Zions Bank Economic Overview Meridian Chamber of Commerce. May 2, 2017

|

|

|

- Angelina Harrington

- 6 years ago

- Views:

Transcription

1 Zions Bank Economic Overview Meridian Chamber of Commerce May 2, 2017

2 National Economic Conditions

3 Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Wall Street Journal

4 Current Level of Consumer Confidence Indicates Economic Prosperity Above 110 indicates economic prosperity Apr CCI = Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Source: The Conference Board

5 Expectations of Future Inflation on the Rise

6 NFIB Small Business Optimism Index Source: Trading Economics

7 Irrational Exuberance?

8 Divergence of Soft vs Hard Data

9 Why?

10 Cumulative Job Loss by Months of Recession Thousands Source: Euler Hermes analysis of Bureau of Labor Statistics Data

11 Cumulative Job Loss by Months of Recession Thousands Source: Euler Hermes analysis of Bureau of Labor Statistics Data

12 Index Slower Recovery than Past Recessions Periods from Value Scaled to Recession 2001 Recession 1990 Recession 1981 Recession 1980 Recession 1973 Recession Source: Federal Reserve Bank of St. Louis

13 Slower Recovery than Past Recessions

14 Mixed March Job Indicators Indicator Expectation Actual Total Nonfarm Payrolls 175,000 98,000 Unemployment Rate 4.7% 4.5% Private Payrolls 200,000 89,000 Monthly Average Hourly Wage Growth Yearly Average Hourly Wage Growth 0.3% 0.2% 2.8% 2.7% Labor Force Participation 62.9% 63.0% Sources: Wall street Journal and Bureau of Labor Statistics

15 98,000 Jobs Added in March Million Jobs Lost Payroll Change 000 s Million Jobs Recovered Source: Bureau of Labor Statistics

16 98,000 Jobs Added in March Payroll Change 000 s January-16 February-16 March-16 April-16 May-16 June-16 July-16 August-16 September-16 October-16 November-16 December-16 January-17 February-17 March-17 Source: Bureau of Labor Statistics

17 National Employment Change Percent Change in National Employment by Industry: Mar 2016 to Mar 2017 Ntl. Res. & Mining Construction Manufacturing Trade, Trans., Utilities Information Financial Activity Prof. & Bus. Serv. Ed. & Health Serv. Leisure & Hospitality Other Services Government -1.2% Total: 1.5% 0.4% 0.3% 0.7% 0.9% 0.7% 2.6% 2.2% 3.2% 2.3% 1.7% -2% -1% 0% 1% 2% 3% 4% Source: Bureau of Labor Statistics; seasonally adjusted

18 National Employment Change Total Change in Number of Jobs by Industry in Thousands: Mar 2016 to Mar 2017 Ntl. Res. & Mining Construction Manufacturing Trade, Trans., Utilities Information Financial Activity Prof. & Bus. Serv. Ed. & Health Serv. Leisure & Hospitality Other Services Government Source: Bureau of Labor Statistics; seasonally adjusted

19 Unemployment Rate Indicates Full Employment % = Full Employment Source: Bureau of Labor Statistics

20 Unemployed and Discouraged Workers Down from Last Month U-6 (Underemployed) U-3 (Unemployment) Source: Bureau of Labor Statistics

21 % Labor Force Participation Among Lowest Level in Almost 40 Years Mar % Apr % Mar % Source: U.S. Bureau of Labor Statistics Note: Seasonally adjusted

22 % 68.0 Labor Force Participation Increasing Slightly Source: U.S. Bureau of Labor Statistics Note: Seasonally adjusted

23 90% 80% 70% 60% 50% Civilian Labor Force Participation Rate Male vs Female 40% 30% Men Women Source: Bureau of Labor Statistics

24 Participation Among Women Aged Has Surged

25 4.0% 3.5% Yearly Wage Growth Down Slightly in March Mar % 3.0% 2.5% Average = 2.4% 2.0% 1.5% 1.0% Source: U.S. Bureau of Labor Statistics Note: Growth rate calculated using real chained dollars

26 Producer Price Index Rising Slightly in March Percent Year-to-Year Change Source: Bureau of Labor Statistics; not seasonally adjusted

27 4.5% 4.0% 3.5% 3.0% 2.5% 2.0% 1.5% 1.0% 0.5% 0.0% -0.5% Inflation Above Fed Target But Below Expectations in March U.S. Consumer Price Index Yearly Change Rate Sept 2011 Dec 2011 Mar 2012 Jun 2012 Sept 2012 Dec 2012 Mar 2013 Jun 2013 Sept 2013 Dec 2013 Mar 2014 Jun 2014 Sept 2014 Dec 2014 Mar 2015 Jun 2015 Sep 2015 Dec 2015 Mar 2016 June 2016 Sep 2016 Dec 2016 Mar 2017 Source: Bureau of Labor Statistics

28 Growth in Consumer Spending Under Par Personal Consumption Expenditure Yearly Percent Change Percent Source: Bureau of Economic Analysis

29 Consumers Drive Growth in GDP 6.00% 4.00% 2.00% 0.00% -2.00% -4.00% Government Inventories Net Exports Fixed Investment Personal Consumption Real GDP Growth Q GDP 0.7%

30 = 100 The U.S. Dollar is Strong Trade Weighted U.S. Dollar Index: Broad Source: Federal Reserve

31 Euro compared to U.S. Dollar $1.60 $ $1.40 $1.30 $1.20 $1.10 $1.00 $0.90 $0.80 PARITY 1.06 Source: Federal Reserve Bank of St. Louis

32 U.S. Dollar Compared to Chinese Yuan $6.00 $6.50 $7.00 $7.50 $8.00 $ China stops the yuan s rise 2001 China joins WTO 2005 China allows the yuan to rise 2010 China allows the yuan to rise Aug 2015 China devalues the yuan by largest amount in 20 years Source: Federal Reserve Bank of St. Louis

33

34 $1.80 $1.70 $1.60 $1.50 $1.40 $1.30 $1.20 $1.10 British Pound Dropped to New Low Following BrexitVote Brexit Vote $ Source: Federal Reserve Bank of St. Louis

35 U.S. Total Rig Count Recovering from Low as Oil Prices Rise $120 $110 $100 $90 $80 $70 $60 $50 $40 $30 $ Oil Prices 2015 Source: Baker Hughes and U.S. Energy Information Administration Note: Total count includes oil and gas rigs 2016 Active Oil Rigs ,200 2,000 1,800 1,600 1,400 1,200 1,

36 Federal Funds Target Rate Sees 3 nd Increase in Over a Decade Federal Funds Target Rate = Source: U.S. Federal Reserve

37 March 2017 Fed Rate Increase Projections 4% 3% 3.0% 3.0% 2% 1.4% 2.1% 1% 0% Long Run Source: Board of Governors of the Federal Reserve

38 Idaho Economic Conditions Source: U.S Census Bureau

39 CA 0.7% OR 1.7% WA 1.8% NV 2.0% ID 1.8% AK 0.6% Idaho Population 3 rd Fastest Growing in U.S. UT 2.0% AZ 1.7% MT 1.0% WY -0.2% CO 1.7% NM 0.0% HI 0.2% Percent Change: 2015 to 2016 U.S. Rate = 0.7% ND 0.1% SD 0.9% NE 0.7% TX 1.6% KS 0.3% 0.0% OK 0.4% MN 0.7% IA 0.4% MO 0.3% AR 0.3% WI 0.2% LA 0.3% IL -0.3% MS 0.0% MI 0.1% IN 0.3% TN 0.9% AL 0.2% 1.5% or more OH 0.1% KY 0.3% 0.7% to 1.4% (at or above U.S. rate) 0.2% to 0.6% 0.0% to 0.1% Population Loss WV -0.5% VT -0.2% PA -0.1% NC 1.1% SC 1.4% GA 1.1% VA 0.5% FL 1.8% NH 0.4% NY 0.0% ME 0.2% DC 1.6% CT -0.2% DE 0.8% MD 0.4% MA 0.4% RI 0.1% NJ 0.1% Source: U.S. Census Bureau

