Economic Outlook. Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project

|

|

|

- Teresa Bryant

- 6 years ago

- Views:

Transcription

1 Economic Outlook Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project League of California Cities Monterey, CA December 3, 2014

2 Economic Update economic data providing mixed signals but they always do!!! important to take a long-run view

3 Real GDP Logged Billions of 2009$, Seasonally Adjusted Economic Forecast Project Source: BEA

4 Real Per Capita GDP Log, 1990 int. GK$ Economic Forecast Project Source: Angus Maddison

5 Real GDP Logged Billions of 2009$, Seasonally Adjusted Linear Trend Economic Forecast Project Source: BEA

6 GDP Growth During an Expansion Average, annualized rate of change Q Q Q Q Q Q Q Q Q Q2 Economic Forecast Project Trough Date Source: BEA

7 Forward Guidance for Today s Talk describe current conditions globally, nationally and locally discuss Fed policy reactions QE3...gone but not forgotten CA outlook

8 Real GDP Growth Annualized percent change from last quarter quarterly change at an annual rate year over year change 2014 Q3 annualized growth rate Economic Forecast Project Source: BEA

9 Real Personal Consumption Expenditures Annualized percent change from last quarter Economic Forecast Project Source: BEA

10 S&P 500 Index 2000= Economic Forecast Project Source: BLS

11 Why Are You Spending so Little? uncertainty? already have everything? other issues out there in the world...

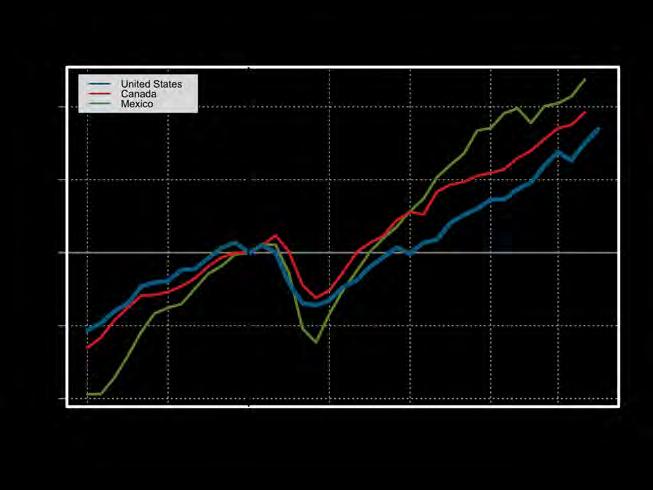

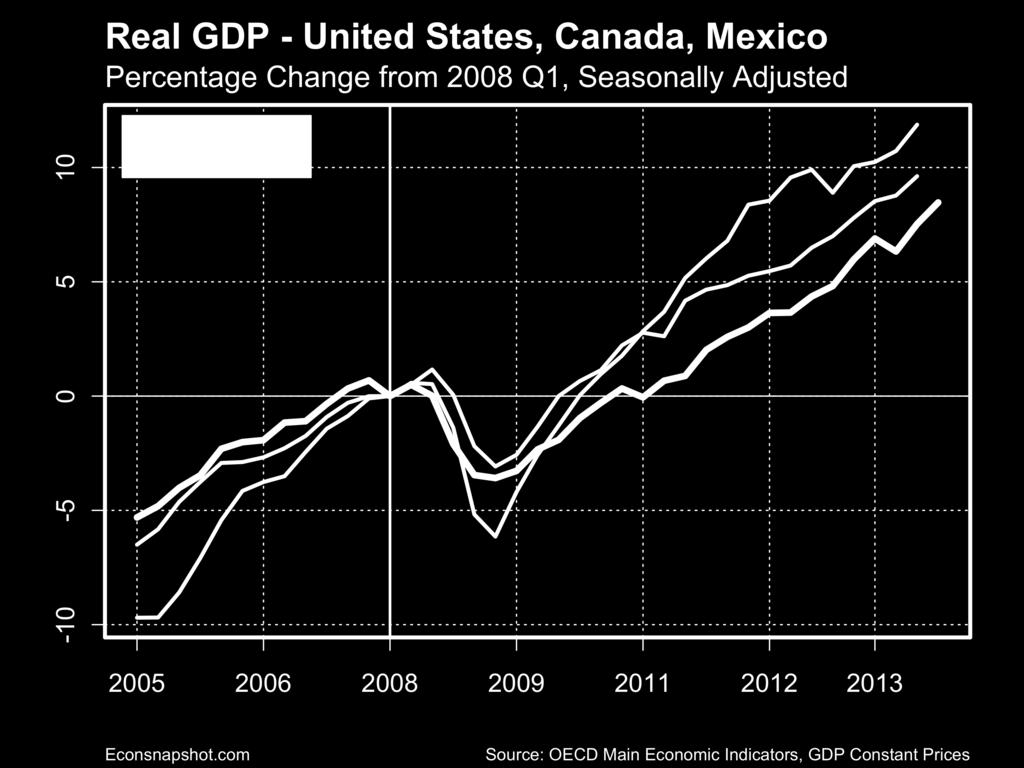

12 How Does the U.S. Compare? U.S. and some trading partners doing well...and some not...

13

14

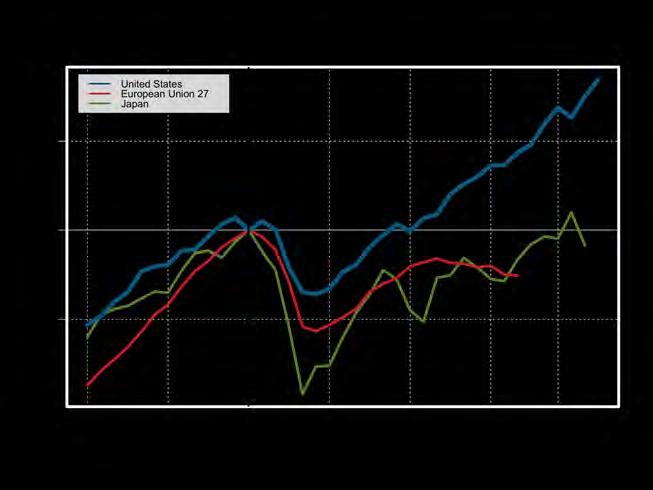

