The Energy Years Leading Trinidad and Tobago s energy sector in a time of global change

|

|

|

- Everett Elliott

- 6 years ago

- Views:

Transcription

1 The Energy Years Leading Trinidad and Tobago s energy sector in a time of global change By Kevin C. Ramnarine KBH Center, University of Texas at Austin January

2 Structure of Lecture The global energy context and megatrends in present Trinidad and Tobago energy sector overview Major policy decisions 2011 to 2015 High points 2011 to 2015 Low points 2011 to 2015 Lessons Learnt / Conclusion

3 What s the big idea? Oil and gas producing countries must have a competitive investment environment that attracts capital and strikes a balance between fair returns to the State for extraction of its resources and fair returns to the company for risks it has taken.

4 The global energy context and megatrends in present

Globalization ( access to acreage) Climate Change debate ( decarbonization) Geopolitics")

5 Major energy trends driven by. Technology ( 3D seismic, microprocessing, fracking) Globalization ( access to acreage) Climate Change debate ( decarbonization) Geopolitics Increased energy demand driven by Asia (China & India, population and economic growth) Texan George Mitchell Father of Fracking

6 The Climate Change debate has dominated the global policy agenda for this decade and impacted on energy policy in most countries. There are persons who question that the burning fossil fuels has caused climate change ( anthropogenic climate change)

7 Key oil supply trends 2010 to present Supply Growth in supply outstrips growth in demand in Increased American and Iraqi production of shale oil. Oil prices collapse. Same trend for natural gas Country 2010 production / bopd 2015 production/ bpod United States % Iraq % Colombia % Saudi Arabia % OECD % OPEC % World % % change

8 Barrels of Oil per day Oil Production in USA, Russia and Saudi Arabia 1996 to Saudi Arabia Russia USA

9 BCFD 80.0 Natural Gas Production 1996 to Axis Title Russia Iran Qatar USA

10 MTOE Primary Energy Consumption Millions of Tonnes of Oil Equivalent (MTOE) Total North America Total S. & Cent. America Total Europe & Eurasia Total Middle East Total Africa Total Asia Pacific

11 MTOE 1000 United States' Oil, Gas and Coal Consumption 1965 to Oil Gas Coal

12 MTOE Oil remains king of the world Gas Coal Oil

13 In 2011, the IEA asked Are we entering a Golden Age of Gas?

14 Millions of Tonnes of Carbon Dioxide Carbon Dioxide Emissions / millions of tonnes 1965 to Japan USA Germany China

15 MTOE 250 Global Wind and Solar Capacity 1995 to OECD Solar Non OECD Solar OECD Wind Non OECD Wind

16

17 Trinidad and Tobago energy sector overview

18 Trinidad and Tobago Overview Commercial Oil production started in 1908 Currently producing 71,000 bopd ( peak 1978) One Refinery capacity 165,000 bopd Currently producing 3.3 billion cubic feet of gas per day ( similar to UK and Argentina and West Virgina) Most gas produced from offshore / continental shelf by multi-nationals

Five Gas Fired power plants ( 2 GW) Main State players: Petrotrin, NGC Main MNC s: BP, Shell, BHP Billiton, EOG Resources and Repsol LNG exported mainly to South")

19 T&T Overview continued Eleven Ammonia plants ( first 1959) Seven Methanol plants ( first 1984) One Natural Gas processing plant. Four LNG Trains ( first export 1999) Five Gas Fired power plants ( 2 GW) Main State players: Petrotrin, NGC Main MNC s: BP, Shell, BHP Billiton, EOG Resources and Repsol LNG exported mainly to South America Ammonia, methanol exported mainly to the USA Refined petroleum products exported mainly to Caribbean and USA. Kevin C. Ramnarine Trinidad s Point Lisas industrial estate at night 1/24/2017

20 BOED 107 years of oil and gas production Trinidad and Tobago 800, , , , , ,000 Nat Gas 200, ,000 0 Land Oil Marine Oil

21 Barrels of Oil Per day mmcfd of natural gas 160,000 Oil and Gas Production 2000 to 2015 ( The emergence of the gas economy of Trinidad and Tobago) 5, , , ,000 4,500 4,000 3,500 3,000 80,000 2,500 60,000 40,000 20,000 2,000 1,500 1, Oil Prod Natural Gas Prod

22 With the Amoco deal we got Trinidad and Tobago which turned out to be one of the combined group s crown jewels Lord John Browne former CEO of BP plc, Beyond Business

23 GDP Per capita US$ current prices 1960 to 2015 ( Trinidad and Tobago vs LATAM and Caribbean)

24 3/1/1995 8/1/1995 1/1/1996 6/1/ /1/1996 4/1/1997 9/1/1997 2/1/1998 7/1/ /1/1998 5/1/ /1/1999 3/1/2000 8/1/2000 1/1/2001 6/1/ /1/2001 4/1/2002 9/1/2002 2/1/2003 7/1/ /1/2003 5/1/ /1/2004 3/1/2005 8/1/2005 1/1/2006 6/1/ /1/2006 4/1/2007 9/1/2007 2/1/2008 7/1/ /1/2008 5/1/ /1/2009 3/1/2010 8/1/2010 1/1/2011 6/1/ /1/2011 4/1/2012 9/1/2012 2/1/2013 7/1/ /1/2013 5/1/ /1/2014 3/1/2015 8/1/2015 1/1/2016 6/1/2016 Millions of USD 3500 Current Account of Trinidad and Tobago 1995 to 2016 / US$ Mn Series1,

25 Millions of Tonnes Per Annum REAL GDP ($TT Billions) LNG Production vs Real GDP 2000 to

26 Trillion Cubic Feet PROVEN RESERVES OF NATURAL GAS TRINIDAD AND TOBAGO 2002 TO Proven Natural Gas Reserves are in decline

27 Guiding Philosophy and Policy Framework

28 My Guiding Philosophy 1. Maintain the integrity of the Ministry of Energy ( respect is earned). 2. Appreciated that the oil and gas business is high risk and capital intensive. 3. Never compromise safety for production or results. 4. Companies will invest if they think they can get the minimum return that satisfies their shareholders. 5. Capital is mobile, it does not have to come to Trinidad goes where it is treated the best.

29 My Guiding Philosophy 6. We should be doing business with the best companies in the world. 7. Recognize the companies that have demonstrated long term commitment to Trinidad. 8. The Government is in a partnership with the companies we are not adversaries. 9. The public directly should own part of the energy sector.

30 Policy Direction Simplify petroleum taxation regime Reduction in levels of taxation. Increase cost recovery rates in PSC s. Restructure capital allowances to improve project economics. Simplify bidding process ( only 2 biddable items) Get ride of taxable PSC Vertical integration of the National Gas Company Initial Public Offerings are great vehicles to transfer wealth Empowerment of private sector partners of Petrotrin. Communicate effectively with the public and stakeholders.

31 Govt Revenue Reserves & Production Drilling Investment Correct Incentives

32 High Points 2011 to 2015

33 Govt Revenue Reserves & Production Drilling Investment Correct Incentives

34 FDI 2000 to 2015 / Petroleum Related ( TT Central Bank Data)

production sharing contracts and/")

35 Upstream Activity on Steroids Signed twenty one (21) production sharing contracts and/ licenses for exploration and production. This is the largest number ever signed by any Minister of Energy and Energy Affairs. These agreements constitute an investment of up to $US 2.0 billion and creates an active upstream programme for the remainder of the current decade.

