Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes. Tom Rogers. Lead Economist, Oxford Economics.

|

|

|

- Jody Holmes

- 5 years ago

- Views:

Transcription

1 Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics 16 th January 2013

2 Overview External environment showing signs of stabilisation if not quite yet recovery. So 2013 will be another tough year for UK exporters. Firms will hold back on investment, despite ever-growing cash piles. Jobs growth likely to slow, but with some pickup in wage growth supporting consumer demand. Risks to inflation to upside in short term and downside in medium term. MPC s policy measures look like supporting housing market in UK regional divide in economic prospects but not entirely a North-South story. Other factors matter too.

3 US households in good financial shape US : Household debt measures % of disposable income Household financial obligations Household debt service ratio Source: FRB 3

4 and banks lending to business 4 US & Eurozone: Corporate loan growth % year Eurozone loans to PNFCs Source : Oxford Economics/Haver Analytics US commercial & industrial loans US loans inc. commercial real estate

5 Imminent risk of breakup reduced Weighted average peripheral bond spread % spread over German bunds Jul Dec Jun Dec Jun Dec-12 Source : Oxford Economics/ Haver Analytics

6 but more austerity to go Discretionary fiscal tightening, Percent of GDP Germany Italy France Belgium Spain Ireland Greece Source : Oxford Economics/Haver Analytics

7 unemployment will restrain consumption Eurozone: Unemployment Rate % 30 Greece Spain Portugal 10 Eurozone Source : Oxford Economics/Haver Analytics

8 some way to go to restore competitiveness Unit labour costs 2000= Greece Forecast 140 Italy France Spain Germany Source: Oxford Economics

9 and banks will struggle with bad debt for some time Eurozone Non-performing bank loans % total loans Spain Forecast 12 Italy Eurozone Source : Oxford Economics/World Bank

10 So a lost decade likely in medium-term Eurozone GDP growth % year average 2.5 Forecast Source : Oxford Economics/Haver Analytics

11 Oxford Economics baseline forecast Av US Japan Eurozone of which: World GDP Growth % Change on Previous Year Germany France Italy UK China India Other Asia Mexico Brazil Other Latin America Eastern Europe MENA World World (PPP)

12 UK outlook - summary Spare capacity within firms will limit job creation in 2013 Firms still loathe to invest, despite ever-growing cash piles Inflation above target in 2013, below target in medium term MPC has sparked signs of life the mortgage market But house prices unlikely to take off in 2013 Southern regions fare best, with some interesting localised differences

13 Flat GDP and strong employment growth UK: Labour market Employment (000s) Unemployment (RHS) Employment (LHS) Unemployment (000s) Source : Haver Analytics

14 leaves us with spare capacity within firms UK: Output per worker 2009= Pre-recession trend % Actual Source : Haver Analytics

15 so limited scope for further job creation UK: Unemployment % 9 Forecast ILO Claimant count Source: Oxford Economics

16 Implies only a gradual recovery in consumer spending UK real consumer spending % change on year ago 4% 3% 2% 1% 0% % -2% -3% Forecast -4% Source : Oxford Economics/Haver Analytics

17 Firms still reluctant to invest UK:BoE agents' survey: Investment intentions % balance 4 Services Manufacturing Source : Haver Analytics

18 despite having plenty of cash UK: PNFC financial balance % of GDP, 4QMA Source : Haver Analytics

19 Inflation below target in medium term UK: Inflation relative to target % year 5 Forecast % target 1 CPI inflation Source: Oxford Economics

20 Lending for Business should kick start mortgage lending UK: Mortgage availability % balance : loosening (+) / tightening (-) *The single datapoints represent 3 month forecasts, while the columns represent actual data Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q Source : Bank of England Credit Conditions Survey

21 but further modest house price falls likely UK: House prices & transactions Prices (% year) Transactions (RHS) Prices (LHS) Transactions (000s) 500 F'cast Source : Oxford Economics