40 Total Population 1,800,000 1,600,000 1,400,000 1,200,000 1,000, , ,000 Idaho Population and Components of Change 1,683,140 18,869 10,296 60,000 50,000 40,000 30,000 20,000 10, ,000 Components of Population Change 400, Net Migration Natural Increase Total Population -20,000 Source: Zions Bank analysis of U.S. Census Bureau data

41 Idaho Population Growth Rates By County 2015 to 2016 State Average = 1.8% Increase of 3.0% or Greater Increase of 1.8% to 2.9% Increase of 1.0% to 1.7% Increase of 0.0% to 0.9% Population Loss Boundary 3.1% Bonner 1.8% Kootenai 2.6% Benewah 0.6% Latah 1.2% Nez Perce Lewis 0.6% 1.6% Adams 1.6% Washington 2.1% Payette Gem 0.8% 1.6% Canyon 2.2% Ada 2.4% Owyhee 0.7% Shoshone 0.0% Clearwater 0.2% Boise 1.6% Idaho -0.6% Valley 4.1% Elmore 0.9% Camas 0.7% Gooding -0.1% Custer 0.2% Jerome 1.2% Twin Falls 1.7% Lemhi -0.4% Blaine 1.1% Lincoln -0.7% Cassia 0.0% Butte 0.0% Minidoka 1.1% Power 0.4% Clark -1.4% Jefferson 2.5% Bingham 0.5% Oneida 1.3% Bannock 0.6% Franklin 2.9% Fremont 1.0% MadisonTeton 2.5% 3.7% Bonneville 2.0% Caribou 1.8% Bear Lake 0.7% Source: U.S. Census Bureau

42 CA 2.1% OR 2.2% WA 2.9% Note: Seasonally Adjusted Source: Bureau of Labor Statistics Idaho Employment Growth 6th in the Nation Percent Change in Employment for States: March 2016 to March 2017 U.S. Rate = 1.5% NV 3.0% AK -2.1% ID 2.7% UT 3.2% AZ 2.0% MT 2.1% WY -2.1% HI 0.7% CO 1.9% NM 0.9% ND -0.3% SD 1.6% NE 0.9% KS 0.3% TX 2.1% OK -0.1% MN 1.5% IA 0.5% MO 1.4% AR 1.1% WI 0.9% LA -0.1% IL 0.4% MS 0.0% MI 1.9% IN 1.5% TN 2.2% AL 1.4% OH 0.7% KY 1.5% GA 3.0% WV -0.8% VT 0.9% PA 1.0% NC 1.6% SC 1.8% VA 1.2% FL 3.0% NY 1.2% 2.0% or more 1.6% to 1.9% (at or above the U.S. rate) 1.0% to 1.5% 0.0% to 0.9% Loss ME 0.9% DC 0.8% CT 0.1% DE 0.8% MD 1.6% MA 1.4% RI 0.8% NJ 1.2%

43 Idaho Total Employment at New Highs Thousands of Employees Loss of 59,000 jobs from Gain of 110,100 jobs since low in Total Nonfarm Employment Source: U.S. Bureau of Labor Statistics, Total nonfarm seasonally adjusted Note: Numbers rounded to nearest thousand

44 Idaho Employment Gains and Losses by Industry Percent Change in Idaho Employment by Industry: March 2016 March 2017 Ntl. Res. & Mining Construction Manufacturing Trade, Trans., Utilities Information Financial Activity Prof. & Bus. Serv. Ed. & Health Serv. Leisure & Hospitality Other Services Government -3.0% Total: 2.6% 5.2% 1.9% 1.5% 4.5% 4.5% 2.7% 3.7% 1.7% 2.5% 2.6% -4% -2% 0% 2% 4% 6% Source: Idaho Department of Labor

45 Idaho Employment Gains and Losses by Industry Total Change in Idaho Employment by Industry: March 2016 March 2017 Ntl. Res. & Mining Construction Manufacturing Trade, Trans., Utilities Information Financial Activity Prof. & Bus. Serv. Ed. & Health Serv. Leisure & Hospitality Other Services Government ,000 1,200 2,000 1,500 2,300 3,700 1,200 Total: 18,000 3,200-1, ,000 2,000 3,000 4,000 Source: Idaho Department of Labor

46 Idaho Employment Change Rates By County March 2016 to March 2017 State Rate = 2.7% Boundary -1.1% Bonner 4.9% Kootenai 2.3% Benewah -1.2% Latah 3.9% Nez Perce 2.8% Lewis -0.55% Shoshone 1.7% Clearwater -2.3% Idaho -0.4% 4.0% or more 2.7% to 3.9% 1.0% to 2.6% 0.0% to 0.9% Loss Adams 4.2% Washington Valley 0.5% Elmore -1.6% Source: Idaho Department of Labor, Seasonally Adjusted Total Nonfarm Employment 0.45% Custer Clark 0.2% -2.4% Payette 1.6% Gem 2.3% Canyon 2.7% Ada 2.8% Owyhee 0.7% Boise 2.8% Camas 1.6% Gooding 1.4% Twin Falls 2.1% Lemhi 2.0% Blaine 1.0% Lincoln 0.8% Jerome 2.8% Minidoka 1.1% Cassia 1.1% Butte 2.33% Power 0.2% Jefferson 2.3% Bingham 4.1% Oneida 2.3% Bannock -2.0% Fremont 4.7% MadisonTeton 5.4% 0.9% Bonneville 2.5% Caribou 0.6% Bear Lake Franklin -1.9% 1.3%

47 OR 4.0% 3.8% CA 5.0% 4.9% WA 4.9% 4.7% NV 4.9% 4.8% AK 6.4% ID 3.6% 3.5% UT 3.1% AZ 5.1% 5.0% Note: Seasonally Adjusted Source: Bureau of Labor Statistics ID Unemployment Rates 12 th Lowest in the Nation MT 3.8% HI 2.8% WY 4.7% 4.5% CO 2.9% 2.6% NM 6.7% 6.8% March 2017 U.S. Rate = 4.5% TX 4.9% 5.0% LA 5.7% 5.8% FL 5.0% 4.8% NH 2.7% 2.8% VT ND 3.0% 2.9% 2.8% MN 4.0% 3.8% NY WI SD 4.4% 4.3% 3.7% 3.4% 2.8% MI 5.3% 5.1% PA IA 5.0% 4.8% NE 3.2% 3.1% OH 3.2% 3.1% IL IN 5.1% 5.4% 4.9% 4.1% 3.9% WV VA 5.2% KS MO 4.9% KY 3.9% 3.8% 4.0% 3.8% 4.1% 3.9% 4.9% 5.0% NC 4.9% 5.1% TN 5.3% 5.1% OK AR SC 4.6% 4.3% 3.7% 3.6% 4.4% MS AL GA 5.2% 5.0% 6.2% 5.8% 5.3% 5.1% 3.9% or less 4.0% to 4.7% (at or below U.S. rate) 4.8% to 5.4% 5.5% to 5.9% 6.0% or more ME MA 3.0% 3.2% 3.4% 3.6% RI 4.3% 4.5% CT 4.7% 4.8% NJ 4.4% 4.2% DE 4.5% DC MD 5.7% 5.8% 4.2% 4.3%

