Exchange Arrangements Entering the 21 st Century: Which Anchor Will Hold?

|

|

|

- Elvin Stone

- 6 years ago

- Views:

Transcription

1 Exchange Arrangements Entering the 21 st Century: Which Anchor Will Hold? Ethan Ilzetzki LSE Carmen M Reinhart Kenneth Rogoff Harvard University Bank of Israel, December 7, 2017

2 Overview Introduce new and updated classification of anchor currencies and exchange arrangements USD dominant anchor / benchmark currency World has not moved to greater ERA flexibility Bretton Woods II: Dooley et al (2003) Anchor currency classifications shed further light on new Triffin Dilemma. Farhi, Gourinchas & Rey (2011), Obstfeld (2013), Farhi & Maggiori (2016)

3 METHODOLOGY

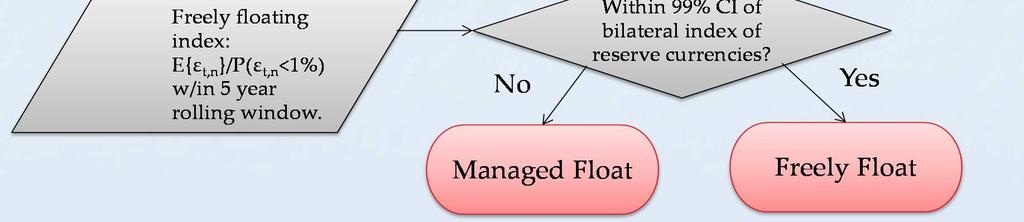

4 Sketch of ERA Algorithm Use monthly absolute value of change in exchange rate. With respect to 10 candidate anchors/benchmark. Freely falling Peg Narrow band Managed float Freely floating Inflation > 40% for 12 months 0 variation for 4 months <2% variation over 2 year rolling window Within99% CI of variation among anchors

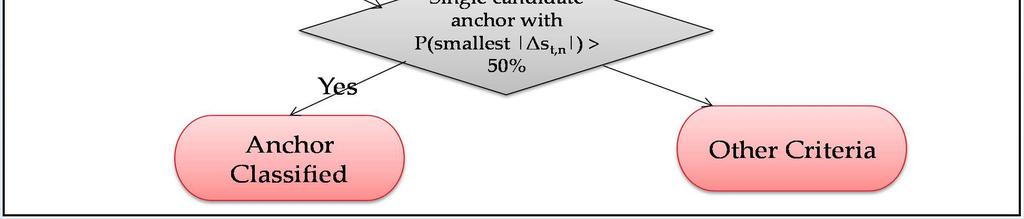

5 Sketch of Anchor Algorithm Freely falling/floating: no anchor Peg / Narrow band: anchor unambiguous Managed float: Single candidate anchor with smallest variation >50% of observations = anchor. If none: use non exchange rate criteria

6 Benchmark Currency Selection Process: Additional Criteria Benchmark Currency Index: Average of four measures: 1. Reserve denomination (% reserves in currency X) 2. Trade invoicing (% of X+M invoiced in X) 3. Denomination of (external public) debt (% denominated in currency X) 4. Previous anchor (1/y, where y is the number of years since anchored to currency X.)

7 Benchmark Currency Selection Process: Additional Criteria Country Years $ index index Benchmark Brazil % 4% USD Canada % 5% USD Chile % 9% USD Colombia % 0% USD Iceland % 19% Marginal India % 7% USD Israel % 12% USD Korea USD Latvia EUR Turkey % 25% USD Uruguay USD

8 Existing Classifications Exchange Arrangements: Reinhart and Rogoff (2004) Shambaugh (2004) Levi-Yeyati and Sturtzenegger (2005) IMF (annually) Anchor Currencies: Frankel and Wei (1994) for E. Asia First to integrate anchor classification formally with ERA classification.

9 MODERN HISTORY: ANCHOR CURRENCIES

10 Summary of Findings The dollar retains its dominant position as the world s reserve currency. By some metrics it is as dominant as it was at the time of the early Bretton Woods era. By other metrics, its global role has expanded: Collapse of the ruble zone Re-anchoring of freely falling Classification consistent with other measures of dollar dominance and provides summary measure of anchor currency based on revealed preference.

11 Post-World War II Major Anchor Currencies Share of countries, , excludes freely falling cases 100 Percent UK pound US dollar French franc and German DM ( ) and Euro ( ) M1 1956M1 1966M1 1976M1 1986M1 1996M1 2006M1

12 The Geography of Anchor Currencies, 2015

13 Stress Test: Whatever it takes, % -2% $ Anchor Borderline -4% -6% Non-$ Anchor -8% Appreciation vs. $: Smaller when classified as anchored -10% Jul-2012 Aug-2012 Sep-2012 Oct-2012 Nov-2012 Dec-2012 Jan-2013 /$

14 /$ Exchange Rate "Taper Tantrum" FRB Tightening signal "Whatever it takes"

15 Markers of an Anchor Currency

16 Markers of an Anchor Currency

17 MODERN HISTORY: EXCHANGE ARRANGEMENTS

18 Summary of Findings Oft cited global transition from fixed to floating exchange rates considerably overstates the reality. Based on ERA classification for 194 countries over IMF classification of all Eurozone member countries as having floating ER since 2007 contributes to the overstatement. Lower incidence of bi-polar or corner solutions (Stanley Fischer, 2001)

19 De Facto ERA Share of (independent) countries in each group Groups 1 and 2: Less flexibility, primarily nominal exchange rate anchors Percent Group 2: Gradualist adjustment (from crawling peg to narrow crawling bands) Group 1: Least flexible (from no separate legal tender to de facto pegs)

20 De Facto ERA Share of (independent) countries in each group Groups 3 and 4: Flexible, incl. most inflation target arrangements 100 Percent Group 4: Freely floating (few high-income cases) 30 Group 3: Broad bands and managed floating

21 De Facto ERA Share of (independent) countries in each group Groups 5 and 6: Freely falling & multiple ER Percent Group 6: Multiple, Dual, or parallel markets with limited or no data on the structure of exchange rates Group 5: Freeely falling, inflation > 40% or currency crash

22 The Geography of Exchange Rate Arrangements, 2015

23 TRIFFIN DILEMMA

24 Summary of Findings A modern Triffin Dilemma may be in the Making. Increasing dominance of USD anchor Continued inflexibility of ERAs Reserve accumulation substituting capital controls (per theoretical analysis of Korinek, 2013) But US declining share of global GDP

25 Exchange Rate Arrangements and Capital Mobility, Share of countries with less flexible exchange rate regimes Share of countries with dual/multiple/parallel exchange rates

26 World Reserves minus Gold (US dollars) % of US GDP Percent Reserves minus gold/ US GDP 100 The Bretton Woods system 80 World Emerging and Developing countries

