns o housng all hree sudes fnd low correlaons beween he reurns o housng and oher asses Goezmann uses repea-sales prce ndexes for four U.S. ces esmaed by Case and Shller (99); Gazlaff uses ndexes for 2 MSAs n Florda esmaed by smlar echnques; Flavn and Yamasha use panel nformaon on he owners own assessmens of house values. The low correlaon beween housng and oher asses suggess ha housng should conrbue o dversfyng he porfolo and lowerng he rsk. Alhough he exac specfcaon vares among hese hree sudes each ndcaes a porfolo share for housng 2 See also Devaney and ayburn (988). 3

6 around ffy per cen for he mnmum varance porfolo. 3 A he rsker end of he effcen froner resuls dffer more across sudes no surprsngly snce hs poron of he froner s much more sensve o esmaon errors (see for example Joron 985). For a sandard porfolo choce problem he holdng perod of he nvesmen s no a major concern. Because mos asse reurns are reasonably well descrbed by random walk processes her varances and covarances over n perods are approxmaely equal o n mes her one-perod counerpars. The soluon o a porfolo-choce problem based on quarerly reurns s hus almos dencal o he soluon based on mul-perod reurns. Despe he recen fndngs of hgh-frequency posve auocorrelaon and long-erm mean reverson n sock prces he random walk assumpon remans a reasonable approxmaon for mos asse reurns. ousng s a major excepon for wo reasons. Frs ndex reurns exhb posve auocorrelaon for many markes; see Case and Shller (989) for U.S. ces and nglund and Ioanndes (996) for nernaonal comparave daa. Second houses are heerogeneous as are he condons of sale. Thus here s a srong dosyncrac componen o he reurn from nvesng n an ndvdual house. The mporance of he dosyncrac componen can be expeced o dmnsh over me n relaon o he prce ndex uncerany. For hs reason and snce ransacon coss are mporan he assumed holdng perod (he nvesmen horzon) may be que mporan n analyzng a porfolo choce problem n whch housng s one of he asses. Goezmann consders he mpac of he holdng perod. e fnds ha he wo aspecs end o have offseng effecs on he rskness of housng. The annualzed sandard devaon of he ndex-based reurn ends o ncrease wh he holdng perod bu he mpac of he dosyncrac componen decreases. On balance accordng o Goezmann s sudy he holdng perod does no appear o be a major concern. 3 Goezmann derves he effcen froner based on four asses all wh non-negavy consrans. Flavn and Yamasha mpose non-negavy consrans on all four asses bu also nclude morgage loans consraned only 4

7 The sudy by chholz e al. (2) focuses on he poenal of bonds and common socks as hedges agans he rsks of homeownershp. Ineresngly hey fnd ha he demand for socks and bonds n an opmal porfolo s no sgnfcanly affeced by homeownershp mplyng ha neher asse provdes a good hedge for housng. Ths suggess ha one has o look owards nsrumens more drecly geared a housng reurns n order o fnd good hedges. III. Daa and Mehods esearch on hs ssue has been hampered by he lack of relable me-seres daa on housng prces and housng reurns. In hs paper we draw upon a body of daa conssng of observaons on all sales of one-famly houses n Sweden from January 98 hrough Augus These daa ha have been used o esmae raher precse quarerly house prce ndexes for egh major Swedsh regons; see nglund e al. (998) and Qugley and edfearn (999). Ths daa seres s much shorer han comparable prce seres ha could be used o esmae sock reurns. To focus on longer-erm reurns hs poses specal problems. We address hose by esmang a vecor auoregresson sysem and we use he esmaed VA model o generae he reurns o housng nvesmen over he longer erm. The daa se on housng ncludes every arm s lengh sale of owner occuped housng n Sweden. Conrac daa reporng he ransacon prce for each sale have been merged wh ax assessmen records conanng dealed nformaon abou he characerscs of each house. epea sales are denfed as s he locaon of each un down o he smalles geographcal un he parsh (akn o a census rac). The daa se s exceponal n s dealed descrpon of each dwellng a he dae of sale and s denfcaon of he panel naure of sales of he same propery. by house value. Gazlaff ncludes commercal real esae and ITs among he asses agan wh non-negavy consrans. 5

8 Assume ha he sale prce of a housng un s he produc of an ndex represenng he level of servces emed by he un and an ndex of prce per qualy un. To represen hs suppose V = P + Q + ω. () where V s he logarhm of he observed sellng prce of house a me Q s he log of he qualy of house sold a me P s he log of he consan qualy housng prce ndex a me and ω s a random error reflecng dosyncrac aspecs of a parcular ransacon e.g. a "dsressed" sale. Accordng o () each house ems a qualy of servce Q ha s prced a P a a parcular pon n me. Q 6

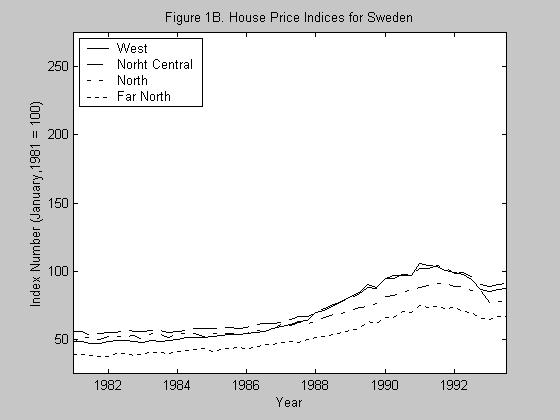

9 We assume ha hs compose erm.e. he dosyncrac error ne of he ndvdual-specfc error s auocorrelaed: ε = ρ τ ε τ + υ (5) where (ξ ) = (ξ 2 ) = ξ 2 (6) (υ ) = (υ 2 ) = υ 2. The panel naure of he daa denfes he key parameers: he prce ndex P he auoregressve erm ρ and he error varances. The mehods of esmang hese parameers are dscussed n nglund e al. (998). Appendx Table A repors he coeffcen esmaes of he prce seres and sandard errors for egh regons n Sweden. The prce ndces are very precsely esmaed. The ndexes are esmaed monhly and aggregaed o quarer year nervals n our analyss. The esmaed prce ndexes for all he egh regons denfed n Appendx Table A. are depced n Fgure. As he dagrams ndcae he course of housng reurns across he dfferen regons of Sweden durng hs perod has been farly well synchronzed. Prces were sagnan n nomnal unl 985 when hey sared o ncrease. ouse prces reached a peak n 99 followed by a sharp drop as a major fnancal crss h Sweden durng he early 99s. Sockholm has he hghes and mos volale housng prces. The reurn from nvesng n an owner-occuped home consss of hree componens: he rae of change of he housng prce ndex P he renal value of he servce flow generaed by he housng un (ne of operang coss and deprecaon) and he rae of change of he dosyncrac componen of he house prce. We mpue a renal value usng he ndex of rens for resdenal aparmens n each regon.e. we assume he aparmen ndex o be vald for 7

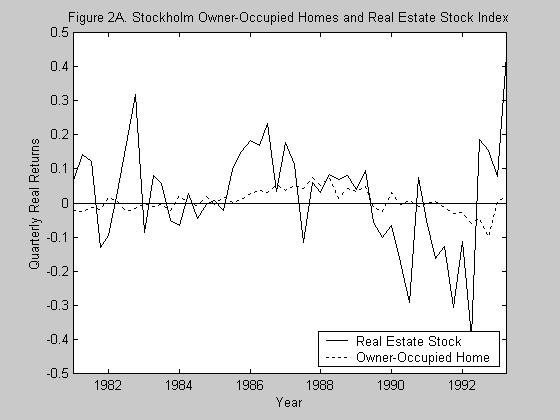

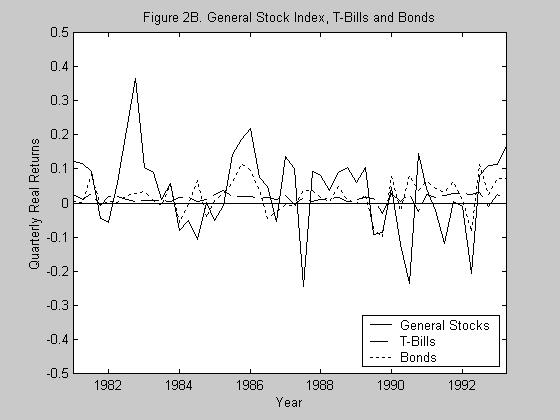

10 one-famly houses as well. 4 We se he ren n he frs quarer of 98 a per cen of house value. Ths follows he wdely used one-n-one-hundred rule. 5 Ths gves us wo reurn seres. The housng ndex reurn r s gven by r = P P - +. P (7) And he reurn on an ndvdual housng un r h by r h = r + ε - ε -. (8) ousng reurns are hghly correlaed across all egh regons ndcang ha here are only small dversfcaon benefs from holdng a mul-regonal housng porfolo whn he counry. Ths conrass wh he Uned Saes where he benefs from regonal dversfcaon are consderable; see Goezmann (993). For hs reason we lm ourselves o ncludng he Sockholm housng marke n he porfolo analyss. Fgure 2A depcs he emporal paern of he real quarerly reurn on Sockholm housng defned accordng o (7) as he weghed change n he monhly prce ndex (see Appendx Table A) aggregaed o quarers plus he quarerly renal servce sream mnus he change n CPI. Followng Goezmann (993) we nclude general socks (he AFGX ndex produced by a leadng busness perodcal) fve-year bonds and hree-monh reasury blls among he nvesmen alernaves. In order o hghlgh he opporunes for hedgng usng currenly raded nsrumens we also nclude an ndex for real esae corporaons raded on he Sockholm sock exchange. Ths ndex covers a group of companes whose man source of ncome comes from real esae holdngs (offce and resdenal). To varyng degrees hey also have oher lnes of busness prmarly n consrucon. In he absence of ITs hs s he 4 Ths s he only conssen ren seres avalable and s based upon comprehensve daa. owever use of hs ndex s problemac snce aparmen rens are regulaed wh he objecve of followng producon coss. Our use of hs ndex probably leads o an underesmae of he shor-erm varaon n he value of renal servces. owever he varaon n rens should n any case be small relave o he varaon n he value of he sock so hs s probably no very serous. 5 See Kan and Qugley 975 for an early saemen. 8