36 Rig Days Took initiatives that led to a significant turnaround in upstream activity as evidenced by an increase in rig days from 1132 rig days in 2010 to 2443 rig days in In addition, there was a significant increase in acquisition of 2D/3D seismic data during the aforementioned period. 4,000 3,500 3,000 2,500 2,000 1,500 1, ,600 3,331 2,472 Rig Days ( Trinidad and Tobago) 2000 to ,369 2,501 2,214 3,274 3,409 2, ,132 2,189 2,788 2,486 2,443 2,

37 BP Rig Days BP s Rig Days

38 August 2014 January 2017

39 Initial Public Offering (IPO) of Phoenix Park Phoenix Park Gas Processors Limited Initial Public Offering (IPO) or TTNGL IPO (August 2015). This was the first time an energy company was listed on the Trinidad and Tobago Stock Exchange. This IPO was successful and was oversubscribed by 1.5 times.

40

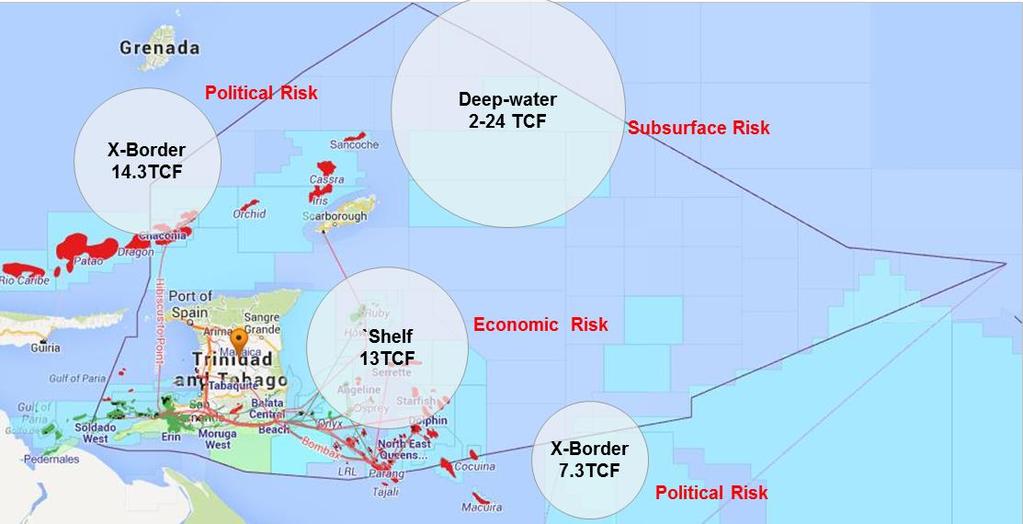

41 PDVSA Head Office, Caracas - July 2013 Between 2012 and 2015 three agreements were negotiated and signed with the Venezuelan Government on the development of cross border natural gas reserves.

42 Port of Spain, Trinidad February 2015

of a Methanol to Di-")

43 Mitsubishi of Japan invest in methanol plant Presided over the progress to Final Investment Decision (FID) of a Methanol to Di- Methyl Ether petrochemical complex by a consortium led by Mitsubishi Gas Chemical of Japan and including the Trinidad based conglomerate Massy. This investment is valued at $US 987 million and will create 2000 construction jobs and 200 permanent jobs in a depressed community in south Trinidad.

44 Low Points 2011 to 2015

45 Kevin C. Ramnarine 1/24/2017 1/24/2017

46

47

48

49 Looking forward and Conclusions

50 mmcfd 4500 T&T supply demand balance 2016 to DCQ Total Sales

.")

51 Deepwater Exploration Opened up Trinidad and Tobago s deepwater acreage to exploration. In total nine production sharing contracts were signed with BHP Billiton and its partners. Arising out of these nine contracts, in 2014/2015, BHP Billiton conducted the largest 3D seismic survey ever conducted by an International Oil Company (20,199 square kilometers).

52 Estimates of the Ministry Of Energy of the potential of the deepwater for oil resources range from 2.2 billion to 8.2 billion barrels of oil initially in place. Deepwater Area

.")

53 Conclusion.the bad news Trinidad is past its peak gas production of 4.3 billion cubic feet per day in The industry will struggle to keep production above 3.5 billion cubic feet per day beyond Oil production is in continual decline due to issues around the no longer relevant business model of Petrotrin. There will be a need to rationalize Point Lisas and / or Atlantic LNG ( shut down plants). New natural gas projects beyond 2017 will not produce enough gas to offset the decline of mature gas reservoirs.

Potential for Venezuelan gas to come to T&T ( political risk).")

54 Areas of potential..a leader is a dealer in hope Potential for big deepwater discoveries ( BHP s drilling campaign in progress technical and geological risk) Potential for Venezuelan gas to come to T&T ( political risk). Potential to apply technology to increase oil production. ( commercial risk). There is an urgent need to privatize Petrotrin ( political risk). Partnerships with Guyana and Suriname ( political risk).

55 The world is what it is The world is what it is; men who are nothing, who allow themselves to become nothing, have no place in it. From A Bend in the River by Sir V.S Naipaul ( Nobel Prize, Literature 2001)

MIDDLE EAST ENERGY SITUATION AND OUTLOOK IRAQ ENERGY FORUM 2017

MIDDLE EAST ENERGY SITUATION AND OUTLOOK IRAQ ENERGY FORUM 2017 2017 1 OVERVIEW OF GLOBAL ENERGY MARKETS 2 Energy exports/imports (million tonnes) 1990 1995 2000 2005 2010 2014 2015 2020 2025 2030 2035

MIDDLE EAST ENERGY SITUATION AND OUTLOOK IRAQ ENERGY FORUM 2017 2017 1 OVERVIEW OF GLOBAL ENERGY MARKETS 2 Energy exports/imports (million tonnes) 1990 1995 2000 2005 2010 2014 2015 2020 2025 2030 2035

Building on Kyoto: Towards a Realistic Global Climate Change Agreement and What Australia Should Do

Building on Kyoto: Towards a Realistic Global Climate Change Agreement and What Australia Should Do Warwick J. McKibbin & Peter J. Wilcoxen ANU Public Lecture, 3 July 2008 Overview Climate Science Lessons

Building on Kyoto: Towards a Realistic Global Climate Change Agreement and What Australia Should Do Warwick J. McKibbin & Peter J. Wilcoxen ANU Public Lecture, 3 July 2008 Overview Climate Science Lessons

Opening address for dinner-debate

Opening address for dinner-debate Mohammed Barkindo Acting for the OPEC Secretary General European Parliament Strasbourg, France 4 July 2006 1 Outline Importance of EU-OPEC Energy Dialogue Current oil

Opening address for dinner-debate Mohammed Barkindo Acting for the OPEC Secretary General European Parliament Strasbourg, France 4 July 2006 1 Outline Importance of EU-OPEC Energy Dialogue Current oil

Market Report Series Oil 2017

Market Report Series Oil 2017 Neil Atkinson, Head Oil Industry & Markets Division, IEA International Institute for Strategic Studies, Bahrain, 17 September 2017 Oil demand continues to grow but at a slower

Market Report Series Oil 2017 Neil Atkinson, Head Oil Industry & Markets Division, IEA International Institute for Strategic Studies, Bahrain, 17 September 2017 Oil demand continues to grow but at a slower

United Nations Conference on Trade and Development

United Nations Conference on Trade and Development 11 th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 15-16 April 2019, Geneva Saudi economic growth strategy on the face of oil price uncertainty

United Nations Conference on Trade and Development 11 th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 15-16 April 2019, Geneva Saudi economic growth strategy on the face of oil price uncertainty

The transition to sustainable energy

ATSE Symposium The transition to sustainable energy Peter Littlewood 8 Nov 2016 The changing world economy Index 180 170 160 150 140 130 120 110 100 90 Economies less energy intensive Electricity less

ATSE Symposium The transition to sustainable energy Peter Littlewood 8 Nov 2016 The changing world economy Index 180 170 160 150 140 130 120 110 100 90 Economies less energy intensive Electricity less