27 Role of the Dollar and US Economy Share of countries US GDP as a share of world GDP (percent, right scale) Share of countries where the US dollar is the principal anchor currency (percent, left scale) M1 1960M1 1970M1 1980M1 1990M1 2000M1 2010M1 Reinhart 10

28 Role of the Franc & DM , and Euro France and Germany GDP as a share of world GDP (percent, right scale) Share of countries where the euro (and previously the French franc and DM) are the principal anchor currency (percent, left scale) M1 1960M1 1970M1 1980M1 1990M1 2000M1 2010M1 0

29 Role of the Pound and the UK Economy Share of countries where the UK pound is the principal anchor currency (percent, left scale) UK GDP as a share of world GDP (percent, right scale) M1 1960M1 1970M1 1980M1 1990M1 2000M1 2010M1 2.0

30 Role of the Yen and Japanese Economy Japan GDP as a share of world GDP (percent, right scale) Share of countries where the yen is the principal anchor currency (percent, left scale) M1 1960M1 1970M1 1980M1 1990M1 2000M1 2010M1 0

31 Chinese Economy China GDP as a share of world GDP (percent, right scale)

32 Conclusions USD as dominant as anchor today as ever. RMB is the wildcard. No substantial move to ER flexibility. Increase in intermediate de-facto regimes. New Triffin Dilemma may be on the horizon.

33 APPENDIX 1: HOW TO CLASSIFY EZ COUNTRIES?

34 Classifying the Eurozone Eurozone >10% of World GDP Poses classification challenge floating externally EZ countries no legal tender internally IMF classify all EZ countries freely floating We classify all as no legal tender

35 Classifying the Eurozone Unit of observation is sovereign country No EZ member has more than 4% voting share Trade: >60% of trade is internal Consistency in time series EZ has moved to less monetary autonomy

36 Classifying the Eurozone: Evidence

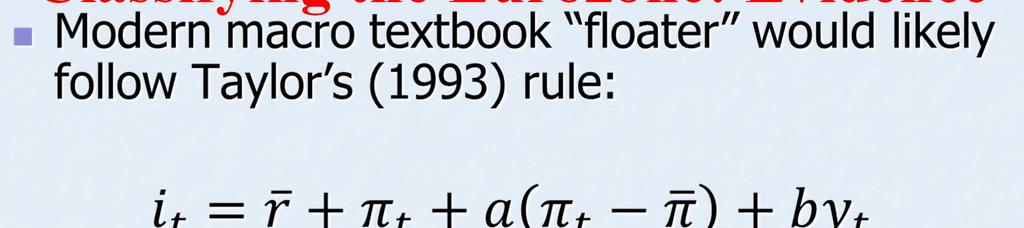

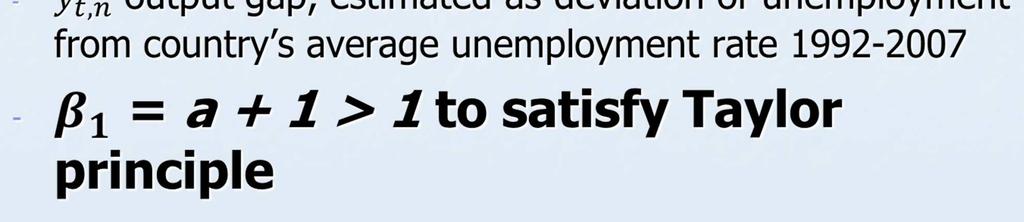

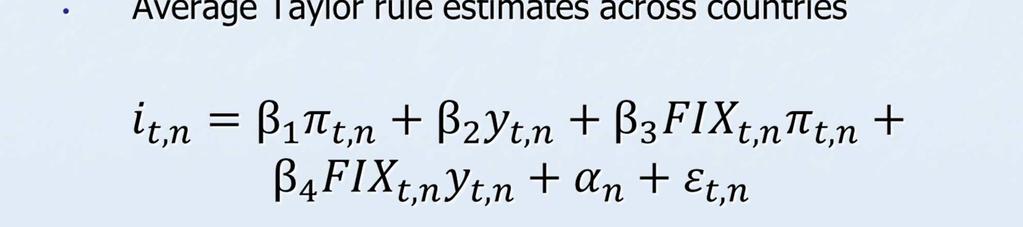

37 Estimating Taylor Rules

38 1.2 Taylor Rule Coefficients: Inflation Germany only country to satisfy Taylor principle Taylor principle violated for EZ as whole Whiskers: 95% confidence intervals

39 Taylor Rule Coefficients: Output Gap 1.5 But monetary policy has been countercyclical for most countries Whiskers: 95% confidence intervals

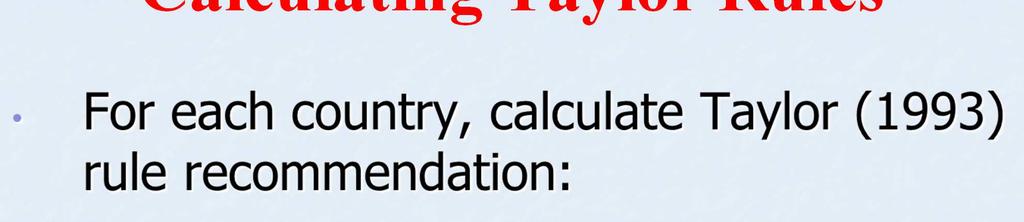

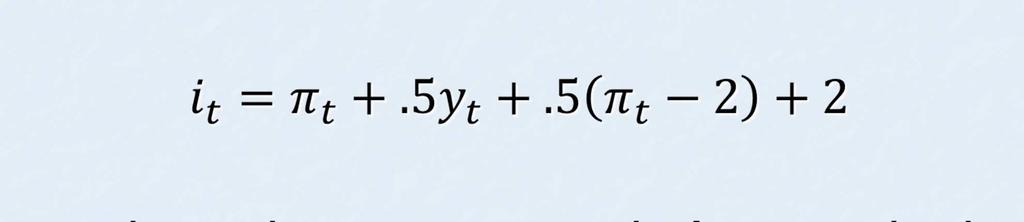

40 Calculating Taylor Rules

41 Taylor Rule vs. Policy Rate 12% 10% 8% 6% DM DM Regime Regime Rule 12% 10% 8% 6% DM DM Regime Regime Rule 4% 4% 2% 0% Policy 2% 0% Policy % 10% DM DM Regime Regime 8% 12% 10% DM DM Regime Regime 8% 6% 4% 2% 0% % -4% Rule Policy 6% 4% 2% 0% % Rule Policy

42 Germany 12% 10% DM DM Regime Regime 8% Rule 6% 4% 2% Policy 0%

43 France 12% 10% DM DM Regime Regime 8% 6% Rule 4% 2% Policy 0%

44 Portugal 12% 10% DM DM Regime Regime 8% 6% Rule 4% 2% Policy 0% -2% -4%

45 Eurozone 12% 10% DM DM Regime Regime 8% 6% Rule 4% 2% Policy 0% -2%

46 Summary No clear break in policy in 1999 ECB follows DM Taylor rule closely until 2008 Post crisis ECB playing stabilizing role for EZ, but little to suggest that doing so for for any individual member

47 APPENDIX 2: ARE INFLATION TARGETERS DIFFERENT?

48 Inflation Targeting One of the biggest developments in dejure monetary arrangements As we will show: IT not particularly informative Masks heterogeneity in exchange arrangements in practice.