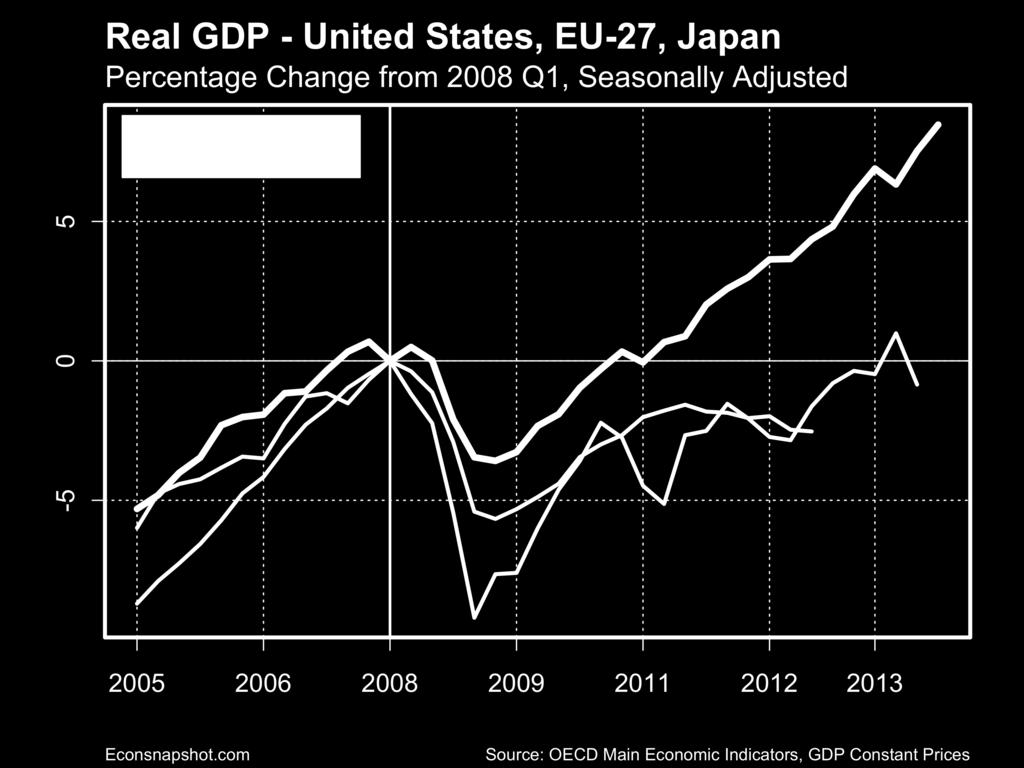

15 How Bad was Japan s Lost Decade

16 How Bad was Japan s Lost Decade Europe wishes it were Japan!!!

17 Real Gross Domestic Product United States (2007Q4=100) Japan (1991Q2=100) Europe (2008Q1=100) Cooley Rupert European Economic Snapshot; Source: Eurostat Quarters from Peak

18 Real Personal Consumption Expenditures United States (2007Q4=100) Japan (1991Q2=100) Europe (2008Q1=100) Cooley Rupert European Economic Snapshot; Source: Eurostat Quarters from Peak

19 Real Gross Fixed Capital Formation United States (2007Q4=100) Japan (1991Q2=100) Europe (2008Q1=100) Cooley Rupert European Economic Snapshot; Source: Eurostat Quarters from Peak

20 Financial Landscape households deleveraging portfolio rebalance

21 Household Leverage Liabilities to Income Economic Forecast Project Source: Flow of Funds, Federal Reserve

22 Checkable Deposits and Currency, Households Percent of GDP Economic Forecast Project Source: Flow of Funds, Federal Reserve

23 Household Net Worth (Assets Liabilities) Ratio to GDP Economic Forecast Project Source: Flow of Funds, Federal Reserve

24 Household s Summary...so far household net worth up consumption growth slow deleveraging

25 Financial Landscape business sector net worth still about 10% below peak cash holdings up

26 Net Worth, Nonfinancial Corporate Business Percent of GDP Economic Forecast Project Source: Flow of Funds, Federal Reserve

27 Checkable Deposits and Currency, NFCB Percent of GDP Economic Forecast Project Source: Flow of Funds, Federal Reserve

28 Banks Awash in Cash Too

29 Reserves Billions of Dollars Excess Reserves Required Reserves Total Reserves Cash Assets Economic Forecast Project Source: FRB St. Louis