Energy Trends and Emissions in the Former Soviet Union

Energy Trends and Emissions in the Former Soviet Union GTSP Annual Meeting May 29, 2008 Presented by M. Evans Looking back Overview Economic and demographic trends Energy trends and energy intensity Toward

Energy Trends and Emissions in the Former Soviet Union GTSP Annual Meeting May 29, 2008 Presented by M. Evans Looking back Overview Economic and demographic trends Energy trends and energy intensity Toward

Market Report Series Oil SIEW 2017 launch - 28 March 2017

Market Report Series Oil 2017 SIEW 2017 launch - 28 March 2017 Oil demand continues to grow but at a slower pace 2.0 Global oil demand growth 2014-2022 1.5 1.0 0.5 0.0 2014 2015 2016 2017 2018 2019 2020

Market Report Series Oil 2017 SIEW 2017 launch - 28 March 2017 Oil demand continues to grow but at a slower pace 2.0 Global oil demand growth 2014-2022 1.5 1.0 0.5 0.0 2014 2015 2016 2017 2018 2019 2020

Alaska s Natural Resource Commodities: A 10-Year Outlook

Alaska Resources Development Council November 14-15, 2018 Alaska s Natural Resource Commodities: A 10-Year Outlook David R. Hammond, Ph.D. Principal Mineral Economist Hammond International Group Commodities

Alaska Resources Development Council November 14-15, 2018 Alaska s Natural Resource Commodities: A 10-Year Outlook David R. Hammond, Ph.D. Principal Mineral Economist Hammond International Group Commodities

School of international and Public Affairs. Columbia University Manuel Pinho

School of international and Public Affairs Columbia University Manuel Pinho SPHERE WITH CORE What matters to China matters to the world Do not give lessons to China: Europe and the US The challenges: Growth

School of international and Public Affairs Columbia University Manuel Pinho SPHERE WITH CORE What matters to China matters to the world Do not give lessons to China: Europe and the US The challenges: Growth

Energy Outlook Global and Domestic Trends and Challenges. Dr. John Caldwell Director of Economics, EEI 1

Energy Outlook Global and Domestic Trends and Challenges Dr. John Caldwell Director of Economics, EEI 1 World GDP Growth Other Economies are Outpacing the U.S. Other, 7996.16, 11% Africa, 3962.51, 6% Latin

Energy Outlook Global and Domestic Trends and Challenges Dr. John Caldwell Director of Economics, EEI 1 World GDP Growth Other Economies are Outpacing the U.S. Other, 7996.16, 11% Africa, 3962.51, 6% Latin

Impact of the Global Economic Crisis on the Energy Industries and Economy

ILO Tripartite Caribbean Conference Promoting Human Prosperity beyond the Global Financial Crisis Kingston Jamaica 1-2 April 2009 Impact of the Global Economic Crisis on the Energy Industries and Economy

ILO Tripartite Caribbean Conference Promoting Human Prosperity beyond the Global Financial Crisis Kingston Jamaica 1-2 April 2009 Impact of the Global Economic Crisis on the Energy Industries and Economy

The Urgent Need for Unconventional Gas to sustain Canada s Natural Gas Production. Dave Russum, P.Geol. AJM Petroleum Consultants and Geo-Help Inc

The Urgent Need for Unconventional Gas to sustain Canada s Natural Gas Production Dave Russum, P.Geol. AJM Petroleum Consultants and Geo-Help Inc CSUG/PTAC Presentation, 18 th November 2004 The Reality

The Urgent Need for Unconventional Gas to sustain Canada s Natural Gas Production Dave Russum, P.Geol. AJM Petroleum Consultants and Geo-Help Inc CSUG/PTAC Presentation, 18 th November 2004 The Reality

Percent

Outline Outline Growth is picking up Percent 6 Advanced economies Emerging and developing economies 5 4 4.9 5.0 4.3 4.4 4.6 4.7 4.7 3.7 3.7 3 2 2.0 2.3 1.6 2.2 2.3 1.9 1.7 1 1.1 1.3 0 2012 2013 2014 2015

Outline Outline Growth is picking up Percent 6 Advanced economies Emerging and developing economies 5 4 4.9 5.0 4.3 4.4 4.6 4.7 4.7 3.7 3.7 3 2 2.0 2.3 1.6 2.2 2.3 1.9 1.7 1 1.1 1.3 0 2012 2013 2014 2015

Living with limits: growth, resources and climate change Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

Living with limits: growth, resources and climate change Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times Grantham Institute for Climate Change Annual Lecture 2011 3 rd November

Living with limits: growth, resources and climate change Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times Grantham Institute for Climate Change Annual Lecture 2011 3 rd November

Oil Prices: Past, Present, & Future

Oil Prices: Past, Present, & Future Gulf Research Center November 23, 2005 A. F. Alhajji*, PhD Gulf Energy Program - Moderator Gulf Research Center Dubai, UAE *A. F. Alhajji, PhD is also George Patten

Oil Prices: Past, Present, & Future Gulf Research Center November 23, 2005 A. F. Alhajji*, PhD Gulf Energy Program - Moderator Gulf Research Center Dubai, UAE *A. F. Alhajji, PhD is also George Patten

Market Report Series. Spanish Energy Club, Madrid, 3 May 2018

Market Report Series Oil 2018 Spanish Energy Club, Madrid, 3 May 2018 Neil Atkinson, Head of Oil Industry and Markets Division Toril Bosoni, Senior Oil Market Analyst, Oil Industry and Markets Division

Market Report Series Oil 2018 Spanish Energy Club, Madrid, 3 May 2018 Neil Atkinson, Head of Oil Industry and Markets Division Toril Bosoni, Senior Oil Market Analyst, Oil Industry and Markets Division

Session 4. Growth. The World Economy Share of Global GDP Year 2011 (PPP)

") Session 4. Growth Stylized Facts on Standards of Living across Countries Characterizing Growth over 1 Years: The US Economy Growth Dynamics of the G7 Countries and the OECD Economies Characterizing Growth

Session 4. Growth Stylized Facts on Standards of Living across Countries Characterizing Growth over 1 Years: The US Economy Growth Dynamics of the G7 Countries and the OECD Economies Characterizing Growth

Global Oil Supplies: Is Supply Constrained? Kevin Lindemer

Global Oil Supplies: Is Supply Constrained? Kevin Lindemer Is Supply Constrained? Signposts continue to indicate a supply constrained world is possible and could emerge, not-with-standing short-term easing.

Global Oil Supplies: Is Supply Constrained? Kevin Lindemer Is Supply Constrained? Signposts continue to indicate a supply constrained world is possible and could emerge, not-with-standing short-term easing.