11 mos naural vehcle for nvesng n real esae for a Swedsh nvesor. Fgures 2A and 2B repor he real reurns on hese asses whch could be used o form an nvesmen porfolo. The daa cover a dramac perod n Swedsh economc hsory. 6 The 98s was a decade of major asse revaluaons as seen by he hgh reurns o socks hroughou he decade and o homes durng he second half of he decade. Durng he 98s he Sockholm sock exchange ouperformed all major sock markes n ndusralzed counres. The developmen of asse prces can be explaned by he deregulaon of cred markes around 985 and by an expansonary fscal polcy. eurns o fxed-ncome nsrumens were also exraordnary. Snce he pary of he krona was mananed a a fxed level afer a devaluaon n 982 despe he fac ha nflaon was hgher n Sweden han abroad he currency had o be defended by hgh neres raes. The early 99s saw an end o he asse-prce boom wh a sharp drop n prces parcularly for real esae n 99 and 992. Ths was assocaed wh a bankng crss wh oal cred losses beween 99 and 993 on he order of 2 per cen of one year s GDP. A general economc crss perssed and GDP fell for hree consecuve years. In he fall of 992 he Swedsh krona was allowed o floa resulng n a deprecaon by weny per cen by he end of he year. From 994 he Swedsh economy sared o recover. The recovery perod s no par of our daa however. IV. Invesmen eurns Snce mos households ake a long erm perspecve on her home nvesmen s mporan o analyze he reurns o housng over dfferen nvesmen horzons. Bu wh only 3 years of daa we canno observe long-horzon varances and covarances drecly. To crcumven hs problem we assume ha reurns are generaed from a fourh order vecor 6 See nglund (999) for an accoun of he evens leadng up o he bankng crss. 9

12 auoregresson sysem on a quarerly bass n he fve asse reurns and we esmae he parameers of hs sysem by he mehod of seemngly unrelaed regressons. Once he parameers for he VA sysem are esmaed s farly sraghforward o compue momens over long horzons; see Appendx B for deals. The esmaed model s presened n Appendx Table B. The model explans much of he varaon n housng reurns ( 2 adj =.72) bu as expeced works less well for fnancal asses. Tess for Granger-causaly fal o rejec he null hypohess of no causaly. xcepons are he reurns o bonds and houses; boh are predced by sock reurns he general ndex as well as he real esae sock ndex. Ineresngly hgh reurns o real esae socks predc hgh housng reurns whle hgh general sock reurns predc low housng reurns. Closely relaed fndngs ha he reurns o securzed real esae help predc he reurns o drec nvesmen n ndvdual properes have been repored for commercal real esae. See Barkham and Gelner (995). The frs wo momens of nvesmen reurns a dfferen horzons based on he esmaed VA parameers are presened n Tables 2 and 3. As noed n Table 2 expeced real reurns are generally que hgh rangng from.3 per cen per quarer for -blls and homes o 3.7 per cen for he general sock ndex reflecng he srong performance of Swedsh asse prces dscussed above. The lower panel of Table 2 dsplays varances a dfferen horzons. To manan comparably he able presens long-horzon varances on a per quarer bass.e. he varance of n-quarer reurns dvded by n. In erms of varance housng reurns are consderably rsker han nomnal asses bu are less rsky han socks. eal esae socks have 2-4 mes he varance of socks n general. In comparng he dfferen horzons we noe ha he en quarer horzon dsplays hgher varances for all asses han any oher horzons. Generally varances are lower a he 4-quarer han a he one-quarer horzon; he housng ndex s he only excepon.

13 For housng we dsngush beween ndex reurns and he reurns o an ndvdual house as defned n (7) and (8). We noe ha he dfference s szeable for shor holdng perods. A he one-perod horzon he varance of he housng ndex reurn equals ha of bonds whereas he varance of he reurn o an ndvdual home s sx mes as large. A longer horzons s less han wce as large. Ye even a he 4-quarer horzon he ndvdual home s a relavely rsky nvesmen wh a varance half ha of common socks and egh mes ha of bonds. Table 3 repors smple correlaon coeffcens beween he nvesmen vehcles for he dfferen me horzons. The reurns o housng are posvely correlaed wh real-esae socks and negavely correlaed wh -blls and bonds. All correlaons wh housng are sronger a longer horzons. The correlaon wh he general sock ndex s close o zero. Our resuls may be compared wh hose of Goezmann (993) and Gazlaff (2) boh of whch apply o one-year horzons. ach of hese sudes fnds a negave correlaon beween housng and bond reurns (-.54 and -.23) a small correlaon wh -blls (-.22 and +.9) and a small negave correlaon wh he S&P 5 sock ndex. Only Gazlaff consders securzed real esae surprsngly fndng a negave correlaon (-.3). Our resuls confrm he general concluson from hese sudes ha he correlaons beween housng and oher key asses are suffcenly low as o make housng a poenally aracve addon o a porfolo a leas a lower rsk levels. Wheher hs warrans he observed porfolo shares of a hundred per cen or more s an ssue dscussed n he nex secon. V. Opmal Porfolos We now use he srucure of hs nformaon o consruc mean-varance effcen porfolos. We focus on hree ses of ssues: he opmal allocaon of nvesmen o housng n

14 effcen porfolos unresrced by consumpon moves; he nheren rsk n housng chosen only for consumpon moves; and he poenal for rsk reducon whch could be afforded by nsrumens o hedge housng nvesmens. V.. Unresrced Porfolos We sar by consderng a benchmark where he amoun of housng s chosen freely by mean-varance opmzaon. We analyze wo cases; boh nclude he four fnancal asses wh housng represened eher by a sngle house or by he housng ndex (Table 4 and 5 and Fgure 3). Porfolo shares excep for a sngle house are only resrced o be beween plus and mnus 5 per cen. The share of a snge house s resrced o be non-negave reflecng he fac ha s dffcul n pracce o shor-sell ndvdual houses. The benchmark cases are no nended o capure real lfe nvesmen opporunes bu raher o brng ou he mplcaons of he reurn paerns n he daa for porfolo choce. We llusrae he soluons o hs problem for wo horzons one quarer and 4 quarers. 7 From Table 4 we see ha he opmal porfolo share n an ndvdual house s close o zero n he mnmum-varance porfolo a boh horzons. Movng ou along he froner ncreases a frs for he onequarer horzon only modesly o a mos 5 per cen bu for he longer horzon more sharply o more han per cen. Wh furher ncreased rsk he opmal porfolo share n an ndvdual house decreases o become zero a hgh rsk levels. The mnmum varance porfolo nvess more han a hundred per cen n -blls and borrows n bonds bu a hgher rsk levels hs s reversed wh borrowng n blls and nvesmen n bonds and shares. eal esae socks are generally unaracve excep far ou on he effcen froner. 7 Snce he correlaon srucures are no very dfferen beween he 2 and 4 quarer horzons he opmal porfolos are also que smlar. 2

15 The resuls of he same exercse assumng ha he nvesor can nves n he housng ndex bu no n an ndvdual house 8 are dsplayed n Table 5. Ths case can be hough of as applyng o a rener household f an ndex marke were avalable. Snce he housng ndex offers a lower varance bu he same expeced reurn as a sngle house comes as no surprse ha he housng ndex porfolo shares n Table 5 are conssenly larger han he correspondng housng shares n Table 4 excep when non-negavy resrcons on a sngle house becomes bndng. In fac he housng ndex shares are que large. For he 4 and one quarer horzons he porfolo shares sar a 9 and 5 per cen for he mnmum varance porfolos and peak a close o and 2 per cen respecvely. Ths suggess ha access o a housng ndex should prove aracve for a rener household. Oher feaures of he effcen froners are much he same as n Table 4. Fgure 3 compares he effcen nvesmen froners when households can nves n fnancal nsrumens and a house wh he froner when hey can nves n fnancal nsrumens and a housng ndex. The gans from an ndex a hgher levels of rsk are apparen. We have also compued opmal porfolo shares mposng non-negavy resrcons on socks bu no on bonds and -blls. Ths reflecs he fac ha shor-sellng s dffcul n pracce whle shor posons n nomnal nsrumens may be nerpreed as borrowng. The general paern of opmal porfolo holdngs (see Table 6) along he effcen froner s roughly he same under hese assumpons. Wh ncreasng rsk he housng fracon goes from close o zero over posve values (peakng a around 4 percen) o zero a he hgh-rsk end of he froner. 8 The case of an unresrced porfolo wh all sx asses e ncludng boh housng ndex and an ndvdual house s unneresng. The opmal nvesmen n an ndvdual house wll always be zero unless he poson n he ndex s resrced by a consran (n our case +/- 5 per cen). 3

16 V.2. ousng Consumpon Choce and sk ouseholds do no make her housng choces purely from an nvesmen perspecve. Under curren nsuonal arrangemens s no feasble o dsenangle he consumpon and nvesmen aspecs of housng choces. Takng he consumpon choce as exogenous we now analyze a he opmal porfolo composon condonal on gven fracons of wealh nvesed n housng. 9 We do hs for four dfferen cases: "rch" homeowners for whom we assume he housng share s per cen of ne wealh; "average" homeowners (housng share = 2 per cen); "poor" homeowners (housng share = 4 per cen); and reners (housng share = ). These porfolo shares span he average shares repored n Table for households of dfferen ages. ow large s he loss n mean-varance erms arbuable o hese resrcons relave o a fully effcen porfolo? The answer o hs queson s repored n Fgures 4A and 4B whch depc mean-varance effcen froners for holdng perods of 4 quarers and one quarer calculaed under he assumpon ha shor sellng of socks s no possble bu negave posons n bonds and -blls are. eners experence almos no losses relave o he unresrced porfolo; effcen froners of boh classes are almos dencal for all dfferen horzons. For he hree homeowner caegores reurn losses ge larger wh ncreasng porfolo shares n housng. Ths s evden from he dfferences n mnmum varance aanable. A he 4-quarer horzon he mnmum sandard devaon s less han. percen for he rener porfolo compared o and 36.7 per cen for he hree homeowner porfolos. A he onequarer horzon he correspondng mnmum varances are even farher apar: and 45. per cen respecvely. A par of hese dfferences s compensaed for by hgher expeced reurns. Comparng a he same sandard devaon (47 per cen) a one quarer 9 Of course he fac ha a large housng consumpon leads o an unbalanced nvesmen porfolo mples an addonal cos o housng consumpon whch should be aken no accoun when choosng housng 4

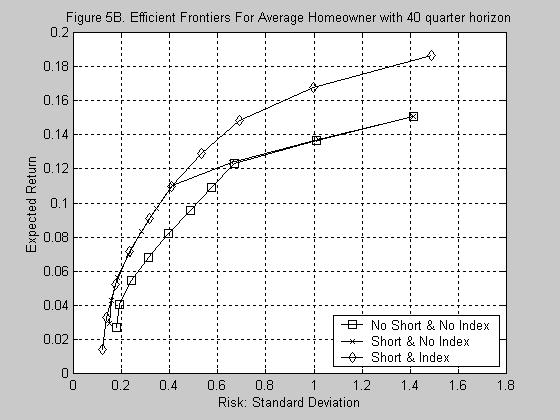

17 horzon he loss n expeced reurn relave o he unresrced porfolo s modes less han.3 per cen for a rch owner bu very large (6.3 per cen) for a poor owner. Table 7 represens he correspondng porfolo composons for reners and poor homeowners. The rener nvess more han hundred per cen n -blls fnanced by borrowng n bonds a he mnmum-varance end of he froner. owever wh ncreasng rsk olerance he rener reverses posons beween -blls and bonds; she borrows n -blls and nvess n bonds and socks. The share of socks s larger n rsker porfolos whle he share of bonds s larger n less-rsky porfolos. Only far ou on he froner do we see any nvesmen n real esae socks. These general paerns hold a all horzons. For he poor homeowner n conras he mnmum varance porfolo s a corner soluon wh maxmum shor-erm borrowng fnancng he house and an nvesmen n bonds. As n case of he rener wh ncreasng rsk he poor homeowner gradually rases he share of socks by borrowng n bonds. V.3. edgng housng rsk ow consder he opporunes for hedgng. Among currenly avalable nsrumens he mos obvous hedgng opporuny would be shor sales of securzed real esae: shorng real esae socks. In hs secon we frs explore he gans ha he real esae socks afford. We hen consder he exra benefs from allowng posons n he housng ndex. We llusrae he hedgng gans for he four household ypes n fgures 5A hrough D for a 4-quarer horzon. ach panel graphs hree effcen froners one allowng neher hedgng opporuny one allowng shor sales n real-esae and oher socks and one allowng boh shor sales n socks and posons n he housng ndex. The correspondng porfolos for he poor homeowner are gven n Table 8. consumpon. Brueckner (997) analyzes he complee choce problem when porfolo and consumpon aspecs 5