30 And How About California s Finances? getting better...

31

32

33 Making Sense of Policy? to what does the Fed respond? two key elements inflation labor market

34 To What Does the Fed Respond? inflation Inflation has continued to run below the Committee s longer-run objective. Market-based measures of inflation compensation have declined somewhat; survey-based measures of longer-term inflation expectations have remained stable. (FOMC statement, October 29, 2014)

35 PCE, Chain type Price Index Percent change from last year Economic Forecast Project Source: BEA

36 5 Year Inflation Expectations Percent Economic Forecast Project Source: FRB St. Louis

37 To What Does the Fed Respond?...and wage growth is subdued

38 Hourly Earnings, Production and Salary Workers Percent change from a year ago Economic Forecast Project Source: BLS

39 The Point? no inflationary pressures...now or later

40 The Labor Market On balance, a range of labor market indicators suggests that underutilization of labor resources is gradually diminishing. (FOMC statement, October 29, 2014)

41 Unemployment Rate Percent Economic Forecast Project Source: BEA

42 Labor Force Participation Rate Percent All Age Age 55 and over Economic Forecast Project Source: BLS

43 Employment to Population Ratio Percent Economic Forecast Project Source: BLS

44 The Taylor Rule and Monetary Policy Measures how the Fed responds (historically)

45 Taylor Rule FF =.5*(6.0 URATE) INF +.5*(INF 2) Implied Taylor Rule Effective Fed Funds Rate Economic Forecast Project Source: BLS, BEA

46

47 A California Perspective employment diffusion index up...a quick aside

48 Unemployment Rate in Monterey County, Unadjusted 20 Percent (%) Source: California Employment Development Department Year

49 Unemployment Rate, Monterey County 20 Original Seasonally Adjusted Percent (%) Source: California Employment Development Department Year

50 Unemployment Rate in Santa Clara County, Unadjusted 12 Percent (%) Source: California Employment Development Department Year

51 Unemployment Rate, Santa Clara County 12 Original Seasonally Adjusted Percent (%) Source: California Employment Development Department Year

52 ...A California Perspective now back to the program

53

54

55 Housing a large decline prices rising...how fast? how far?

56 Zillow Home Value Index (ZHVI) Index (100 = Max Value) California [ $ 538,300 ] United States [ $ 196,400 ] efp.com Source: Zillow Research Data Note: Maximum value in brackets.

57 Zillow Home Value Index (ZHVI), by County Index (100 = Pre 2012 Max Value) San Francisco [ $ 822,500 ] Los Angeles [ $ 568,500 ] California [ $ 538,300 ] Santa Barbara [ $ 692,400 ] Monterey [ $ 685,600 ] San Joaquin [ $ 415,100 ] efp.com Source: Zillow Research Data Note: Pre 2012 Max Value value in brackets.

58 0 Peak to Trough Percentage Change, by County Bottom Six Counties Top Six Counties San Joaquin Stanislaus Solano Colusa Yuba Lake California Orange Humboldt San Mateo Santa Clara Marin San Francisco

59 Peak to Current Value Percentage Change, by County Bottom Six Counties Top Six Counties Lake Lassen San Joaquin Madera Colusa Stanislaus California Siskiyou Alameda Marin San Mateo Santa Clara San Francisco

60 Zillow Home Value Index (ZHVI) YoY Growth Rate (%) Santa Barbara, CA California United States efp.com Source: Zillow Research Data

61 Final Thoughts Although mixed signals, on net, positive signs QE3...gone but not forgotten Fed has created room to bring back QE if necessary tighten sooner rather than later CA rebounding on most fronts

62 Thank You

The Global Economy: Sustaining Momentum

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

The U.S. Economic Recovery: Why so weak and what should be done? William J. Crowder Ph.D.

The U.S. Economic Recovery: Why so weak and what should be done? William J. Crowder Ph.D. Weak Recovery? It s no secret that the U.S. economy has still not fully recovered from the financial crisis and

The U.S. Economic Recovery: Why so weak and what should be done? William J. Crowder Ph.D. Weak Recovery? It s no secret that the U.S. economy has still not fully recovered from the financial crisis and

BC Pension Forum. Economic Outlook. Presented by: Ben Homsy, CFA Portfolio Manager

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

Global economy maintaining solid growth momentum. Canada leading the pack

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

The U.S. Economic Outlook

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

U.S. Economy in a Snapshot

U.S. Economy in a Snapshot Economic Press Briefing: May 19, 2016 The views expressed here are those of the presenter and do not necessarily represent the views of the Federal Reserve Bank of New York or

U.S. Economy in a Snapshot Economic Press Briefing: May 19, 2016 The views expressed here are those of the presenter and do not necessarily represent the views of the Federal Reserve Bank of New York or

Economy On The Rebound

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Big Changes, Unknown Impacts

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States?