22 UK forecast Forecast for UK (Annual percentage changes unless specified) Domestic Demand Private Consumption Fixed Investment Stockbuilding (% of GDP) Government Consumption Exports of Goods and Services Imports of Goods and Services GDP Industrial Production CPI Current Balance (% of GDP) Government Budget (% of GDP) Short-Term Interest Rates (%) Long-Term Interest Rates (%) Exchange Rate (US$ per ) Exchange Rate (Euro per )

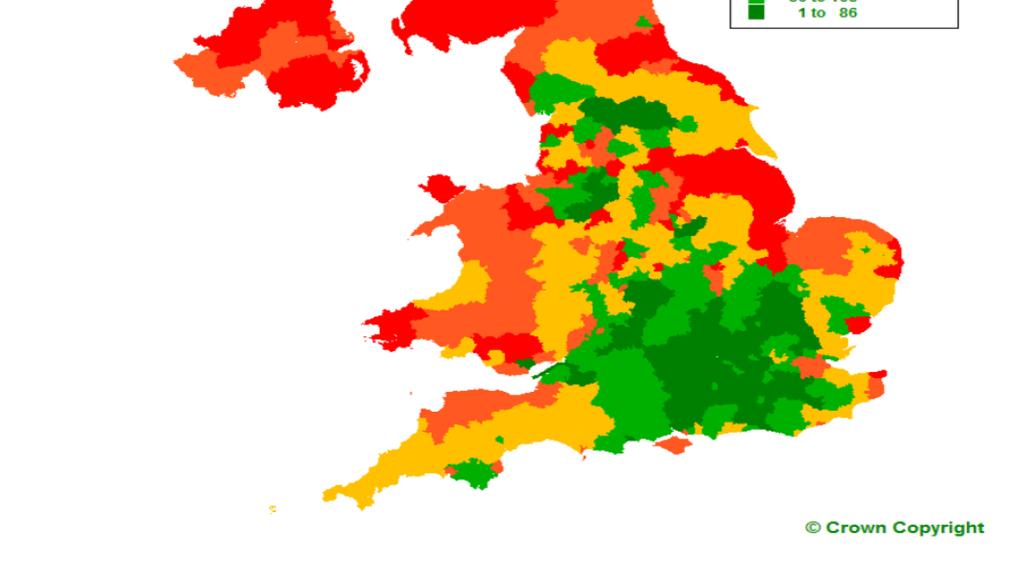

23 Regional prospects divided Unemployment rates around UK regions, 2013 Percent of labour force SE SW EE L EM S W NW WM YH NE N Source : Oxford Economics/Haver Analytics

24 Regional prospects divided Average GVA growth Percent on year ago 2.8% 2.6% 2.4% 2.2% 2.0% 1.8% 1.6% 1.4% L SE SW EE WM EM YH NW NI S W NE Source : Oxford Economics/Haver Analytics

25 But not entirely a North-South story

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip?

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

The World Did Not End in Q1

The World Did Not End in Q1 Sam Wilkin Senior Advisor, Business Research Blog: www.samwilkin.com 06.2015 1 2 3 4 5 Exports to Russia: 10% of Finnish exports; 4% of Finnish GDP 1. Global Economic Weather

The World Did Not End in Q1 Sam Wilkin Senior Advisor, Business Research Blog: www.samwilkin.com 06.2015 1 2 3 4 5 Exports to Russia: 10% of Finnish exports; 4% of Finnish GDP 1. Global Economic Weather

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

The Global Economy: Sustaining Momentum

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

RBC Economics Financial Update Dawn Desjardins

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

Economic & Financial Market Outlook

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

Outline. Overview of globalization. Global outlook for real economic activity & inflation. Risks to the outlook

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

From Recession to Recovery

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

Reading the Tea Leaves: Investing for 2010 and Beyond

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

Impacts of the Global Economy on Asia Pacific Travel. 29 June 2007 John Walker

Impacts of the Global Economy on Asia Pacific Travel 29 June 2007 John Walker jwalker@oxfordeconomics.com Oxford Economics Founded in 1981 Over 300 clients including blue chip companies and government

Impacts of the Global Economy on Asia Pacific Travel 29 June 2007 John Walker jwalker@oxfordeconomics.com Oxford Economics Founded in 1981 Over 300 clients including blue chip companies and government