OPEC. Annual Statistical Bulletin Fuad Al Zayer Head, Data Services Department OPEC September

OPEC Annual Statistical Bulletin 2006 Fuad Al Zayer Head, Data Services Department OPEC 1 13 September 2007 http://www.opec.org 2006, OUTLINE Present the 2006 edition of the OPEC ASB Show examples of topics

OPEC Annual Statistical Bulletin 2006 Fuad Al Zayer Head, Data Services Department OPEC 1 13 September 2007 http://www.opec.org 2006, OUTLINE Present the 2006 edition of the OPEC ASB Show examples of topics

Market Outlook January,

Market Outlook 2004 January, 2004 www.teekay.com Forward Looking Statements This document contains forward-looking statements (as defined in Section 21E of the Securities Exchange Act of 1934, as amended)

Market Outlook 2004 January, 2004 www.teekay.com Forward Looking Statements This document contains forward-looking statements (as defined in Section 21E of the Securities Exchange Act of 1934, as amended)

4 th IEA-IEF-OPEC Symposium on Energy Outlooks. Riyadh, 22 January 2014

4 th IEA-IEF-OPEC Symposium on Energy Outlooks Riyadh, 22 January 2014 Spare or stranded?* mb/d 7.0 Medium-Term Oil Market Balance 6.0 5.0 4.0 3.0 2.0 1.0 0.0-1.0 2004 2005 2006 2007 2008 2009 2010 2011

4 th IEA-IEF-OPEC Symposium on Energy Outlooks Riyadh, 22 January 2014 Spare or stranded?* mb/d 7.0 Medium-Term Oil Market Balance 6.0 5.0 4.0 3.0 2.0 1.0 0.0-1.0 2004 2005 2006 2007 2008 2009 2010 2011

Climate Change & India

Climate Change & India New Delhi How has India warmed over the past 117 years? How the temperatures have increased seasonally? How far away we are from 1.5 degree C target? Methodology 117 years (1901-1916)

Climate Change & India New Delhi How has India warmed over the past 117 years? How the temperatures have increased seasonally? How far away we are from 1.5 degree C target? Methodology 117 years (1901-1916)

DECLINE IN COMMODITY PRICES GCC OUTLOOK NOVEMBER 22 ND, 2015

DECLINE IN COMMODITY PRICES GCC OUTLOOK NOVEMBER 22 ND, 2015 1 EVERYONE HAS A PLAN UNTIL THEY GET PUNCHED IN THE FACE 2 HE WHO IS NOT COURAGEOUS ENOUGH TO TAKE RISKS WILL ACCOMPLISH NOTHING IN LIFE 3 IT

DECLINE IN COMMODITY PRICES GCC OUTLOOK NOVEMBER 22 ND, 2015 1 EVERYONE HAS A PLAN UNTIL THEY GET PUNCHED IN THE FACE 2 HE WHO IS NOT COURAGEOUS ENOUGH TO TAKE RISKS WILL ACCOMPLISH NOTHING IN LIFE 3 IT

OPEC MARKET SHARE 60% 50% 40% 30% 20% 10% ACTUAL DOE IEA PEL PIRA DBAB DRI-WEFA

2025 2030 OPEC MARKET SHARE 60% 50% 40% 30% 20% 10% 0% 22 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 ACTUAL DOE IEA PEL PIRA DBAB DRI-WEFA PRICE OUTLOOK $60 $50 $40 1999$/BBL $30 $20 $10 $0

2025 2030 OPEC MARKET SHARE 60% 50% 40% 30% 20% 10% 0% 22 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 ACTUAL DOE IEA PEL PIRA DBAB DRI-WEFA PRICE OUTLOOK $60 $50 $40 1999$/BBL $30 $20 $10 $0

SUMMARY. Natural Gas In The World 2017 Edition

CEDIGAZ, the International Association for Natural Gas SUMMARY Natural Gas In The World 217 Edition CEDIGAZ, October 217 NATURAL GAS IN THE WORLD 217 SUMMARY Worldwide proven natural gas reserves grew

CEDIGAZ, the International Association for Natural Gas SUMMARY Natural Gas In The World 217 Edition CEDIGAZ, October 217 NATURAL GAS IN THE WORLD 217 SUMMARY Worldwide proven natural gas reserves grew

Major Issues and Trends Facing the Port and Marine Transportation Industry

Major Issues and Trends Facing the Port and Marine Transportation Industry Presented to: AAPA Marine Terminal Management Training Program April 24, 2006 Charleston Riverview Hotel Charleston, SC - USA

Major Issues and Trends Facing the Port and Marine Transportation Industry Presented to: AAPA Marine Terminal Management Training Program April 24, 2006 Charleston Riverview Hotel Charleston, SC - USA

INVESTMENT OPPORTUNITIES AND FUTURE BIDDING ROUNDS IN PERU

INVESTMENT OPPORTUNITIES AND FUTURE BIDDING ROUNDS IN PERU Dr. Daniel Saba De Andrea Chairman of the Board 17th Latin Oil Week RIO DE JANEIRO 2011 PERÚ An attractive country to invest in E&P activities

INVESTMENT OPPORTUNITIES AND FUTURE BIDDING ROUNDS IN PERU Dr. Daniel Saba De Andrea Chairman of the Board 17th Latin Oil Week RIO DE JANEIRO 2011 PERÚ An attractive country to invest in E&P activities

Producer - Consumer Dialogue - Rising to New Challenges -

Producer - Consumer Dialogue - Rising to New Challenges - Klaus Rehaag Head, Oil Industry & Markets Division Editor, Oil Market Report International Energy Agency Paris, France klaus.rehaag@iea.org Asia

Producer - Consumer Dialogue - Rising to New Challenges - Klaus Rehaag Head, Oil Industry & Markets Division Editor, Oil Market Report International Energy Agency Paris, France klaus.rehaag@iea.org Asia

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies Chief Economist, PAGI Group, JLL (Port, Airport & Global Infrastructure) Agenda Where are we in the cycle? What are the barriers

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies Chief Economist, PAGI Group, JLL (Port, Airport & Global Infrastructure) Agenda Where are we in the cycle? What are the barriers

ENERGY TRANSITION PATHWAYS FOR THE 2030 AGENDA IN ASIA AND THE PACIFIC

ENERGY TRANSITION PATHWAYS FOR THE 2030 AGENDA IN ASIA AND THE PACIFIC Hongpeng Liu Director, Energy Division, UNESCAP Objectives and progress of Energy Transition Asia-Pacific policy-makers face three

ENERGY TRANSITION PATHWAYS FOR THE 2030 AGENDA IN ASIA AND THE PACIFIC Hongpeng Liu Director, Energy Division, UNESCAP Objectives and progress of Energy Transition Asia-Pacific policy-makers face three

OIL MARKET OUTLOOK, MAIN UNCERTAINTY FACTORS & PRICE INDICATIONS TO Symposium Energieinnovation

OIL MARKET OUTLOOK, MAIN UNCERTAINTY FACTORS & PRICE INDICATIONS TO 2020 11. Symposium Energieinnovation 23 February 2010 Johannes Benigni JBC Energy GmbH 10. Februar 2010 Research Energy Studies Consulting

OIL MARKET OUTLOOK, MAIN UNCERTAINTY FACTORS & PRICE INDICATIONS TO 2020 11. Symposium Energieinnovation 23 February 2010 Johannes Benigni JBC Energy GmbH 10. Februar 2010 Research Energy Studies Consulting

Global Construction Outlook: Laura Hanlon Product Manager, Global Construction Outlook May 21, 2009

Global Construction Outlook: Short-term term Pain, Long-term Gain Laura Hanlon Product Manager, Global Construction Outlook May 21, 2009 What This Means for You The world is set to be hit this year with

Global Construction Outlook: Short-term term Pain, Long-term Gain Laura Hanlon Product Manager, Global Construction Outlook May 21, 2009 What This Means for You The world is set to be hit this year with

U.S. and Ohio Midstream Infrastructure Development

U.S. and Ohio Midstream Infrastructure Development Findings and Results from ICF s Study for American Petroleum Institute, April 2017, U.S. Oil and Gas Infrastructure Investment through 2035 An Engine

U.S. and Ohio Midstream Infrastructure Development Findings and Results from ICF s Study for American Petroleum Institute, April 2017, U.S. Oil and Gas Infrastructure Investment through 2035 An Engine

Rebalancing Global Crude Flows

Rebalancing Global Crude Flows John R. Auers Executive Vice President AIChE Dallas Chapter April Section Meeting April 28, 2015 Page 1 TM&C North American Crude & Condensate Outlook TM&C began publishing

Rebalancing Global Crude Flows John R. Auers Executive Vice President AIChE Dallas Chapter April Section Meeting April 28, 2015 Page 1 TM&C North American Crude & Condensate Outlook TM&C began publishing