48 Idaho Unemployment Rates By County March 2017 State Rate = 3.5% Boundary 5.5% Bonner 5.0% Kootenai 4.3% Benewah 6.9% Latah 3.2% Nez Lewis Perce7.0% 3.1% % Shoshone 7.0% Clearwater 9.0% Idaho 5.5% 3.0% or lower Adams 7.1% Valley 5.1% Lemhi 6.0% 3.1% to 3.6% 3.7% to 5.9% 6.0% to 6.9% 7.0% or greater Washington 5.6% Custer Clark 4.5% 2.0% PayetteGem 6.0% 4.2% Canyon 3.9 Ada 3.0% Owyhee 4.2% Boise 5.4% Elmore 4.1% Camas 3.1% Gooding 2.8% Twin Falls 3.2% Blaine 2.8% Lincoln 4.2% Jerome 3.1% Cassia 2.7% Butte 3.5% Minidoka 2.9% Power 3.6% Jefferson 2.7% Bingham 3.4% Bannock 3.3% Oneida 3.0% Fremont 2,8% Madison Teton 2.1% 3.0% Bonneville 2.9% Caribou 3.7% Bear Lake Franklin 3.4% 2.7% Source: Idaho Department of Labor

49 CA 4.5% WA 4.8% OR 4.5% NV 5.9% UT 5.6% AZ 4.3% Source: Bureau of Economic Analysis ID Personal Income Growth Same as National Average AK -1.0% ID 3.6% Percent Change in Personal Income : U.S. = 3.6%; ID = 3.6% MT 2.3% WY -1.7% HI 4.5% CO 3.9% NM 2.1% ND -1.5% SD 1.2% NE 2.8% KS 2.8% TX 2.9% OK 0.6% MN 3.0% IA 2.3% MO 3.5% AR 3.2% WI 3.1% LA 1.5% IL 3.1% MS 3.2% MI 3.6% IN 3.9% TN 3.9% AL 3.3% 4.0% or more OH 3.0% KY 2.6% GA 4.8% WV 1.0% VT 3.3% PA 2.9% NC 4.1% SC 4.4% VA 3.6% FL 4.9% NH 4.7% NY 2.9% 3.6% to 3.9% (at or above the U.S. rate) 2.0% to 3.5% 0.0% to 1.9% Decrease ME 3.7% DC 4.5% CT 3.0% DE 2.9% MD 3.7% MA 4.3% RI 3.1% NJ 3.2%

50 Construction

51 Idaho Median Home Sale Prices Reaching Approaching Pre-Recession Highs $240,000 $220,000 $200,000 $180,000 $160,000 $140,000 $120,000 $100, Idaho U.S. Source: Graphiq.com reporting data from CoreLogic

52 Idaho Maintains Lower Percentage of Foreclosures than Nation 2008 Percentage of total homes in foreclosure process U.S. Idaho Source: Graphiq.com

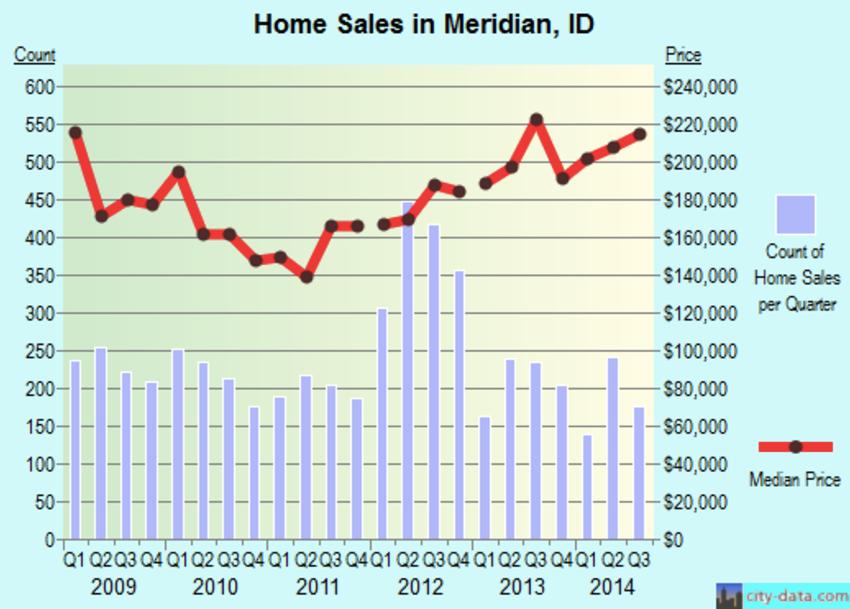

53 25,000 Idaho Residential Construction Activity Slowly Climbing 20,000 15,000 10,000 5, Single-Family Units Multifamily Total f Source: U.S. Department of Commerce and U.S. Census Bureau

54 Millions $3,500 $3,000 $2,500 $2,000 $1,500 $1,000 $500 Idaho Value of New Residential Construction Increasing $ Single Family Units Multi Family Units Total f Source: U.S. Census Bureau

55 Meridian

56 Meridian At a Glance Population 90,739 Unemployment 3.0% Median Income - $54,746 Median Home Value - $213,100 Median Gross Rent - $987 Largest Employers Blue Cross Scentsy Forbes best places to retire 2016

57 Meridian is Experiencing Explosive Growth

58 Manufacturing and Construction Lead Jobs in Meridian

59 Meridian Unemployment Dropping

60 Housing Prices Increasing in Meridian

61

62 Idaho Economic Indicators Population Nonfarm Employment Unemployment Rate Personal Income Housing Starts f 2018f Sources: Idaho Division of Financial Management and Moody s Economy.com e = estimate f = forecast

63 Zions Bank, A Division of ZB, N.A. Member FDIC. Content is offered for informational purposes only and should not be construed as tax, legal, financial or business advice. Please contact a professional about your specific needs and advice. Content may contain trademarks or trade names owned by parties who are not affiliated with ZB, N.A. Use of such marks does not imply any sponsorship by or affiliation with third parties, and ZB, N.A. does not claim any ownership of or make representations about products and services offered under or associated with such marks. Robert Spendlove Economic and Public Policy Officer Robert.Spendlove@zionsbank.com Phone:

Rotary Club of Pocatello Economic Overview. April 28, 2016

Rotary Club of Pocatello Economic Overview April 28, 2016 Economic Headwinds National and international uncertainty Continued low energy prices Depressed business investment Unstable inflation outlook

Rotary Club of Pocatello Economic Overview April 28, 2016 Economic Headwinds National and international uncertainty Continued low energy prices Depressed business investment Unstable inflation outlook

Zions Bank Economic Overview Cache Valley Home Builders Association. April 12, 2017

Zions Bank Economic Overview Cache Valley Home Builders Association April 12, 2017 National Economic Conditions Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source:

Zions Bank Economic Overview Cache Valley Home Builders Association April 12, 2017 National Economic Conditions Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source:

Zions Bank Economic Overview West Point Economic Summit. March 30, 2017

Zions Bank Economic Overview West Point Economic Summit March 30, 2017 National Economic Conditions Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Wall Street

Zions Bank Economic Overview West Point Economic Summit March 30, 2017 National Economic Conditions Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Wall Street

Zions Bank Economic Overview

Zions Bank Economic Overview Kenworth National Dealers Conference November 8, 2018 1 National Economic Conditions 2 Volatility Returns to the Stock Market 27,000 Dow Jones Industrial Average October 10,

Zions Bank Economic Overview Kenworth National Dealers Conference November 8, 2018 1 National Economic Conditions 2 Volatility Returns to the Stock Market 27,000 Dow Jones Industrial Average October 10,