49 Inflation Targeters Managed / Freely floating Or wide bands Crawling pegs

50 Monetary Practices of IT Central Banks

51 Augmented Taylor Rule Estimates Unbalanced Panel Regression Results w. Country Fixed Effects Dependent Variable = Nominal Interest Rate Inflation.68***.67***.74***.74***.73*** (.014) (.015) (.017) (.017) (.017) Log(Exchange Rate) 2.24*** 2.03*** 1.99*** 1.60*** (.144) (.147) (.150) (.150) Unemployment.10***.07*** (.017) (.017) Commodity Price Inflation 1.00 Inflation*"Fixed" (.628) Fixed IT: Less aggressive on inflation -.19*** -.19*** -.18*** (.026) (.026) (.026) Log(Exchange Rate)*"Fixed" Fixed IT: More aggressive on.34***.36***.34*** exchange rate (.053) (.053) (.054) Commodity Price Inflation*"Fixed".22 (.168) R n

52 Stress Testing ER Classification of IT Central Banks Consider two major shocks: 1. Lehman, September FRB signalling tightening cycle in June 2014

53 Lehman Jan-08 Feb-08 Mar-08 Apr-08 May-08 Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov-08 Dec-08 NON-IT 1+2 IT 1+2 NON-IT 3+4 IT

54 102 Fed Tightening Announcement Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 NON-IT 1+2 IT 1+2 IT 3+4 NON-IT 3+4

55 14 Lehman 2008 Inflation May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec NON-IT 1+2 NON-IT 3+4 IT 1+2 IT 3+4

56 7 Fed Tightening Announcement 2014 Inflation Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 NON-IT CAT 1+2 NON-IT CAT 3+4 IT CAT 1+2 IT CAT 3+4

57 Summary IT masks heterogeneity in exchange rate practices Our ERA classification gives information that goes beyond the IT headline Pegged IT central banks less aggressive on inflation & more on exchange rate Similar exchange rate behaviorto non-it pegged currencies in face of major shocks. But inflation is lower in IT countries, even those with a dual mandate

58 APPENDIX 3: ANCHOR AND ERA ALGORITHMS

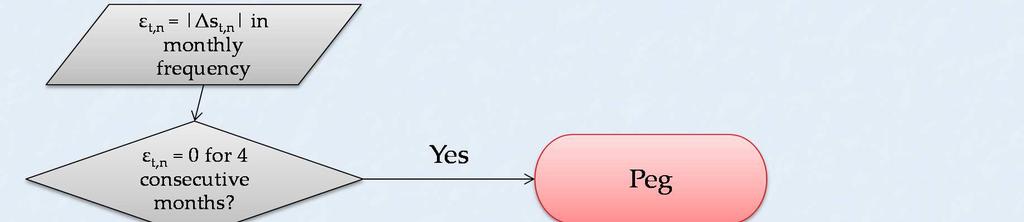

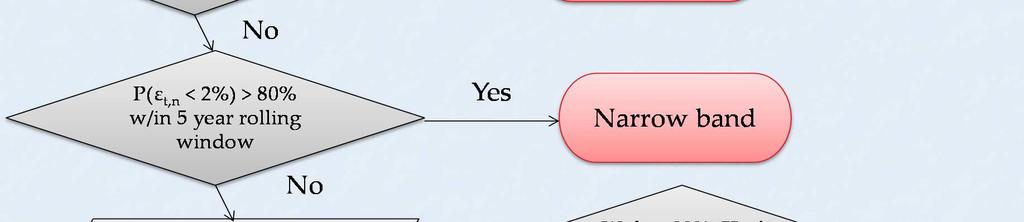

59 ER Arrangement Classification Algorithm Sequence and general scheme

60 ER Arrangement Classification Algorithm Statistical tests

61 Anchor Currency Selection Process

62 APPENDIX 4: CAPITAL CONTROLS

63 Summary of Findings Introduce an index of exchange restrictions As a minimal measure of capital controls. Global trend towards increased capital mobility. A fairly modern phenomenon for emerging and developing countries.

64 Index of Exchange Restrictions This index takes on the value 1 if any one or more of the following conditions hold and 0 otherwise. There is a de-jure dual market / multiple exchange rates OR There is a de-facto parallel market and the parallel premium >10% over 12-month moving average. Sources: IMF AEAER, Franz Pick. Index = 1 is sufficient but not necessary for capital controls.

65 Share of Independent Countries with Dual, Multiple, or Parallel Exchange Rates, January 1950-September 2016: 90 Advanced economies Share of countries(solid line) Share weighted by GDP (dashed line) M1 1960M1 1970M1 1980M1 1990M1 2000M1 2010M1

66 Share of Independent Countries with Dual, Multiple, or Parallel Exchange Rates, January 1950-September 2016: All independent countries Share of countries (solid line) Share weighted by GDP (dashed line) M1 1960M1 1970M1 1980M1 1990M1 2000M1 2010M1

Outline. Overview of globalization. Global outlook for real economic activity & inflation. Risks to the outlook

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

Global Economic Outlook

Global Economic Outlook Mark A. Wynne Vice President & Associate Director of Research Director, Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas Presentation to Vistas Conference

Global Economic Outlook Mark A. Wynne Vice President & Associate Director of Research Director, Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas Presentation to Vistas Conference

Market Insights. June 30, 2018

June 30, 2018 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.7% 1.2% 1.3% 2.1% 2.3% 1.7% 2.3%

June 30, 2018 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.7% 1.2% 1.3% 2.1% 2.3% 1.7% 2.3%

Market Insights. March 29, 2019

March 29, 2019 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.2% 1.4% 2.1% 2.3% 1.7% 2.4% 2.3%

March 29, 2019 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.2% 1.4% 2.1% 2.3% 1.7% 2.4% 2.3%

Grasshoppers, Ants and Locusts: the future of the world economy

Ralph Miliband Series on the Restructuring of World Power Grasshoppers, Ants and Locusts: the future of the world economy Martin Wolf Associate editor and chief economics commentator, Financial Times Professor

Ralph Miliband Series on the Restructuring of World Power Grasshoppers, Ants and Locusts: the future of the world economy Martin Wolf Associate editor and chief economics commentator, Financial Times Professor