Rebalancing Global Crude Flows

Rebalancing Global Crude Flows John Mayes Director of Special Studies AFPM Annual Meeting San Antonio, Texas March 24, 2015 TM&C North American Crude & Condensate Outlook TM&C publishes North American

Rebalancing Global Crude Flows John Mayes Director of Special Studies AFPM Annual Meeting San Antonio, Texas March 24, 2015 TM&C North American Crude & Condensate Outlook TM&C publishes North American

Market Opportunities for Irish Dairy 2025

Market Opportunities for Irish Dairy 2025 National Dairy Conference 2014 Red Cow Moran Hotel, Dublin Aidan Cotter Chief Executive Wednesday, 19 th November, 2014 AIDAN COTTER BORD BIA CHIEF EXECUTIVE 28

Market Opportunities for Irish Dairy 2025 National Dairy Conference 2014 Red Cow Moran Hotel, Dublin Aidan Cotter Chief Executive Wednesday, 19 th November, 2014 AIDAN COTTER BORD BIA CHIEF EXECUTIVE 28

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Downstream. Mike Wirth Executive Vice President Chevron Corporation

Downstream Mike Wirth Executive Vice President 2 Strategy Focused on Improving Returns Improve returns and grow earnings across the value chain Operational Excellence Focused refining and marketing portfolio

Downstream Mike Wirth Executive Vice President 2 Strategy Focused on Improving Returns Improve returns and grow earnings across the value chain Operational Excellence Focused refining and marketing portfolio

India: Can the Tiger Economy Continue to Run?

India: Can the Tiger Economy Continue to Run? India s GDP is on the rise US$ trillions Nominal GDP (left axis) GDP growth (right axis) 3.0 2.5 2.0 1.5 1.0 0.5 0.0 1990 1992 1994 1996 1998 2000 2002 2004

India: Can the Tiger Economy Continue to Run? India s GDP is on the rise US$ trillions Nominal GDP (left axis) GDP growth (right axis) 3.0 2.5 2.0 1.5 1.0 0.5 0.0 1990 1992 1994 1996 1998 2000 2002 2004

Iran Unrivalled Market in the Middle East

ITALY-IRAN COOPERATION Through ICC-ISCE Iran Unrivalled Market in the Middle East an Overview Table of Contents An Introduction to ISCE Iran s Economy at a Glance Construction Market Table of Contents

ITALY-IRAN COOPERATION Through ICC-ISCE Iran Unrivalled Market in the Middle East an Overview Table of Contents An Introduction to ISCE Iran s Economy at a Glance Construction Market Table of Contents

Organized Session 3: Protectionism and BRICS economies

ASIA-PACIFIC RESEARCH AND TRAINING NETWORK ON TRADE ARTNeT CONFERENCE ARTNeT Trade Economists Conference Trade in the Asian century - delivering on the promise of economic prosperity 22-23 rd September

ASIA-PACIFIC RESEARCH AND TRAINING NETWORK ON TRADE ARTNeT CONFERENCE ARTNeT Trade Economists Conference Trade in the Asian century - delivering on the promise of economic prosperity 22-23 rd September

Geopolitics of Natural Gas

Geopolitics of Natural Gas A joint study: Energy Forum of the Baker Institute Rice University Program on Energy and Sustainable Development Stanford University Amy M. Jaffe and David G. Victor Study Conference

Geopolitics of Natural Gas A joint study: Energy Forum of the Baker Institute Rice University Program on Energy and Sustainable Development Stanford University Amy M. Jaffe and David G. Victor Study Conference

Petrochemical Industry in China

Petrochemical Industry in China - Growing Demand and Supply in the Future by Qu Guangdong Director, SRI Consulting Beijing Office 1 Chemical Industry In China Contents Macro Economic Situation in China

Petrochemical Industry in China - Growing Demand and Supply in the Future by Qu Guangdong Director, SRI Consulting Beijing Office 1 Chemical Industry In China Contents Macro Economic Situation in China

1. Electricity demand was higher than expected

South Africa s Power Crisis: understanding its root causes and assessing efforts to restore supply security Centre for Development and Enterprise Round Table 5 May 2008 Prof Anton Eberhard Management Program

South Africa s Power Crisis: understanding its root causes and assessing efforts to restore supply security Centre for Development and Enterprise Round Table 5 May 2008 Prof Anton Eberhard Management Program

Promoting Competitiveness in Latin America and the Caribbean. Panel: International Trade and. Gabriel Duque Deputy Foreign Trade Minister

Promoting Competitiveness in Latin America and the Caribbean Panel: International Trade and Global Integration Ministry of Trade, Industry and Tourism Gabriel Duque Deputy Foreign Trade Minister Mexico

Promoting Competitiveness in Latin America and the Caribbean Panel: International Trade and Global Integration Ministry of Trade, Industry and Tourism Gabriel Duque Deputy Foreign Trade Minister Mexico

Global SURF (Subsea Umbilicals, Risers and Flowlines) Market: 2018 World Market Review and Forecast to 2023

Market: 2018 World Market Review and Forecast to 2023") Global SURF (Subsea Umbilicals, Risers and Flowlines) Market: 2018 World Market Review and Forecast to 2023 By Water Depth Shallow Water and Deep Water By Type- Umbilical, Riser and Flowlines By Umbilical

Global SURF (Subsea Umbilicals, Risers and Flowlines) Market: 2018 World Market Review and Forecast to 2023 By Water Depth Shallow Water and Deep Water By Type- Umbilical, Riser and Flowlines By Umbilical

Maximizing the Value Chain

Trinidad and Tobago Energy Conference 2018 The Trini Potential Pat Bishop 2010 Transforming the T&T Natural Gas Industry: Maximizing the Value Chain Mark Loquan, President The National Gas Company of Trinidad

Trinidad and Tobago Energy Conference 2018 The Trini Potential Pat Bishop 2010 Transforming the T&T Natural Gas Industry: Maximizing the Value Chain Mark Loquan, President The National Gas Company of Trinidad

The best design acknowledges that you can't disconnect the form from the material.

Sir Jonathan Ive Senior Vice President of Design, Apple Inc. The best design acknowledges that you can't disconnect the form from the material. The material informs the form. The only way to make the MacBook

Sir Jonathan Ive Senior Vice President of Design, Apple Inc. The best design acknowledges that you can't disconnect the form from the material. The material informs the form. The only way to make the MacBook

It s time to sober up!

It s time to sober up! Uppsala University, Sweden Pisa, July 2006 Kjell [ ] A World Addicted to Oil "We have a serious problem. America is addicted to oil, which is often imported from unstable parts of

It s time to sober up! Uppsala University, Sweden Pisa, July 2006 Kjell [ ] A World Addicted to Oil "We have a serious problem. America is addicted to oil, which is often imported from unstable parts of

ENERGY TRANSITION PATHWAYS FOR THE 2030 AGENDA IN ASIA AND THE PACIFIC

ENERGY TRANSITION PATHWAYS FOR THE 2030 AGENDA IN ASIA AND THE PACIFIC Mr Hongpeng Liu Director, Energy Division, Economic and Social Commission for Asia and the Pacific Objectives and progress of the

ENERGY TRANSITION PATHWAYS FOR THE 2030 AGENDA IN ASIA AND THE PACIFIC Mr Hongpeng Liu Director, Energy Division, Economic and Social Commission for Asia and the Pacific Objectives and progress of the

Oil Markets. Kevin Lindemer Executive Managing Director, Energy Markets Group

Oil Markets Kevin Lindemer Executive Managing Director, Energy Markets Group 2008 Outlook Downside risks in demand are increasing due to weaker economic outlook Upside supply risks still present but balance