Zions Bank Economic Overview

Zions Bank Economic Overview WIB Education Summit September 19, 2017 National Economic Conditions Dow Breaks 22,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Federal

Zions Bank Economic Overview WIB Education Summit September 19, 2017 National Economic Conditions Dow Breaks 22,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Federal

Zions Bank Economic Overview Utah Government Finance Officers Assoc. April 21, 2017

Zions Bank Economic Overview Utah Government Finance Officers Assoc. April 21, 2017 National Economic Conditions Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source:

Zions Bank Economic Overview Utah Government Finance Officers Assoc. April 21, 2017 National Economic Conditions Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source:

Zions Bank Economic Overview. March 14, 2017

Zions Bank Economic Overview March 14, 2017 National Economic Conditions Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Wall Street Journal 120.0 110.0 100.0

Zions Bank Economic Overview March 14, 2017 National Economic Conditions Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Wall Street Journal 120.0 110.0 100.0

Zions Bank Economic Overview Logan Rotary Club. March 16, 2017

Zions Bank Economic Overview Logan Rotary Club March 16, 2017 National Economic Conditions Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Wall Street Journal

Zions Bank Economic Overview Logan Rotary Club March 16, 2017 National Economic Conditions Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Wall Street Journal

Zions Bank Economic Overview

Zions Bank Economic Overview Intermountain Credit Education League May 10, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around

Zions Bank Economic Overview Intermountain Credit Education League May 10, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around

Zions Bank Economic Overview

Zions Bank Economic Overview Veteran Owned Business Conference May 11, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around Correction

Zions Bank Economic Overview Veteran Owned Business Conference May 11, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around Correction

Zions Bank Economic Overview Utah Bankers Association Emerging Bank Leaders Conference. November 9, 2017

Zions Bank Economic Overview Utah Bankers Association Emerging Bank Leaders Conference November 9, 2017 National Economic Conditions Dow Breaks 23,000 The Trump Bump Dow Reaches New Heights Following U.S.

Zions Bank Economic Overview Utah Bankers Association Emerging Bank Leaders Conference November 9, 2017 National Economic Conditions Dow Breaks 23,000 The Trump Bump Dow Reaches New Heights Following U.S.

Zions Bank Economic Overview Coldwell Banker Commercial Group. November 6, 2017

Zions Bank Economic Overview Coldwell Banker Commercial Group November 6, 2017 National Economic Conditions Dow Breaks 23,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election

Zions Bank Economic Overview Coldwell Banker Commercial Group November 6, 2017 National Economic Conditions Dow Breaks 23,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election

Zions Bank Economic Overview

Zions Bank Economic Overview Utah Valley University Business and Economic Forum May 18, 2017 National Economic Conditions Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election

Zions Bank Economic Overview Utah Valley University Business and Economic Forum May 18, 2017 National Economic Conditions Dow 20,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election

Zions Bank Economic Overview

Zions Bank Economic Overview UAFS & NAIB Convention September 14, 2017 National Economic Conditions Dow Breaks 22,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source:

Zions Bank Economic Overview UAFS & NAIB Convention September 14, 2017 National Economic Conditions Dow Breaks 22,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source:

Zions Bank Municipal Conference Economic Overview August 13, 2015

Zions Bank Municipal Conference Economic Overview August 13, 2015 Overview National Economic Conditions Utah Economic Conditions Utah is One of the Fastest Growing CA 0.9% States in the Country Percent

Zions Bank Municipal Conference Economic Overview August 13, 2015 Overview National Economic Conditions Utah Economic Conditions Utah is One of the Fastest Growing CA 0.9% States in the Country Percent

Zions Bank Economic Overview

Zions Bank Economic Overview Utah Manufacturers Association & Associated General Contractors Utah Finance and Economic Summit September 26, 2017 National Economic Conditions Dow Breaks 22,000 The Trump

Zions Bank Economic Overview Utah Manufacturers Association & Associated General Contractors Utah Finance and Economic Summit September 26, 2017 National Economic Conditions Dow Breaks 22,000 The Trump

Zions Bank Economic Overview

Zions Bank Economic Overview Utah Bankruptcy Lawyers Forum March 20, 2018 National Economic Conditions When Good News is Bad News Is Good News?? Dow Tops 26,000 Up 44% Since 2016 Election Source: Wall

Zions Bank Economic Overview Utah Bankruptcy Lawyers Forum March 20, 2018 National Economic Conditions When Good News is Bad News Is Good News?? Dow Tops 26,000 Up 44% Since 2016 Election Source: Wall

Zions Bank Economic Overview. December 5, 2017

Zions Bank Economic Overview December 5, 2017 National Economic Conditions Dow Breaks 24,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Federal Reserve Bank of

Zions Bank Economic Overview December 5, 2017 National Economic Conditions Dow Breaks 24,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Federal Reserve Bank of

Zions Bank Economic Overview

Zions Bank Economic Overview National Assoc of Credit Managers Member Seminar December 12, 2017 National Economic Conditions Dow Breaks 24,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential

Zions Bank Economic Overview National Assoc of Credit Managers Member Seminar December 12, 2017 National Economic Conditions Dow Breaks 24,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential

Understanding the New Trump Economy Economic Overview. November 17, 2016

Understanding the New Trump Economy Economic Overview November 17, 2016 Uncertainty at the Na@onal and Interna@onal Level Source: Bureau of Labor Statistics The Trump Bump Why? National Job Growth 500

Understanding the New Trump Economy Economic Overview November 17, 2016 Uncertainty at the Na@onal and Interna@onal Level Source: Bureau of Labor Statistics The Trump Bump Why? National Job Growth 500

Zions Bank Economic Overview

Zions Bank Economic Overview Logan Rotary Club June 28, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around Correction Territory

Zions Bank Economic Overview Logan Rotary Club June 28, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around Correction Territory

Economic Forecast to Professional Republican Women Association. January 5, 2017

Economic Forecast to Professional Republican Women Association January 5, 2017 Economic Headwinds National and international uncertainty Continued low energy prices Depressed business investment Unstable

Economic Forecast to Professional Republican Women Association January 5, 2017 Economic Headwinds National and international uncertainty Continued low energy prices Depressed business investment Unstable

More of the Same; Or now for Something Completely Different?

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

Colorado Counties Treasurers Association

Colorado Counties Treasurers Association Place cover image here Richard Wobbekind Executive Director, Business Research Division June 21, 2016 Real GDP Growth Quarterly and Annualized Real GDP 1990-2016

Colorado Counties Treasurers Association Place cover image here Richard Wobbekind Executive Director, Business Research Division June 21, 2016 Real GDP Growth Quarterly and Annualized Real GDP 1990-2016

Overview of the Regional Economy

Overview of the Regional Economy Jason Bram, Research Officer Presentation to the Community Depository Institutions Advisory Council (CDIAC) October 13, 2017 The views expressed here are those of the presenter

Overview of the Regional Economy Jason Bram, Research Officer Presentation to the Community Depository Institutions Advisory Council (CDIAC) October 13, 2017 The views expressed here are those of the presenter

Regional Economic Conditions

Regional Economic Conditions Jason Bram, Research Officer Community Advisory Group Meeting June 27, 2017 The views expressed here are those of the presenter and do not necessarily represent those of the

Regional Economic Conditions Jason Bram, Research Officer Community Advisory Group Meeting June 27, 2017 The views expressed here are those of the presenter and do not necessarily represent those of the

SEASON FINAL REGISTRATION REPORTS

Materials Included: 2015-2016 SEASON FINAL REGISTRATION REPORTS 2014-15 & 2015-16 Comparison by Group 2 2015-16 USA Hockey Member Counts 3 2015-16 8 and Under Report 4 2015-16 Players & Girls/Women by

Materials Included: 2015-2016 SEASON FINAL REGISTRATION REPORTS 2014-15 & 2015-16 Comparison by Group 2 2015-16 USA Hockey Member Counts 3 2015-16 8 and Under Report 4 2015-16 Players & Girls/Women by

Understanding the Regional Divergence in Adult Mortality in the United States

Understanding the Regional Divergence in Adult Mortality in the United States Andrew Fenelon, PhD University of Maryland, College Park American Life Expectancy 77 76 75 Life Expectancy in Years 74 73 72

Understanding the Regional Divergence in Adult Mortality in the United States Andrew Fenelon, PhD University of Maryland, College Park American Life Expectancy 77 76 75 Life Expectancy in Years 74 73 72

Cement & Construction Outlook

Cement & Construction Outlook Minnesota Concrete Council November 17, 2011 Dave Zwicke, PCA Analytics Manager, Sr. Economist Bottom Line Economy in a slow growth period characterized by tepid job gains.

