The World Did Not End in Q1

|

|

|

- Hollie Wilkinson

- 5 years ago

- Views:

Transcription

1 The World Did Not End in Q1 Sam Wilkin Senior Advisor, Business Research Blog:

2 1

3 2

4 3

5 4

6 5 Exports to Russia: 10% of Finnish exports; 4% of Finnish GDP

7 1. Global Economic Weather Report 2. Economic Outlook Europe Grexit US China Russia/Ukraine 6

8 Global Economic Growth Heat Map 1993 Source: IMF 7

9 Global Economic Growth Heat Map 2004 Source: IMF 8

10 Global Economic Growth Heat Map 2009 Source: IMF 9

11 Global Economic Growth Heat Map 2010 Source: IMF 10

12 Global Economic Growth Heat Map 2014 Source: IMF 11

13 Global Economic Growth Heat Map 2015 Source: IMF 12

14 Next up: Europe Outlook What happens if Greece exits? China Outlook US Outlook Russia/Ukraine Outlook 13

15 1. Global Economic Weather Report 2. Economic Outlook Europe Grexit US China Russia/Ukraine 14

16 15

17 16

18 17

19 Eurozone: Lending to non-financial corporations % year Source: Haver Analytics

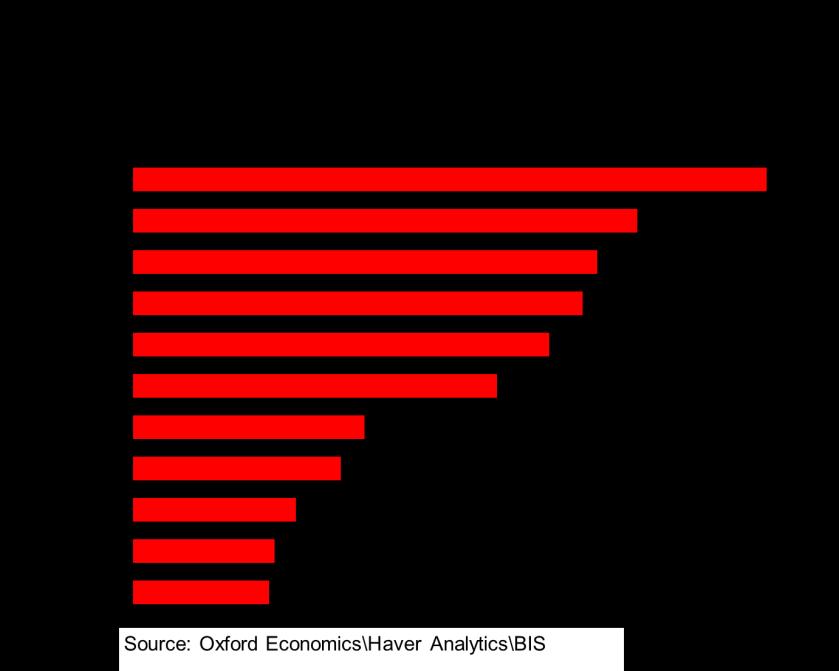

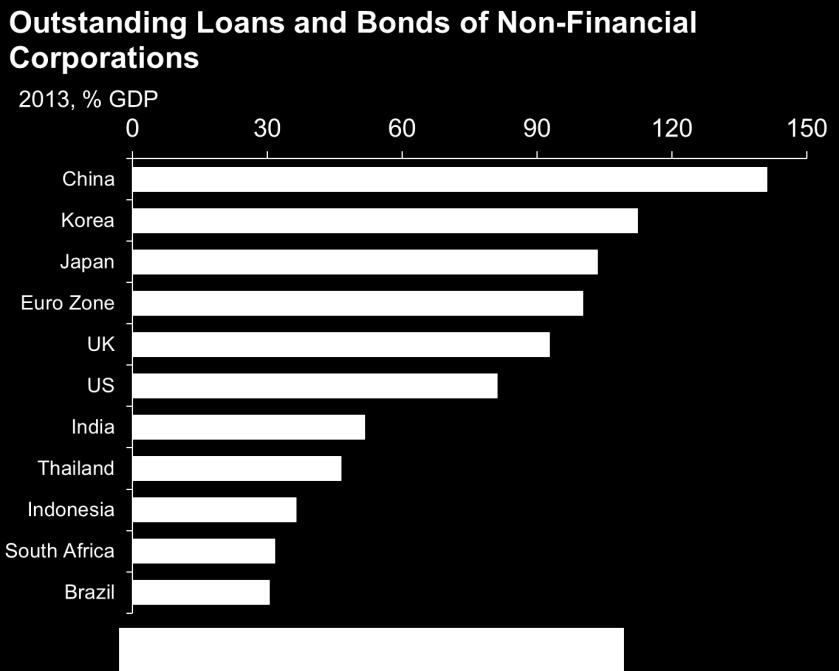

20 19

21 Eurozone: Consumer confidence & retail sales % balance % year 5 Consumer confidence 5 0 (LHS) *3 month moving average Retail sales* (RHS) Source: Haver Analytics

22 21

23 Eurozone: Industrial new orders % year Source: Oxford Economics

24 Cash holdings of non-financial corporations % of GDP UK Germany France Source : Oxford Economics/Haver Analytics

25 Eurozone: GDP % quarter % year-on-year (RHS) % quarter-onquarter (LHS) Forecast % year Source: Oxford Economics

26 RAPPORTO DEBITI/PIL Household FAMIGLIE Debt (%GDP) RAPPORTO DEBITI/PIL Household FAMIGLIE Debt (%GDP) Regno UK Unito Stati Uniti US Spain Spagna 80 Eurozone Zona euro 80 Germany Germania Francia France Italia Italy Source: Oxford Economics

27 200 RAPPORTO DEBITI/PIL Corporate AZIENDE* Debt (%GDP) 200 RAPPORTO DEBITI/PIL Corporate AZIENDE* Debt (%GDP) Spagna Spain 150 Zona euro Eurozone 150 Francia France Italy Italia Regno Unito UK Germania Germany US Stati Uniti * Settore non-finanziario 50 Source: Oxford Economics * Settore non-finanziario.

28 Eurozone: GDP % quarter % year-on-year (RHS) % quarter-onquarter (LHS) Forecast % year Source: Oxford Economics

29 Unit labour costs 2000= Greece Spain France Germany Forecast Italy Source: 28 Oxford Economics

30 29 Productivity growth Ireland Slovakia Spain Portugal France Neth Eurozone Beligum Germany Austria Greece Finland Italy ,% Source : Oxford Economics/Haver Analytics

31 GDP growth forecast for Ireland Slovakia Spain Malta Luxembourg Estonia Slovenia Germany Netherlands Portugal EuroZone France Belgium Austria Italy Finland Greece Cyprus Source: Oxford Economics % year

32 1. Global Economic Weather Report 2. Economic Outlook Europe Grexit US China Russia/Ukraine 31

33 Germany and other AAA countries Eurozone periphery states 32

34 Eurozone: Credit spreads % spread of 10-year bonds over German bunds Greece Portugal Italy Spain Ireland Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Source :Oxford Economics/Haver Analytics

35 Italy Eurozone: Credit spreads % spread of 10-year bonds over German bunds Italy Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Source :Oxford Economics/Haver Analytics

36 Eurozone: Credit spreads % spread of 10-year bonds over German bunds Greece Portugal Italy Spain Ireland : Draghi's "Whatever it takes" Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan Source :Oxford Economics/Haver Analytics

37 Italy Eurozone: Credit spreads % spread of 10-year bonds over German bunds Italy : Draghi's "Whatever it takes" Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Source :Oxford Economics/Haver Analytics