Oil Markets Kevin Lindemer Executive Managing Director, Energy Markets Group 2008 Outlook Downside risks in demand are increasing due to weaker economic outlook Upside supply risks still present but balance

Lawrence J. Lau 刘遵义. CSIS Forum Washington, D.C., 22nd May 2013

U.S.-China Economic Relations in the Next Ten Years: Towards Deeper Engagement and Mutual Benefit Lawrence J. Lau 刘遵义 Ralph and Claire Landau Professor of Economics, The Chinese Univ. of Hong Kong and

U.S.-China Economic Relations in the Next Ten Years: Towards Deeper Engagement and Mutual Benefit Lawrence J. Lau 刘遵义 Ralph and Claire Landau Professor of Economics, The Chinese Univ. of Hong Kong and

U.S. Oil & Gas Industry Chartbook

U.S. Oil & Gas Industry Chartbook BBVA Research USA Houston, TX July 2015 DISCLAIMER This document was prepared by Banco Bilbao Vizcaya Argentaria s (BBVA) BBVA Research U.S. on behalf of itself and its

U.S. Oil & Gas Industry Chartbook BBVA Research USA Houston, TX July 2015 DISCLAIMER This document was prepared by Banco Bilbao Vizcaya Argentaria s (BBVA) BBVA Research U.S. on behalf of itself and its

Short and Medium-Term Oil Market Outlook. 13 th Shanghai Derivatives Market Forum - 25 May 2016

Short and Medium-Term Oil Market Outlook 13 th Shanghai Derivatives Market Forum - 25 May 2016 Oil world changed on Nov. 27 th 2014 $/bbl 120 Brent crude oil 100 80 60 40 Copyright 2016 Argus Media 20

Short and Medium-Term Oil Market Outlook 13 th Shanghai Derivatives Market Forum - 25 May 2016 Oil world changed on Nov. 27 th 2014 $/bbl 120 Brent crude oil 100 80 60 40 Copyright 2016 Argus Media 20

Cheese (American, Italian, Hard, Soft, Fresh and Others) Market - Global Industry Analysis, Size, Share, Growth, Trends and Forecast,

Market - Global Industry Analysis, Size, Share, Growth, Trends and Forecast,") Cheese (American, Italian, Hard, Soft, Fresh and Others) Market - Global Industry Analysis, Size, Share, Growth, Trends and Forecast, 2013-2019 ResearchMoz include new market research report" Cheese (American,

Cheese (American, Italian, Hard, Soft, Fresh and Others) Market - Global Industry Analysis, Size, Share, Growth, Trends and Forecast, 2013-2019 ResearchMoz include new market research report" Cheese (American,

The World Picture A View for Sea Trade

The World Picture A View for Sea Trade Presented to: AAPA Marine Terminal Management October 20, 2008 Baltimore, MD Presented by: Scott Sigman Principal, Global Trade & Transportation IHS Global Insight

The World Picture A View for Sea Trade Presented to: AAPA Marine Terminal Management October 20, 2008 Baltimore, MD Presented by: Scott Sigman Principal, Global Trade & Transportation IHS Global Insight

What can we expect from the energy markets in 2017?

What can we expect from the energy markets in 2017? Luc De Leersnyder & Jens Lievens E&C Consultants 23/11/2016 What do we do? ENERGY PROCUREMENT CONSULTANCY Gas & electricity Focused on price, not on

What can we expect from the energy markets in 2017? Luc De Leersnyder & Jens Lievens E&C Consultants 23/11/2016 What do we do? ENERGY PROCUREMENT CONSULTANCY Gas & electricity Focused on price, not on

Pacific Rim Coal Marketing

Wyoming Infrastructure Authority Spring Energy Conference June 11-12, 2015 Cheyanne Pacific Rim Coal Marketing Michael Mewing MC2 Company Pty Limited Pacific Rim Coal Marketing * Asia s reliance on coal

Wyoming Infrastructure Authority Spring Energy Conference June 11-12, 2015 Cheyanne Pacific Rim Coal Marketing Michael Mewing MC2 Company Pty Limited Pacific Rim Coal Marketing * Asia s reliance on coal

Global growth prospects

Global growth prospects Percent 6 Advanced Economies Emerging Markets and Developing Economies 5 4.9 5.0 4.7 4.7 4.5 4 4.3 4.3 3.7 3.7 3 2 2.3 2.3 2.2 2.0 2.0 1.7 1.7 1 1.1 1.3 0 2012 2013 2014 2015 2016

Global growth prospects Percent 6 Advanced Economies Emerging Markets and Developing Economies 5 4.9 5.0 4.7 4.7 4.5 4 4.3 4.3 3.7 3.7 3 2 2.3 2.3 2.2 2.0 2.0 1.7 1.7 1 1.1 1.3 0 2012 2013 2014 2015 2016

Energy Security: Markets and Policy

Energy Security: Markets and Policy Pierre Noël EPRG, University of Cambridge Critical Infrastructure Conference, London, 20 April 2011 Contents Global Oil and the Middle East European Gas and Russia Japan

Energy Security: Markets and Policy Pierre Noël EPRG, University of Cambridge Critical Infrastructure Conference, London, 20 April 2011 Contents Global Oil and the Middle East European Gas and Russia Japan

A New Dawn? Mike Beveridge - Managing Director

A New Dawn? Mike Beveridge - Managing Director January 2017 Fit at 50? 2 January 2018 Life Begins At 70? 3 What A Difference A Year Makes: From $55/bbl to $70/bbl $US 75 LTM Max: $70 70 65 60 55 LTM Avg:

A New Dawn? Mike Beveridge - Managing Director January 2017 Fit at 50? 2 January 2018 Life Begins At 70? 3 What A Difference A Year Makes: From $55/bbl to $70/bbl $US 75 LTM Max: $70 70 65 60 55 LTM Avg:

NITC Outlook On Middle East Oil Movement & Tanker Shipping

NITC Outlook On Middle East Oil Movement & Tanker Shipping Presented by: Mohammad Souri Chairman & CEO, NITC Intertanko s Annual Event Istanbul, 20-23 April 2008 1 Country Oil Proven Reserve Billion Barrel

NITC Outlook On Middle East Oil Movement & Tanker Shipping Presented by: Mohammad Souri Chairman & CEO, NITC Intertanko s Annual Event Istanbul, 20-23 April 2008 1 Country Oil Proven Reserve Billion Barrel

Comparison of urban energy use and carbon emission in Tokyo, Beijing, Seoul and Shanghai

International Workshop on Urban Energy and Carbon Modeling, February 5-6, 28, AIT Centre, Asian Institute of Technology, Pathumthani, Thailand Comparison of urban energy use and carbon emission in Tokyo,

International Workshop on Urban Energy and Carbon Modeling, February 5-6, 28, AIT Centre, Asian Institute of Technology, Pathumthani, Thailand Comparison of urban energy use and carbon emission in Tokyo,

2019 Global Travel Forecast: Air, Hotel and Ground Prices

2019 Global Travel Forecast: Air, Hotel and Ground Prices Methodology 28 countries and 10 US cities Airlines, Hotel, Rental Car Forecast in USD, guidelines on currency exchange forecast Forecast projections

2019 Global Travel Forecast: Air, Hotel and Ground Prices Methodology 28 countries and 10 US cities Airlines, Hotel, Rental Car Forecast in USD, guidelines on currency exchange forecast Forecast projections

How is Natural Gas Availability Curtailing the growth of DRI production in the MENA region?