18 Fgure 5 shows he gans ha real esae socks and he housng ndex can respecvely brng o homeowners. Sarng from porfolos ha allow neher shor-sellng of real-esae socks nor radng n he housng ndex we see ha he wo froners dverge for less-rsky porfolos bu converge for rsker porfolos. Comparng he wo effcen froners wh shor posons allowed for real esae socks bu wh and whou access o he housng ndex we noe ha he froners sar very close a he mnmum varance porfolos bu dverge subsanally for rsker porfolos. The housng ndex brngs exra benefs o homeowners even afer real esae socks are used as a hedge. Imporanly whle real esae socks end o benef more rsk averse homeowners he housng ndex can brng subsanal gans o less rsk averse homeowners n erms of reducng rsk for her rsker porfolos. The porfolo composons n Table 8 shows ha when an ndex s avalable real esae socks ndex and -blls are used o fnance long posons n general socks and bonds excep for hgh rsk porfolos. A hgh rsks even bonds are held n shor posons leavng only general socks n long posons. The role of real esae socks as a hedge s explaned by he hgh varance and low expeced reurn of real esae socks (relave o oher socks) and by he relavely srong posve correlaon beween real esae socks and houses. The correlaon coeffcen s around.4 a longer horzons. When housng nvesmen s subopmally large from a porfolo perspecve as s n hese homeowner porfolos nvesmen shares n real esae socks become generally smaller (and shor posons are larger). The fgures llusrae he resulng gans from shor posons n real esae socks n mean-varance erms. For poor homeowners he gans are que large ndeed. A he 4- quarer horzon he sandard devaon of he mnmum varance porfolo s reduced from 36.7 o 3.6 per cen whle he expeced reurn s ncreased from 2.3 o 4. per cen. A he one-quarer horzon gans are much smaller. The varance of he mnmum varance porfolo are reaed smulaneously. See also eaon and ucas (2) 6

19 for a poor homeowner s reduced from 45. whou shor sellng of socks o 44.3 per cen wh shor sellng whle he ncrease n expeced reurn s merely.2 per cen from.5 o.7. The usefulness of real esae socks as a hedge s lmed by he relavely low correlaon wh housng reurns. The housng prce ndex n conras has a sronger correlaon wh reurns from a sngle house rangng from.42 a he shores horzon o.77 a longer horzons. Allowng posons n he ndex has a dramac mpac on he composon of he mnmum varance porfolos for he poor homeowners. When a poson n he housng ndex s allowed he resuls n Table 8 ndcae ha here s a large negave poson (39 per cen) n ha ndex a posve poson n -blls and posons close o zero n oher nsrumens. To mnmze rsk housng should be fnanced almos exclusvely by gong shor n he housng ndex. Compared o he case when a housng ndex s no avalable here s some reducon n he mnmum varance porfolo a he one-quarer horzon from 44.3 per cen o 4.7 per cen (and a he 4-quarer horzon from 3.7 o 24. per cen). Ths safey comes a he expense of a sharp drop n expeced reurns however. To accoun for hs we may compare he expeced reurns a he mnmum varances achevable whou he housng ndex wh hose wh he housng ndex avalable. The reurn ncreases from 4. o 6.9 per cen a he 4-quarer horzon and from.7 per cen o 5. per cen a he one-quarer horzon. These resuls ndcae clearly ha here s subsanal scope for welfare mprovemen by allowng rade n more drec hedgng nsrumens such as home prce ndex fuures. We have also seen ha he ndex appears n posve amouns n he effcen porfolos for reners. eners as well as nsuonal nvesors would seem o be he naural marke counerpars of owners. Wh boh a supply sde and a demand sde he basc requremens for a marke are fulflled. 7

20 VI. Concluson We have used an unusually rch source of daa on housng prces n Sockholm o analyze he nvesmen mplcaons of housng choces. Our emprcal analyss derves marke-wde prce and reurn seres for housng nvesmen durng a 3 year perod and also provdes esmaes of he ndvdual specfc dosyncrac varaon n housng reurns. Because ndex changes and he dosyncrac componen follow auocorrelaed processes he analyss of porfolo choce s dependen upon he holdng perod specfed. We analyze he composon of household nvesmen porfolos conanng housng common socks socks n real esae holdng companes bonds and -blls. For shor holdng perods he effcen porfolo conans essenally no housng. For longer perods low rsk porfolos conan 5 o 5 percen housng. These resuls sugges ha here are large poenal gans from polces or nsuons ha would perm households o hedge her lumpy nvesmens n housng. We esmae he poenal value of hedges n reducng rsk for he same nvesmen reurns. The value s surprsngly large especally for poorer homeowners. Ths s he frs sysemac evdence on he opc. Gven he ways n whch daa on house sales are colleced cenrally n Sweden would seem ha one could develop a ransparen and relable prce ndex ha should be useful for radng n hese dervaves. Ths marke would perm households o hedge her mos mporan nvesmen and o dversfy her curren rsks n owner-occuped housng. Currenly hese rsks are que large especally for young households. Our analyss suggess ha fnancal nsrumens could reduce hese rsks que consderably. 8

21 eferences Barkham chard and Davd Gelner Prce Dscovery n Amercan and Brsh Propery Markes eal sae conomcs 23() 995: Brueckner Jan Consumpon and Invesmen Moves and he Porfolo Choces of omeowners Journal of eal sae Fnance and conomcs 5 997: Capln Andrew e al. ousng Parnershps Cambrdge MA: MIT Press 997. Case Karl. and ober J. Shller "The ffcency of he Marke for Sngle-Famly omes" Amercan conomc evew 79() 989: Case Karl. and ober J. Shller Forecasng Prces and xcess eurns n he ousng Marke AUA Journal 8(3) 99: Case Karl. ober J. Shller and Allan. Wess "Index-Based Fuures and Opons Markes n eal sae" Journal of Porfolo Managemen 9(2) 993: Devaney Mchael and Wllam ayburn When a ouse s More Than a ome: Performance of he ousehold Porfolo Journal of eal sae esearch Sprng 988. dn Per-Anders Peer nglund and rk kman Avreglerngen och hushållens skulder (Deregulaon and ousehold Deb) n Bankerna under krsen Bankkrskommén Sockholm 995. chholz Pe M.A. Kees G. Koedjk and Frans A. de oon The Porfolo Implcaon of ome Ownershp manuscrp Maasrch Unversy 2. nglund Peer The Swedsh Bankng Crss: oos and Consequences Oxford evew of conomc Polcy 5(3) 999: nglund Peer John M. Qugley and Chrsan. edfearn "Improved Prce Indexes For eal sae: Measurng he Course of Swedsh ousng Prces Journal of Urban conomcs 44(2) 998: nglund Peer and Yanns M. Ioanndes "ouse Prce Dynamcs. An Inernaonal mprcal Perspecve Journal of ousng conomcs 6 996: Flavn Marjore and Takash Yamasha "Owner-Occuped ousng and he Composon of he ousehold Porfolo Owner he fe Cycle" Workng Paper #6389 aonal Bureau of conomc esearch January 998. Gazlaff Dean. The ffec of Sngle-Famly ousng on Mul-Asse Porfolo Allocaons unpublshed manuscrp 2. Goezmann Wllam elson "The Sngle Famly ome n he Invesmen Porfolo" Journal of eal sae Fnance and conomcs 6(3) 993:

22 amlon James D. Tme Seres Analyss Prnceon J: Prnceon Unversy Press 994. eaon John and Deborah ucas Porfolo Choce n he Presence of Background sk conomc Journal Joron Phlppe Inernaonal Porfolo Dversfcaon wh Porfolo sk Journal of Busness 58(3) 985: Kan John F. and John Qugley ousng Markes and acal Dscrmnaon ew York Y: Columba Unversy Press 975. Qugley John M. and Chrsan. edfearn "ousng Marke ffcency and he Opporunes for xcess eurns" Paper prepared for he aonal Bureau of conomc esearch Conference on eal sae Cambrdge MA ovember 999. osen arvey S. Kenneh T. osen and Douglas olz-akn ousng Tenure Uncerany and Taxaon evew of conomcs and Sascs : Sweeney James. "ousng Un Manenance and he Modes of Tenure" Journal of conomc Theory 8 974: -38. Turner Tracy M. Does Invesmen sk Affec he ousng Decsons of Famles? manuscrp UC Davs 2. 2

23 Table fe-cycle ousng Invesmen. Mean house value as a per cen of mean ne wealh by age caegory Age of household head Uned Saes 989 Sweden (25-34) (35-44) (45-54) (55-64) (65-74) (75 +) Sources: Flavn and Yamasha (998) Table 2 and dn e al. (995) Table 8b. oe: Age nervals n parenhess refer o Sweden. Table 2 Means and Varances of eal Quarerly Asse eurns.. Socks Gen. Socks T-Blls Bonds. Index ouses xpeced eurns Varances orzon quarer quarers quarers quarers oe: eurns are generaed from he VA model of Appendx Table B. For comparably varances are expressed n quarerly erms by dvdng by he number of quarers. 2

24 Table 3 Correlaon Coeffcens Among Asse eurns a Dfferen Tme orzons Tme orzon.. Socks Gen. Socks T-Blls Bond. Index ouses quarer.. Socks quarers quarers quarers quarer Gen. Socks quarers quarers quarers quarer T-blls quarers quarers quarers quarer Bonds quarers quarers quarers ousng ndex quarer.499 quarers quarers quarers

25 Sandard Devaon Table 4 Opmal Unresrced Porfolos. Four Fnancal Insrumens and a ouse. xpeced eurns.. Socks Gen. Socks T-Bll Bond ouse 4-quarer horzon One-quarer horzon Table 5 Opmal Unresrced Porfolos. Four Fnancal Insrumens and he ousng Index. Sandard Devaon xpeced eurns.. Socks Gen. Socks T-Bll Bond. Index 4-quarer horzon One-quarer horzon