Global growth forecasts Key countries/regions,

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

After the British referendum

Future of Europe After the British referendum Broader issues for the UK and the EU David Marsh, Managing Director, OMFIF 27 October 2016 Nicosia 1 European politics moves against integration A new phase

Future of Europe After the British referendum Broader issues for the UK and the EU David Marsh, Managing Director, OMFIF 27 October 2016 Nicosia 1 European politics moves against integration A new phase

GLOBAL ECONOMICS, REAL ESTATE PRICING & OUTLOOK FOR 2017 RICHARD BARKHAM GLOBAL CHIEF ECONOMIST

GLOBAL ECONOMICS, REAL ESTATE PRICING & OUTLOOK FOR 2017 RICHARD BARKHAM GLOBAL CHIEF ECONOMIST BREXIT TRUMPISM EURO-TRUMPISM 4 ECONOMICS, PRICING & OUTLOOK FOR 2017 LET S GET GEOPOLITICS IN PERSPECTIVE

GLOBAL ECONOMICS, REAL ESTATE PRICING & OUTLOOK FOR 2017 RICHARD BARKHAM GLOBAL CHIEF ECONOMIST BREXIT TRUMPISM EURO-TRUMPISM 4 ECONOMICS, PRICING & OUTLOOK FOR 2017 LET S GET GEOPOLITICS IN PERSPECTIVE

Economic & Financial Market Outlook

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies Chief Economist, PAGI Group, JLL (Port, Airport & Global Infrastructure) Agenda Where are we in the cycle? What are the barriers

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies Chief Economist, PAGI Group, JLL (Port, Airport & Global Infrastructure) Agenda Where are we in the cycle? What are the barriers

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 2 OVERVIEW OF THE GREAT DEPRESSION January 22, 2018 I. THE 1920S A. GDP growth and inflation B.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 2 OVERVIEW OF THE GREAT DEPRESSION January 22, 2018 I. THE 1920S A. GDP growth and inflation B.

SA economic review Kevin Lings. August 2018

SA economic review Kevin Lings August 2018 South Africa real GDP growth year-on-year %y/y 8 7 6 5 Ave 4.3% 4 Ave 2.5% 3 2 Ave 0.9% 1 0-1 -2-3 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 2

SA economic review Kevin Lings August 2018 South Africa real GDP growth year-on-year %y/y 8 7 6 5 Ave 4.3% 4 Ave 2.5% 3 2 Ave 0.9% 1 0-1 -2-3 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 2

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*

CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*") COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun Jul

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun Jul

The Global Economy: Sustaining Momentum

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

Seven Lean Years Explaining Persistent Global Economic Weakness

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Vermont Economic Conference:

Vermont Economic Conference: Mapping Our Economic Future Michael Dolega Director & Senior Economist TD Economics January 5 2018 Summary Global economy gathering speed, leading to another upgrade in outlook.

Vermont Economic Conference: Mapping Our Economic Future Michael Dolega Director & Senior Economist TD Economics January 5 2018 Summary Global economy gathering speed, leading to another upgrade in outlook.

IMF Reform: The Unfinished Agenda. Jose De Gregorio Barry Eichengreen Takatoshi Ito Charles Wyplosz

IMF Reform: The Unfinished Agenda Jose De Gregorio Barry Eichengreen Takatoshi Ito Charles Wyplosz October 2018 1 IMF Reform 2 IMF Reform 3 We revisit the issue How the world has changed How the IMF has

IMF Reform: The Unfinished Agenda Jose De Gregorio Barry Eichengreen Takatoshi Ito Charles Wyplosz October 2018 1 IMF Reform 2 IMF Reform 3 We revisit the issue How the world has changed How the IMF has

RISI EUROPEAN CONFERENCE. (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last?

The European Economy Things look good just now. Can this last?") RISI EUROPEAN CONFERENCE (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last? Andrea Boltho Magdalen College University of Oxford and Oxford Economics CONCLUSIONS OF

RISI EUROPEAN CONFERENCE (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last? Andrea Boltho Magdalen College University of Oxford and Oxford Economics CONCLUSIONS OF

Foreign overnights in the Nordic countries 2015

Foreign overnights in the Nordic countries 2015 Sources: Statistics Statistics Statistics Statistics July 2016 VISIT FINLAND STATISTICS Contents Foreign overnights in the Nordic countries.4 Overnights

Foreign overnights in the Nordic countries 2015 Sources: Statistics Statistics Statistics Statistics July 2016 VISIT FINLAND STATISTICS Contents Foreign overnights in the Nordic countries.4 Overnights

The Aftermath of Global Financial Crises

The Aftermath of Global Financial Crises Carmen M. Reinhart, University of Maryland, NBER, and CEPR Brookings Institution Washington DC, April 20, 2009 This talk is based on several works with Kenneth

The Aftermath of Global Financial Crises Carmen M. Reinhart, University of Maryland, NBER, and CEPR Brookings Institution Washington DC, April 20, 2009 This talk is based on several works with Kenneth

China in the World Economy

China in the World Economy Lawrence J. Lau, Ph. D. Ralph and Claire Landau Professor of Economics, The Chinese Univ. of Hong Kong and Kwoh-Ting Li Professor in Economic Development, Emeritus, Stanford

China in the World Economy Lawrence J. Lau, Ph. D. Ralph and Claire Landau Professor of Economics, The Chinese Univ. of Hong Kong and Kwoh-Ting Li Professor in Economic Development, Emeritus, Stanford

On Monetary Cooperation in East Asia

On Monetary Cooperation in East Asia In View of Experience with the European Monetary Cooperation Soko Tanaka 1 Experience with European Monetary Cooperation 4 Institutional Components of the EMS Collective

On Monetary Cooperation in East Asia In View of Experience with the European Monetary Cooperation Soko Tanaka 1 Experience with European Monetary Cooperation 4 Institutional Components of the EMS Collective

MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION

OXYGEN EVENTS CONFERENCE GALA PERFORMANCE 2017 MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION - THE CASE OF ROMANIA - Ph.D. Andrei RĂDULESCU Senior Economist, Banca Transilvania Researcher, Institute

OXYGEN EVENTS CONFERENCE GALA PERFORMANCE 2017 MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION - THE CASE OF ROMANIA - Ph.D. Andrei RĂDULESCU Senior Economist, Banca Transilvania Researcher, Institute

This Time is Different: Eight Centuries of Financial Folly

This Time is Different: Eight Centuries of Financial Folly Carmen M. Reinhart, University of Maryland, NBER, and CEPR Kenneth S. Rogoff, Harvard University and NBER (Princeton University Press, forthcoming