How is Natural Gas Availability Curtailing the growth of DRI production in the MENA region? 29 April 2014 World DRI & Pellet Congress Abu Dhabi Robert Smith 1 The Issues Natural gas availability in the

How is Natural Gas Availability Curtailing the growth of DRI production in the MENA region? 29 April 2014 World DRI & Pellet Congress Abu Dhabi Robert Smith 1 The Issues Natural gas availability in the

Global Outlook for Agriculture Trend versus Cycle

Global Outlook for Agriculture Trend versus Cycle Michael Swanson Ph.D. Wells Fargo October 2017 Everything is connected we just don t see how. Connection corollary: Nothing natural moves in a straight

Global Outlook for Agriculture Trend versus Cycle Michael Swanson Ph.D. Wells Fargo October 2017 Everything is connected we just don t see how. Connection corollary: Nothing natural moves in a straight

ROLE OF COPPER IN CHILEAN ECONOMY

ROLE OF COPPER IN CHILEAN ECONOMY Patricio Meller, Bernardo Lara & Gonzalo Valdés January 2010 1 Basic Data: Chile 2009 Population (millions) 17 Yn/cap (US$ PPP) 14,299 GDP (billions US$) 243 Territory

ROLE OF COPPER IN CHILEAN ECONOMY Patricio Meller, Bernardo Lara & Gonzalo Valdés January 2010 1 Basic Data: Chile 2009 Population (millions) 17 Yn/cap (US$ PPP) 14,299 GDP (billions US$) 243 Territory

The Future of the World s International Education

The Future of the World s International Education long-term driving forces or trends that influence almost everything at all levels of societal development. They have great importance now, and we are relatively

The Future of the World s International Education long-term driving forces or trends that influence almost everything at all levels of societal development. They have great importance now, and we are relatively

SUSTAINABILITY CRITERIA FOR FISHERIES SUBSIDIES: THE LATIN AMERICAN CONTEXT

SUSTAINABILITY CRITERIA FOR FISHERIES SUBSIDIES: THE LATIN AMERICAN CONTEXT 29-30 July 2009, Guayaquil, Ecuador The Sunken Billions Kieran Kelleher Fisheries Team Leader The World Bank The Economic Justification

SUSTAINABILITY CRITERIA FOR FISHERIES SUBSIDIES: THE LATIN AMERICAN CONTEXT 29-30 July 2009, Guayaquil, Ecuador The Sunken Billions Kieran Kelleher Fisheries Team Leader The World Bank The Economic Justification

Trade Growth - Fundamental Driver of Port Operations and Development Strategies

Trade Growth - Fundamental Driver of Port Operations and Development Strategies Marine Terminal Management Training Program October 15, 2007 Long Beach, CA Paul Bingham Global Insight, Inc. 1 Agenda Economic

Trade Growth - Fundamental Driver of Port Operations and Development Strategies Marine Terminal Management Training Program October 15, 2007 Long Beach, CA Paul Bingham Global Insight, Inc. 1 Agenda Economic

IN THE MIDST OF A PHASE CHANGE

IN THE MIDST OF A PHASE CHANGE NEW ZEALAND WIND ENERGY ASSOCIATION CONFERENCE, WELLINGTON 2014 KOBAD BHAVNAGRI TWITTER: @KOBADB / / // / Kobad Bhavnagri NZ Wind Energy Association Conference, April 2014

IN THE MIDST OF A PHASE CHANGE NEW ZEALAND WIND ENERGY ASSOCIATION CONFERENCE, WELLINGTON 2014 KOBAD BHAVNAGRI TWITTER: @KOBADB / / // / Kobad Bhavnagri NZ Wind Energy Association Conference, April 2014

Outline. Overview of globalization. Global outlook for real economic activity & inflation. Risks to the outlook

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

Shifts in the Geopolitical Landscape and Their Impact on Petroleum Sector Capex Strategies

Shifts in the Geopolitical Landscape and Their Impact on Petroleum Sector Capex Strategies Golden, CO April 14, 2016 Thomas A. Petrie, CFA Chairman, Petrie Partners Figure 1 Chaos Prevails Russia Wins

Shifts in the Geopolitical Landscape and Their Impact on Petroleum Sector Capex Strategies Golden, CO April 14, 2016 Thomas A. Petrie, CFA Chairman, Petrie Partners Figure 1 Chaos Prevails Russia Wins

South Asia. Economy and trade. Shailesh Garg Director General Manager Drewry Maritime Services Pvt. Ltd

South Asia Economy and trade 10 October 2018 Shailesh Garg Director General Manager Drewry Maritime Services Pvt. Ltd. +91 124 497 4950 shailesh@drewry.co.uk Agenda Global & regional overview Country overview

South Asia Economy and trade 10 October 2018 Shailesh Garg Director General Manager Drewry Maritime Services Pvt. Ltd. +91 124 497 4950 shailesh@drewry.co.uk Agenda Global & regional overview Country overview

Index, nominal terms, 2010 = Energy. Agriculture Metals

Outline Broad commodity price trends Index, nominal terms, 2010 = 100 180 150 Energy 120 90 60 Agriculture Metals 30 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Source:

Outline Broad commodity price trends Index, nominal terms, 2010 = 100 180 150 Energy 120 90 60 Agriculture Metals 30 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Source:

China s energy insecurity: strategies and future prospects

China s energy insecurity: strategies and future prospects Philip Andrews-Speed Centre for Energy, Petroleum and Mineral Law and Policy, University of Dundee Andrews-Speed 1 Energy supply & demand 1,800.00

China s energy insecurity: strategies and future prospects Philip Andrews-Speed Centre for Energy, Petroleum and Mineral Law and Policy, University of Dundee Andrews-Speed 1 Energy supply & demand 1,800.00

The outlook: what we know, the known unknowns and the unknown unknowns

The outlook: what we know, the known unknowns and the unknown unknowns 24 April 2017 Seoul Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1

The outlook: what we know, the known unknowns and the unknown unknowns 24 April 2017 Seoul Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1

An update on Grid parity

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 market volume [TWh] 35.000 30.000 25.000 20.000 15.000 10.000 5.000 - RES COM IND An update on Grid

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 market volume [TWh] 35.000 30.000 25.000 20.000 15.000 10.000 5.000 - RES COM IND An update on Grid

Energy, Economy and Policy: A Glimpse at the 21 st Century

Gas Well Deliquification Workshop Denver, Colorado February, 2009 Energy, Economy and Policy: A Glimpse at the 21 st Century Scott W. Tinker Bureau of Economic Geology Jackson School of Geosciences The

Gas Well Deliquification Workshop Denver, Colorado February, 2009 Energy, Economy and Policy: A Glimpse at the 21 st Century Scott W. Tinker Bureau of Economic Geology Jackson School of Geosciences The

US-China Trade Conflict: Dejavu or New One

US-China Trade Conflict: Dejavu or New One Lessons From US-Japan Trade Conflict in 1980s and 1990s Tamotsu Nakamura & Yoichi Matsubayashi Plan of Talk 1. US-Japan Trade Conflict in Retrospect 2. Similarities

US-China Trade Conflict: Dejavu or New One Lessons From US-Japan Trade Conflict in 1980s and 1990s Tamotsu Nakamura & Yoichi Matsubayashi Plan of Talk 1. US-Japan Trade Conflict in Retrospect 2. Similarities

PEMEX PETROQUIMICA 2013 ANNUAL CONFERENCE. PCI Xylenes & Polyester Doug Rightler

PEMEX PETROQUIMICA 2013 ANNUAL CONFERENCE PCI Xylenes & Polyester Doug Rightler Discussion Points» MEG demand growth by region.» MEG supply - China is in control or is it?» Price drivers - the Chinese

PEMEX PETROQUIMICA 2013 ANNUAL CONFERENCE PCI Xylenes & Polyester Doug Rightler Discussion Points» MEG demand growth by region.» MEG supply - China is in control or is it?» Price drivers - the Chinese

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

2016 Grains & Oilseeds Outlook. The global outlook remains positive. 12/7/2015. Matthew C. Roberts

12/7/215 216 Grains & Oilseeds Outlook Matthew C. Roberts Roberts.628@osu.edu The global outlook remains positive. www.matthewcroberts.com 2 www.matthewcroberts.com 3 www.matthewcroberts.com 4 www.matthewcroberts.com

12/7/215 216 Grains & Oilseeds Outlook Matthew C. Roberts Roberts.628@osu.edu The global outlook remains positive. www.matthewcroberts.com 2 www.matthewcroberts.com 3 www.matthewcroberts.com 4 www.matthewcroberts.com

Agricultural Outlook: Rebalancing U.S. Agriculture

Agricultural Outlook: Rebalancing U.S. Agriculture Michael J. Swanson Ph.D. Agricultural Economist January 2018 2018 Wells Fargo Bank, N.A. All rights reserved. For public use. The U.S. Ag Sector renormalizes!