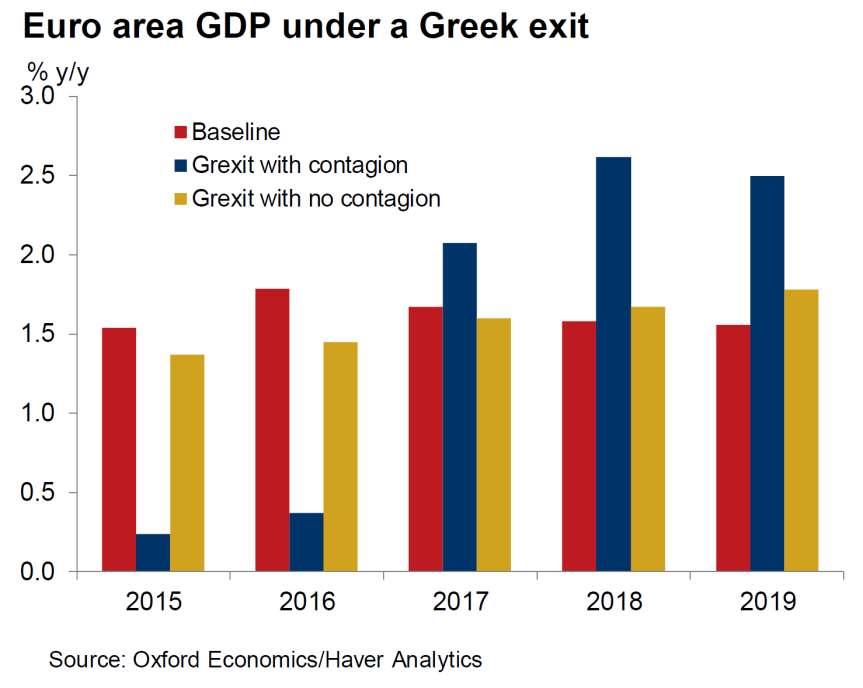

38 Eurozone: Credit spreads % spread of 10-year bonds over German bunds Greece Portugal Italy Spain Ireland : Draghi's "Whatever it takes" Now! Greek Elections Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan Source :Oxford Economics/Haver Analytics

39 Italy Eurozone: Credit spreads % spread of 10-year bonds over German bunds 6 Now! 5 Italy : Draghi's "Whatever it takes" 4 3 Greek Elections Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Source :Oxford Economics/Haver Analytics

40 Now! Germany and other AAA countries Greece

41 Implicit views of markets based on bond prices: 1. Greece and EU reach agreement 78% 2. Agreement stays on track months 67% 3. Capital controls 48% 4. Greek exit 38% Source: Oxford Economics 40

42 Retail deposits at Eurozone banks* % annual growth Spain Greece Ireland -30 Cyprus Portugal * Non-MFIs excluding central government Source : Oxford Economics/ECB

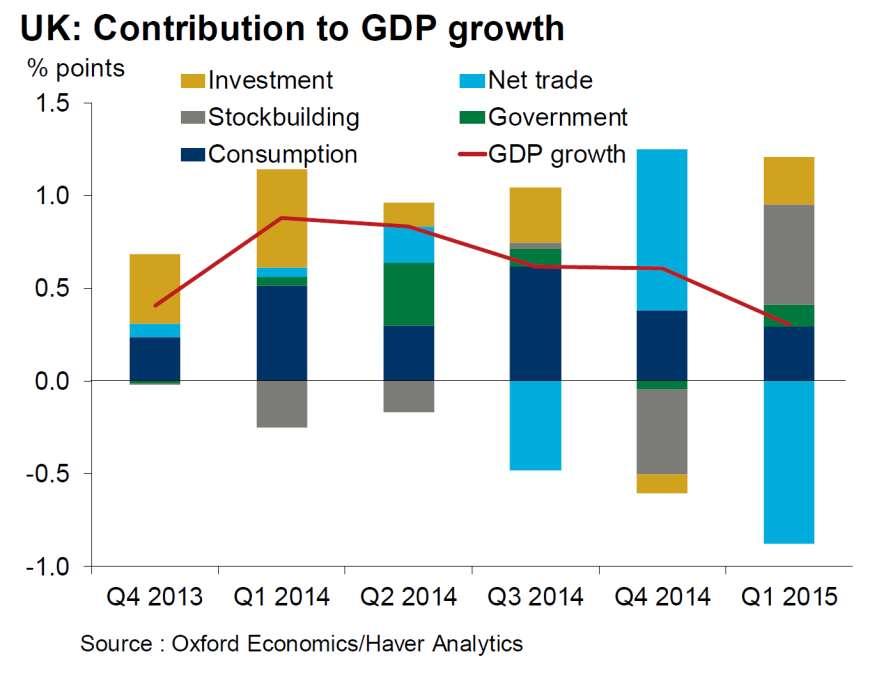

43 Eurozone bank lending to Greece In 2008: 175bn In 2014: 42bn (0.5% of German GDP) (Eurozone gov t lending to Greece: 250bn) 42

44 43

45 44 Greek exit scenario

46 45

47 46 Greek exit scenario

48 1. Global Economic Weather Report 2. Economic Outlook Europe Grexit US China Russia/Ukraine 47