Grasshoppers, Ants and Locusts: the future of the world economy

Ralph Miliband Series on the Restructuring of World Power Grasshoppers, Ants and Locusts: the future of the world economy Martin Wolf Associate editor and chief economics commentator, Financial Times Professor

Ralph Miliband Series on the Restructuring of World Power Grasshoppers, Ants and Locusts: the future of the world economy Martin Wolf Associate editor and chief economics commentator, Financial Times Professor

Seven Lean Years Explaining Persistent Global Economic Weakness

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Vermont Economic Conference:

Vermont Economic Conference: Mapping Our Economic Future Michael Dolega Director & Senior Economist TD Economics January 5 2018 Summary Global economy gathering speed, leading to another upgrade in outlook.

Vermont Economic Conference: Mapping Our Economic Future Michael Dolega Director & Senior Economist TD Economics January 5 2018 Summary Global economy gathering speed, leading to another upgrade in outlook.

Global Economic Outlook

Global Economic Outlook Mark A. Wynne Vice President & Associate Director of Research Director, Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas Presentation to Vistas Conference

Global Economic Outlook Mark A. Wynne Vice President & Associate Director of Research Director, Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas Presentation to Vistas Conference

Global economy maintaining solid growth momentum. Canada leading the pack

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

U.S. Economy in a Snapshot

U.S. Economy in a Snapshot Economic Press Briefing: May 19, 2016 The views expressed here are those of the presenter and do not necessarily represent the views of the Federal Reserve Bank of New York or

U.S. Economy in a Snapshot Economic Press Briefing: May 19, 2016 The views expressed here are those of the presenter and do not necessarily represent the views of the Federal Reserve Bank of New York or

U.S. AUTO INDUSTRY UPDATE Federal Reserve Bank of Chicago Automotive Outlook Symposium. Emily Kolinski Morris Chief Economist May 2015

U.S. AUTO INDUSTRY UPDATE Federal Reserve Bank of Chicago Automotive Outlook Symposium Emily Kolinski Morris Chief Economist May 2015 NORTH AMERICA INDUSTRY VOLUME SUMMARY 13.1 Total North America* (Mils.)

U.S. AUTO INDUSTRY UPDATE Federal Reserve Bank of Chicago Automotive Outlook Symposium Emily Kolinski Morris Chief Economist May 2015 NORTH AMERICA INDUSTRY VOLUME SUMMARY 13.1 Total North America* (Mils.)

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States?

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

URBAN LAND INSTITUTE

URBAN LAND INSTITUTE 2012 ULI FALL MEETING (Denver, 18 October 2012) The Global Economic Outlook Dark clouds on the horizon Andrea Boltho Magdalen College University of Oxford Oxford Economics and REAG

URBAN LAND INSTITUTE 2012 ULI FALL MEETING (Denver, 18 October 2012) The Global Economic Outlook Dark clouds on the horizon Andrea Boltho Magdalen College University of Oxford Oxford Economics and REAG

It Was Never Going To Be Easy

It Was Never Going To Be Easy Stephen Toplis, Head of Research July 2010 Introduction Global power shift sustained Average outlook on the improve Fiscal constraints binding Domestic rebalance under way

It Was Never Going To Be Easy Stephen Toplis, Head of Research July 2010 Introduction Global power shift sustained Average outlook on the improve Fiscal constraints binding Domestic rebalance under way

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Market Insights. June 30, 2018

June 30, 2018 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.7% 1.2% 1.3% 2.1% 2.3% 1.7% 2.3%

June 30, 2018 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.7% 1.2% 1.3% 2.1% 2.3% 1.7% 2.3%

Market Insights. March 29, 2019

March 29, 2019 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.2% 1.4% 2.1% 2.3% 1.7% 2.4% 2.3%

March 29, 2019 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.2% 1.4% 2.1% 2.3% 1.7% 2.4% 2.3%

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

Global growth forecasts Key countries/regions,

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition May 7 and 8, 2013 İstanbul, Turkey Outline 1 The Financial System 2 Weak Growth 3 4 5 Unprecedented