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

The Auction Market In 2015 & 2016 Review & Forecast. Dr. Ira Silver NAAA Economist

The Auction Market In 2015 & 2016 Review & Forecast Dr. Ira Silver NAAA Economist silver@naaa.com Agenda Economic conditions Economic outlook Light vehicle sales Light vehicle sales outlook NAAA 2015 Annual

The Auction Market In 2015 & 2016 Review & Forecast Dr. Ira Silver NAAA Economist silver@naaa.com Agenda Economic conditions Economic outlook Light vehicle sales Light vehicle sales outlook NAAA 2015 Annual

Charting a Path to Lift Off? Understanding the Shifting Economic Winds

Charting a Path to Lift Off? Understanding the Shifting Economic Winds Thomas F. Siems, Ph.D. Assistant Vice President and Senior Economist Federal Reserve Bank of Dallas Government Finance Officers Arlington,

Charting a Path to Lift Off? Understanding the Shifting Economic Winds Thomas F. Siems, Ph.D. Assistant Vice President and Senior Economist Federal Reserve Bank of Dallas Government Finance Officers Arlington,

More of the Same; Or now for Something Completely Different?

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

Federal Reserve Bank of Dallas, FIRM (Financial Institution Relationship Management)

") The Economic Roller Coaster: Where Have We Been? And Where Are We Going? Thomas F. Siems, Ph.D. Senior Economist and Director of Economic Outreach Federal Reserve Bank of Dallas Economic Summit Dallas

The Economic Roller Coaster: Where Have We Been? And Where Are We Going? Thomas F. Siems, Ph.D. Senior Economist and Director of Economic Outreach Federal Reserve Bank of Dallas Economic Summit Dallas

ABA Commercial Real Estate Lending Committee

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

The Economy: A View from the (Atlanta) Fed (Staff)

Fed (Staff)") The Economy: A View from the (Atlanta) Fed (Staff) 2018 Alabama Economic Outlook Montgomery, AL January 11, 2018 2 The new supply-side economics? In their discussion of monetary policy, participants saw

The Economy: A View from the (Atlanta) Fed (Staff) 2018 Alabama Economic Outlook Montgomery, AL January 11, 2018 2 The new supply-side economics? In their discussion of monetary policy, participants saw

National and Regional Economic Outlook. Central Southern CAA Conference

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Trends. September 10, 2013

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Economic Outlook for Canada: Economy Confronting Capacity Limits

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

It Was Never Going To Be Easy

It Was Never Going To Be Easy Stephen Toplis, Head of Research July 2010 Introduction Global power shift sustained Average outlook on the improve Fiscal constraints binding Domestic rebalance under way

It Was Never Going To Be Easy Stephen Toplis, Head of Research July 2010 Introduction Global power shift sustained Average outlook on the improve Fiscal constraints binding Domestic rebalance under way

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Update.

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Update February 26, 2013 The Worst Recession Since the Great Depression 0% Loss from Peak

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Update February 26, 2013 The Worst Recession Since the Great Depression 0% Loss from Peak

U.S. Economic Activity. Federal Reserve Bank of Dallas

U.S. Economic Activity Federal Reserve Bank of Dallas 2019 Contents 1 Economic Activity 2 Wages and Prices 3 Financial Activity Economic Activity Economic Activity Index 160 Consumer Confidence and Sentiment

U.S. Economic Activity Federal Reserve Bank of Dallas 2019 Contents 1 Economic Activity 2 Wages and Prices 3 Financial Activity Economic Activity Economic Activity Index 160 Consumer Confidence and Sentiment

U.S. Economic Activity. Federal Reserve Bank of Dallas

U.S. Economic Activity Federal Reserve Bank of Dallas 2019 Contents 1 Economic Activity 2 Wages and Prices 3 Financial Activity Economic Activity Economic Activity New Orders for Durable Goods Billions

U.S. Economic Activity Federal Reserve Bank of Dallas 2019 Contents 1 Economic Activity 2 Wages and Prices 3 Financial Activity Economic Activity Economic Activity New Orders for Durable Goods Billions

U.S. Economic Activity. Federal Reserve Bank of Dallas

U.S. Economic Activity Federal Reserve Bank of Dallas 2019 Contents 1 Economic Activity 2 Wages and Prices 3 Financial Activity Economic Activity Economic Activity Index 160 Consumer Confidence and Sentiment

U.S. Economic Activity Federal Reserve Bank of Dallas 2019 Contents 1 Economic Activity 2 Wages and Prices 3 Financial Activity Economic Activity Economic Activity Index 160 Consumer Confidence and Sentiment

Composition of Federal Spending

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

The ABA Advantage: Economic Issues Update & ABA Resources

The ABA Advantage: Economic Issues Update & ABA Resources aba.com 1-800-BANKERS Meet the team Jim Chessen Chief Economist Curtis Dubay Senior Economist Brittany Kleinpaste Vice President of Economic Policy

The ABA Advantage: Economic Issues Update & ABA Resources aba.com 1-800-BANKERS Meet the team Jim Chessen Chief Economist Curtis Dubay Senior Economist Brittany Kleinpaste Vice President of Economic Policy

10 County Conference. Richard Wobbekind. Executive Director Business Research Division & Senior Associate Dean Leeds School of Business

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

Agriculture and the Economy: A View from the Chicago Fed

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Seven Lean Years Explaining Persistent Global Economic Weakness

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

2019 Economic Outlook: Will the Recovery Ever End?

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six years of steady growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half Full

The Economic Outlook Economic Policy Division Glass Half Full Six years of steady growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half Full

The World and U.S. Economy and San Pedro Bay Container Trade Outlook Forecast Review

The World and U.S. Economy and San Pedro Bay Container Trade Outlook Forecast Review Michael Keenan Harbor Planning and Economic Analyst Port of Los Angeles October 5, 2009 Review of 2007 Container Trade

The World and U.S. Economy and San Pedro Bay Container Trade Outlook Forecast Review Michael Keenan Harbor Planning and Economic Analyst Port of Los Angeles October 5, 2009 Review of 2007 Container Trade

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes. Tom Rogers. Lead Economist, Oxford Economics.