49 48

50 49

51 50

52 51

53 52

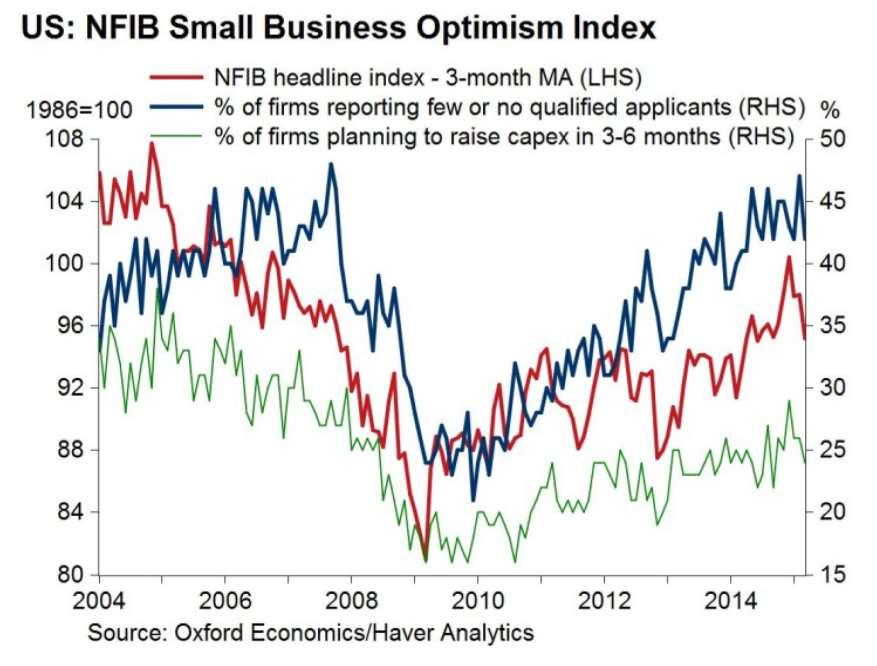

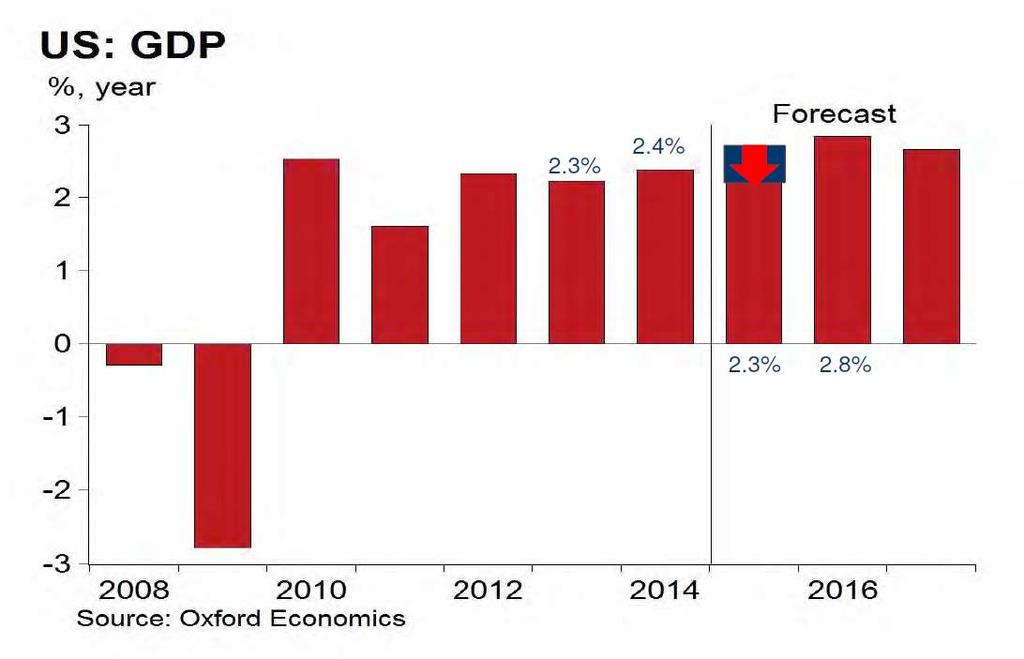

54 US, UK & Eurozone: Corporate loan growth % year 25 UK loans to PNFCs US loans inc. commercial real estate 5 0 Eurozone loans to PNFCs Source : Oxford Economics/Haver Analytics

55 54

56 US: Consumer attitudes 1985= Consumer confidence Conference Board Consumer sentiment University of Michigan Source: Conference Board, University of Michigan/Haver Analytics

57 US: Real wage rate % year Nominal Real Source: BLS, Oxford Economics

58 US: Relative unit labour costs 2008= Forecast Source : Oxford Economics/Haver Analytics

59 Manufacturing Investment Index: 2007 = Japan UK Germany US Source : Oxford Economics/Haver Analytics

60 59

61 60

62 61

63 62

64 63

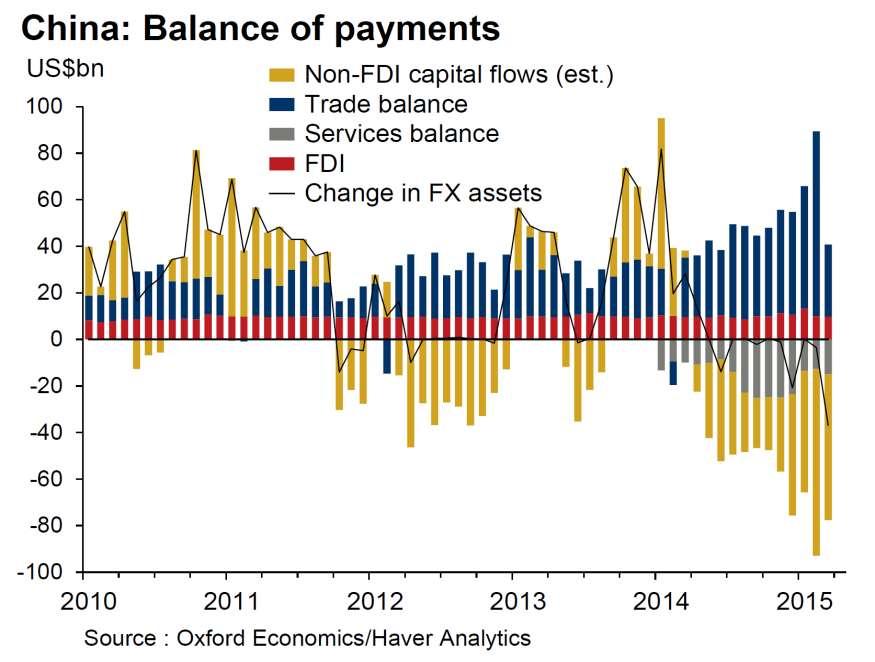

65 1. Global Economic Weather Report 2. Economic Outlook Europe Grexit US China Russia/Ukraine 64

66 65

67 World: Broad money % year 12 Excluding China Including China Source : Oxford Economics/Haver Analytics

68 67

69 68

70 69

71 70

72 China s Forex reserves of $3.6trn Gov t debt of 17% GDP External debt of 9% GDP = bailoutability 71

73 72

74 Economic Growth Forecast for China (%) About 10% About 6% 73

75 1. Global Economic Weather Report 2. Economic Outlook Europe Grexit US China Russia/Ukraine 74

76 Source: nypost.com 75

77 76 Source: abcnews.com

78 77 Source: taringa.net

79 78 Source: businessinsider.com

80 Increase in income per person over the past 30 years in the world s major oil-rich nations* * Oil revenues are more than 10% of economic output * Population of three million people or more 11 Source: World Bank World Development Indicators

81 Increase in income per person over the past 30 years in the world s major oil-rich nations* 6 th -best performance out of 163 countries in the world * Oil revenues are more than 10% of economic output * Population of three million people or more 153 out of out of out of Source: World Bank World Development Indicators

82 A barrier to manufacturing (especially exports) A barrier to democracy A target in war Rental income : control more valuable than creation 13

83 Increase in income per person over the past 30 years in the world s major oil-rich nations* Russia +$3,600 since 1998 A class by itself? Or, will the resource curse return? * Oil revenues are more than 10% of economic output * Population of three million people or more 11 Source: World Bank World Development Indicators

84 Economic Growth Forecast for Russia (%) 83

85 84

86 85

87 86 Conclusion

88 OVERALL SUMMARY Eurozone Market impacts of brinksmanship ended in 2012 But people & companies are deleveraging Hence new normal growth, with some bright spots US Deleveraging largely complete. Q1 slowdown a one-off Hence return to growth; but will it be old normal? China No longer the world s credit engine. New normal is 6% per annum. And, might crash Russia Revenge of the resource curse. New normal is uncertain 87

89 88

90 89

91 The World Did Not End in Q1 Sam Wilkin Senior Advisor, Business Research Blog:

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes. Tom Rogers. Lead Economist, Oxford Economics.

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

The Baltic economies: Current situation and future trends, possibilities and pitfalls

The Baltic economies: Current situation and future trends, possibilities and pitfalls Riga, 15 October 2015 Morten Hansen Head of Economics Department, Stockholm School of Economics in Riga Member of the

The Baltic economies: Current situation and future trends, possibilities and pitfalls Riga, 15 October 2015 Morten Hansen Head of Economics Department, Stockholm School of Economics in Riga Member of the

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip?