Cement & Construction Outlook Minnesota Concrete Council November 17, 2011 Dave Zwicke, PCA Analytics Manager, Sr. Economist Bottom Line Economy in a slow growth period characterized by tepid job gains.

2009 National Pharmacist Workforce Study. Visual Data

2009 National Pharmacist Workforce Study Visual Data Figure 1.1: National Aggregate g Demand Index Values http://www.pharmacymanpower.com/ 5 4 3 4.28 4.07 Shortage Surplus 4.19 4.07 4.02 3.97 3.92 4.21

2009 National Pharmacist Workforce Study Visual Data Figure 1.1: National Aggregate g Demand Index Values http://www.pharmacymanpower.com/ 5 4 3 4.28 4.07 Shortage Surplus 4.19 4.07 4.02 3.97 3.92 4.21

The MS Economic Outlook The Fall Forum

The Economic Outlook The Fall Forum Darrin Webb, State Economist University Research Center Mississippi Institutions of Higher Learning dwebb@mississippi.edu (601)432 6556 September 2016 University Research

The Economic Outlook The Fall Forum Darrin Webb, State Economist University Research Center Mississippi Institutions of Higher Learning dwebb@mississippi.edu (601)432 6556 September 2016 University Research

Overview of the Regional Economy

Overview of the Regional Economy Jason Bram, Research Officer Presentation to the Community Depository Institutions Advisory Council (CDIAC) March 5, 2019 The views expressed here are those of the presenter

Overview of the Regional Economy Jason Bram, Research Officer Presentation to the Community Depository Institutions Advisory Council (CDIAC) March 5, 2019 The views expressed here are those of the presenter

Economic Growth in the Trump Economy

Economic Growth in the Trump Economy Presented to State Data Center Conference William F. Fox, Director November 18, 2016 GDP Grows, Though Slowly 10.0 8.0 Percentage Change, Previous Qtr, SAAR 6.0 4.0

Economic Growth in the Trump Economy Presented to State Data Center Conference William F. Fox, Director November 18, 2016 GDP Grows, Though Slowly 10.0 8.0 Percentage Change, Previous Qtr, SAAR 6.0 4.0

Anatomy of a Jackpot: Characteristics of Purchasers of Large Jackpot Lottery Tickets

Anatomy of a Jackpot: Characteristics of Purchasers of Large Jackpot Lottery Tickets The 15 th International Conference on Gambling & Risk Taking May 27-31, 2013 Todd Maki & Don Feeney 1 Although not shown

Anatomy of a Jackpot: Characteristics of Purchasers of Large Jackpot Lottery Tickets The 15 th International Conference on Gambling & Risk Taking May 27-31, 2013 Todd Maki & Don Feeney 1 Although not shown

SUMMARY MEMBERSHIP ANALYSIS FOR THE STATE OF. Trends of first-time 4 to 8 year-old male ice hockey players to

SUMMARY MEMBERSHIP ANALYSIS FOR THE STATE OF New York Trends of first-time 4 to 8 year-old male ice hockey players 1997-98 to 27-8 p.2 -Background and Methodology p.3 -National Acquisition and Retention

SUMMARY MEMBERSHIP ANALYSIS FOR THE STATE OF New York Trends of first-time 4 to 8 year-old male ice hockey players 1997-98 to 27-8 p.2 -Background and Methodology p.3 -National Acquisition and Retention

CREATIVE DESTRUCTION AND THE KNOWLEDGE ECONOMY

CREATIVE DESTRUCTION AND THE KNOWLEDGE ECONOMY Where people work and how it has changed. Creative Destruction & the Process of Change The Second Industrial Revolution & Agriculture Miracle. The Third Revolution

CREATIVE DESTRUCTION AND THE KNOWLEDGE ECONOMY Where people work and how it has changed. Creative Destruction & the Process of Change The Second Industrial Revolution & Agriculture Miracle. The Third Revolution

SUMMARY MEMBERSHIP ANALYSIS FOR THE STATE OF. Trends of first-time 4 to 8 year-old male ice hockey players to

SUMMARY MEMBERSHIP ANALYSIS FOR THE STATE OF Rhode Island Trends of first-time 4 to 8 year-old male ice hockey players 1997-98 to 27-8 p.2 -Background and Methodology p.3 -National Acquisition and Retention

SUMMARY MEMBERSHIP ANALYSIS FOR THE STATE OF Rhode Island Trends of first-time 4 to 8 year-old male ice hockey players 1997-98 to 27-8 p.2 -Background and Methodology p.3 -National Acquisition and Retention

SUMMARY MEMBERSHIP ANALYSIS FOR THE STATE OF. New Hampshire. Trends of first-time 4 to 8 year-old male ice hockey players to

SUMMARY MEMBERSHIP ANALYSIS FOR THE STATE OF New Hampshire Trends of first-time 4 to 8 year-old male ice hockey players 1997-98 to 27-8 p.2 -Background and Methodology p.3 -National Acquisition and Retention

SUMMARY MEMBERSHIP ANALYSIS FOR THE STATE OF New Hampshire Trends of first-time 4 to 8 year-old male ice hockey players 1997-98 to 27-8 p.2 -Background and Methodology p.3 -National Acquisition and Retention

SUMMARY MEMBERSHIP ANALYSIS FOR THE STATE OF. Trends of first-time 4 to 8 year-old male ice hockey players to

SUMMARY MEMBERSHIP ANALYSIS FOR THE STATE OF New Mexico Trends of first-time 4 to 8 year-old male ice hockey players 1997-98 to 27-8 p.2 -Background and Methodology p.3 -National Acquisition and Retention

SUMMARY MEMBERSHIP ANALYSIS FOR THE STATE OF New Mexico Trends of first-time 4 to 8 year-old male ice hockey players 1997-98 to 27-8 p.2 -Background and Methodology p.3 -National Acquisition and Retention

Wenlin Liu, Senior Economist. Stateof Wyoming. Economic Analysis Division State of Wyoming 1

WYOMING DEMOGRAPHIC AND ECONOMIC TREND LCCC LIFE Program April 7, 2012 Cheyenne, Wyoming Wenlin Liu, Senior Economist Economic Analysis Division Stateof Wyoming Economic Analysis Division State of Wyoming

WYOMING DEMOGRAPHIC AND ECONOMIC TREND LCCC LIFE Program April 7, 2012 Cheyenne, Wyoming Wenlin Liu, Senior Economist Economic Analysis Division Stateof Wyoming Economic Analysis Division State of Wyoming

Minimum Wages By State, Municipality and County

Compliance Alert January 21 st, 2019 Minimum Wages By State, Municipality and County AL N/A N/A AK $9.89 AZ $11.00 $12.00 - January 1, 2020 Flagstaff $12.00 $13.00 - January 1, 2020 $15.00 - January 1,