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

The Chamber of Commerce for Greater Philadelphia Economic Outlook Survey Results

The Chamber of Commerce for Greater Philadelphia Economic Outlook Survey Results January 19, 2018 Elif Sen Senior Economic Analyst FEDERAL RESERVE BANK OF PHILADELPHIA * The views expressed today are my

The Chamber of Commerce for Greater Philadelphia Economic Outlook Survey Results January 19, 2018 Elif Sen Senior Economic Analyst FEDERAL RESERVE BANK OF PHILADELPHIA * The views expressed today are my

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

From Recession to Recovery

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

2015 Economic Forecast & Industry Outlook. Robert A. Kleinhenz, Ph.D. Chief Economist, Kyser Center for Economic Research, LAEDC October 8, 2014

2015 Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Chief Economist,, LAEDC October 8, 2014 Outline U.S. Economy California Economy Southern California Economy & Industries Five-Year Outlook

2015 Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Chief Economist,, LAEDC October 8, 2014 Outline U.S. Economy California Economy Southern California Economy & Industries Five-Year Outlook

2nd Year. Addt'l Wage or Pension. Total Package 50% 1 Alameda $37.12 $24.13 $2.25 $4.50 $0.00 $6.24 $46.40 $30.16 $2.25 $4.50 $0.50 $8.

> 0 to 1,600 OJT Hours 1,601 to 3,200 OJT Hours 40% 50% 1 Alameda $37.12 $24.13 $2.25 $4.50 $0.00 $6.24 $46.40 $30.16 $2.25 $4.50 $0.50 $8.99 2 Alpine $28.10 $18.27 $2.25 $4.50 $0.00 $3.08 $35.12 $22.83

> 0 to 1,600 OJT Hours 1,601 to 3,200 OJT Hours 40% 50% 1 Alameda $37.12 $24.13 $2.25 $4.50 $0.00 $6.24 $46.40 $30.16 $2.25 $4.50 $0.50 $8.99 2 Alpine $28.10 $18.27 $2.25 $4.50 $0.00 $3.08 $35.12 $22.83

Babson Capital/UNC Charlotte Economic Forecast. May 13, 2014

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

The Fed and the Economic Outlook

The Fed and the Economic Outlook Mark L. J. Wright Research Director Federal Reserve Bank of Minneapolis March 28, 2018 Disclaimer The views expressed are my own and not necessarily those of the Federal

The Fed and the Economic Outlook Mark L. J. Wright Research Director Federal Reserve Bank of Minneapolis March 28, 2018 Disclaimer The views expressed are my own and not necessarily those of the Federal

DEDUCTIONS EFFECTIVE DECEMBER 1, NOVEMBER 30, MONTHLY PREMIUM

BAY AREA REGION HEALTH NET SMARTCARE CONTRA COSTA HEALTH PLAN WESTERN HEALTH ADVANTAGE $831.44 $695.93 $135.51 $1,662.88 $1,391.85 $271.03 $2,161.74 $1,809.41 $352.33 $1,111.13 $800.23 $310.90 $2,222.26

BAY AREA REGION HEALTH NET SMARTCARE CONTRA COSTA HEALTH PLAN WESTERN HEALTH ADVANTAGE $831.44 $695.93 $135.51 $1,662.88 $1,391.85 $271.03 $2,161.74 $1,809.41 $352.33 $1,111.13 $800.23 $310.90 $2,222.26

MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION

OXYGEN EVENTS CONFERENCE GALA PERFORMANCE 2017 MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION - THE CASE OF ROMANIA - Ph.D. Andrei RĂDULESCU Senior Economist, Banca Transilvania Researcher, Institute

OXYGEN EVENTS CONFERENCE GALA PERFORMANCE 2017 MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION - THE CASE OF ROMANIA - Ph.D. Andrei RĂDULESCU Senior Economist, Banca Transilvania Researcher, Institute

Paul Bingham Managing Director, Global Trade and Transportation February 18, 2009

Economic Outlook and Ports Paul Bingham Managing Director, Global Trade and Transportation February 18, 2009 The Outlook for Trade Depends on Goods Demand Integrated international supply-chains offer efficiencies

Economic Outlook and Ports Paul Bingham Managing Director, Global Trade and Transportation February 18, 2009 The Outlook for Trade Depends on Goods Demand Integrated international supply-chains offer efficiencies

Economic & Financial Market Outlook

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

RBC Economics Financial Update Dawn Desjardins

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

Northwest Economic Research Center College of Urban and Public Affairs Forecast Breakfast Economic Outlook

Northwest Economic Research Center College of Urban and Public Affairs 2019 Forecast Breakfast Economic Outlook 1/10/2019 2 U.S. ECONOMY 1/10/2019 3 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Northwest Economic Research Center College of Urban and Public Affairs 2019 Forecast Breakfast Economic Outlook 1/10/2019 2 U.S. ECONOMY 1/10/2019 3 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