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

URBAN LAND INSTITUTE

URBAN LAND INSTITUTE 2012 ULI FALL MEETING (Denver, 18 October 2012) The Global Economic Outlook Dark clouds on the horizon Andrea Boltho Magdalen College University of Oxford Oxford Economics and REAG

URBAN LAND INSTITUTE 2012 ULI FALL MEETING (Denver, 18 October 2012) The Global Economic Outlook Dark clouds on the horizon Andrea Boltho Magdalen College University of Oxford Oxford Economics and REAG

Lithuanian export: is it time to prepare for changes? Aleksandr Izgorodin Expert

Lithuanian export: is it time to prepare for changes? Aleksandr Izgorodin Expert Export is the main locomotive behind growth in LT economy Lithuania: change in real GDP and its components, % 78,2 71,8

Lithuanian export: is it time to prepare for changes? Aleksandr Izgorodin Expert Export is the main locomotive behind growth in LT economy Lithuania: change in real GDP and its components, % 78,2 71,8

RBC Economics Financial Update Dawn Desjardins

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

Emerging from the euro debt crisis Making the single currency work

Emerging from the euro debt crisis Making the single currency work Dr. Michael Heise, Allianz SE American Institute for Contemporary German Studies Johns Hopkins University Washington D.C., August 20,

Emerging from the euro debt crisis Making the single currency work Dr. Michael Heise, Allianz SE American Institute for Contemporary German Studies Johns Hopkins University Washington D.C., August 20,

Better in than out? Economic performance inside and outside the European monetary union. Roma, Rapporto Europa 2015

Better in than out? Economic performance inside and outside the European monetary union Rapporto Europa 2015 Roma, 9.7.2015 1 Table of Content I. The political threat Why European monetary union? II. Europe

Better in than out? Economic performance inside and outside the European monetary union Rapporto Europa 2015 Roma, 9.7.2015 1 Table of Content I. The political threat Why European monetary union? II. Europe

Grasshoppers, Ants and Locusts: the future of the world economy

Ralph Miliband Series on the Restructuring of World Power Grasshoppers, Ants and Locusts: the future of the world economy Martin Wolf Associate editor and chief economics commentator, Financial Times Professor

Ralph Miliband Series on the Restructuring of World Power Grasshoppers, Ants and Locusts: the future of the world economy Martin Wolf Associate editor and chief economics commentator, Financial Times Professor

Seven Lean Years Explaining Persistent Global Economic Weakness

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Vignettes on Greece. Daniel Gros. Panel discussion Euro-crisis & Greece March 20, 2013 l Hellenic Observatory l London

Vignettes on Greece by Daniel Gros Panel discussion Euro-crisis & Greece March 20, 2013 l Hellenic Observatory l London Thinking ahead for Europe Centre for European Policy Studies (CEPS) www.ceps.eu Outline:

Vignettes on Greece by Daniel Gros Panel discussion Euro-crisis & Greece March 20, 2013 l Hellenic Observatory l London Thinking ahead for Europe Centre for European Policy Studies (CEPS) www.ceps.eu Outline:

Global Economic Outlook. Kellie Maske, Sr. Economics Fellow FedEx Corporate Economics September 2011

Kellie Maske, Sr. Economics Fellow FedEx Corporate Economics U.S. Outlook: Moderate Growth Overall 6 4 US Real GDP Growth 2 % Change 0 (2) (4) Forecast (6) (8) Bars = QOQ% Annualized Line = YOY% (10) 2005

Kellie Maske, Sr. Economics Fellow FedEx Corporate Economics U.S. Outlook: Moderate Growth Overall 6 4 US Real GDP Growth 2 % Change 0 (2) (4) Forecast (6) (8) Bars = QOQ% Annualized Line = YOY% (10) 2005

World real GDP growth in 2010 Annual percent change

World real GDP growth in 2010 Annual percent change 1 or more 6-1 3-6% 0-3% Less than No data Source: International Monetary Fund. World real GDP growth in 2011 Annual percent change 1 or more 6-1 3-6%

World real GDP growth in 2010 Annual percent change 1 or more 6-1 3-6% 0-3% Less than No data Source: International Monetary Fund. World real GDP growth in 2011 Annual percent change 1 or more 6-1 3-6%

After the British referendum

Future of Europe After the British referendum Broader issues for the UK and the EU David Marsh, Managing Director, OMFIF 27 October 2016 Nicosia 1 European politics moves against integration A new phase

Future of Europe After the British referendum Broader issues for the UK and the EU David Marsh, Managing Director, OMFIF 27 October 2016 Nicosia 1 European politics moves against integration A new phase

Finland s sawmilling industry

Finland s sawmilling industry Howard Sidney-Wilmot Stora Enso - Sales Director UK, Ireland & Benelux September 2015 Stora Enso Wood Products 13/10/2015 1 Finland s forest products 19bn total value 11bn

Finland s sawmilling industry Howard Sidney-Wilmot Stora Enso - Sales Director UK, Ireland & Benelux September 2015 Stora Enso Wood Products 13/10/2015 1 Finland s forest products 19bn total value 11bn

AREA TOTALS OECD Composite Leading Indicators. OECD Total. OECD + Major 6 Non Member Countries. Major Five Asia. Major Seven.

Reference series Composite leading indicators OECD Composite Leading Indicators AREA TOTALS 7-03- 19 OECD Total 19 OECD + Major 6 Non Member Countries 19 Major Seven 19 Major Five Asia 19 Euro area 19

Reference series Composite leading indicators OECD Composite Leading Indicators AREA TOTALS 7-03- 19 OECD Total 19 OECD + Major 6 Non Member Countries 19 Major Seven 19 Major Five Asia 19 Euro area 19

RISI EUROPEAN CONFERENCE. (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last?

The European Economy Things look good just now. Can this last?") RISI EUROPEAN CONFERENCE (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last? Andrea Boltho Magdalen College University of Oxford and Oxford Economics CONCLUSIONS OF

RISI EUROPEAN CONFERENCE (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last? Andrea Boltho Magdalen College University of Oxford and Oxford Economics CONCLUSIONS OF

Impacts of the Global Economy on Asia Pacific Travel. 29 June 2007 John Walker

Impacts of the Global Economy on Asia Pacific Travel 29 June 2007 John Walker jwalker@oxfordeconomics.com Oxford Economics Founded in 1981 Over 300 clients including blue chip companies and government

Impacts of the Global Economy on Asia Pacific Travel 29 June 2007 John Walker jwalker@oxfordeconomics.com Oxford Economics Founded in 1981 Over 300 clients including blue chip companies and government

The structure of the euro area recovery

The structure of the euro area recovery Rolf Strauch, Chief Economist JPMorgan Investor Seminar, IMF Annual Meetings Washington, October 2017 The euro area: a systemic player in global trade Trade openness

The structure of the euro area recovery Rolf Strauch, Chief Economist JPMorgan Investor Seminar, IMF Annual Meetings Washington, October 2017 The euro area: a systemic player in global trade Trade openness

Global economic cycle has slowed

Year-on-year % change Confidence index, 50= no change Global economic cycle has slowed 25% 70 20% International trade growth 65 15% 10% Industrial production growth 60 5% 55 0% 50-5% Business confidence

Year-on-year % change Confidence index, 50= no change Global economic cycle has slowed 25% 70 20% International trade growth 65 15% 10% Industrial production growth 60 5% 55 0% 50-5% Business confidence

Turkey: Recent Developments and Future Prospects. ISBANK Economic Research Division November 2018

Turkey: Recent Developments and Future Prospects ISBANK Economic Research Division November 2018 Macroeconomic Outlook Strong Economic Growth Cycle GDP of 851 bn USD (2017), 10.6k USD (2017) per capita

Turkey: Recent Developments and Future Prospects ISBANK Economic Research Division November 2018 Macroeconomic Outlook Strong Economic Growth Cycle GDP of 851 bn USD (2017), 10.6k USD (2017) per capita

Despite geopolitical woes Lithuania s economy enjoys balanced growth

Lithuanian Economic Outlook Despite geopolitical woes Lithuania s economy enjoys balanced growth Indrė Genytė-Pikčienė Chief analyst Economic Research Department DNB Markets 30 th of May, 2014 2000 I 2000

Lithuanian Economic Outlook Despite geopolitical woes Lithuania s economy enjoys balanced growth Indrė Genytė-Pikčienė Chief analyst Economic Research Department DNB Markets 30 th of May, 2014 2000 I 2000

Outline. Overview of globalization. Global outlook for real economic activity & inflation. Risks to the outlook

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD?