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition May 7 and 8, 2013 İstanbul, Turkey Outline 1 The Financial System 2 Weak Growth 3 4 5 Unprecedented

Global Economic Outlook. Kellie Maske, Sr. Economics Fellow FedEx Corporate Economics September 2011

Kellie Maske, Sr. Economics Fellow FedEx Corporate Economics U.S. Outlook: Moderate Growth Overall 6 4 US Real GDP Growth 2 % Change 0 (2) (4) Forecast (6) (8) Bars = QOQ% Annualized Line = YOY% (10) 2005

Kellie Maske, Sr. Economics Fellow FedEx Corporate Economics U.S. Outlook: Moderate Growth Overall 6 4 US Real GDP Growth 2 % Change 0 (2) (4) Forecast (6) (8) Bars = QOQ% Annualized Line = YOY% (10) 2005

The Baltic economies: Current situation and future trends, possibilities and pitfalls

The Baltic economies: Current situation and future trends, possibilities and pitfalls Riga, 15 October 2015 Morten Hansen Head of Economics Department, Stockholm School of Economics in Riga Member of the

The Baltic economies: Current situation and future trends, possibilities and pitfalls Riga, 15 October 2015 Morten Hansen Head of Economics Department, Stockholm School of Economics in Riga Member of the

Federal Reserve Bank of Dallas, FIRM (Financial Institution Relationship Management)

") The Economic Roller Coaster: Where Have We Been? And Where Are We Going? Thomas F. Siems, Ph.D. Senior Economist and Director of Economic Outreach Federal Reserve Bank of Dallas Economic Summit Dallas

The Economic Roller Coaster: Where Have We Been? And Where Are We Going? Thomas F. Siems, Ph.D. Senior Economist and Director of Economic Outreach Federal Reserve Bank of Dallas Economic Summit Dallas

More of the Same; Or now for Something Completely Different?

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

Future Global Trade Trends - Risks & Opportunities. Pulse of the Ports: Peak Season Forecast March 21, 2013

1 Future Global Trade Trends - Risks & Opportunities Pulse of the Ports: Peak Season Forecast March 21, 2013 June 2012 Dr. Walter Kemmsies Chief Economist Summary Higher economic growth in 2013, possible

1 Future Global Trade Trends - Risks & Opportunities Pulse of the Ports: Peak Season Forecast March 21, 2013 June 2012 Dr. Walter Kemmsies Chief Economist Summary Higher economic growth in 2013, possible

GLOBAL ECONOMICS, REAL ESTATE PRICING & OUTLOOK FOR 2017 RICHARD BARKHAM GLOBAL CHIEF ECONOMIST

GLOBAL ECONOMICS, REAL ESTATE PRICING & OUTLOOK FOR 2017 RICHARD BARKHAM GLOBAL CHIEF ECONOMIST BREXIT TRUMPISM EURO-TRUMPISM 4 ECONOMICS, PRICING & OUTLOOK FOR 2017 LET S GET GEOPOLITICS IN PERSPECTIVE

GLOBAL ECONOMICS, REAL ESTATE PRICING & OUTLOOK FOR 2017 RICHARD BARKHAM GLOBAL CHIEF ECONOMIST BREXIT TRUMPISM EURO-TRUMPISM 4 ECONOMICS, PRICING & OUTLOOK FOR 2017 LET S GET GEOPOLITICS IN PERSPECTIVE

Economic Outlook: fear over fundamentals

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

Global economy s strong momentum intact despite elevated level of uncertainty. Canada headed for another year of solid growth

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

Economic Overview. Melissa K. Peralta Senior Economist April 27, 2017

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

sector: recent developments VÍTOR CONSTÂNCIO

The economy and the banking sector: recent developments VÍTOR CONSTÂNCIO January 2006 Recent performance of the economy and prospects Factors behind the period of slow growth Challenges to the Banking

The economy and the banking sector: recent developments VÍTOR CONSTÂNCIO January 2006 Recent performance of the economy and prospects Factors behind the period of slow growth Challenges to the Banking

The U.S. Economic Outlook

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

SA economic review Kevin Lings. August 2018

SA economic review Kevin Lings August 2018 South Africa real GDP growth year-on-year %y/y 8 7 6 5 Ave 4.3% 4 Ave 2.5% 3 2 Ave 0.9% 1 0-1 -2-3 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 2

SA economic review Kevin Lings August 2018 South Africa real GDP growth year-on-year %y/y 8 7 6 5 Ave 4.3% 4 Ave 2.5% 3 2 Ave 0.9% 1 0-1 -2-3 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 2

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD?