26 Sandard Devaon Table 6 Opmal Porfolos. Four Fnancal Insrumens and a ouse. xpeced eurns o Shor Sellng of Socks... Socks Gen. Socks T-Bll Bond ouse 4-quarer horzon One-quarer horzon

27 Table 7 Opmal Porfolos. o Shor Sellng. o Index. Sandard Devaon xpeced eurns Panel A. eners (ousng = ).. Socks Gen. Socks T-Bll Bond ouse 4-quarer horzon One-quarer horzon Sandard Devaon xpeced eurns Panel B. Poor omeowners (ousng = 4).. Socks Gen. Socks T-Bll Bond ouse 4-quarer horzon One-quarer horzon

28 Sandard Devaon xpeced eurns Table 8 Opmal Porfolos for Poor omeowners (ousng = 4) wh Shor Sellng and he ousng Index Panel A. 4 Quarer orzon.. Socks Gen. Socks T-Bll Bond Index ouse Shor sellng no ndex Shor sellng and ndex Sandard Devaon xpeced eurns Panel B. One Quarer orzon.. Socks Gen. Socks T-Bll Bond Index ouse Shor sellng no ndex Shor sellng and ndex

29 27

30 28

31 29

32 3

33 3

34 32

35 Appendx Table A. Monhly smaes of egonal Prce Changes for Sweden January 98 =. (nres are he logarhms of esmaed prce ncrease durng each monh) -raos n parenheses Year/Monh egon Sockholm as Cenral Souh Cenral Souh Wes orh Cenral orh Far orh 98: Feb (2.34) (.29) (.8) (.8) (.2) (.34) (.) (.25) (2.54) (.6) (.77) (.28) (2.2) (.82) (.6) (.77) (.66) (.) (.3) (.8) (.9) (.3) (2.3) (.52) (.22) (.26) (.8) (.79) (.69) (.44) (.72) (.3) (.45) (.) (.32) (.32) (.52) (.47) (.33) (.9) (.42) (.23) (.59) (.99) (.36) (.82) (.4) (.5) (.2) (.) (.63) (.45) (.57) (.99) (.4) (.6) (.8) (.77) (.9) (.6) (.4) (.4) (.) (.36) (.67) (2.54) (2.69) (.3) (.) (2.9) (.3) (.59) (.3) (.83) (2.44) (.83) (.) (.99) (.8) (.55) (.3) (2.4) (2.8) (2.8) (.8) (.2) (2.4) (.7) 982: Jan (2.2) (2.3) (5.35) (.7) (2.69) (.33) (.2) (.98) (.99) (.73) (.95) (.3) (.77) (.6) (.2) (.38) (.25) (.66) (.3) (.27) (2.9) (.89) (.) (.44) (.5) (.23) (.76) (2.) (.57) (.89) (.77) (.7) (.56) (.67) (2.65) (.23) (.6) (.79) (.4) (.) (.5) (.54) (.79) (.5) (.47) (.36) (.76) (.5) (.27) (.3) (2.73) (.42) (.6) (.4) (.62) (.37) (.47) (.63) (.59) (.4) (.6) (.74) (.45) (.58) (.9) (.23) (.87) (.3) (.5) (.75) (.59) (.6) (.6) (2.) (.5) (.22) (.26) (.65) (.57) (.5) (2.) (.94) (.74) (.87) (.9) (.8) (.83) (.6) (.22) (.7) (.89) (.25) (.89) (.9) (.9) (.59) 983: Jan (.6) (2.6) (.) (2.27) (.7) (.26) (.64) (.9) 33

36 (.5) (.2) (.65) (2.3) (.8) (.9) (.8) (.2) (.9) (.5) (.6) (2.5) (.6) (.3) (.) (.69) (2.64) (.85) (.26) (.4) (.96) (.85) (.9) (.37) (3.4) (.69) (.7) (.27) (.39) (.5) (.59) (.49) (.38) (.8) (.99) (.86) (.2) (.59) (.63) (.5) (.58) (.3) (.29) (2.43) (.64) (.9) (.55) (.43) (.5) (.87) (.8) (.3) (.5) (.6) (.25) (.9) (.2) (.28) (.3) (.52) (.93) (.3) (.9) (.7) (.82) (.75) (.) (.24) (.26) (.79) (.78) (.29) (.8) (.3) (.97) (.34) (.38) (.6) (.37) (.9) (.5) (.5) (.33) (.49) (.79) (.44) (.2) (.9) 984: Jan (.32) (.67) (.2) (.4) (.74) (.4) (.62) (.87) (.9) (.4) (.49) (.79) (.3) (.26) (.89) (.2) (.2) (.96) (.25) (.8) (.9) (.8) (.9) (.63) (.36) (.45) (.9) (.5) (.42) (.6) (.77) (.67) (.9) (.8) (.8) (.62) (.52) (.39) (.33) (.54) (.32) (.84) (.4) (.38) (.3) (.77) (.87) (.73) (.25) (.89) (.8) (2.9) (.2) (.8) (.95) (.2) (.87) (.66) (.5) (.42) (.) (.64) (.54) (-.) (.6) (.36) (.27) (.47) (.68) (2.5) (.3) (.42) (.7) (.25) (.6) (.9) (.7) (.3) (.2) (.68) (.2) (.4) (.58) (.42) (.47) (.32) (.54) (.82) (2.57) (.46) (.2) (.85) (.83) (2.3) (.9) (.67) 985: Jan (.9) (.5) (.64) (.82) (.25) (.2) (.26) (.24) (.2) (.39) (.98) (.33) (.2) (.72) (.26) (.9) (.73) (2.8) (.66) (.62) (.6) (.3) (.4) (.7) (.85) (.2) (.34) (.97) (.23) (.4) (.57) (.7) (.92) (.4) (.37) (.2) (.6) (.4) (.39) (.7) (.3) (.26) (.87) (.3) (.) (.57) (.6) (.9) (.33) (.33) (.53) (.6) (.) (-.) (.68) (.57) 34

37 (.6) (.8) (.36) (.27) (.65) (.25) (.76) (.47) (.32) (.66) (.8) (.5) (.7) (.7) (.73) (.97) (.25) (.69) (.6) (.67) (.36) (.5) (.67) (.34) (.9) (.26) (.62) (.24) (.97) (.28) (.74) (.8) (.24) (.34) (.49) (.6) (.5) (.37) (.6) (.79) 986: Jan (.35) (.5) (.33) (.22) (.33) (.95) (.43) (.48) (2.) (.79) (.7) (.24) (.5) (.5) (.9) (.48) (.5) (.37) (.3) (.46) (.7) (.58) (.4) (.8) (.62) (.47) (.38) (.4) (.8) (.6) (.55) (.92) (.2) (2.) (.96) (.) (2.28) (.2) (.22) (.2) (.65) (.6) (.5) (.8) (.2) (.48) (.92) (.24) (.3) (.69) (.38) (.32) (.53) (.5) (.2) (.42) (.34) (.7) (.32) (.5) (.6) (.4) (.5) (.52) (.98) (.9) (.5) (.) (.43) (.47) (.) (.24) (.23) (.9) (.25) (.4) (2.3) (.57) (.3) (.35) (.3) (.4) (.93) (.78) (.6) (.2) (2.4) (.7) (.54) (2.8) (.2) (.4) (.48) (.3) (.) (.7) 987: Jan (3.23) (.63) (.64) (2.63) (.) (.23) (.76) (.8) (2.35) (.4) (.4) (.58) (.7) (.8) (.3) (.74) (.5) (.93) (.) (.43) (.25) (.8) (.22) (.3) (.65) (.7) (.24) (.62) (.84) (.66) (.89) (.88) (.67) (.35) (.2) (.2) (.84) (2.82) (.33) (2.3) (2.7) (.8) (.9) (.7) (.59) (.84) (.3) (.34) (.54) (.5) (2.4) (.63) (.59) (.38) (.69) (.92) (.44) (.52) (.44) (.56) (.98) (.4) (.3) (.6) (.76) (.22) (.92) (.22) (.47) (.73) (.63) (.54) (.) (.82) (.84) (.6) (.6) (.3) (.65) (.52) (2.2) (-.) (.68) (.76) (.6) (.48) (.8) (.8) (.24) (2.49) (.9) (.2) (.32) (.86) (.7) (.93) 988: Jan (.79) (.5) (.54) (.3) (5.68) (.9) (.34) (.88) 35

38 (.4) (.45) (.79) (3.5) (3.93) (.48) (2.4) (.3) (.8) (.36) (.27) (4.5) (2.93) (.69) (.29) (.5) (.54) (.6) (.2) (.4) (.) (-.) (.4) (.4) (.7) (.34) (2.) (.5) (2.48) (.24) (.29) (.74) (2.26) (.89) (.28) (.8) (.32) (3.6) (.93) (.32) (.24) (2.92) (.34) (.5) (.) (.7) (.39) (.2) (.) (.93) (.27) (.98) (.58) (.98) (.7) (.) (.) (.56) (.2) (.56) (.48) (.8) (.8) (.93) (.49) (.6) (.76) (.5) (.47) (.6) (.32) (.3) (.59) (.6) (.34) (.26) (.93) (.5) (.73) (.8) (.34) (3.43) (.) (2.6) (.25) (.83) (.7) (2.59) 989: Jan (.8) (.87) (.96) (2.8) (.26) (2.2) (.6) (.57) (.) (.29) (.69) (.54) (.8) (.2) (.84) (.2) (.58) (.69) (.3) (.7) (2.32) (.3) (.6) (.55) (.62) (2.4) (3.) (.93) (.6) (.2) (.34) (.3) (.) (.33) (.42) (.4) (.53) (.46) (.8) (.94) (.32) (2.73) (.65) (.93) (2.33) (.59) (.9) (.36) (.92) (.7) (.9) (3.9) (.93) (2.2) (.4) (.39) (.6) (.44) (.28) (3.2) (.62) (.4) (.63) (.34) (.38) (.5) (.) (2.66) (3.49) (.68) (.68) (.6) (.62) (.2) (.98) (.62) (3.43) (.6) (.32) (.58) (.67) (.25) (.24) (.8) (.66) (.34) (.65) (.37) (.38) (.66) (.93) (.7) (.2) (.97) (.4) (-.) 99: Jan (3.64) (3.9) (3.65) (.28) (5.28) (2.49) (2.5) (2.27) (.89) (2.6) (.89) (.37) (3.68) (.5) (.53) (.77) (.39) (2.3) (.47) (.73) (.88) (.53) (.49) (.74) (2.78) (.6) (.9) (.7) (.25) (.4) (.2) (.44) (.88) (.45) (.83) (.6) (.9) (.7) (.52) (.24) (.36) (.7) (.26) (3.92) (.6) (2.5) (.45) (.5) (.64) (.93) (.22) (.87) (2.8) (.8) (.6) (2.47) 36