Compliance Alert January 21 st, 2019 Minimum Wages By State, Municipality and County AL N/A N/A AK $9.89 AZ $11.00 $12.00 - January 1, 2020 Flagstaff $12.00 $13.00 - January 1, 2020 $15.00 - January 1,

Growth in Moscow: A Study of Modest Population Growth and Rising Economic Prosperity*

Growth in Moscow: A Study of Modest Population Growth and Rising Economic Prosperity* Jon R. Miller Professor of Economics College of Business and Economics University of Idaho Moscow, Idaho Steven Peterson

Growth in Moscow: A Study of Modest Population Growth and Rising Economic Prosperity* Jon R. Miller Professor of Economics College of Business and Economics University of Idaho Moscow, Idaho Steven Peterson

Federal Regulatory Update WTBA/WisDOT Contractor/Engineer Conference

Federal Regulatory Update 2019 WTBA/WisDOT Contractor/Engineer Conference by Nick Goldstein ARTBA Vice President of Regulatory & Legal Issues January 17, 2019 How the Public Feels Regulations and Transportation

Federal Regulatory Update 2019 WTBA/WisDOT Contractor/Engineer Conference by Nick Goldstein ARTBA Vice President of Regulatory & Legal Issues January 17, 2019 How the Public Feels Regulations and Transportation

Kevin Thorpe Financial Economist & Principal Cassidy Turley

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

MAINTAINING MOMENTUM:

MAINTAINING MOMENTUM: 2018 National Economic Update September 12, 2018 noun mo men tum \ mō-ˈmen-təm, mə- \ 1 b : the strength or force that allows something to continue or to grow stronger or faster as

MAINTAINING MOMENTUM: 2018 National Economic Update September 12, 2018 noun mo men tum \ mō-ˈmen-təm, mə- \ 1 b : the strength or force that allows something to continue or to grow stronger or faster as

Naples, Marco Island, Everglades Convention and Visitors Bureau May 2018 Visitor Profile

RESEARCH DATA SERVICES, INC. 777 SOUTH HARBOUR ISLAND BOULEVARD SUITE 260 TAMPA, FLORIDA 33602 TEL (813) 254-2975 FAX (813) 223-2986 Naples, Marco Island, Everglades Convention and Visitors Bureau May

RESEARCH DATA SERVICES, INC. 777 SOUTH HARBOUR ISLAND BOULEVARD SUITE 260 TAMPA, FLORIDA 33602 TEL (813) 254-2975 FAX (813) 223-2986 Naples, Marco Island, Everglades Convention and Visitors Bureau May

Bikes Belong Survey: The Size & Impact of Road Riding Events

Bikes Belong Survey: The Size & Impact of Road Riding Events November 2009 Recreational road bicycling events are popular all across the United States. Participants are inspired by the opportunities to

Bikes Belong Survey: The Size & Impact of Road Riding Events November 2009 Recreational road bicycling events are popular all across the United States. Participants are inspired by the opportunities to

Habit Formation in Voting: Evidence from Rainy Elections Thomas Fujiwara, Kyle Meng, and Tom Vogl ONLINE APPENDIX

Habit Formation in Voting: Evidence from Rainy Elections Thomas Fujiwara, Kyle Meng, and Tom Vogl ONLINE APPENDIX Figure A1: Share of Counties with Election-Day Rainfall by Year Share of counties with

Habit Formation in Voting: Evidence from Rainy Elections Thomas Fujiwara, Kyle Meng, and Tom Vogl ONLINE APPENDIX Figure A1: Share of Counties with Election-Day Rainfall by Year Share of counties with

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Trends. September 10, 2013

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

SHOOTING IN AMERICA. An Economic Force for Conservation 2018 EDITION

TARGET SHOOTING IN AMERICA An Economic Force for Conservation 2018 EDITION INTRODUCTION Target shooting is enjoyed by millions of Americans each year. It is so popular, in fact: More people participate

TARGET SHOOTING IN AMERICA An Economic Force for Conservation 2018 EDITION INTRODUCTION Target shooting is enjoyed by millions of Americans each year. It is so popular, in fact: More people participate

The Burden of HPV Related Cancers in Kentucky

The Burden of HPV Related Cancers in Kentucky Presented on November 15, 2017 by Katie Bathje, Kentucky Cancer Consortium Many thanks to: Thomas C. Tucker, PhD, MPH Jaclyn Nee, DrPH 1 % coverage Adolescent

The Burden of HPV Related Cancers in Kentucky Presented on November 15, 2017 by Katie Bathje, Kentucky Cancer Consortium Many thanks to: Thomas C. Tucker, PhD, MPH Jaclyn Nee, DrPH 1 % coverage Adolescent

Produce Safety Alliance Course and Trainer Totals through September 19, 2018

Course and Trainer Totals through 19, 218 Totals: 216 218 Train-the-Trainer Courses Domestic 58 Total TTT Courses since Sept. 216 International 12 Total 7 2,27 Total Trainer Participants 1,716 (Domestic)

Course and Trainer Totals through 19, 218 Totals: 216 218 Train-the-Trainer Courses Domestic 58 Total TTT Courses since Sept. 216 International 12 Total 7 2,27 Total Trainer Participants 1,716 (Domestic)

Walgreens Pharmacy West Fairview Ave., Boise, ID o Hours: Open 24 hours

ADA Ada County Sheriffs Office 7200 Barrister Dr Boise, ID 83704-208-577-3000 o Bin in Evidence Room Lobby, Hours: 8-4/M-F Boise Police/City Hall West 333 North Mark Stall Pl Boise, ID 83704-208-570-6000

ADA Ada County Sheriffs Office 7200 Barrister Dr Boise, ID 83704-208-577-3000 o Bin in Evidence Room Lobby, Hours: 8-4/M-F Boise Police/City Hall West 333 North Mark Stall Pl Boise, ID 83704-208-570-6000

SECTION SEVEN. Characteristics of People with IDD and Staff in Large Public Residential Facilities

SECTION SEVEN Characteristics of People with IDD and Staff in Large Public Residential Facilities FY Section 7: Characteristics of People with IDD and Staff in Large State-Operated IDD Facilities This

SECTION SEVEN Characteristics of People with IDD and Staff in Large Public Residential Facilities FY Section 7: Characteristics of People with IDD and Staff in Large State-Operated IDD Facilities This

2012 Payne County Economic Outlook

2012 Payne County Economic Outlook by Dan Rickman Regents Professor of Economics and Oklahoma Gas and Electric Services Chair in Regional Economic Analysis http://economy.okstate.edu/ 20,000 U.S. Real

2012 Payne County Economic Outlook by Dan Rickman Regents Professor of Economics and Oklahoma Gas and Electric Services Chair in Regional Economic Analysis http://economy.okstate.edu/ 20,000 U.S. Real

Gay Gilbert, Administrator Unemployment Insurance USDOL/ETA June 22, 2016

Gay Gilbert, Administrator Unemployment Insurance USDOL/ETA June 22, 2016 Where is Our Program Today? Most Critical Challenges A Program in Transition Using our Valuable Resources What s Important for

Gay Gilbert, Administrator Unemployment Insurance USDOL/ETA June 22, 2016 Where is Our Program Today? Most Critical Challenges A Program in Transition Using our Valuable Resources What s Important for

The 2019 Economic Outlook Forum The Outlook for MS

The 2019 Economic Outlook Forum The Outlook for MS February 2019 Mississippi University Research Center Mississippi Institutions of Higher Learning Darrin Webb, State Economist dwebb@mississippi.edu (601)432-6556