Agricultural Outlook: Rebalancing U.S. Agriculture Michael J. Swanson Ph.D. Agricultural Economist January 2018 2018 Wells Fargo Bank, N.A. All rights reserved. For public use. The U.S. Ag Sector renormalizes!

Shifting International Trade Routes A National Economic Outlook. February 1, 2011

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

Challenges, Prospects & Opportunities. Seychelles Fisheries Sector

Challenges, Prospects & Opportunities Seychelles Fisheries Sector Geographical Location General information Total population: 94,000 people Total territory: 1,374,000 km 2 Land/Ocean territory:459 km 2

Challenges, Prospects & Opportunities Seychelles Fisheries Sector Geographical Location General information Total population: 94,000 people Total territory: 1,374,000 km 2 Land/Ocean territory:459 km 2

China at a glance 2011

China at a glance 2011 GDP PPP Growth rate Per capita Value US$11.29 trillion 9.2% US$8,400 Ranking 3 7 119 Labor force Imports Exports Value 816.2 million US$1.74 trillion US$1.90 trillion Ranking 1 3

China at a glance 2011 GDP PPP Growth rate Per capita Value US$11.29 trillion 9.2% US$8,400 Ranking 3 7 119 Labor force Imports Exports Value 816.2 million US$1.74 trillion US$1.90 trillion Ranking 1 3

Airlines, the economy and air transport demand

Airlines, the economy and air transport demand Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 Returns for airlines investors lower this year;

Airlines, the economy and air transport demand Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 Returns for airlines investors lower this year;

Airline industry outlook 2019

Airline industry outlook 2019 Brian Pearce Chief Economist 12 December 2018 Million barrels a day US$ per barrel Are the markets signalling recession ahead? 60 55 Business confidence (left scale) FTSE

Airline industry outlook 2019 Brian Pearce Chief Economist 12 December 2018 Million barrels a day US$ per barrel Are the markets signalling recession ahead? 60 55 Business confidence (left scale) FTSE

Car Production. Brazil Mexico. Production in thousands. Source: AMIA Asociacion Mexicana de la industria automotriz.

Car Production Production in thousands 4000 3000 2000 1000 Brazil Mexico 0 2013 2014 2015 Source: AMIA Asociacion Mexicana de la industria automotriz. Mexico s Expanding Middle Class Percent of population

Car Production Production in thousands 4000 3000 2000 1000 Brazil Mexico 0 2013 2014 2015 Source: AMIA Asociacion Mexicana de la industria automotriz. Mexico s Expanding Middle Class Percent of population

Multidimensional Analysis

Multidimensional Analysis of Macro Sustainability of Russia: New Methods for Measuring Progress Dr Stanislav Shmelev, Senior Research Fellow, Oxford University, UK E-mail: s.shmelev@ouce.ox.ac.uk Tel:

Multidimensional Analysis of Macro Sustainability of Russia: New Methods for Measuring Progress Dr Stanislav Shmelev, Senior Research Fellow, Oxford University, UK E-mail: s.shmelev@ouce.ox.ac.uk Tel:

2017 Major Projects Pipeline Report Adrian Hart, Senior Manager Infrastructure & Mining

2017 Major Projects Pipeline Report Adrian Hart, Senior Manager Infrastructure & Mining Major Projects Pipeline Report - 2017 Presentation Outline Key findings of the 2017 Pipeline Report The outlook for

2017 Major Projects Pipeline Report Adrian Hart, Senior Manager Infrastructure & Mining Major Projects Pipeline Report - 2017 Presentation Outline Key findings of the 2017 Pipeline Report The outlook for

China and Latin America: Opportunities and Challenges

China and Latin America: Opportunities and Challenges Alicia García-Herrero - Chief Economist Emerging Markets Economic Research Department BBVA Medellin, IADB Annual Meetings, March 2009 1 Contents China

China and Latin America: Opportunities and Challenges Alicia García-Herrero - Chief Economist Emerging Markets Economic Research Department BBVA Medellin, IADB Annual Meetings, March 2009 1 Contents China

The Mystery of Growing Foreign Exchange Reserve

The Mystery of Growing Foreign Exchange Reserve January - March 2007 Total increase = $136 Billion Trade surplus 34% To be explained 54% Net FDI inflow 12% Source: PBoC Renminbi Pressure Indicator Initial

The Mystery of Growing Foreign Exchange Reserve January - March 2007 Total increase = $136 Billion Trade surplus 34% To be explained 54% Net FDI inflow 12% Source: PBoC Renminbi Pressure Indicator Initial

Key Humanitarian and Development Trends

Key Humanitarian and Development Trends Mikaela Gavas Centre for Aid and Public Expenditure Christina Bennett Humanitarian Policy Group Overseas Development Institute The new global context for development

Key Humanitarian and Development Trends Mikaela Gavas Centre for Aid and Public Expenditure Christina Bennett Humanitarian Policy Group Overseas Development Institute The new global context for development

Your Texas Economy. Current through: Tuesday, Nov 20, 2018

Your Texas Economy Current through: Tuesday, Nov 20, 2018 Overview of Texas Economy The Texas economy is growing robustly in 2018 2018 job growth through October is 2.9 percent annualized compared to 2.1

Your Texas Economy Current through: Tuesday, Nov 20, 2018 Overview of Texas Economy The Texas economy is growing robustly in 2018 2018 job growth through October is 2.9 percent annualized compared to 2.1

Energy Reform in Mexico: Secondary Legislation

Energy Reform in Mexico: Secondary Legislation Dr. Guillermo C. Domínguez Vargas Comisionado Laredo, Tx., May 22, 2014. www.cnh.gob.mx guillermo.dominguez@cnh.gob.mx @DrGCDV Nine Bills 1. Hydrocarbons

Energy Reform in Mexico: Secondary Legislation Dr. Guillermo C. Domínguez Vargas Comisionado Laredo, Tx., May 22, 2014. www.cnh.gob.mx guillermo.dominguez@cnh.gob.mx @DrGCDV Nine Bills 1. Hydrocarbons

International Trade Economic Forecasts An Overview of Orange County and Southern California Exports

International Trade Economic Forecasts An Overview of Orange County and Southern California Exports Mira Farka Adrian R. Fleissig Institute for Economic and Environmental Studies Orange County / Inland

International Trade Economic Forecasts An Overview of Orange County and Southern California Exports Mira Farka Adrian R. Fleissig Institute for Economic and Environmental Studies Orange County / Inland

CXC geo Question 6 Economic Development

CXC geo 2015 Question 6 Economic Development Define the term secondary industry and give one example of a secondary industry that you have studied. 3marks Secondary industries are those industries which

CXC geo 2015 Question 6 Economic Development Define the term secondary industry and give one example of a secondary industry that you have studied. 3marks Secondary industries are those industries which