This Time is Different: Eight Centuries of Financial Folly Carmen M. Reinhart, University of Maryland, NBER, and CEPR Kenneth S. Rogoff, Harvard University and NBER (Princeton University Press, forthcoming

Economic Overview. Melissa K. Peralta Senior Economist April 27, 2017

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition May 7 and 8, 2013 İstanbul, Turkey Outline 1 The Financial System 2 Weak Growth 3 4 5 Unprecedented

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition May 7 and 8, 2013 İstanbul, Turkey Outline 1 The Financial System 2 Weak Growth 3 4 5 Unprecedented

RBC Economics Financial Update Dawn Desjardins

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

Reading the Tea Leaves: Investing for 2010 and Beyond

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

The Israeli Economy 2009 The Caesarea Center Conference

The Israeli Economy 2009 The Caesarea Center Conference Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

The Israeli Economy 2009 The Caesarea Center Conference Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

Further Opening Up and Reform of China s Capital Market

Further Opening Up and Reform of China s Capital Market Haizhou Huang January 7, 2016 China economy and capital market: Finding new normal 1 Macro: We expect China GDP to grow 6.9% in 2015 and 6.8% in

Further Opening Up and Reform of China s Capital Market Haizhou Huang January 7, 2016 China economy and capital market: Finding new normal 1 Macro: We expect China GDP to grow 6.9% in 2015 and 6.8% in

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD?

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD? FROM BUST TO BOOM. AN EPIC BUST After 16 years of growth with a short pause for breath in 2002, the Icelandic economy entered

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD? FROM BUST TO BOOM. AN EPIC BUST After 16 years of growth with a short pause for breath in 2002, the Icelandic economy entered

United Nations Conference on Trade and Development

United Nations Conference on Trade and Development 11 th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 15-16 April 2019, Geneva Saudi economic growth strategy on the face of oil price uncertainty

United Nations Conference on Trade and Development 11 th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 15-16 April 2019, Geneva Saudi economic growth strategy on the face of oil price uncertainty

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Macroeconomic Research and Statistics Department Vol. XVIl, No.3 March 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02 Table

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Macroeconomic Research and Statistics Department Vol. XVIl, No.3 March 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02 Table

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.9 September 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.9 September 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.11 November 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.11 November 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

New Growth Segments for the Air Cargo Industry

Page 1 New Growth Segments for the Air Cargo Industry 4 th Air Cargo Economics Conference Prague, April 22-23, 2004 Page 2 Assumptions Primary commodity sectors and their growth Perishables: are they really

Page 1 New Growth Segments for the Air Cargo Industry 4 th Air Cargo Economics Conference Prague, April 22-23, 2004 Page 2 Assumptions Primary commodity sectors and their growth Perishables: are they really

Panel on Post-Crisis Growth Performance Determinants, Effects and Policy Implications

Panel on Post-Crisis Growth Performance Determinants, Effects and Policy Implications Carmen M. Harvard University Bank of Canada and European Central Bank Conference Ottawa, June 8-9, 2015 1 Outline (i)

Panel on Post-Crisis Growth Performance Determinants, Effects and Policy Implications Carmen M. Harvard University Bank of Canada and European Central Bank Conference Ottawa, June 8-9, 2015 1 Outline (i)

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Current Hawaii Economic Conditions. Eugene Tian

Current Hawaii Economic Conditions Eugene Tian Department of Business, Economic Development & Tourism At the PATA/TTRA 2016 Annual Outlook & Economic Forecast Forum February 3, 2016 Positive Signs in the

Current Hawaii Economic Conditions Eugene Tian Department of Business, Economic Development & Tourism At the PATA/TTRA 2016 Annual Outlook & Economic Forecast Forum February 3, 2016 Positive Signs in the

MUSTAFA MOHATAREM Chief Economist, General Motors

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

Index, nominal terms, 2010 = Energy. Agriculture Metals

Outline Broad commodity price trends Index, nominal terms, 2010 = 100 180 150 Energy 120 90 60 Agriculture Metals 30 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Source:

Outline Broad commodity price trends Index, nominal terms, 2010 = 100 180 150 Energy 120 90 60 Agriculture Metals 30 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Source:

Global Containerboard Outlook

Global Containerboard Outlook European Conference March 2018 Gleb Sinavskis Economist, European Paper Packaging Copyright 2018 RISI, Inc. Proprietary Information Gleb Sinavskis Economist, European Paper

Global Containerboard Outlook European Conference March 2018 Gleb Sinavskis Economist, European Paper Packaging Copyright 2018 RISI, Inc. Proprietary Information Gleb Sinavskis Economist, European Paper

UK Trade Statistics 2017

Value ( million) Rate of Exchange (USD against GBP) ORNAMENTAL AQUATIC TRADE ASSOCIATION LTD. "The Voice of the Ornamental Fish Industry" 1 st Floor Office Suite, Wessex House 4 Station Road, Westbury,

Value ( million) Rate of Exchange (USD against GBP) ORNAMENTAL AQUATIC TRADE ASSOCIATION LTD. "The Voice of the Ornamental Fish Industry" 1 st Floor Office Suite, Wessex House 4 Station Road, Westbury,

The outlook: what we know, the known unknowns and the unknown unknowns

The outlook: what we know, the known unknowns and the unknown unknowns 24 April 2017 Seoul Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1

The outlook: what we know, the known unknowns and the unknown unknowns 24 April 2017 Seoul Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1

Utility Debt Securitization Authority 2013 T/TE Billed Revenues Tracking Report

Utility Debt Securitization Authority 2013 T/TE Billed Revenues Tracking Report Billing Budgeted Billed Dollar Percent Month Revenues Revenues Variance Variance Jan 2018 11,943,180.68 12,697,662.47 754,481.79

Utility Debt Securitization Authority 2013 T/TE Billed Revenues Tracking Report Billing Budgeted Billed Dollar Percent Month Revenues Revenues Variance Variance Jan 2018 11,943,180.68 12,697,662.47 754,481.79

Muhlenkamp & Company. Webinar December 1, Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Macro-economic risk and the outlook for aviation

Macro-economic risk and the outlook for aviation 25 th January 2018, Dublin Brian Pearce, Chief Economist, IATA www.iata.org/economics Macro matters 24% 20% Global GDP and RPK growth 12% 10% 16% 12% 8%

Macro-economic risk and the outlook for aviation 25 th January 2018, Dublin Brian Pearce, Chief Economist, IATA www.iata.org/economics Macro matters 24% 20% Global GDP and RPK growth 12% 10% 16% 12% 8%

Global economy maintaining solid growth momentum. Canada leading the pack

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Beef Cattle Market Update

Beef Cattle Market Update August 8, 2017 Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences University of Missouri brownsc@missouri.edu http://amap.missouri.edu Twitter

Beef Cattle Market Update August 8, 2017 Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences University of Missouri brownsc@missouri.edu http://amap.missouri.edu Twitter