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD? FROM BUST TO BOOM. AN EPIC BUST After 16 years of growth with a short pause for breath in 2002, the Icelandic economy entered

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD? FROM BUST TO BOOM. AN EPIC BUST After 16 years of growth with a short pause for breath in 2002, the Icelandic economy entered

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

NEW COMMERCIAL VEHICLE REGISTRATIONS EUROPEAN UNION 1. July and August 2017

PRESS EMBARGO: NEW COMMERCIAL VEHICLE REGISTRATIONS EUROPEAN UNION 1 July and August 2017 Next press release: Tuesday 24 October 2017 1 Data for Malta unavailable Page 1 of 12 Commercial vehicle registrations:

PRESS EMBARGO: NEW COMMERCIAL VEHICLE REGISTRATIONS EUROPEAN UNION 1 July and August 2017 Next press release: Tuesday 24 October 2017 1 Data for Malta unavailable Page 1 of 12 Commercial vehicle registrations:

sector: recent developments VÍTOR CONSTÂNCIO

The economy and the banking sector: recent developments VÍTOR CONSTÂNCIO January 2006 Recent performance of the economy and prospects Factors behind the period of slow growth Challenges to the Banking

The economy and the banking sector: recent developments VÍTOR CONSTÂNCIO January 2006 Recent performance of the economy and prospects Factors behind the period of slow growth Challenges to the Banking

Economic Outlook: fear over fundamentals

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

Lecture 3 The Lisbon Strategy

Lecture 3 The Lisbon Strategy Outline The Lisbon European Council held in March 2000 recognized the need of reforming labour,, product, and financial markets in order the performance of the EU economy

Lecture 3 The Lisbon Strategy Outline The Lisbon European Council held in March 2000 recognized the need of reforming labour,, product, and financial markets in order the performance of the EU economy

Economic & Financial Market Outlook

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

Airlines, the economy and air transport demand

Airlines, the economy and air transport demand Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 Returns for airlines investors lower this year;

Airlines, the economy and air transport demand Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 Returns for airlines investors lower this year;

Global Economic Indicators: Eurozone Trade

Global Economic Indicators: Eurozone Trade November 15, 216 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 48-664-1333 djohnson@ Please visit our sites at www. blog. thinking outside the box

Global Economic Indicators: Eurozone Trade November 15, 216 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 48-664-1333 djohnson@ Please visit our sites at www. blog. thinking outside the box

Global Economic Indicators: Eurozone Trade

Global Economic Indicators: Eurozone Trade January 15, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 48-664-1333 djohnson@ Please visit our sites at www. blog. thinking outside the box Table

Global Economic Indicators: Eurozone Trade January 15, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 48-664-1333 djohnson@ Please visit our sites at www. blog. thinking outside the box Table

Economic potential of Agriculture and Pig production in Baltic region. Mindaugas Jurgelis, analyst 30 May, 2012

Economic potential of Agriculture and Pig production in Baltic region Mindaugas Jurgelis, analyst 30 May, 2012 1 Global tendencies of food production 2 Food prices near historical peak level FAO food price

Economic potential of Agriculture and Pig production in Baltic region Mindaugas Jurgelis, analyst 30 May, 2012 1 Global tendencies of food production 2 Food prices near historical peak level FAO food price

The Economy of Finland

The Economy of Finland Aug 30st 2013, Finnish Ministry of Foreign Affairs Presentation for the American Fulbright Grantees Petteri Rautaporras, Economist at the Federation of Finnish Technology Industries

The Economy of Finland Aug 30st 2013, Finnish Ministry of Foreign Affairs Presentation for the American Fulbright Grantees Petteri Rautaporras, Economist at the Federation of Finnish Technology Industries

Macroeconomic Imbalances in

Macroeconomic Imbalances in the Euro Area Jürgen von Hagen Rome, 21 May 2011 Europe: Growing imbalances within, balanced without 8 6 4 2 0-2 -4-6 10 Figure 1A: Current Account Balances IE EL FR FI IT SE

Macroeconomic Imbalances in the Euro Area Jürgen von Hagen Rome, 21 May 2011 Europe: Growing imbalances within, balanced without 8 6 4 2 0-2 -4-6 10 Figure 1A: Current Account Balances IE EL FR FI IT SE

What is the outlook for the prime residential markets?

What is the outlook for the prime residential markets? Katy Warrick Market Update Mat Oakley Commercial View Lucian Cook Residential Forecasts Emily Donovan London Development Living in uncertain times

What is the outlook for the prime residential markets? Katy Warrick Market Update Mat Oakley Commercial View Lucian Cook Residential Forecasts Emily Donovan London Development Living in uncertain times

GLOBAL ECONOMICS, REAL ESTATE PRICING & OUTLOOK FOR 2017 RICHARD BARKHAM GLOBAL CHIEF ECONOMIST

GLOBAL ECONOMICS, REAL ESTATE PRICING & OUTLOOK FOR 2017 RICHARD BARKHAM GLOBAL CHIEF ECONOMIST BREXIT TRUMPISM EURO-TRUMPISM 4 ECONOMICS, PRICING & OUTLOOK FOR 2017 LET S GET GEOPOLITICS IN PERSPECTIVE

GLOBAL ECONOMICS, REAL ESTATE PRICING & OUTLOOK FOR 2017 RICHARD BARKHAM GLOBAL CHIEF ECONOMIST BREXIT TRUMPISM EURO-TRUMPISM 4 ECONOMICS, PRICING & OUTLOOK FOR 2017 LET S GET GEOPOLITICS IN PERSPECTIVE

The economic value of the EU shipping industry. Andrew P Goodwin

The economic value of the EU shipping industry Andrew P Goodwin 2 nd April 2014 Introduction Shipping is a vital facilitator of world trade 135 % Increase in world GDP in the last two decades 180 % Increase

The economic value of the EU shipping industry Andrew P Goodwin 2 nd April 2014 Introduction Shipping is a vital facilitator of world trade 135 % Increase in world GDP in the last two decades 180 % Increase

Reading the Tea Leaves: Investing for 2010 and Beyond

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

Global growth forecasts Key countries/regions,

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition May 7 and 8, 2013 İstanbul, Turkey Outline 1 The Financial System 2 Weak Growth 3 4 5 Unprecedented

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition May 7 and 8, 2013 İstanbul, Turkey Outline 1 The Financial System 2 Weak Growth 3 4 5 Unprecedented

Beer statistics edition. The Brewers of Europe

Beer statistics 2017 edition The Brewers of Europe Beer statistics 2017 edition The Brewers of Europe December 2017 ISBN 978-2-9601382-9-0 EAN 9782960138290 1 TABLE OF CONTENTS Foreword by President

Beer statistics 2017 edition The Brewers of Europe Beer statistics 2017 edition The Brewers of Europe December 2017 ISBN 978-2-9601382-9-0 EAN 9782960138290 1 TABLE OF CONTENTS Foreword by President

Global Economic Outlook

Global Economic Outlook Mark A. Wynne Vice President & Associate Director of Research Director, Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas Presentation to Vistas Conference

Global Economic Outlook Mark A. Wynne Vice President & Associate Director of Research Director, Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas Presentation to Vistas Conference

Austria: Key Economic Features

Austria: Key Economic Features and EU Guanghua School of Management Josef Christl, Macro-Consult 16. Oktober 2017 Austria: a small, but rich country Population, mn. GDP per capita PPP, USD 1600 60000 1400