39 (2.76) (.56) (.45) (.55) (.5) (.9) (.23) (.25) (.63) (.22) (.5) (.23) (.95) (.79) (.47) (.8) (.9) (.3) (.79) (.9) (.) (.89) (.5) (.8) (.38) (.9) (.59) (.38) (.53) (.54) (.5) (.44) (.9) (4.23) (.3) (.35) (.52) (2.45) (.5) (.7) 99: Jan (4.6) (.9) (3.65) (3.79) (6.2) (.2) (.26) (2.23) (2.7) (3.95) (.59) (4.5) (5.42) (.52) (.33) (2.7) (.32) (.93) (.4) (.7) (.84) (.37) (.6) (.56) (3.7) (.76) (.45) (.38) (.37) (.9) (.93) (.46) (.8) (2.9) (.69) (.47) (.2) (.38) (.8) (.24) (.7) (.85) (.7) (.45) (.62) (.35) (.8) (.36) (.92) (.68) (.3) (.25) (.) (.5) (.28) (.37) (.9) (.) (.5) (.6) (.9) (.44) (.3) (.37) (.48) (.68) (.2) (.37) (.3) (.22) (.47) (.29) (.52) (.43) (2.77) (.88) (.26) (.25) (.97) (.6) (.58) (.53) (.22) (.9) (.62) (.36) (3.29) (.65) (.4) (.85) (.22) (3.57) (2.66) (.95) (.8) (.56) 992: Jan (2.49) (.6) (.93) (3.3) (2.22) (.7) (.72) (.2) (.98) (.2) (.5) (.79) (.9) (.84) (2.29) (.6) (.2) (.44) (.47) (.4) (.49) (.5) (.54) (.55) (.9) (.26) (.3) (.) (.43) (2.3) (.79) (.3) (.94) (.36) (.68) (.4) (.44) (.5) (.49) (.54) (.93) (.) (.7) (.7) (.77) (.8) (.29) (.54) (.5) (.4) (.) (.68) (.8) (.29) (.99) (.36) (.85) (.48) (2.2) (.64) (.8) (.94) (.5) (.69) (.43) (.28) (2.58) (.42) (.4) (.6) (.35) (.34) (.38) (.85) (.34) (.52) (3.) (.85) (.65) (.79) (.3) (.43) (.8) (.45) (.7) (.72) (2.35) (.3) (.45) (.6) (.7) (.43) (.46) (2.7) (2.36) (.58) 993: Jan (.62) (.5) (.37) (.44) (.) (.26) (2.8) (.3) 37

A study of volatility risk

Journal of Fnance and Accounng 2014; 2(1): 1-10 Publshed onlne January 30, 2014 (hp://www.scencepublshnggroup.com/j/jfa) do: 10.11648/j.jfa.20140201.11 A sudy of volaly rsk Kala Lama *, Jlan Faouz Graduae

Journal of Fnance and Accounng 2014; 2(1): 1-10 Publshed onlne January 30, 2014 (hp://www.scencepublshnggroup.com/j/jfa) do: 10.11648/j.jfa.20140201.11 A sudy of volaly rsk Kala Lama *, Jlan Faouz Graduae

Betting Against Beta

Beng Agans Bea Andrea Frazzn and Lasse Heje Pedersen * Ths draf: February 4, 2013 Absrac. We presen a model wh leverage and margn consrans ha vary across nvesors and me. We fnd evdence conssen wh each

Beng Agans Bea Andrea Frazzn and Lasse Heje Pedersen * Ths draf: February 4, 2013 Absrac. We presen a model wh leverage and margn consrans ha vary across nvesors and me. We fnd evdence conssen wh each

Time-Varying Correlations and Optimal Allocation in Emerging Market Equities for Australian Investors: A Study Using East European Depositary Receipts

Tme-Varyng Correlaons and Opmal Allocaon n Emergng Marke Eques for Ausralan Invesors: A Sudy Usng Eas European Deposary Receps Auhor Gupa, Rakesh, Jhendranahan, Thadavlll Publshed 2008 Journal Tle Inernaonal

Tme-Varyng Correlaons and Opmal Allocaon n Emergng Marke Eques for Ausralan Invesors: A Sudy Usng Eas European Deposary Receps Auhor Gupa, Rakesh, Jhendranahan, Thadavlll Publshed 2008 Journal Tle Inernaonal

Research Division Federal Reserve Bank of St. Louis Working Paper Series

Research Dvson Federal Reserve Bank of S. Lous Workng Paper Seres Inflaon: Do Expecaons Trump he Gap? Jeremy M. Pger and Rober H. Rasche Workng Paper 006-013A hp://research.slousfed.org/wp/006/006-013.pdf

Research Dvson Federal Reserve Bank of S. Lous Workng Paper Seres Inflaon: Do Expecaons Trump he Gap? Jeremy M. Pger and Rober H. Rasche Workng Paper 006-013A hp://research.slousfed.org/wp/006/006-013.pdf

Exercise 8. Panel Data (Answers) (the values of any variable are correlated over time for the same individuals)

(the values of any variable are correlated over time for the same individuals)") ercse 8. Panel Daa Answers. Gven m a,.,. I follows ha Varm m s Varm Varm s - Covm, m s Wh anel daa s lkel ha Covm, m s > he vales of an varable are correlaed over me for he same ndvdals Wh ooled daa hen

ercse 8. Panel Daa Answers. Gven m a,.,. I follows ha Varm m s Varm Varm s - Covm, m s Wh anel daa s lkel ha Covm, m s > he vales of an varable are correlaed over me for he same ndvdals Wh ooled daa hen

2. Literature Review Theory of Investment behavior

Effec of Equy Rsk Facors on he Reurn of Sock Porfolos of Companes Lsed a he Narob Secures Exchange n Kenya Beween 2009 and 2014 Mchael.N. Njogo 1* Edde Smyu 2 Sephen. T. Wahaka 3 Deparmen of Accounng and

Effec of Equy Rsk Facors on he Reurn of Sock Porfolos of Companes Lsed a he Narob Secures Exchange n Kenya Beween 2009 and 2014 Mchael.N. Njogo 1* Edde Smyu 2 Sephen. T. Wahaka 3 Deparmen of Accounng and

Stock (mis)pricing and Investment Dynamics in Africa

pricing and Investment Dynamics in Africa") Sock msprcng and nvesmen Dynamcs n Afrca Sad Aanda Musapha n 273 July 2017 Workng aper Seres Afrcan Developmen Bank Group Workng aper N o 273 Absrac The sudy ascerans he exen of msprcng n equy porfolos

Sock msprcng and nvesmen Dynamcs n Afrca Sad Aanda Musapha n 273 July 2017 Workng aper Seres Afrcan Developmen Bank Group Workng aper N o 273 Absrac The sudy ascerans he exen of msprcng n equy porfolos

THE PERFORMANCE OF ALTERNATIVE INTEREST RATE RISK MEASURES AND IMMUNIZATION STRATEGIES UNDER A HEATH-JARROW-MORTON FRAMEWORK

THE PERFORMANCE OF ALTERNATIVE INTEREST RATE RISK MEASURES AND IMMUNIZATION STRATEGIES UNDER A HEATH-JARROW-MORTON FRAMEWORK By Şenay Ağca Dsseraon submed o he faculy of Vrgna Polyechnc Insue and Sae Unversy

THE PERFORMANCE OF ALTERNATIVE INTEREST RATE RISK MEASURES AND IMMUNIZATION STRATEGIES UNDER A HEATH-JARROW-MORTON FRAMEWORK By Şenay Ağca Dsseraon submed o he faculy of Vrgna Polyechnc Insue and Sae Unversy

A Critical Analysis of the Technical Assumptions of the Standard Micro Portfolio Approach to Sovereign Debt Management

Please ce hs paper as: Blommesen, H. J. and A. Hubg (2012), A Crcal Analyss of he echncal Assumpons of he Sandard Mcro Porfolo Approach o Soveregn Deb Managemen, OECD Workng Papers on Soveregn Borrowng

Please ce hs paper as: Blommesen, H. J. and A. Hubg (2012), A Crcal Analyss of he echncal Assumpons of he Sandard Mcro Porfolo Approach o Soveregn Deb Managemen, OECD Workng Papers on Soveregn Borrowng

REIT Markets and Rational Speculative Bubbles: An Empirical Investigation

REIT Markes and Raonal Speculave Bubbles: An Emprcal Invesgaon George A. Waers Asssan Professor Deparmen of Economcs Illnos Sae Unversy Normal, IL 61790-4200 gawaer@lsu.edu 309-438-7301 and James E. Payne

REIT Markes and Raonal Speculave Bubbles: An Emprcal Invesgaon George A. Waers Asssan Professor Deparmen of Economcs Illnos Sae Unversy Normal, IL 61790-4200 gawaer@lsu.edu 309-438-7301 and James E. Payne

PERSONAL VERSION. Readers are kindly asked to use the official publication in references.

PSONAL VSION Ths s a so called personal verson auhors s anuscrp as acceped for publshng afer he revew process bu pror o fnal layou and copyedng of he arcle. Bu, H & Vrk, N S 204, ' Lqudy and asse prces:

PSONAL VSION Ths s a so called personal verson auhors s anuscrp as acceped for publshng afer he revew process bu pror o fnal layou and copyedng of he arcle. Bu, H & Vrk, N S 204, ' Lqudy and asse prces:

System GMM estimation with a small sample Marcelo Soto July 15, 2009

ysem GMM esmaon wh a small sample Marcelo oo July 15, 9 Barcelona Economcs Workng Paper eres Workng Paper nº 395 YTEM GMM ETIMATION WITH A MALL AMPLE Marcelo oo July 9 Properes of GMM esmaors for panel

ysem GMM esmaon wh a small sample Marcelo oo July 15, 9 Barcelona Economcs Workng Paper eres Workng Paper nº 395 YTEM GMM ETIMATION WITH A MALL AMPLE Marcelo oo July 9 Properes of GMM esmaors for panel

Morningstar Investor Return

Morningsar Invesor Reurn Morningsar Mehodology Paper March 3, 2009 2009 Morningsar, Inc. All righs reserved. The informaion in his documen is he propery of Morningsar, Inc. Reproducion or ranscripion by

Morningsar Invesor Reurn Morningsar Mehodology Paper March 3, 2009 2009 Morningsar, Inc. All righs reserved. The informaion in his documen is he propery of Morningsar, Inc. Reproducion or ranscripion by

The Yen and The Competitiveness of Japanese Industries and Firms. March 4, 2008 (preliminary draft) Robert Dekle Department of Economics USC

Robert Dekle Department of Economics USC") 1 The Yen and The Compeveness of apanese Indusres and Frms March 4 2008 prelmnary draf Rober Dekle Deparmen of Economcs USC Kyoj Fukao Insue of Economc Research Hosubash Unversy Prepared for he ESRI Workshop

1 The Yen and The Compeveness of apanese Indusres and Frms March 4 2008 prelmnary draf Rober Dekle Deparmen of Economcs USC Kyoj Fukao Insue of Economc Research Hosubash Unversy Prepared for he ESRI Workshop