Financial Crises: Past and Future. Carmen M Reinhart Harvard University Adam Smith Lecture NABE 60 th Annual Meeting, Boston, September 30, 2018

Financial Crises: Past and Future Carmen M Reinhart Harvard University Adam Smith Lecture NABE 60 th Annual Meeting, Boston, September 30, 2018 Roadmap The post-crisis decade Global risks: Advanced economies

Financial Crises: Past and Future Carmen M Reinhart Harvard University Adam Smith Lecture NABE 60 th Annual Meeting, Boston, September 30, 2018 Roadmap The post-crisis decade Global risks: Advanced economies

URBAN LAND INSTITUTE

URBAN LAND INSTITUTE 2012 ULI FALL MEETING (Denver, 18 October 2012) The Global Economic Outlook Dark clouds on the horizon Andrea Boltho Magdalen College University of Oxford Oxford Economics and REAG

URBAN LAND INSTITUTE 2012 ULI FALL MEETING (Denver, 18 October 2012) The Global Economic Outlook Dark clouds on the horizon Andrea Boltho Magdalen College University of Oxford Oxford Economics and REAG

Recent Events in the Market for Canadian Snow Crab

Recent Events in the Market for Canadian Snow Crab Overview The quantity of snow crab produced and exported by Canada increased dramatically through the late 1990s, but has levelled off and remained quite

Recent Events in the Market for Canadian Snow Crab Overview The quantity of snow crab produced and exported by Canada increased dramatically through the late 1990s, but has levelled off and remained quite

2012 Annual Conference THE HEAT IS ON! A New World Competition

2012 Annual Conference THE HEAT IS ON! A New World Competition Going for Gold! Review of Global Hotel Performance with a focus on Olympic performance Elizabeth Winkle, STR Global InterContinental Buckhead

2012 Annual Conference THE HEAT IS ON! A New World Competition Going for Gold! Review of Global Hotel Performance with a focus on Olympic performance Elizabeth Winkle, STR Global InterContinental Buckhead

India: Can the Tiger Economy Continue to Run?

India: Can the Tiger Economy Continue to Run? India s GDP is on the rise US$ trillions Nominal GDP (left axis) GDP growth (right axis) 3.0 2.5 2.0 1.5 1.0 0.5 0.0 1990 1992 1994 1996 1998 2000 2002 2004

India: Can the Tiger Economy Continue to Run? India s GDP is on the rise US$ trillions Nominal GDP (left axis) GDP growth (right axis) 3.0 2.5 2.0 1.5 1.0 0.5 0.0 1990 1992 1994 1996 1998 2000 2002 2004

Selected Interest & Exchange Rates

(51/517) OMA f* Lt UCSMit» s s s " Selected Interest & Exchange Rates Weekly Series of Charts January 25, 1982 Prepared by the FINANCIAL MARKETS SECTION DIVISION OF INTERNATIONAL FINANCE BOARD OF GOVERNORS

(51/517) OMA f* Lt UCSMit» s s s " Selected Interest & Exchange Rates Weekly Series of Charts January 25, 1982 Prepared by the FINANCIAL MARKETS SECTION DIVISION OF INTERNATIONAL FINANCE BOARD OF GOVERNORS

Babson Capital/UNC Charlotte Economic Forecast. May 13, 2014

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Composition of Federal Spending

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

The Herzliya Conference The Economic Dimension Prof. Rafi Melnick Provost, Interdisciplinary Center (IDC) Herzliya

Herzliya") The Herzliya Conference The Economic Dimension 2009 Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

The Herzliya Conference The Economic Dimension 2009 Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

Unconventional Monetary Policy: Thoughts on the U.S. and Japanese Experiences

Unconventional Monetary Policy: Thoughts on the U.S. and Japanese Experiences International Conference on Capital Flows and Safe Assets John Rogers Senior Adviser Federal Reserve Board May 27, 2013 The

Unconventional Monetary Policy: Thoughts on the U.S. and Japanese Experiences International Conference on Capital Flows and Safe Assets John Rogers Senior Adviser Federal Reserve Board May 27, 2013 The

A comment on recent events, and...

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

From Recession to Recovery

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

Selected Interest & Exchange Rates

(5/517) Selected Interest & Exchange Rates Weekly Series of Charts i January 29, 1990 Prepared by the FINANCIAL MARKETS SECTION DIVISION OF INTERNATIONAL FINANCE BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM

(5/517) Selected Interest & Exchange Rates Weekly Series of Charts i January 29, 1990 Prepared by the FINANCIAL MARKETS SECTION DIVISION OF INTERNATIONAL FINANCE BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM

Can China Pilot a Soft Landing? 2017 Article IV Consultation Analysis, Outlook, and Policy Advice

Can China Pilot a Soft Landing? 2017 Article IV Consultation Analysis, Outlook, and Policy Advice September 2017 1 KEY RECENT DEVELOPMENTS China has had strong growth momentum which Real GDP Real GDP Stabilizes

Can China Pilot a Soft Landing? 2017 Article IV Consultation Analysis, Outlook, and Policy Advice September 2017 1 KEY RECENT DEVELOPMENTS China has had strong growth momentum which Real GDP Real GDP Stabilizes

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

U.S. Economic Activity. Federal Reserve Bank of Dallas

U.S. Economic Activity Federal Reserve Bank of Dallas 2019 Contents 1 Economic Activity 2 Wages and Prices 3 Financial Activity Economic Activity Economic Activity Index 160 Consumer Confidence and Sentiment

U.S. Economic Activity Federal Reserve Bank of Dallas 2019 Contents 1 Economic Activity 2 Wages and Prices 3 Financial Activity Economic Activity Economic Activity Index 160 Consumer Confidence and Sentiment

U.S. Economic Activity. Federal Reserve Bank of Dallas

U.S. Economic Activity Federal Reserve Bank of Dallas 2019 Contents 1 Economic Activity 2 Wages and Prices 3 Financial Activity Economic Activity Economic Activity New Orders for Durable Goods Billions

U.S. Economic Activity Federal Reserve Bank of Dallas 2019 Contents 1 Economic Activity 2 Wages and Prices 3 Financial Activity Economic Activity Economic Activity New Orders for Durable Goods Billions

U.S. Economic Activity. Federal Reserve Bank of Dallas

U.S. Economic Activity Federal Reserve Bank of Dallas 2019 Contents 1 Economic Activity 2 Wages and Prices 3 Financial Activity Economic Activity Economic Activity Index 160 Consumer Confidence and Sentiment

U.S. Economic Activity Federal Reserve Bank of Dallas 2019 Contents 1 Economic Activity 2 Wages and Prices 3 Financial Activity Economic Activity Economic Activity Index 160 Consumer Confidence and Sentiment

Airline industry outlook 2019

Airline industry outlook 2019 Brian Pearce Chief Economist 12 December 2018 Million barrels a day US$ per barrel Are the markets signalling recession ahead? 60 55 Business confidence (left scale) FTSE

Airline industry outlook 2019 Brian Pearce Chief Economist 12 December 2018 Million barrels a day US$ per barrel Are the markets signalling recession ahead? 60 55 Business confidence (left scale) FTSE

National and Regional Economic Outlook. Central Southern CAA Conference

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes. Tom Rogers. Lead Economist, Oxford Economics.