Austria: Key Economic Features and EU Guanghua School of Management Josef Christl, Macro-Consult 16. Oktober 2017 Austria: a small, but rich country Population, mn. GDP per capita PPP, USD 1600 60000 1400

The Shifts and the Shocks Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

The Shifts and the Shocks Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times Peterson Institute for International Economics 9 th October 2014 Washington DC The Shifts and the

The Shifts and the Shocks Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times Peterson Institute for International Economics 9 th October 2014 Washington DC The Shifts and the

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

Social Convergence, Development Failures and Industrial Relations: The Case of Portugal

Social Convergence, Development Failures and Industrial Relations: The Case of Pilar González Faculty of Economics, University of Porto António Figueiredo Quaternaire Context joined the EU with very low

Social Convergence, Development Failures and Industrial Relations: The Case of Pilar González Faculty of Economics, University of Porto António Figueiredo Quaternaire Context joined the EU with very low

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis. May 8 th, Presented by:

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis May 8 th, 2008 Presented by: Patricia Croft, Vice President & Chief Economist Phillips, Hager & North Investment Management Limited

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis May 8 th, 2008 Presented by: Patricia Croft, Vice President & Chief Economist Phillips, Hager & North Investment Management Limited

Conference SMEs and the Euro. The Financial Impact of the Euro on SMEs

Conference SMEs and the Euro The Financial Impact of the Euro on SMEs Brussels, October 18, 2007 Doris Ritzberger-Grünwald Head, Foreign Research Division ceec.oenb.at 1 www.oenb.at oenb.info@oenb.at Overview

Conference SMEs and the Euro The Financial Impact of the Euro on SMEs Brussels, October 18, 2007 Doris Ritzberger-Grünwald Head, Foreign Research Division ceec.oenb.at 1 www.oenb.at oenb.info@oenb.at Overview

Economic development the challenge of the new normal

Economic development the challenge of the new normal Neil Gibson, Director of Regional Services 24th November 2010 Overview The new normal globally The new normal in Northern Ireland Inequalities and imbalances

Economic development the challenge of the new normal Neil Gibson, Director of Regional Services 24th November 2010 Overview The new normal globally The new normal in Northern Ireland Inequalities and imbalances

Montreal Real Estate Forum. Economic Outlooks for March 31, Cooperating in building the future

Montreal Real Estate Forum March 31, 2015 Economic Outlooks for 2015 François Dupuis Vice-President and Chief Economist Desjardins Group Cooperating in building the future Outline The global economy and

Montreal Real Estate Forum March 31, 2015 Economic Outlooks for 2015 François Dupuis Vice-President and Chief Economist Desjardins Group Cooperating in building the future Outline The global economy and

The Eurozone integration, des-integration and possible future developments

The Eurozone integration, des-integration and possible future developments 18 th Monetary Policy Workshop at the Berlin School of Economcs and Law, 12 13 October 2017 Overview Position 1: The euro itself

The Eurozone integration, des-integration and possible future developments 18 th Monetary Policy Workshop at the Berlin School of Economcs and Law, 12 13 October 2017 Overview Position 1: The euro itself

Macro-economic risk and the outlook for aviation

Macro-economic risk and the outlook for aviation 25 th January 2018, Dublin Brian Pearce, Chief Economist, IATA www.iata.org/economics Macro matters 24% 20% Global GDP and RPK growth 12% 10% 16% 12% 8%

Macro-economic risk and the outlook for aviation 25 th January 2018, Dublin Brian Pearce, Chief Economist, IATA www.iata.org/economics Macro matters 24% 20% Global GDP and RPK growth 12% 10% 16% 12% 8%

Global Construction Outlook: Laura Hanlon Product Manager, Global Construction Outlook May 21, 2009

Global Construction Outlook: Short-term term Pain, Long-term Gain Laura Hanlon Product Manager, Global Construction Outlook May 21, 2009 What This Means for You The world is set to be hit this year with

Global Construction Outlook: Short-term term Pain, Long-term Gain Laura Hanlon Product Manager, Global Construction Outlook May 21, 2009 What This Means for You The world is set to be hit this year with

The Great Convergence: China, India and the new global economy. Mark Thirlwell Program Director, International Economy July 2006

The Great Convergence: China, India and the new global economy Mark Thirlwell Program Director, International Economy July 2006 India Two views of the largest economies in 2005 Top 12 economies by GDP,

The Great Convergence: China, India and the new global economy Mark Thirlwell Program Director, International Economy July 2006 India Two views of the largest economies in 2005 Top 12 economies by GDP,

Global Economic Indicators: Global Leading Indicators

Global Economic Indicators: Global Leading Indicators November 27, 2017 Dr. Edward Yardeni 516-2-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit

Global Economic Indicators: Global Leading Indicators November 27, 2017 Dr. Edward Yardeni 516-2-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit

Vermont Economic Conference:

Vermont Economic Conference: Mapping Our Economic Future Michael Dolega Director & Senior Economist TD Economics January 5 2018 Summary Global economy gathering speed, leading to another upgrade in outlook.

Vermont Economic Conference: Mapping Our Economic Future Michael Dolega Director & Senior Economist TD Economics January 5 2018 Summary Global economy gathering speed, leading to another upgrade in outlook.

Beer statistics edition. The Brewers of Europe

Beer statistics 2016 edition The Brewers of Europe Beer statistics 2016 edition The Brewers of Europe November 2016 ISBN 978-2-9601382-7-6 EAN 9782960138276 1 TABLE OF CONTENTS Foreword by President

Beer statistics 2016 edition The Brewers of Europe Beer statistics 2016 edition The Brewers of Europe November 2016 ISBN 978-2-9601382-7-6 EAN 9782960138276 1 TABLE OF CONTENTS Foreword by President

BC Pension Forum. Economic Outlook. Presented by: Ben Homsy, CFA Portfolio Manager

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

From Recession to Recovery

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

Federal Reserve Bank of Dallas, FIRM (Financial Institution Relationship Management)

") The Economic Roller Coaster: Where Have We Been? And Where Are We Going? Thomas F. Siems, Ph.D. Senior Economist and Director of Economic Outreach Federal Reserve Bank of Dallas Economic Summit Dallas

The Economic Roller Coaster: Where Have We Been? And Where Are We Going? Thomas F. Siems, Ph.D. Senior Economist and Director of Economic Outreach Federal Reserve Bank of Dallas Economic Summit Dallas

Bank Profitability and Macroeconomic Factors

Bank Profitability and Macroeconomic Factors Ricardo Martinho Banco de Portugal João Gouveia de Oliveira Banco de Portugal & Nova SBE Vitor Oliveira Banco de Portugal 17 October 2017 Lisbon Conference

Bank Profitability and Macroeconomic Factors Ricardo Martinho Banco de Portugal João Gouveia de Oliveira Banco de Portugal & Nova SBE Vitor Oliveira Banco de Portugal 17 October 2017 Lisbon Conference

Composition of Federal Spending

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

Ministry of Economy and Sustainable Development of Georgia

Ministry of Economy and Sustainable Development of Georgia Economic Growth 42,000.0 36,000.0 30,000.0 24,000.0 18,000.0 12,000.0 6,000.0 0.0 GDP AND ECONOMIC GROWTH 7.2% 6.2% 6.4% 4.6% 4.8% 3.4% 2.9% 2.8%

Ministry of Economy and Sustainable Development of Georgia Economic Growth 42,000.0 36,000.0 30,000.0 24,000.0 18,000.0 12,000.0 6,000.0 0.0 GDP AND ECONOMIC GROWTH 7.2% 6.2% 6.4% 4.6% 4.8% 3.4% 2.9% 2.8%

OECD employment rate increases to 68.4% in the third quarter of 2018

Paris, 17th January 2019 News Release: 3rd Quarter 2018 OECD employment rate increases to 68.4% in the third quarter of 2018 The OECD area employment rate the share of the working-age population with jobs

Paris, 17th January 2019 News Release: 3rd Quarter 2018 OECD employment rate increases to 68.4% in the third quarter of 2018 The OECD area employment rate the share of the working-age population with jobs

Fibre to the Home: Taking your life to new horizons!