The 2019 Economic Outlook Forum The Outlook for MS February 2019 Mississippi University Research Center Mississippi Institutions of Higher Learning Darrin Webb, State Economist dwebb@mississippi.edu (601)432-6556

Target Shooting by Hunters and Their Use of Shooting Ranges: 1975, 1991, and 2011

U.S. Fish & Wildlife Service Target Shooting by Hunters and Their Use of Shooting Ranges: 1975, 1991, and 2011 Addendum to the 2011 National Survey of Fishing, Hunting, and Wildlife-Associated Recreation

U.S. Fish & Wildlife Service Target Shooting by Hunters and Their Use of Shooting Ranges: 1975, 1991, and 2011 Addendum to the 2011 National Survey of Fishing, Hunting, and Wildlife-Associated Recreation

2018 KENTUCKY FACT BOOK

2018 KENTUCKY FACT BOOK A statistical guide to the Thoroughbred industry in Kentucky Prepared by The Jockey Club Preface This report has been compiled as an industry service by The Jockey Club with the

2018 KENTUCKY FACT BOOK A statistical guide to the Thoroughbred industry in Kentucky Prepared by The Jockey Club Preface This report has been compiled as an industry service by The Jockey Club with the

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

Wisconsin Concrete Pavement Association. Ed Sullivan, SVP & Chief Economist

Wisconsin Concrete Pavement Association Ed Sullivan, SVP & Chief Economist February 2018 I Pewaukee, Wisconsin Labor Markets Net Job Creation Monthly Gain 500 7.0% Unemployment Rate U3 Measurement 400

Wisconsin Concrete Pavement Association Ed Sullivan, SVP & Chief Economist February 2018 I Pewaukee, Wisconsin Labor Markets Net Job Creation Monthly Gain 500 7.0% Unemployment Rate U3 Measurement 400

Northwest Economic Research Center College of Urban and Public Affairs Forecast Breakfast Economic Outlook

Northwest Economic Research Center College of Urban and Public Affairs 2019 Forecast Breakfast Economic Outlook 1/10/2019 2 U.S. ECONOMY 1/10/2019 3 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Northwest Economic Research Center College of Urban and Public Affairs 2019 Forecast Breakfast Economic Outlook 1/10/2019 2 U.S. ECONOMY 1/10/2019 3 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Traffic Safety Facts. State Traffic Data Data. Overview

Traffic Safety Facts 2015 Data June 2017 DOT HS 812 412 State Traffic Data Key Findings Traffic fatalities increased by 7 percent from 2014 to 2015 (32,744 to 35,092) for the United States. The fatality

Traffic Safety Facts 2015 Data June 2017 DOT HS 812 412 State Traffic Data Key Findings Traffic fatalities increased by 7 percent from 2014 to 2015 (32,744 to 35,092) for the United States. The fatality

Economy On The Rebound

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

8:00 am 5:00 pm NASRO Basic Course Music Road Resort Hotel. 8:00 am 5:00 pm NASRO Basic Course - ** Music Road Resort Hotel

NASRO NATIONAL SCHOOL SAFETY CONFERENCE Smoky Mountains, TN June 23 28, 2019 This event has been approved for UASI reimbursement. Travel, Per Diem, Tuition reimbursement, Backfill and Overtime is at the

NASRO NATIONAL SCHOOL SAFETY CONFERENCE Smoky Mountains, TN June 23 28, 2019 This event has been approved for UASI reimbursement. Travel, Per Diem, Tuition reimbursement, Backfill and Overtime is at the

Babson Capital/UNC Charlotte Economic Forecast. May 13, 2014

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

Economic Overview. Melissa K. Peralta Senior Economist April 27, 2017

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

2019 Economic Outlook: Will the Recovery Ever End?

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

National and Regional Economic Outlook. Central Southern CAA Conference

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

Population of Puerto Rico (Millions of people)

") Dr. Mario Marazzi-Santiago Instituto de Estadísticas Executive Director August 15, 2015 Population of Puerto Rico (Millions of people) 4.5 4 3.5 3 2.5 2 1.5 1 0.5 1950 1955 1960 1965 1970 1975 1980 1985

Dr. Mario Marazzi-Santiago Instituto de Estadísticas Executive Director August 15, 2015 Population of Puerto Rico (Millions of people) 4.5 4 3.5 3 2.5 2 1.5 1 0.5 1950 1955 1960 1965 1970 1975 1980 1985

Featured Fish-Week ofjuly 16th

Featured Fish-Week ofjuly 16th 5-6 Premium GradeKoi 25% O f,only$8.21each! 5-6 GinRinMixKoi 15% O f,only$10.41each! 6-8 StandardGradeButerflyKoi Buy1FulCount,Get1FulCount50% O f! 3-4 Yelow CometGoldfish

Featured Fish-Week ofjuly 16th 5-6 Premium GradeKoi 25% O f,only$8.21each! 5-6 GinRinMixKoi 15% O f,only$10.41each! 6-8 StandardGradeButerflyKoi Buy1FulCount,Get1FulCount50% O f! 3-4 Yelow CometGoldfish

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee The U.S. economy has now enjoyed 7 years of economic growth since the Great Recession Real GDP grew by 1.2% in

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee The U.S. economy has now enjoyed 7 years of economic growth since the Great Recession Real GDP grew by 1.2% in

Potential Solutions for Mercury Control in the Cement Industry Portland Cement Association Meeting

Potential Solutions for Mercury Control in the Cement Industry Portland Cement Association Meeting August 24, 2009 Agenda Albemarle Sorbent Technologies Quick Overview Mercury Sorbents Control Options

Potential Solutions for Mercury Control in the Cement Industry Portland Cement Association Meeting August 24, 2009 Agenda Albemarle Sorbent Technologies Quick Overview Mercury Sorbents Control Options

Warm Mix Asphalt in the United States: From Evolution to Revolution

Warm Mix Asphalt in the United States: From Evolution to Revolution Matthew Corrigan, P.E. Asphalt Pavement Engineer Mobile Asphalt Testing Trailer Technical Manager U.S. DOT Federal Highway Administration

Warm Mix Asphalt in the United States: From Evolution to Revolution Matthew Corrigan, P.E. Asphalt Pavement Engineer Mobile Asphalt Testing Trailer Technical Manager U.S. DOT Federal Highway Administration

Chapter 2: Visual Description of Data

Chapter 2: Visual Description of Data El Mechry El Koudous Fordham University January 24, 2018 Meshry (Fordham University) Chapter 2 January 24, 2018 1 / 35 Introduction In this chapter we will cover:

Chapter 2: Visual Description of Data El Mechry El Koudous Fordham University January 24, 2018 Meshry (Fordham University) Chapter 2 January 24, 2018 1 / 35 Introduction In this chapter we will cover:

From Recession to Recovery

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks. Business Research Division Leeds School of Business

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks Presented by the Business Research Division Leeds School of Business University of Colorado at Boulder U.S. Economic

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks Presented by the Business Research Division Leeds School of Business University of Colorado at Boulder U.S. Economic

FARS Acc_Aux Analytical Users Manual. The Tables in this Manual Contain Fatal Crash Counts

FARS Acc_Aux Analytical Users Manual The Tables in this Manual Contain Fatal Crash Counts FARS Acc_Aux File s 2005-2014 ANCHOR Table of Contents 1 A_CRAINJ A_CT A_D15_19 A_D15_20 A_D16_19 A_D16_20 A_D16_24

FARS Acc_Aux Analytical Users Manual The Tables in this Manual Contain Fatal Crash Counts FARS Acc_Aux File s 2005-2014 ANCHOR Table of Contents 1 A_CRAINJ A_CT A_D15_19 A_D15_20 A_D16_19 A_D16_20 A_D16_24