Authors: Christian Panzer, Gustav Resch, Reinhard Haas, Patrick Schumacher. Energy Economics Group, Vienna University of Technology

Dervng fuure suppor shemes of RES, y onsderng he os evoluon of RES ehnologes a volale energy and raw maeral pres aompaned y ehnologal learnng mpas Auhors: Chrsan Panzer, Gusav Resh, Renhard Haas, Park

Dervng fuure suppor shemes of RES, y onsderng he os evoluon of RES ehnologes a volale energy and raw maeral pres aompaned y ehnologal learnng mpas Auhors: Chrsan Panzer, Gusav Resh, Renhard Haas, Park

NoC Impact on Design Methodology. Characteristics of NoC-based design. Timing Closure in Traditional VLSI

NoC Impac on Desgn Mehodology Avnoam Kolodny NoC as Means o Handle Complexy (Oucome of Moore s Law) Prncples for dealng wh complexy: Absracon Herarchy egulary Desgn Mehodology 000 00 Termnals per module

NoC Impac on Desgn Mehodology Avnoam Kolodny NoC as Means o Handle Complexy (Oucome of Moore s Law) Prncples for dealng wh complexy: Absracon Herarchy egulary Desgn Mehodology 000 00 Termnals per module

Paul M. Sommers David U. Cha And Daniel P. Glatt. March 2010 MIDDLEBURY COLLEGE ECONOMICS DISCUSSION PAPER NO

AN EMPIRICAL TEST OF BILL JAMES S PYTHAGOREAN FORMULA by Paul M. Sommers David U. Cha And Daniel P. Gla March 2010 MIDDLEBURY COLLEGE ECONOMICS DISCUSSION PAPER NO. 10-06 DEPARTMENT OF ECONOMICS MIDDLEBURY

AN EMPIRICAL TEST OF BILL JAMES S PYTHAGOREAN FORMULA by Paul M. Sommers David U. Cha And Daniel P. Gla March 2010 MIDDLEBURY COLLEGE ECONOMICS DISCUSSION PAPER NO. 10-06 DEPARTMENT OF ECONOMICS MIDDLEBURY

Productivity and Competitiveness: The Case of Football Teams Playing in the UEFA Champions League

Ahens Journal of Spors March 2016 Producvy and Compeveness: The Case of Fooball Teams Playng n he UEFA Champons League By Manuel Espa-Escuer Luca Isabel Garca-Cebran The purpose of hs sudy s o evaluae

Ahens Journal of Spors March 2016 Producvy and Compeveness: The Case of Fooball Teams Playng n he UEFA Champons League By Manuel Espa-Escuer Luca Isabel Garca-Cebran The purpose of hs sudy s o evaluae

The influence of settlement on flood prevention capability of the floodcontrol wall along the Bund in Shanghai

IAG6 Paper number 8 The nfluence of selemen on flood prevenon capably of he floodconrol wall along he Bund n Shangha 3 BAO CHN, LIN-D YANG & HUI-FNG CHNG 3 Tong Unversy. (e-mal: chenbao@ong.edu.cn) Tong

IAG6 Paper number 8 The nfluence of selemen on flood prevenon capably of he floodconrol wall along he Bund n Shangha 3 BAO CHN, LIN-D YANG & HUI-FNG CHNG 3 Tong Unversy. (e-mal: chenbao@ong.edu.cn) Tong

Time & Distance SAKSHI If an object travels the same distance (D) with two different speeds S 1 taking different times t 1

with two different speeds S 1 taking different times t 1") www.sakshieducaion.com Time & isance The raio beween disance () ravelled by an objec and he ime () aken by ha o ravel he disance is called he speed (S) of he objec. S = = S = Generally if he disance ()

www.sakshieducaion.com Time & isance The raio beween disance () ravelled by an objec and he ime () aken by ha o ravel he disance is called he speed (S) of he objec. S = = S = Generally if he disance ()

Reduced drift, high accuracy stable carbon isotope ratio measurements using a reference gas with the Picarro 13 CO 2 G2101-i gas analyzer

Reduced drft, hgh accuracy stable carbon sotope rato measurements usng a reference gas wth the Pcarro 13 CO 2 G2101- gas analyzer Chrs Rella, Ph.D. Drector of Research & Development Pcarro, Inc., Sunnyvale,

Reduced drft, hgh accuracy stable carbon sotope rato measurements usng a reference gas wth the Pcarro 13 CO 2 G2101- gas analyzer Chrs Rella, Ph.D. Drector of Research & Development Pcarro, Inc., Sunnyvale,

BISI Wear Dance Art Clothing. September 10, April 27, 2019

wwwbs-dancercom Elk Grove Vllage, IL 60007 Meacham Beserfeld) Phone: 8473636398 nfo@bs-dancercom brng shake 19 2018-20! Creave apparel, ye fashonable o DANCE n! We offer BISI dance are from head o oe for

wwwbs-dancercom Elk Grove Vllage, IL 60007 Meacham Beserfeld) Phone: 8473636398 nfo@bs-dancercom brng shake 19 2018-20! Creave apparel, ye fashonable o DANCE n! We offer BISI dance are from head o oe for

Interpreting Sinusoidal Functions

6.3 Inerpreing Sinusoidal Funcions GOAL Relae deails of sinusoidal phenomena o heir graphs. LEARN ABOUT he Mah Two sudens are riding heir bikes. A pebble is suck in he ire of each bike. The wo graphs show

6.3 Inerpreing Sinusoidal Funcions GOAL Relae deails of sinusoidal phenomena o heir graphs. LEARN ABOUT he Mah Two sudens are riding heir bikes. A pebble is suck in he ire of each bike. The wo graphs show

Capacity Utilization Metrics Revisited: Delay Weighting vs Demand Weighting. Mark Hansen Chieh-Yu Hsiao University of California, Berkeley 01/29/04

Capaciy Uilizaion Merics Revisied: Delay Weighing vs Demand Weighing Mark Hansen Chieh-Yu Hsiao Universiy of California, Berkeley 01/29/04 1 Ouline Inroducion Exising merics examinaion Proposed merics

Capaciy Uilizaion Merics Revisied: Delay Weighing vs Demand Weighing Mark Hansen Chieh-Yu Hsiao Universiy of California, Berkeley 01/29/04 1 Ouline Inroducion Exising merics examinaion Proposed merics

APPLYING BI-OBJECTIVE SHORTEST PATH METHODS TO MODEL CYCLE ROUTE-CHOICE ABSTRACT

Andrea Rah, Chrs Van Houe, Judh Y.T. Wang, and Mahas Ehrgo APPLYING BI-OBJECTIVE SHORTEST PATH METHODS TO MODEL CYCLE ROUTE-CHOICE Andrea Rah 1, Chrs Van Houe 2, Judh Y. T. Wang 3, and Mahas Ehrgo 4 The

Andrea Rah, Chrs Van Houe, Judh Y.T. Wang, and Mahas Ehrgo APPLYING BI-OBJECTIVE SHORTEST PATH METHODS TO MODEL CYCLE ROUTE-CHOICE Andrea Rah 1, Chrs Van Houe 2, Judh Y. T. Wang 3, and Mahas Ehrgo 4 The

World Academy of Science, Engineering and Technology International Journal of Civil and Environmental Engineering Vol:4, No:10, 2010

Evaluaon of he Dsplacemen-Based and he Force-Based Adapve Pushover Mehods n Sesmc Response Esmaon of Irregular Buldngs Consderng Torsonal Effecs R. Abbasna, F. Mohajer Nav, S. Zahedfar, and A. Tajk Absrac

Evaluaon of he Dsplacemen-Based and he Force-Based Adapve Pushover Mehods n Sesmc Response Esmaon of Irregular Buldngs Consderng Torsonal Effecs R. Abbasna, F. Mohajer Nav, S. Zahedfar, and A. Tajk Absrac

The t-test. What We Will Cover in This Section. A Research Situation

The -es 1//008 P331 -ess 1 Wha We Will Cover in This Secion Inroducion One-sample -es. Power and effec size. Independen samples -es. Dependen samples -es. Key learning poins. 1//008 P331 -ess A Research

The -es 1//008 P331 -ess 1 Wha We Will Cover in This Secion Inroducion One-sample -es. Power and effec size. Independen samples -es. Dependen samples -es. Key learning poins. 1//008 P331 -ess A Research

Kinematics. Overview. Forward Kinematics. Example: 2-Link Structure. Forward Kinematics. Forward Kinematics

Overvew Knemacs Tomas Funkouser Prnceon Unversy C0S 46, Sprng 004 Knemacs Consders only moon Deermned by posons, veloces, acceleraons Dynamcs Consders underlyng forces Compue moon from nal condons and

Overvew Knemacs Tomas Funkouser Prnceon Unversy C0S 46, Sprng 004 Knemacs Consders only moon Deermned by posons, veloces, acceleraons Dynamcs Consders underlyng forces Compue moon from nal condons and

Market Timing with GEYR in Emerging Stock Market: The Evidence from Stock Exchange of Thailand

Journal of Finance and Invesmen Analysis, vol. 1, no. 4, 2012, 53-65 ISSN: 2241-0998 (prin version), 2241-0996(online) Scienpress Ld, 2012 Marke Timing wih GEYR in Emerging Sock Marke: The Evidence from

Journal of Finance and Invesmen Analysis, vol. 1, no. 4, 2012, 53-65 ISSN: 2241-0998 (prin version), 2241-0996(online) Scienpress Ld, 2012 Marke Timing wih GEYR in Emerging Sock Marke: The Evidence from

Wladimir Andreff, Madeleine Andreff. To cite this version: HAL Id: halshs https://halshs.archives-ouvertes.