2019 ECONOMIC OUTLOOK

2019 ECONOMIC OUTLOOK How Much Longer Can the Second Longest Economic Expansion on Record Last? Craig Dismuke Chief Economist cdismuke@viningsparks.com Dudley Carter Economist dcarter@viningsparks.com

2019 ECONOMIC OUTLOOK How Much Longer Can the Second Longest Economic Expansion on Record Last? Craig Dismuke Chief Economist cdismuke@viningsparks.com Dudley Carter Economist dcarter@viningsparks.com

Southern California Economic Forecast & Industry Outlook

2016-17 Southern California Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Sr. VP/Chief Economist, LAEDC February 17, 2016 Outline U.S. Economy California Economy Southern California Economy

2016-17 Southern California Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Sr. VP/Chief Economist, LAEDC February 17, 2016 Outline U.S. Economy California Economy Southern California Economy

Muhlenkamp & Company. Webinar December 1, Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Colorado Economic Update

Colorado Economic Update Steamboat Economic Summit Place cover image here Brian Lewandowski Associate Director, Business Research Division October 21, 2016 Recession 8 Months Recession 18 Months Real GDP

Colorado Economic Update Steamboat Economic Summit Place cover image here Brian Lewandowski Associate Director, Business Research Division October 21, 2016 Recession 8 Months Recession 18 Months Real GDP

The U. S. Economic Outlook: Robert J. Gordon

The U. S. Economic Outlook: Upside and Risks Robert J. Gordon Ottawa a Economics Association Ottawa, a, September 14, 2017 Immigration Medical Care My Policy Package: Be Like Canada d University Tuition

The U. S. Economic Outlook: Upside and Risks Robert J. Gordon Ottawa a Economics Association Ottawa, a, September 14, 2017 Immigration Medical Care My Policy Package: Be Like Canada d University Tuition

Zions Bank Economic Overview

Zions Bank Economic Overview Kenworth National Dealers Conference November 8, 2018 1 National Economic Conditions 2 Volatility Returns to the Stock Market 27,000 Dow Jones Industrial Average October 10,

Zions Bank Economic Overview Kenworth National Dealers Conference November 8, 2018 1 National Economic Conditions 2 Volatility Returns to the Stock Market 27,000 Dow Jones Industrial Average October 10,

11 th Annual Oregon Economic Forum!

11 th Annual Oregon Economic Forum! (almost) Beyond! Macroeconomics Portland, OR! October 16, 2014! Expansion Continues! Five Years and More!! Recession Indicators Nonfarm Payrolls Real Personal Income

11 th Annual Oregon Economic Forum! (almost) Beyond! Macroeconomics Portland, OR! October 16, 2014! Expansion Continues! Five Years and More!! Recession Indicators Nonfarm Payrolls Real Personal Income

East Bay Financial Planners Association Conference

East Bay Financial Planners Association Conference Is The New Normal Here to Stay? January 10, 2018 Rich Taylor Vice President Client Portfolio Manager Percent Change (%) Subpar Economic Growth Real GDP

East Bay Financial Planners Association Conference Is The New Normal Here to Stay? January 10, 2018 Rich Taylor Vice President Client Portfolio Manager Percent Change (%) Subpar Economic Growth Real GDP

Europe June Craig Menear. Chairman, CEO & President. Diane Dayhoff. Vice President, Investor Relations

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

Global economy s strong momentum intact despite elevated level of uncertainty. Canada headed for another year of solid growth

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks. Business Research Division Leeds School of Business

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks Presented by the Business Research Division Leeds School of Business University of Colorado at Boulder U.S. Economic

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks Presented by the Business Research Division Leeds School of Business University of Colorado at Boulder U.S. Economic

France : Economic developments and reforms, where are we heading?

France : Economic developments and reforms, where are we heading? The Economic Club of New York : 18 April 2018 François VILLEROY de GALHAU, Governor of the Banque de France 1 WHERE ARE WE STARTING FROM?

France : Economic developments and reforms, where are we heading? The Economic Club of New York : 18 April 2018 François VILLEROY de GALHAU, Governor of the Banque de France 1 WHERE ARE WE STARTING FROM?

Economic & Market Outlook

Economic & Market Outlook August 2017 The investments described herein are: NOT FDIC INSURED NOT BANK GUARANTEED MAY LOSE VALUE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL OR STATE GOVERNMENT AGENCY Average

Economic & Market Outlook August 2017 The investments described herein are: NOT FDIC INSURED NOT BANK GUARANTEED MAY LOSE VALUE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL OR STATE GOVERNMENT AGENCY Average

Trade Growth - Fundamental Driver of Port Operations and Development Strategies

Trade Growth - Fundamental Driver of Port Operations and Development Strategies Marine Terminal Management Training Program October 15, 2007 Long Beach, CA Paul Bingham Global Insight, Inc. 1 Agenda Economic

Trade Growth - Fundamental Driver of Port Operations and Development Strategies Marine Terminal Management Training Program October 15, 2007 Long Beach, CA Paul Bingham Global Insight, Inc. 1 Agenda Economic

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

Telling Canada s story in numbers Elizabeth Richards Analytical Studies Branch April 20, 2017

Recent Developments in the Canadian Economy: How have the decline in oil prices and a weaker Canadian dollar affected Canada s economy? www.statcan.gc.ca Telling Canada s story in numbers Elizabeth Richards

Recent Developments in the Canadian Economy: How have the decline in oil prices and a weaker Canadian dollar affected Canada s economy? www.statcan.gc.ca Telling Canada s story in numbers Elizabeth Richards

Keynesian Macroeconomics for the 21 st Century Part 3: Demand Dynamics, Inequality and Secular Stagnation

Keynesian Macroeconomics for the 21 st Century Part 3: Demand Dynamics, Inequality and Secular Stagnation YSI INET Lectures Edinburgh, Scotland October, 2017 Steven Fazzari Washington University in St.