2014 Economic Indicators, Trends & Observations. 51 South Main Street Janesville, WI P F RockCountyAlliance.

2014 Economic Indicators, Trends & Observations 51 South Main Street Janesville, WI 53545 P.608.757.5598 F.608.757.5586 RockCountyAlliance.com Indicators, Trends & Observations National Level State of

2014 Economic Indicators, Trends & Observations 51 South Main Street Janesville, WI 53545 P.608.757.5598 F.608.757.5586 RockCountyAlliance.com Indicators, Trends & Observations National Level State of

Big Changes, Unknown Impacts

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

The Global Economy: Sustaining Momentum

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

Policy Choices for a Genuine Vermont Economy

Policy Choices for a Genuine Vermont Economy Jon D. Erickson, Zach Zimmerman, Eric Zencey Gund Institute for Ecological Economics University of Vermont www.uvm.edu/giee Vermont Act 113 An act relating

Policy Choices for a Genuine Vermont Economy Jon D. Erickson, Zach Zimmerman, Eric Zencey Gund Institute for Ecological Economics University of Vermont www.uvm.edu/giee Vermont Act 113 An act relating

2016 River Use Statistics -by Steve Sullivan

Grand Canyon River Office 2016 River Use Statistics -by Steve Sullivan Topics River Use Statistics Overview Commercial River Use Statistics Noncommercial River Use Statistics Noncommercial River Lottery

Grand Canyon River Office 2016 River Use Statistics -by Steve Sullivan Topics River Use Statistics Overview Commercial River Use Statistics Noncommercial River Use Statistics Noncommercial River Lottery

How Much Wind Is in the Sails?

How Much Wind Is in the Sails? Erie Chamber of Commerce Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations September 20, 2017 Real GDP Growth

How Much Wind Is in the Sails? Erie Chamber of Commerce Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations September 20, 2017 Real GDP Growth

Your Texas Economy. Current through: Tuesday, Nov 20, 2018

Your Texas Economy Current through: Tuesday, Nov 20, 2018 Overview of Texas Economy The Texas economy is growing robustly in 2018 2018 job growth through October is 2.9 percent annualized compared to 2.1

Your Texas Economy Current through: Tuesday, Nov 20, 2018 Overview of Texas Economy The Texas economy is growing robustly in 2018 2018 job growth through October is 2.9 percent annualized compared to 2.1

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

FARS Acc_Aux Analytical Users Manual

FARS Acc_Aux Analytical Users Manual The s Included in the 'ACC_AUX' database are produced from definitions defined in the 'NCSA - Analytical Data Classification Manual' The Tables in this Manual Contain

FARS Acc_Aux Analytical Users Manual The s Included in the 'ACC_AUX' database are produced from definitions defined in the 'NCSA - Analytical Data Classification Manual' The Tables in this Manual Contain

Annual Data Report

Annual Data Report 2014-2015 A Report of the Association of American Veterinary Medical Colleges 1101 Vermont Avenue, NW 20005 202-371-9195 http://www.aavmc.org As of March 11, 2015 Introduction The membership

Annual Data Report 2014-2015 A Report of the Association of American Veterinary Medical Colleges 1101 Vermont Avenue, NW 20005 202-371-9195 http://www.aavmc.org As of March 11, 2015 Introduction The membership

Southern California Economic Forecast & Industry Outlook

2016-17 Southern California Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Sr. VP/Chief Economist, LAEDC February 17, 2016 Outline U.S. Economy California Economy Southern California Economy

2016-17 Southern California Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Sr. VP/Chief Economist, LAEDC February 17, 2016 Outline U.S. Economy California Economy Southern California Economy

Utility Monitoring Central Archive

Utility Monitoring Central Archive Note that the UMC Archive files mainly cover defunct stations. Some stations may however still be active and some of the info may still be valid. FEMA - FEDERAL EMERGENCY

Utility Monitoring Central Archive Note that the UMC Archive files mainly cover defunct stations. Some stations may however still be active and some of the info may still be valid. FEMA - FEDERAL EMERGENCY

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Economic Recovery Has Stalled, Recession in the Cards by Year End

Economic Indicators to Watch for Signs of Recovery Economic Recovery Has Stalled, Recession in the Cards by Year End New York, NY Monday, June 27, 2011 Richard Yamarone Author of The Trader s Guide to

Economic Indicators to Watch for Signs of Recovery Economic Recovery Has Stalled, Recession in the Cards by Year End New York, NY Monday, June 27, 2011 Richard Yamarone Author of The Trader s Guide to

Muhlenkamp & Company. Webinar December 1, Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Charting a Path to Lift Off? Understanding the Shifting Economic Winds

Charting a Path to Lift Off? Understanding the Shifting Economic Winds Thomas F. Siems, Ph.D. Assistant Vice President and Senior Economist Federal Reserve Bank of Dallas Government Finance Officers Arlington,

Charting a Path to Lift Off? Understanding the Shifting Economic Winds Thomas F. Siems, Ph.D. Assistant Vice President and Senior Economist Federal Reserve Bank of Dallas Government Finance Officers Arlington,

WORKFORCE LOCAL AREA EMPLOYMENT STATISTICS (LAUS)

") AUGUST 2018 WORKFORCE LOCAL AREA EMPLOYMENT STATISTICS (LAUS) 1,200,000 1,100,000 1,000,000 900,000 Labor Force Employment 1,152,626 1,116,938 800,000 700,000 600,000 500,000 2016 to 2017: 35957 (3.1%)

AUGUST 2018 WORKFORCE LOCAL AREA EMPLOYMENT STATISTICS (LAUS) 1,200,000 1,100,000 1,000,000 900,000 Labor Force Employment 1,152,626 1,116,938 800,000 700,000 600,000 500,000 2016 to 2017: 35957 (3.1%)

NATIONAL UNEMPLOYMENT INSURANCE PROGRAM UPDATE GAY GILBERT, ADMINISTRATOR UNEMPLOYMENT INSURANCE USDOL/ETA JUNE 27, 2018

NATIONAL UNEMPLOYMENT INSURANCE PROGRAM UPDATE GAY GILBERT, ADMINISTRATOR UNEMPLOYMENT INSURANCE USDOL/ETA JUNE 27, 2018 UI NATIONAL UPDATE v Program Highlights v Quick Look at the Data v Strategic Investments/Initiative

NATIONAL UNEMPLOYMENT INSURANCE PROGRAM UPDATE GAY GILBERT, ADMINISTRATOR UNEMPLOYMENT INSURANCE USDOL/ETA JUNE 27, 2018 UI NATIONAL UPDATE v Program Highlights v Quick Look at the Data v Strategic Investments/Initiative

Transitions: 2019 Economic Forecast for Metro Denver February 6, 2019

Transitions: 2019 Economic Forecast for Metro Denver February 6, 2019 Prepared by: Can Stock Photo / jkirsh In Partnership with: Consumer Changes and Influences Slowing population growth Aging of the population

Transitions: 2019 Economic Forecast for Metro Denver February 6, 2019 Prepared by: Can Stock Photo / jkirsh In Partnership with: Consumer Changes and Influences Slowing population growth Aging of the population

2018 ILLINOIS FACT BOOK

2018 ILLINOIS FACT BOOK A statistical guide to the Thoroughbred industry in Illinois Prepared by The Jockey Club Preface This report has been compiled as an industry service by The Jockey Club with the

2018 ILLINOIS FACT BOOK A statistical guide to the Thoroughbred industry in Illinois Prepared by The Jockey Club Preface This report has been compiled as an industry service by The Jockey Club with the