Economc predcon of spor performances from he Bejng Olympcs o he 2010 FIFA World Cup n Souh Afrca: he noon of surprsng sporng oucomes Wladmr Andreff Madelene Andreff To ce hs verson: Wladmr Andreff Madelene

Economc predcon of spor performances from he Bejng Olympcs o he 2010 FIFA World Cup n Souh Afrca: he noon of surprsng sporng oucomes Wladmr Andreff Madelene Andreff To ce hs verson: Wladmr Andreff Madelene

Lifecycle Funds. T. Rowe Price Target Retirement Fund. Lifecycle Asset Allocation

Lifecycle Funds Towards a Dynamic Asse Allocaion Framework for Targe Reiremen Funds: Geing Rid of he Dogma in Lifecycle Invesing Anup K. Basu Queensland Universiy of Technology The findings of he Mercer

Lifecycle Funds Towards a Dynamic Asse Allocaion Framework for Targe Reiremen Funds: Geing Rid of he Dogma in Lifecycle Invesing Anup K. Basu Queensland Universiy of Technology The findings of he Mercer

The Impact of Demand Correlation on Bullwhip Effect in a Two-stage Supply Chain with Two Retailers

The Impac of Demand Correlaon on Bullwhp Effec n a Two-age Supply Chan wh Two Realer Janhua J Huafeng Je Zhang and Cucu eng Ana College of Economc and anagemen Shangha Jao Tong Unvery Shangha 0005 Chna

The Impac of Demand Correlaon on Bullwhp Effec n a Two-age Supply Chan wh Two Realer Janhua J Huafeng Je Zhang and Cucu eng Ana College of Economc and anagemen Shangha Jao Tong Unvery Shangha 0005 Chna

Strategic Decision Making in Portfolio Management with Goal Programming Model

American Journal of Operaions Managemen and Informaion Sysems 06; (): 34-38 hp://www.sciencepublishinggroup.com//aomis doi: 0.648/.aomis.0600.4 Sraegic Decision Making in Porfolio Managemen wih Goal Programming

American Journal of Operaions Managemen and Informaion Sysems 06; (): 34-38 hp://www.sciencepublishinggroup.com//aomis doi: 0.648/.aomis.0600.4 Sraegic Decision Making in Porfolio Managemen wih Goal Programming

The Great Recession in the U.K. Labour Market: A Transatlantic View

The Grea Recession in he U.K. Labour Marke: A Transalanic View Michael W. L. Elsby (Edinburgh, Michigan, NBER) Jennifer C. Smih (Warwick) Bank of England, 25 March 2011 U.K. and U.S. unemploymen U.K. unemploymen

The Grea Recession in he U.K. Labour Marke: A Transalanic View Michael W. L. Elsby (Edinburgh, Michigan, NBER) Jennifer C. Smih (Warwick) Bank of England, 25 March 2011 U.K. and U.S. unemploymen U.K. unemploymen

Proportional Reasoning

Proporional Reasoning Focus on Afer his lesson, you will be able o... solve problems using proporional reasoning use more han one mehod o solve proporional reasoning problems When you go snowboarding or

Proporional Reasoning Focus on Afer his lesson, you will be able o... solve problems using proporional reasoning use more han one mehod o solve proporional reasoning problems When you go snowboarding or

Analyzing the Bullwhip Effect in a Supply Chain with ARMA(1,1) Demand Using MMSE Forecasting

Demand Using MMSE Forecasting") Inernaona Journa on Advances n Informaon cences and ervce cences Voume Number March Anayzng he Buwhp Effec n a uppy han wh ARMA emand Usng MME Forecasng huanxu Wang choo of Economy and Managemen hangha

Inernaona Journa on Advances n Informaon cences and ervce cences Voume Number March Anayzng he Buwhp Effec n a uppy han wh ARMA emand Usng MME Forecasng huanxu Wang choo of Economy and Managemen hangha

AP Physics 1 Per. Unit 2 Homework. s av

Name: Dae: AP Physics Per. Uni Homework. A car is driven km wes in hour and hen 7 km eas in hour. Eas is he posiive direcion. a) Wha is he average velociy and average speed of he car in km/hr? x km 3.3km/

Name: Dae: AP Physics Per. Uni Homework. A car is driven km wes in hour and hen 7 km eas in hour. Eas is he posiive direcion. a) Wha is he average velociy and average speed of he car in km/hr? x km 3.3km/

Engineering Analysis of Implementing Pedestrian Scramble Crossing at Traffic Junctions in Singapore

Engneerng Analyss of Implementng Pedestran Scramble Crossng at Traffc Junctons n Sngapore Dr. Lm Wee Chuan Eldn Department of Chemcal & Bomolecular Engneerng, Natonal Unversty of Sngapore, 4 Engneerng

Engneerng Analyss of Implementng Pedestran Scramble Crossng at Traffc Junctons n Sngapore Dr. Lm Wee Chuan Eldn Department of Chemcal & Bomolecular Engneerng, Natonal Unversty of Sngapore, 4 Engneerng

Stock Return Expectations in the Credit Market

Sock Reurn Expecaions in he Credi Marke Hans Bysröm * Sepember 016 In his paper we compue long-erm sock reurn expecaions (across he business cycle) for individual firms using informaion backed ou from

Sock Reurn Expecaions in he Credi Marke Hans Bysröm * Sepember 016 In his paper we compue long-erm sock reurn expecaions (across he business cycle) for individual firms using informaion backed ou from

Using Rates of Change to Create a Graphical Model. LEARN ABOUT the Math. Create a speed versus time graph for Steve s walk to work.

2.4 Using Raes of Change o Creae a Graphical Model YOU WILL NEED graphing calculaor or graphing sofware GOAL Represen verbal descripions of raes of change using graphs. LEARN ABOUT he Mah Today Seve walked

2.4 Using Raes of Change o Creae a Graphical Model YOU WILL NEED graphing calculaor or graphing sofware GOAL Represen verbal descripions of raes of change using graphs. LEARN ABOUT he Mah Today Seve walked

Evaluating the Effectiveness of Price and Yield Risk Management Products in Reducing. Revenue Risk for Southeastern Crop Producers * Todd D.

Evaluatng the Effectveness of Prce and Yeld Rsk Management Products n Reducng Revenue Rsk for Southeastern Crop Producers * Todd D. Davs ** Abstract A non-parametrc smulaton model ncorporatng prce and

Evaluatng the Effectveness of Prce and Yeld Rsk Management Products n Reducng Revenue Rsk for Southeastern Crop Producers * Todd D. Davs ** Abstract A non-parametrc smulaton model ncorporatng prce and

A Probabilistic Approach to Worst Case Scenarios

A Probabilisic Approach o Wors Case Scenarios A Probabilisic Approach o Wors Case Scenarios By Giovanni Barone-Adesi Universiy of Albera, Canada and Ciy Universiy Business School, London Frederick Bourgoin

A Probabilisic Approach o Wors Case Scenarios A Probabilisic Approach o Wors Case Scenarios By Giovanni Barone-Adesi Universiy of Albera, Canada and Ciy Universiy Business School, London Frederick Bourgoin

What the Puck? an exploration of Two-Dimensional collisions

Wha he Puck? an exploraion of Two-Dimensional collisions 1) Have you ever played 8-Ball pool and los he game because you scrached while aemping o sink he 8-Ball in a corner pocke? Skech he sho below: Each

Wha he Puck? an exploraion of Two-Dimensional collisions 1) Have you ever played 8-Ball pool and los he game because you scrached while aemping o sink he 8-Ball in a corner pocke? Skech he sho below: Each

Market timing and statistical arbitrage: Which market timing opportunities arise from equity price busts coinciding with recessions?

Journal of Applied Finance & Banking, vol.1, no.1, 2011, 53-81 ISSN: 1792-6580 (prin version), 1792-6599 (online) Inernaional Scienific Press, 2011 Marke iming and saisical arbirage: Which marke iming

Journal of Applied Finance & Banking, vol.1, no.1, 2011, 53-81 ISSN: 1792-6580 (prin version), 1792-6599 (online) Inernaional Scienific Press, 2011 Marke iming and saisical arbirage: Which marke iming

Idiosyncratic Volatility, Stock Returns and Economy Conditions: The Role of Idiosyncratic Volatility in the Australian Stock Market

Idiosyncraic Volailiy, Sock Reurns and Economy Condiions: The Role of Idiosyncraic Volailiy in he Ausralian Sock Marke Bin Liu Amalia Di Iorio RMIT Universiy Melbourne Ausralia Absrac This sudy examines

Idiosyncraic Volailiy, Sock Reurns and Economy Condiions: The Role of Idiosyncraic Volailiy in he Ausralian Sock Marke Bin Liu Amalia Di Iorio RMIT Universiy Melbourne Ausralia Absrac This sudy examines

Identification of trend patterns related to the dynamics of competitive intelligence budgets (the case of Romanian software industry)

") Advances n Manageen & Appled Econocs, vol., no.3, 01, 133-16 ISSN: 179-7544 (prn verson), 179-755 (onlne) Scenpress Ld, 01 Idenfcaon of rend paerns relaed o he dynacs of copeve nellgence budges (he case

Advances n Manageen & Appled Econocs, vol., no.3, 01, 133-16 ISSN: 179-7544 (prn verson), 179-755 (onlne) Scenpress Ld, 01 Idenfcaon of rend paerns relaed o he dynacs of copeve nellgence budges (he case

Betting Against Beta

Being Agains Bea Andrea Frazzini and Lasse H. Pedersen * This draf: Ocober 5, 2010 Absrac. We presen a model in which some invesors are prohibied from using leverage and oher invesors leverage is limied

Being Agains Bea Andrea Frazzini and Lasse H. Pedersen * This draf: Ocober 5, 2010 Absrac. We presen a model in which some invesors are prohibied from using leverage and oher invesors leverage is limied

3. The amount to which $1,000 will grow in 5 years at a 6 percent annual interest rate compounded annually is

8 h Grade Eam - 00. Which one of he following saemens is rue? a) There is a larges negaive raional number. b) There is a larges negaive ineger. c) There is a smalles ineger. d) There is a smalles negaive

8 h Grade Eam - 00. Which one of he following saemens is rue? a) There is a larges negaive raional number. b) There is a larges negaive ineger. c) There is a smalles ineger. d) There is a smalles negaive

Homework 2. is unbiased if. Y is consistent if. c. in real life you typically get to sample many times.

Econ526 Mulile Choice. Homework 2 Choose he one ha bes comlees he saemen or answers he quesion. (1) An esimaor ˆ µ of he oulaion value µ is unbiased if a. ˆ µ = µ. b. has he smalles variance of all esimaors.

Econ526 Mulile Choice. Homework 2 Choose he one ha bes comlees he saemen or answers he quesion. (1) An esimaor ˆ µ of he oulaion value µ is unbiased if a. ˆ µ = µ. b. has he smalles variance of all esimaors.

Guidance Statement on Calculation Methodology

Guidance Saemen on Calculaion Mehodology Adopion Dae: 28 Sepember 200 Effecive Dae: January 20 Reroacive Applicaion: No Required www.gipssandards.org 200 CFA Insiue Guidance Saemen on Calculaion Mehodology

Guidance Saemen on Calculaion Mehodology Adopion Dae: 28 Sepember 200 Effecive Dae: January 20 Reroacive Applicaion: No Required www.gipssandards.org 200 CFA Insiue Guidance Saemen on Calculaion Mehodology

Interval Type-1 Non-Singleton Type-2 TSK Fuzzy Logic Systems Using the Kalman Filter - Back Propagation Hybrid Learning Mechanism

Inerval Type- Non-Sngleon Type- TSK Fuzzy Logc Sysems Usng he Kalman Fler - Bac Propagaon Hybrd Learnng Mechansm Gerardo M Mendez, Angeles Hernández, Marcela Casllo-Leal, Danel Loras, Insuo Tecnologco

Inerval Type- Non-Sngleon Type- TSK Fuzzy Logc Sysems Usng he Kalman Fler - Bac Propagaon Hybrd Learnng Mechansm Gerardo M Mendez, Angeles Hernández, Marcela Casllo-Leal, Danel Loras, Insuo Tecnologco

DO BUBBLES AND TIME-VARYING RISK PREMIUMS AFFECT STOCK PRICES? A KALMAN FILTER APPROACH a

DO BUBBS AD TIM-VARYIG RISK RMIUMS AFFCT STOCK RICS? A KAMA FITR AROACH a Dr. -Tarn Cen, Acaema Snca, Tawan Dr. C. James Hueng, Unversy o Alabama, USA Dr. Cen-u Je n, aonal Tawan Unversy, Tawan ABSTRACT

DO BUBBS AD TIM-VARYIG RISK RMIUMS AFFCT STOCK RICS? A KAMA FITR AROACH a Dr. -Tarn Cen, Acaema Snca, Tawan Dr. C. James Hueng, Unversy o Alabama, USA Dr. Cen-u Je n, aonal Tawan Unversy, Tawan ABSTRACT

Do Competitive Advantages Lead to Higher Future Rates of Return?