Keynesian Macroeconomics for the 21 st Century Part 3: Demand Dynamics, Inequality and Secular Stagnation YSI INET Lectures Edinburgh, Scotland October, 2017 Steven Fazzari Washington University in St.

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

MUSTAFA MOHATAREM Chief Economist, General Motors

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition May 7 and 8, 2013 İstanbul, Turkey Outline 1 The Financial System 2 Weak Growth 3 4 5 Unprecedented

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition May 7 and 8, 2013 İstanbul, Turkey Outline 1 The Financial System 2 Weak Growth 3 4 5 Unprecedented

The U.S. Economic Outlook

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

State of American Trucking

State of American Trucking October 11, 2018 Rod Suarez Economic Analyst American Trucking Associations rsuarez@trucking.org Business Cycles U.S. Expansions Duration October 1949 - July 1953 May 1954 -

State of American Trucking October 11, 2018 Rod Suarez Economic Analyst American Trucking Associations rsuarez@trucking.org Business Cycles U.S. Expansions Duration October 1949 - July 1953 May 1954 -

Steel: A Buyer s Market for the Worst of Reasons. John Anton Director, IHS Global Insight Steel Service August 2009

Steel: A Buyer s Market for the Worst of Reasons John Anton Director, IHS Global Insight Steel Service August 2009 The U.S. Recession Is Bottoming Out This recession has been the most severe of the postwar

Steel: A Buyer s Market for the Worst of Reasons John Anton Director, IHS Global Insight Steel Service August 2009 The U.S. Recession Is Bottoming Out This recession has been the most severe of the postwar

Southwest Ohio Regional Economy in Context. Richard Stock, PhD. Business Research Group

Southwest Ohio Regional Economy in Context Richard Stock, PhD. Business Research Group State of the Metro Area (in January Each Year) Total Employment has slowly increased in the last three years after

Southwest Ohio Regional Economy in Context Richard Stock, PhD. Business Research Group State of the Metro Area (in January Each Year) Total Employment has slowly increased in the last three years after

IFP HIPAA Guaranteed Issue plans monthly rates

IFP HIPAA Guaranteed Issue plans monthly rates Effective March 1, 2012 for HMO and PPO plans HIPAA Guaranteed-issue plans are available to individuals who meet the requirements specified on the Blue Shield

IFP HIPAA Guaranteed Issue plans monthly rates Effective March 1, 2012 for HMO and PPO plans HIPAA Guaranteed-issue plans are available to individuals who meet the requirements specified on the Blue Shield

U.S. AUTO INDUSTRY UPDATE Federal Reserve Bank of Chicago Automotive Outlook Symposium. Emily Kolinski Morris Chief Economist May 2015

U.S. AUTO INDUSTRY UPDATE Federal Reserve Bank of Chicago Automotive Outlook Symposium Emily Kolinski Morris Chief Economist May 2015 NORTH AMERICA INDUSTRY VOLUME SUMMARY 13.1 Total North America* (Mils.)

U.S. AUTO INDUSTRY UPDATE Federal Reserve Bank of Chicago Automotive Outlook Symposium Emily Kolinski Morris Chief Economist May 2015 NORTH AMERICA INDUSTRY VOLUME SUMMARY 13.1 Total North America* (Mils.)

First Lecture Capitalism: A Brief History

Nitzan / 3270 GPE I I. Capitalism: A Brief History / 1 First Lecture Capitalism: A Brief History Definition Economic system? Private ownership / profit motive / wage labour Beginnings 16 th century: Feudal

Nitzan / 3270 GPE I I. Capitalism: A Brief History / 1 First Lecture Capitalism: A Brief History Definition Economic system? Private ownership / profit motive / wage labour Beginnings 16 th century: Feudal

Economic Analysis What s happening with U.S. potential GDP growth?

Economic Analysis What s happening with U.S. potential GDP growth? Kan Chen Capital stock, labor, and productivity do not show a significant increase following the recent fiscal stimulus According to our

Economic Analysis What s happening with U.S. potential GDP growth? Kan Chen Capital stock, labor, and productivity do not show a significant increase following the recent fiscal stimulus According to our

The Great Economic Reset

The Great Economic Reset CMTA Annual Conference Squaw Creek Lake Tahoe April 13, 2016 Presented by Douglas C. Robinson, RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory

The Great Economic Reset CMTA Annual Conference Squaw Creek Lake Tahoe April 13, 2016 Presented by Douglas C. Robinson, RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory

Why Is the Recovery from the Financial Crisis So Sluggish?