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

Monetary policy in a fixedexchange-rate. Presentation by Anders Møller Christensen Assistant Governor, Danmarks Nationalbank May 2006

Monetary policy in a fixedexchange-rate regime Presentation by Anders Møller Christensen Assistant Governor, Danmarks Nationalbank May 2006 MONETARY-POLICY STRATEGIES 24-05-2006 DANMARKS NATIONALBANK 2

Monetary policy in a fixedexchange-rate regime Presentation by Anders Møller Christensen Assistant Governor, Danmarks Nationalbank May 2006 MONETARY-POLICY STRATEGIES 24-05-2006 DANMARKS NATIONALBANK 2

UK Trade Statistics 2016

Value ( million) Rate of Exchange (USD against GBP) ORNAMENTAL AQUATIC TRADE ASSOCIATION LTD. "The Voice of the Ornamental Fish Industry" 1 st Floor Office Suite, Wessex House 4 Station Road, Westbury,

Value ( million) Rate of Exchange (USD against GBP) ORNAMENTAL AQUATIC TRADE ASSOCIATION LTD. "The Voice of the Ornamental Fish Industry" 1 st Floor Office Suite, Wessex House 4 Station Road, Westbury,

Trade Growth - Fundamental Driver of Port Operations and Development Strategies

Trade Growth - Fundamental Driver of Port Operations and Development Strategies Marine Terminal Management Training Program October 15, 2007 Long Beach, CA Paul Bingham Global Insight, Inc. 1 Agenda Economic

Trade Growth - Fundamental Driver of Port Operations and Development Strategies Marine Terminal Management Training Program October 15, 2007 Long Beach, CA Paul Bingham Global Insight, Inc. 1 Agenda Economic

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Global economic cycle has slowed

Year-on-year % change Confidence index, 50= no change Global economic cycle has slowed 25% 70 20% International trade growth 65 15% 10% Industrial production growth 60 5% 55 0% 50-5% Business confidence

Year-on-year % change Confidence index, 50= no change Global economic cycle has slowed 25% 70 20% International trade growth 65 15% 10% Industrial production growth 60 5% 55 0% 50-5% Business confidence

The future of the Euro Area and Its Enlargement. André Sapir

The future of the Euro Area and Its Enlargement André Sapir Outline EMU: lessons from the crisis When should Romania join EMU? Lessons from the crisis: What was wrong with EMU 1.0? Impact of EMU on financial

The future of the Euro Area and Its Enlargement André Sapir Outline EMU: lessons from the crisis When should Romania join EMU? Lessons from the crisis: What was wrong with EMU 1.0? Impact of EMU on financial

Ministry of Economy and Sustainable Development of Georgia

Ministry of Economy and Sustainable Development of Georgia Economic Growth 42,000.0 36,000.0 30,000.0 24,000.0 18,000.0 12,000.0 6,000.0 0.0 GDP AND ECONOMIC GROWTH 7.2% 6.2% 6.4% 4.6% 4.8% 3.4% 2.9% 2.8%

Ministry of Economy and Sustainable Development of Georgia Economic Growth 42,000.0 36,000.0 30,000.0 24,000.0 18,000.0 12,000.0 6,000.0 0.0 GDP AND ECONOMIC GROWTH 7.2% 6.2% 6.4% 4.6% 4.8% 3.4% 2.9% 2.8%

Colombia: Economic Adjustment and Outlook. Andres-Mauricio Velasco Technical Deputy Minister of Finance, Republic of Colombia February 2018

Colombia: Economic Adjustment and Outlook Andres-Mauricio Velasco Technical Deputy Minister of Finance, Republic of Colombia February 2018 What is Colombian Ministry of Finance s outlook and funding strategies

Colombia: Economic Adjustment and Outlook Andres-Mauricio Velasco Technical Deputy Minister of Finance, Republic of Colombia February 2018 What is Colombian Ministry of Finance s outlook and funding strategies

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip?

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Commemorative Books Coverage List

Commemorative Books Coverage List England International Football 2018 Date of Paper Pages Event Covered (Daily Mirror ) 3 Apr 1905 Pages 8 and 14 England 1 Scotland 0 (Home Championship) 5 Apr 1909 Page

Commemorative Books Coverage List England International Football 2018 Date of Paper Pages Event Covered (Daily Mirror ) 3 Apr 1905 Pages 8 and 14 England 1 Scotland 0 (Home Championship) 5 Apr 1909 Page

DECLINE IN COMMODITY PRICES GCC OUTLOOK NOVEMBER 22 ND, 2015

DECLINE IN COMMODITY PRICES GCC OUTLOOK NOVEMBER 22 ND, 2015 1 EVERYONE HAS A PLAN UNTIL THEY GET PUNCHED IN THE FACE 2 HE WHO IS NOT COURAGEOUS ENOUGH TO TAKE RISKS WILL ACCOMPLISH NOTHING IN LIFE 3 IT

DECLINE IN COMMODITY PRICES GCC OUTLOOK NOVEMBER 22 ND, 2015 1 EVERYONE HAS A PLAN UNTIL THEY GET PUNCHED IN THE FACE 2 HE WHO IS NOT COURAGEOUS ENOUGH TO TAKE RISKS WILL ACCOMPLISH NOTHING IN LIFE 3 IT

Global trade: how does it look?