Do Compeiive Advanages Lead o Higher Fuure Raes of Reurn? Vicki Dickinson Universiy of Florida Greg Sommers Souhern Mehodis Universiy 2010 CARE Conference Forecasing and Indusry Fundamenals April 9, 2010

Do Compeiive Advanages Lead o Higher Fuure Raes of Reurn? Vicki Dickinson Universiy of Florida Greg Sommers Souhern Mehodis Universiy 2010 CARE Conference Forecasing and Indusry Fundamenals April 9, 2010

The Current Account as A Dynamic Portfolio Choice Problem

Public Disclosure Auhorized Policy Research Working Paper 486 WPS486 Public Disclosure Auhorized Public Disclosure Auhorized The Curren Accoun as A Dynamic Porfolio Choice Problem Taiana Didier Alexandre

Public Disclosure Auhorized Policy Research Working Paper 486 WPS486 Public Disclosure Auhorized Public Disclosure Auhorized The Curren Accoun as A Dynamic Porfolio Choice Problem Taiana Didier Alexandre

THE REMOVAL OF ONE-COMPONENT BUBBLES FROM GLASS MELTS IN A ROTATING CYLINDER

Orgnal papers THE REMOVAL OF ONE-COMPONENT BUBBLES FROM GLASS MELTS IN A ROTATING CYLINDER LUBOMÍR NÌMEC, VLADISLAVA TONAROVÁ Laboraory of Inorganc Maerals, Jon Workplace of he Insue of Chemcal Technology

Orgnal papers THE REMOVAL OF ONE-COMPONENT BUBBLES FROM GLASS MELTS IN A ROTATING CYLINDER LUBOMÍR NÌMEC, VLADISLAVA TONAROVÁ Laboraory of Inorganc Maerals, Jon Workplace of he Insue of Chemcal Technology

Evaluation of a Center Pivot Variable Rate Irrigation System

Evaluaton of a Center Pvot Varable Rate Irrgaton System Ruxu Su Danel K. Fsher USDA-ARS Crop Producton Systems Research Unt, Stonevlle, Msssspp Abstrat: Unformty of water dstrbuton of a varable rate center

Evaluaton of a Center Pvot Varable Rate Irrgaton System Ruxu Su Danel K. Fsher USDA-ARS Crop Producton Systems Research Unt, Stonevlle, Msssspp Abstrat: Unformty of water dstrbuton of a varable rate center

Methodology for ACT WorkKeys as a Predictor of Worker Productivity

Methodology for ACT WorkKeys as a Predctor of Worker Productvty The analyss examned the predctve potental of ACT WorkKeys wth regard to two elements. The frst s tme to employment. People takng WorkKeys

Methodology for ACT WorkKeys as a Predctor of Worker Productvty The analyss examned the predctve potental of ACT WorkKeys wth regard to two elements. The frst s tme to employment. People takng WorkKeys

ANALYSIS OF RELIABILITY, MAINTENANCE AND RISK BASED INSPECTION OF PRESSURE SAFETY VALVES

ANALYSIS OF RELIABILITY, MAINTENANCE AND RISK BASED INSPECTION OF PRESSURE SAFETY VALVES Venilon Forunao Francisco Machado Mechanical Engineering Dep, Insiuo Superior Técnico, Av. Rovisco Pais, 049-00,

ANALYSIS OF RELIABILITY, MAINTENANCE AND RISK BASED INSPECTION OF PRESSURE SAFETY VALVES Venilon Forunao Francisco Machado Mechanical Engineering Dep, Insiuo Superior Técnico, Av. Rovisco Pais, 049-00,

TRACK PROCEDURES 2016 RACE DAY

TRACK PROCEDURES 2016 RACE DAY Pi gaes will officially open a 4:00pm for regular programs. Big shows will have earlier opening imes. Hauler parking may be available approximaely 1 hour prior o pi gaes

TRACK PROCEDURES 2016 RACE DAY Pi gaes will officially open a 4:00pm for regular programs. Big shows will have earlier opening imes. Hauler parking may be available approximaely 1 hour prior o pi gaes

KEY CONCEPTS AND PROCESS SKILLS. 1. An allele is one of the two or more forms of a gene present in a population. MATERIALS AND ADVANCE PREPARATION

Gene Squares 61 40- o 2 3 50-minue sessions ACIVIY OVERVIEW P R O B L E M S O LV I N G SUMMARY Sudens use Punne squares o predic he approximae frequencies of rais among he offspring of specific crier crosses.

Gene Squares 61 40- o 2 3 50-minue sessions ACIVIY OVERVIEW P R O B L E M S O LV I N G SUMMARY Sudens use Punne squares o predic he approximae frequencies of rais among he offspring of specific crier crosses.

1. The value of the digit 4 in the number 42,780 is 10 times the value of the digit 4 in which number?

Mahemaics. he value of he digi in he number 70 is 0 imes he value of he digi in which number?. Mike is years old. Joe is imes as old as Mike. Which equaion shows how o find Joe s age? 70 000 = = = + =

Mahemaics. he value of he digi in he number 70 is 0 imes he value of he digi in which number?. Mike is years old. Joe is imes as old as Mike. Which equaion shows how o find Joe s age? 70 000 = = = + =

The impact of foreign players on international football performance

MPRA Munch Personal RePEc Archve The mpact of foregn players on nternatonal football performance Orhan Karaca Ekonomst Magazne, Research Department October 008 Onlne at http://mpra.ub.un-muenchen.de/11064/

MPRA Munch Personal RePEc Archve The mpact of foregn players on nternatonal football performance Orhan Karaca Ekonomst Magazne, Research Department October 008 Onlne at http://mpra.ub.un-muenchen.de/11064/

Economics 487. Homework #4 Solution Key Portfolio Calculations and the Markowitz Algorithm

Economics 87 Homework # Soluion Key Porfolio Calculaions and he Markowiz Algorihm A. Excel Exercises: (10 poins) 1. Download he Excel file hw.xls from he class websie. This file conains monhly closing

Economics 87 Homework # Soluion Key Porfolio Calculaions and he Markowiz Algorihm A. Excel Exercises: (10 poins) 1. Download he Excel file hw.xls from he class websie. This file conains monhly closing

8/31/11. the distance it travelled. The slope of the tangent to a curve in the position vs time graph for a particles motion gives:

Physics 101 Tuesday Class 2 Chaper 2 Secions 2.1-2.4 Displacemen and disance Velociy and speed acceleraion Reading Quiz The slope of he angen o a curve in he posiion vs ime graph for a paricles moion gives:

Physics 101 Tuesday Class 2 Chaper 2 Secions 2.1-2.4 Displacemen and disance Velociy and speed acceleraion Reading Quiz The slope of he angen o a curve in he posiion vs ime graph for a paricles moion gives:

Performance Attribution for Equity Portfolios

PERFORMACE ATTRIBUTIO FOR EQUITY PORTFOLIOS Performance Aribuion for Equiy Porfolios Yang Lu and David Kane Inroducion Many porfolio managers measure performance wih reference o a benchmark. The difference

PERFORMACE ATTRIBUTIO FOR EQUITY PORTFOLIOS Performance Aribuion for Equiy Porfolios Yang Lu and David Kane Inroducion Many porfolio managers measure performance wih reference o a benchmark. The difference

A Liability Tracking Portfolio for Pension Fund Management

Proceedings of he 46h ISCIE Inernaional Symposium on Sochasic Sysems Theory and Is Applicaions Kyoo, Nov. 1-2, 214 A Liabiliy Tracking Porfolio for Pension Fund Managemen Masashi Ieda, Takashi Yamashia

Proceedings of he 46h ISCIE Inernaional Symposium on Sochasic Sysems Theory and Is Applicaions Kyoo, Nov. 1-2, 214 A Liabiliy Tracking Porfolio for Pension Fund Managemen Masashi Ieda, Takashi Yamashia

Time-Variation in Diversification Benefits of Commodity, REITs, and TIPS 1

Time-Variaion in Diversificaion Benefis of Commodiy, REITs, and TIPS 1 Jing-zhi Huang 2 and Zhaodong Zhong 3 This Draf: July 11, 2006 Absrac Diversificaion benefis of hree ho asse classes, Commodiy, Real

Time-Variaion in Diversificaion Benefis of Commodiy, REITs, and TIPS 1 Jing-zhi Huang 2 and Zhaodong Zhong 3 This Draf: July 11, 2006 Absrac Diversificaion benefis of hree ho asse classes, Commodiy, Real

DIFFUSION ESTIMATION OF MIXTURE MODELS WITH LOCAL AND GLOBAL PARAMETERS

DIFFUSION ESTIMATION OF MIXTURE MODES WITH OCA AND GOBA PARAMETERS Kaml Dedecus and Vladmíra Sečkárová Insue of Informaon Theory and Auomaon Czech Academy of Scences Pod Vodárenskou věží 1143/4 182 08

DIFFUSION ESTIMATION OF MIXTURE MODES WITH OCA AND GOBA PARAMETERS Kaml Dedecus and Vladmíra Sečkárová Insue of Informaon Theory and Auomaon Czech Academy of Scences Pod Vodárenskou věží 1143/4 182 08

Geometrical Description of Signals GEOMETRICAL DESCRIPTION OF SIGNALS. Geometrical/Vectorial Representation. Coder. { } S i SOURCE CODER RECEIVER

UNIVERIÀ DEGLI UDI DI CAGLIARI Unversà degl ud d Cglr Corso d Lure Mgsrle n Ingegner Eleronc e delle elecomunczon UNIVERIÀ DEGLI UDI DI CAGLIARI Geomercl Descrpon of gnls n( { } OURCE CODER RECEIVER GEOMERICAL

UNIVERIÀ DEGLI UDI DI CAGLIARI Unversà degl ud d Cglr Corso d Lure Mgsrle n Ingegner Eleronc e delle elecomunczon UNIVERIÀ DEGLI UDI DI CAGLIARI Geomercl Descrpon of gnls n( { } OURCE CODER RECEIVER GEOMERICAL

FORECASTING TECHNIQUES ADE 2013 Prof Antoni Espasa TOPIC 1 PART 2 TRENDS AND ACCUMULATION OF KNOWLEDGE. SEASONALITY HANDOUT