Fibre to the Home: Taking your life to new horizons! Hartwig Tauber, Director General FTTH Council Europe Press Conference - Milan, 13 January 2011 FTTH Council Europe Photo by Nicolo Baravalle FTTH Council

Fibre to the Home: Taking your life to new horizons! Hartwig Tauber, Director General FTTH Council Europe Press Conference - Milan, 13 January 2011 FTTH Council Europe Photo by Nicolo Baravalle FTTH Council

IRELAND: EUROPE S FASTEST GROWING ECONOMY

IRELAND: EUROPE S FASTEST GROWING ECONOMY Remarkable turnaround story continues to get better S&P Capital IQ June 9 th, 2015 Index Page 3: Macroeconomy Page 13: Fiscal & NTMA Funding Page 23: Rebalancing

IRELAND: EUROPE S FASTEST GROWING ECONOMY Remarkable turnaround story continues to get better S&P Capital IQ June 9 th, 2015 Index Page 3: Macroeconomy Page 13: Fiscal & NTMA Funding Page 23: Rebalancing

Architecture - the Market

2 Architecture - the Market Architect: Ibelings van Tilburg architecten Project: De Karel Doorman Winner of the BNA Building of the Year 2013 Public Prize Photographer: Ossip van Duivenbode Place: Rotterdam

2 Architecture - the Market Architect: Ibelings van Tilburg architecten Project: De Karel Doorman Winner of the BNA Building of the Year 2013 Public Prize Photographer: Ossip van Duivenbode Place: Rotterdam

DEVELOPMENT AID AT A GLANCE

DEVELOPMENT AID AT A GLANCE STATISTICS BY REGION 5. EUROPE 2018 edition All the data in this report are available at: http://www.oecd.org/dac/financing-sustainable-development/ 5.1. ODA TO EUROPE - SUMMARY

DEVELOPMENT AID AT A GLANCE STATISTICS BY REGION 5. EUROPE 2018 edition All the data in this report are available at: http://www.oecd.org/dac/financing-sustainable-development/ 5.1. ODA TO EUROPE - SUMMARY

Panel on Post-Crisis Growth Performance Determinants, Effects and Policy Implications

Panel on Post-Crisis Growth Performance Determinants, Effects and Policy Implications Carmen M. Harvard University Bank of Canada and European Central Bank Conference Ottawa, June 8-9, 2015 1 Outline (i)

Panel on Post-Crisis Growth Performance Determinants, Effects and Policy Implications Carmen M. Harvard University Bank of Canada and European Central Bank Conference Ottawa, June 8-9, 2015 1 Outline (i)

Market Insights. March 29, 2019

March 29, 2019 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.2% 1.4% 2.1% 2.3% 1.7% 2.4% 2.3%

March 29, 2019 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.2% 1.4% 2.1% 2.3% 1.7% 2.4% 2.3%

Market Insights. June 30, 2018

June 30, 2018 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.7% 1.2% 1.3% 2.1% 2.3% 1.7% 2.3%

June 30, 2018 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.7% 1.2% 1.3% 2.1% 2.3% 1.7% 2.3%

Max Sort Sortation Option - Letters

Max Sort Sortation Option - Letters Western Europe Prices Product Code PS5 PS6 Austria* 0.330 7.550 0.330 7.400 Belgium* 0.370 3.700 0.370 3.540 Denmark* 0.620 5.350 0.620 4.215 Finland* 0.385 4.400 0.385

Max Sort Sortation Option - Letters Western Europe Prices Product Code PS5 PS6 Austria* 0.330 7.550 0.330 7.400 Belgium* 0.370 3.700 0.370 3.540 Denmark* 0.620 5.350 0.620 4.215 Finland* 0.385 4.400 0.385

Airline industry outlook 2019

Airline industry outlook 2019 Brian Pearce Chief Economist 12 December 2018 Million barrels a day US$ per barrel Are the markets signalling recession ahead? 60 55 Business confidence (left scale) FTSE

Airline industry outlook 2019 Brian Pearce Chief Economist 12 December 2018 Million barrels a day US$ per barrel Are the markets signalling recession ahead? 60 55 Business confidence (left scale) FTSE

Embassy of Hungary. Invest in Hungary. HE Péter Szabadhegy Ambassador of Hungary

Invest in Hungary HE Péter Szabadhegy Ambassador of Hungary AstraZeneca s HQ at Alderely Park 25 March 2015 Hungary In the Heart of Europe Your gate to a market of 500 million customers Capital: Budapest

Invest in Hungary HE Péter Szabadhegy Ambassador of Hungary AstraZeneca s HQ at Alderely Park 25 March 2015 Hungary In the Heart of Europe Your gate to a market of 500 million customers Capital: Budapest

Chief Economist s Report

Chief Economist s Report 22 February 2017 IATA Legal Symposium, Washington Brian Pearce Chief Economist, IATA Airline Industry Economics Advisory Workshop 2016 1 Themes 1. World economy still stuck on

Chief Economist s Report 22 February 2017 IATA Legal Symposium, Washington Brian Pearce Chief Economist, IATA Airline Industry Economics Advisory Workshop 2016 1 Themes 1. World economy still stuck on

Dick Vos Senior Manager Research & Strategy

Dick Vos Senior Manager Research & Strategy! House prices now falling at fastest rate since early 1990s House prices will fall 7% in 'uncertain' market IMF warns on global house prices House prices Through

Dick Vos Senior Manager Research & Strategy! House prices now falling at fastest rate since early 1990s House prices will fall 7% in 'uncertain' market IMF warns on global house prices House prices Through

GDP GDP , 2004, (%) 2002, ) EU15=100, 2002 EU25

2002, ) EU15=100, 2002 EU25") Europe - Profile Total Population Unemployment GDP GDP per capita 2004, (Mil.) Rate 2004, (%) 2002, (Bil. ) EU15=100, 2002 EU25 454.9 9.0 9,613 91 EU15 380.8 8.0 9,169 100 10 ACC. 74.1 14.3 444 47 U.S.

Europe - Profile Total Population Unemployment GDP GDP per capita 2004, (Mil.) Rate 2004, (%) 2002, (Bil. ) EU15=100, 2002 EU25 454.9 9.0 9,613 91 EU15 380.8 8.0 9,169 100 10 ACC. 74.1 14.3 444 47 U.S.

History of the European Monetary Integration

History of the European Monetary Integration European Payment Union (1950-1958) Facilitated multilateral clearing of payment imbalances. The Bank of International Settlements acted as a clearing house.

History of the European Monetary Integration European Payment Union (1950-1958) Facilitated multilateral clearing of payment imbalances. The Bank of International Settlements acted as a clearing house.