Edmonton, December 2018 Global trade: how does it look? Marie-France Paquet The Office of the Chief Economist Global Affairs Canada Overview 1. Canadian economy at a glance 2. Provincial economy at a glance

Edmonton, December 2018 Global trade: how does it look? Marie-France Paquet The Office of the Chief Economist Global Affairs Canada Overview 1. Canadian economy at a glance 2. Provincial economy at a glance

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

The Mystery of Growing Foreign Exchange Reserve

The Mystery of Growing Foreign Exchange Reserve January - March 2007 Total increase = $136 Billion Trade surplus 34% To be explained 54% Net FDI inflow 12% Source: PBoC Renminbi Pressure Indicator Initial

The Mystery of Growing Foreign Exchange Reserve January - March 2007 Total increase = $136 Billion Trade surplus 34% To be explained 54% Net FDI inflow 12% Source: PBoC Renminbi Pressure Indicator Initial

Post-Bubble Global Trends. AAPA Webinar. February 18, Dr. Walter Kemmsies, Chief Economist Moffatt & Nichol Commercial Analysis Group

Post-Bubble Global Trends AAPA Webinar February 18, 2009 Dr. Walter Kemmsies, Chief Economist Moffatt & Nichol Commercial Analysis Group Takeaways The world economy is circling the drain World is wealthier

Post-Bubble Global Trends AAPA Webinar February 18, 2009 Dr. Walter Kemmsies, Chief Economist Moffatt & Nichol Commercial Analysis Group Takeaways The world economy is circling the drain World is wealthier

Chart Collection for Morning Briefing

Chart Collection for Morning Briefing September 11, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 4-664-1333 aquintana@ Please visit our sites at blog. thinking outside the box 4.6 4.4 4.2

Chart Collection for Morning Briefing September 11, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 4-664-1333 aquintana@ Please visit our sites at blog. thinking outside the box 4.6 4.4 4.2

Forecast evaluation report Robert Chote Chairman

Forecast evaluation report 2017 Robert Chote Chairman Background to the FER The FER is an annual report looking at the performance of past EFO forecasts against the latest outturn data Rationale Accountability

Forecast evaluation report 2017 Robert Chote Chairman Background to the FER The FER is an annual report looking at the performance of past EFO forecasts against the latest outturn data Rationale Accountability

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

18 th May Global Steel Industry Trends: Is the perception the reality?

18 th May 2004 Global Steel Industry Trends: Is the perception the reality? Investors have perceived the steel industry negatively Poor returns over the long term, high volatility, relatively small size

18 th May 2004 Global Steel Industry Trends: Is the perception the reality? Investors have perceived the steel industry negatively Poor returns over the long term, high volatility, relatively small size

Steel Market Outlook. AM/NS Calvert

Steel Market Outlook AM/NS Calvert Agenda Economic indicators Key steel consuming markets and forecasted demand Steel consumptions trends Global steel markets and raw materials Comments on trade 1 U.S.

Steel Market Outlook AM/NS Calvert Agenda Economic indicators Key steel consuming markets and forecasted demand Steel consumptions trends Global steel markets and raw materials Comments on trade 1 U.S.

Selected Interest & Exchange Rates

5 Yyc l51/517) \ \. > ' v.j : V ' Selected Interest & Exchange Rates Weekly Series of Charts i November 8, 1982 Prepared by the FINANCIAL MARKETS SECTION DIVISION OF INTERNATIONAL FINANCE BOARD OF GOVERNORS

5 Yyc l51/517) \ \. > ' v.j : V ' Selected Interest & Exchange Rates Weekly Series of Charts i November 8, 1982 Prepared by the FINANCIAL MARKETS SECTION DIVISION OF INTERNATIONAL FINANCE BOARD OF GOVERNORS

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis. May 8 th, Presented by:

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis May 8 th, 2008 Presented by: Patricia Croft, Vice President & Chief Economist Phillips, Hager & North Investment Management Limited

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis May 8 th, 2008 Presented by: Patricia Croft, Vice President & Chief Economist Phillips, Hager & North Investment Management Limited

Predicting the Markets: Chapter 12 Charts: Predicting Currencies

Predicting the Markets: Chapter 12 Charts: October 5, 218 Dr. Edward Yardeni Chief Investment Strategist Mali Quintana Senior Economist info@yardenibook.com Please visit our sites at www. blog. thinking

Predicting the Markets: Chapter 12 Charts: October 5, 218 Dr. Edward Yardeni Chief Investment Strategist Mali Quintana Senior Economist info@yardenibook.com Please visit our sites at www. blog. thinking

Presentation from the USDA Agricultural Outlook Forum 2017

Presentation from the USDA Agricultural Outlook Forum 2017 United States Department of Agriculture 93 rd Annual Agricultural Outlook Forum A New Horizon: The Future of Agriculture February 23-24, 2017

Presentation from the USDA Agricultural Outlook Forum 2017 United States Department of Agriculture 93 rd Annual Agricultural Outlook Forum A New Horizon: The Future of Agriculture February 23-24, 2017

Selected Interest & Exchange Rates

(516/517) h. Selected Interest & Exchange Rates Weekly Series of Charts November 22, 1982 DIVISION OF INTERNATIONAL FINANCE Prepared by the BOARD OF GOVERNORS FINANCIAL MARKETS FEDERAL RESERVE SYSTEM SECTION

(516/517) h. Selected Interest & Exchange Rates Weekly Series of Charts November 22, 1982 DIVISION OF INTERNATIONAL FINANCE Prepared by the BOARD OF GOVERNORS FINANCIAL MARKETS FEDERAL RESERVE SYSTEM SECTION

President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H. Parker Willis Lecture in Political Economics

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

Three-speed economic recovery

Three-speed economic recovery Projection after 2012 GDP growth, percent 10 8 6 4 2 0-2 Euro area -4-6 1992 1996 2000 2004 2008 2012 2016 Source: IMF WEO, April 2013. Emerging market and developing economies

Three-speed economic recovery Projection after 2012 GDP growth, percent 10 8 6 4 2 0-2 Euro area -4-6 1992 1996 2000 2004 2008 2012 2016 Source: IMF WEO, April 2013. Emerging market and developing economies

Sulphur Market Outlook

Sulphur Market Outlook Meena Chauhan Head of Sulphur and Sulphuric Acid Integer Research The Fertilizer Institute Outlook and Technology conference Fort Lauderdale, Florida Founded in 2002, Integer Research

Sulphur Market Outlook Meena Chauhan Head of Sulphur and Sulphuric Acid Integer Research The Fertilizer Institute Outlook and Technology conference Fort Lauderdale, Florida Founded in 2002, Integer Research

Farmland Booms and Busts: Will the Cycle be Broken?

Farmland Booms and Busts: Will the Cycle be Broken? Kansas Society of Farm Managers and Rural Appraisers Salina, KS February 23 rd, 2012 Brian C. Briggeman Associate Professor and Director of the Arthur

Farmland Booms and Busts: Will the Cycle be Broken? Kansas Society of Farm Managers and Rural Appraisers Salina, KS February 23 rd, 2012 Brian C. Briggeman Associate Professor and Director of the Arthur

Fund Performance Bulletin

Fund Performance Bulletin July 20, 200 July 20, 200 Page of 0 PATHFINDER B20 Hansard Pathfinder UK 29/0/99.27.72 -.78-2.7. -20...94 27.00 2.2 C20 Hansard Pathfinder America /2/98 0.9.04 -.40 -. 9.0 -.20

Fund Performance Bulletin July 20, 200 July 20, 200 Page of 0 PATHFINDER B20 Hansard Pathfinder UK 29/0/99.27.72 -.78-2.7. -20...94 27.00 2.2 C20 Hansard Pathfinder America /2/98 0.9.04 -.40 -. 9.0 -.20