Why Is the Recovery from the Financial Crisis So Sluggish? Robert E. Hall Hoover Institution and Department of Economics Stanford University Keynote Address Agricultural and Applied Economics Association

Why Is the Recovery from the Financial Crisis So Sluggish? Robert E. Hall Hoover Institution and Department of Economics Stanford University Keynote Address Agricultural and Applied Economics Association

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder Member FDIC VectraBank.com Economic Outlook 2015 Richard

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder Member FDIC VectraBank.com Economic Outlook 2015 Richard

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Inland Empire International Trade Economic Forecast

Inland Empire International Trade Economic Forecast Mira Farka Adrian Fleissig Institute for Economic and Environmental Studies Orange County / Inland Empire Regional SBDC Network California State University,

Inland Empire International Trade Economic Forecast Mira Farka Adrian Fleissig Institute for Economic and Environmental Studies Orange County / Inland Empire Regional SBDC Network California State University,

Alternative Measures of Economic Activity. Jan J. J. Groen, Officer Research and Statistics Group

Alternative Measures of Economic Activity Jan J. J. Groen, Officer Research and Statistics Group High School Fed Challenge Student Orientation: February 1 and 2, 217 Outline Alternative indicators: data

Alternative Measures of Economic Activity Jan J. J. Groen, Officer Research and Statistics Group High School Fed Challenge Student Orientation: February 1 and 2, 217 Outline Alternative indicators: data

Kevin Thorpe Financial Economist & Principal Cassidy Turley

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

After the British referendum

Future of Europe After the British referendum Broader issues for the UK and the EU David Marsh, Managing Director, OMFIF 27 October 2016 Nicosia 1 European politics moves against integration A new phase

Future of Europe After the British referendum Broader issues for the UK and the EU David Marsh, Managing Director, OMFIF 27 October 2016 Nicosia 1 European politics moves against integration A new phase

Trade and Economic Trends

Trade and Economic Trends Marine Terminal Management Training Program Paul Bingham Managing Director, Global Commerce & Transportation IHS Global Insight Long Beach, CA September 21, 2009 The Global Recession

Trade and Economic Trends Marine Terminal Management Training Program Paul Bingham Managing Director, Global Commerce & Transportation IHS Global Insight Long Beach, CA September 21, 2009 The Global Recession

A comment on recent events, and...

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

State of the City of Carpinteria

April 21, 2017 Mark Schniepp Director State of the City of Carpinteria jobs 1,000 Employment in Information / Carpinteria Valley 2006 -- 2016 800 600 400 200 0 2006 2008 2010 2012 2014 2016 ConstructiveDIVE.com

April 21, 2017 Mark Schniepp Director State of the City of Carpinteria jobs 1,000 Employment in Information / Carpinteria Valley 2006 -- 2016 800 600 400 200 0 2006 2008 2010 2012 2014 2016 ConstructiveDIVE.com

Demographics, Debt, Dollar and Deflation Is the next Great Reset coming?

Demographics, Debt, Dollar and Deflation Is the next Great Reset coming? CMTA Advanced Investment Workshop January 28, 20145 Presented by Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered

Demographics, Debt, Dollar and Deflation Is the next Great Reset coming? CMTA Advanced Investment Workshop January 28, 20145 Presented by Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip?

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

U.S Cement Outlook IEEE. Ed Sullivan Group VP, Chief Economist

U.S Cement Outlook IEEE Ed Sullivan Group VP, Chief Economist 1 Construction Activity Billion Real $ 1,400 1,200 1,000 2014 = 2.5% 2015 = 5.6% 800 600 400 200 0 12 Year Peak-to- Peak Recovery 1998 2000

U.S Cement Outlook IEEE Ed Sullivan Group VP, Chief Economist 1 Construction Activity Billion Real $ 1,400 1,200 1,000 2014 = 2.5% 2015 = 5.6% 800 600 400 200 0 12 Year Peak-to- Peak Recovery 1998 2000

Real Estate: Investing for the Future. Sponsored By:

Real Estate: Investing for the Future Sponsored By: Percent Change, Year Ago 6 5 4 3 2 1 Real GDP Growth United States, 2000 Prices 0 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 U.S. Employment

Real Estate: Investing for the Future Sponsored By: Percent Change, Year Ago 6 5 4 3 2 1 Real GDP Growth United States, 2000 Prices 0 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 U.S. Employment

Zions Bank Economic Overview

Zions Bank Economic Overview WIB Education Summit September 19, 2017 National Economic Conditions Dow Breaks 22,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Federal

Zions Bank Economic Overview WIB Education Summit September 19, 2017 National Economic Conditions Dow Breaks 22,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Federal

2009 California & Bay Area Real Estate Market Outlook

2009 California & Bay Area Real Estate Market Outlook November 24, 2008 Fairmont Hotel Leslie Appleton-Young C.A.R. Vice President and Chief Economist California Real Estate Market: 2008 California s Housing

2009 California & Bay Area Real Estate Market Outlook November 24, 2008 Fairmont Hotel Leslie Appleton-Young C.A.R. Vice President and Chief Economist California Real Estate Market: 2008 California s Housing

What you should know, higher prices trade tensions, and the expanding economy September 11, 2018 Mark Schniepp Director

The 2018 Economy What you should know, higher prices trade tensions, and the expanding economy September 11, 2018 Mark Schniepp Director 1 The annual update Why are you here? (1) I m here for the update

The 2018 Economy What you should know, higher prices trade tensions, and the expanding economy September 11, 2018 Mark Schniepp Director 1 The annual update Why are you here? (1) I m here for the update

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.