Beer statistics edition. The Brewers of Europe

Beer statistics 2015 edition The Brewers of Europe Beer statistics 2015 edition The Brewers of Europe Editor: Marlies Van de Walle October 2015 ISBN 978-2-9601382-5-2 EAN 9782960138252 1 TABLE OF CONTENTS

Beer statistics 2015 edition The Brewers of Europe Beer statistics 2015 edition The Brewers of Europe Editor: Marlies Van de Walle October 2015 ISBN 978-2-9601382-5-2 EAN 9782960138252 1 TABLE OF CONTENTS

CURRENT DEMOGRAPHIC SITUATION IN LATVIA

CURRENT DEMOGRAPHIC SITUATION IN LATVIA Peteris Zvidrins University of Latvia Workshop Very old people s housing and housing and health situation in Latvia 21 May, 2013 Population and its change in 10

CURRENT DEMOGRAPHIC SITUATION IN LATVIA Peteris Zvidrins University of Latvia Workshop Very old people s housing and housing and health situation in Latvia 21 May, 2013 Population and its change in 10

Global trade: how does it look?

Edmonton, December 2018 Global trade: how does it look? Marie-France Paquet The Office of the Chief Economist Global Affairs Canada Overview 1. Canadian economy at a glance 2. Provincial economy at a glance

Edmonton, December 2018 Global trade: how does it look? Marie-France Paquet The Office of the Chief Economist Global Affairs Canada Overview 1. Canadian economy at a glance 2. Provincial economy at a glance

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

PwC Automotive Global Future of the Auto Sector Felix Kuhnert, European Automotive Leader 06 November 2012

www.pwc.com Automotive Global Future of the Auto Sector Felix Kuhnert, European Automotive Leader Agenda Page 1 Global Snapshot 1 2 Fasten your seatbelt! Turbulence in Europe ahead! 6 3 Growth takes place

www.pwc.com Automotive Global Future of the Auto Sector Felix Kuhnert, European Automotive Leader Agenda Page 1 Global Snapshot 1 2 Fasten your seatbelt! Turbulence in Europe ahead! 6 3 Growth takes place

WDF Europe Cup Men: Pairs

WDF Europe Cup - Men: Pairs // :: Last - Best of legs : : : Smith/Maya-Spain-B Bless/Bellmont-Switzerland-A Lukasiak/Torbj rnsson-sweden-b Sivertsen/Knudsen-Norway-A Sakys/Jankunas-Lithuania-B Niskala/Finnali!-Finland-B

WDF Europe Cup - Men: Pairs // :: Last - Best of legs : : : Smith/Maya-Spain-B Bless/Bellmont-Switzerland-A Lukasiak/Torbj rnsson-sweden-b Sivertsen/Knudsen-Norway-A Sakys/Jankunas-Lithuania-B Niskala/Finnali!-Finland-B

TEGMA Fall Transportation Symposium

TEGMA 2017 Fall Transportation Symposium John Wilson Senior Vice President Dairy industry trends 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Million

TEGMA 2017 Fall Transportation Symposium John Wilson Senior Vice President Dairy industry trends 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Million

Further Opening Up and Reform of China s Capital Market

Further Opening Up and Reform of China s Capital Market Haizhou Huang January 7, 2016 China economy and capital market: Finding new normal 1 Macro: We expect China GDP to grow 6.9% in 2015 and 6.8% in

Further Opening Up and Reform of China s Capital Market Haizhou Huang January 7, 2016 China economy and capital market: Finding new normal 1 Macro: We expect China GDP to grow 6.9% in 2015 and 6.8% in

The outlook: what we know, the known unknowns and the unknown unknowns

The outlook: what we know, the known unknowns and the unknown unknowns 24 April 2017 Seoul Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1

The outlook: what we know, the known unknowns and the unknown unknowns 24 April 2017 Seoul Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1

Demographic change, long-run housing demand and the related challenges for the Irish banking sector

Demographic change, long-run housing demand and the related challenges for the Irish banking sector December 5 th, 2016 esri.ie David Duffy, Daniel Foley, Kieran McQuinn and Niall McInerney Outline: Addresses

Demographic change, long-run housing demand and the related challenges for the Irish banking sector December 5 th, 2016 esri.ie David Duffy, Daniel Foley, Kieran McQuinn and Niall McInerney Outline: Addresses

Can China Pilot a Soft Landing? 2017 Article IV Consultation Analysis, Outlook, and Policy Advice

Can China Pilot a Soft Landing? 2017 Article IV Consultation Analysis, Outlook, and Policy Advice September 2017 1 KEY RECENT DEVELOPMENTS China has had strong growth momentum which Real GDP Real GDP Stabilizes

Can China Pilot a Soft Landing? 2017 Article IV Consultation Analysis, Outlook, and Policy Advice September 2017 1 KEY RECENT DEVELOPMENTS China has had strong growth momentum which Real GDP Real GDP Stabilizes

The Euro Area: A Reality Check

Fletcher School, Tufts University The Euro Area: A Reality Check Prof. George Alogoskoufis Monetary Cooperation in Europe Four sub-periods in the evolution of monetary cooperation in the European Union.

Fletcher School, Tufts University The Euro Area: A Reality Check Prof. George Alogoskoufis Monetary Cooperation in Europe Four sub-periods in the evolution of monetary cooperation in the European Union.

A Giant Producer, & An Emerging Giant Consumer/Investor. Hong Liang

A Giant Producer, & An Emerging Giant Consumer/Investor China s Role in Global Trade and Investment Hong Liang Chief Economist, Head of Research October, 2016 I China: A global manufacturing power house,

A Giant Producer, & An Emerging Giant Consumer/Investor China s Role in Global Trade and Investment Hong Liang Chief Economist, Head of Research October, 2016 I China: A global manufacturing power house,

Romania nominal and real convergence on the way to euro adoption

Romania nominal and real convergence on the way to euro adoption Ionut Dumitru President of the Fiscal Council and Chief-economist, Raiffeisen Bank Romania February 2015 Eurozone enlargement current status

Romania nominal and real convergence on the way to euro adoption Ionut Dumitru President of the Fiscal Council and Chief-economist, Raiffeisen Bank Romania February 2015 Eurozone enlargement current status

The Herzliya Indices. National Security Balance The Civilian Quantitative Dimension. Herzliya Conference Prof. Rafi Melnick, IDC Herzliya

The Herzliya Indices National Security Balance The Civilian Quantitative Dimension Herzliya Conference 2015 Prof. Rafi Melnick, IDC Herzliya 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

The Herzliya Indices National Security Balance The Civilian Quantitative Dimension Herzliya Conference 2015 Prof. Rafi Melnick, IDC Herzliya 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

ABA Commercial Real Estate Lending Committee

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

EUROPEAN RIDERS, HORSES AND SHOWS AT THE FEI 2012

EUROPEAN RIDERS, HORSES AND SHOWS AT THE FEI 2012 Presentation to the EEF Sports Forum Essen, 21 st March 2013 1 Introduction In 2010 the Small Nations Working Group started this study, to know exactly

EUROPEAN RIDERS, HORSES AND SHOWS AT THE FEI 2012 Presentation to the EEF Sports Forum Essen, 21 st March 2013 1 Introduction In 2010 the Small Nations Working Group started this study, to know exactly

Canadian Housing In Flux

Dr. Sherry Cooper Chief Economist Dominion Lending Centres The Title of the presentation Second line if needed Third line if needed Canadian Housing In Flux Today s date Location of presentation March

Dr. Sherry Cooper Chief Economist Dominion Lending Centres The Title of the presentation Second line if needed Third line if needed Canadian Housing In Flux Today s date Location of presentation March

Universities and the Education Revolution. Professor Richard Larkins Chair, Universities Australia VC and President Monash University

Universities and the Education Revolution Professor Richard Larkins Chair, Universities Australia VC and President Monash University Role of Universities in Prosperity Third largest earner of export dollars

Universities and the Education Revolution Professor Richard Larkins Chair, Universities Australia VC and President Monash University Role of Universities in Prosperity Third largest earner of export dollars