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD? FROM BUST TO BOOM. AN EPIC BUST After 16 years of growth with a short pause for breath in 2002, the Icelandic economy entered

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD? FROM BUST TO BOOM. AN EPIC BUST After 16 years of growth with a short pause for breath in 2002, the Icelandic economy entered

After the British referendum

Future of Europe After the British referendum Broader issues for the UK and the EU David Marsh, Managing Director, OMFIF 27 October 2016 Nicosia 1 European politics moves against integration A new phase

Future of Europe After the British referendum Broader issues for the UK and the EU David Marsh, Managing Director, OMFIF 27 October 2016 Nicosia 1 European politics moves against integration A new phase

France : Economic developments and reforms, where are we heading?

France : Economic developments and reforms, where are we heading? The Economic Club of New York : 18 April 2018 François VILLEROY de GALHAU, Governor of the Banque de France 1 WHERE ARE WE STARTING FROM?

France : Economic developments and reforms, where are we heading? The Economic Club of New York : 18 April 2018 François VILLEROY de GALHAU, Governor of the Banque de France 1 WHERE ARE WE STARTING FROM?

Paul Bingham Managing Director, Global Trade and Transportation February 18, 2009

Economic Outlook and Ports Paul Bingham Managing Director, Global Trade and Transportation February 18, 2009 The Outlook for Trade Depends on Goods Demand Integrated international supply-chains offer efficiencies

Economic Outlook and Ports Paul Bingham Managing Director, Global Trade and Transportation February 18, 2009 The Outlook for Trade Depends on Goods Demand Integrated international supply-chains offer efficiencies

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Trends. September 10, 2013

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

The Shifts and the Shocks Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

The Shifts and the Shocks Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times Peterson Institute for International Economics 9 th October 2014 Washington DC The Shifts and the

The Shifts and the Shocks Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times Peterson Institute for International Economics 9 th October 2014 Washington DC The Shifts and the

The structure of the euro area recovery

The structure of the euro area recovery Rolf Strauch, Chief Economist JPMorgan Investor Seminar, IMF Annual Meetings Washington, October 2017 The euro area: a systemic player in global trade Trade openness

The structure of the euro area recovery Rolf Strauch, Chief Economist JPMorgan Investor Seminar, IMF Annual Meetings Washington, October 2017 The euro area: a systemic player in global trade Trade openness

ABA Commercial Real Estate Lending Committee

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

The Auction Market In 2015 & 2016 Review & Forecast. Dr. Ira Silver NAAA Economist

The Auction Market In 2015 & 2016 Review & Forecast Dr. Ira Silver NAAA Economist silver@naaa.com Agenda Economic conditions Economic outlook Light vehicle sales Light vehicle sales outlook NAAA 2015 Annual

The Auction Market In 2015 & 2016 Review & Forecast Dr. Ira Silver NAAA Economist silver@naaa.com Agenda Economic conditions Economic outlook Light vehicle sales Light vehicle sales outlook NAAA 2015 Annual

Economic Outlook for Canada: Economy Confronting Capacity Limits

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

The U.S. Economic Outlook

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

RISI EUROPEAN CONFERENCE. (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last?

The European Economy Things look good just now. Can this last?") RISI EUROPEAN CONFERENCE (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last? Andrea Boltho Magdalen College University of Oxford and Oxford Economics CONCLUSIONS OF

RISI EUROPEAN CONFERENCE (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last? Andrea Boltho Magdalen College University of Oxford and Oxford Economics CONCLUSIONS OF

10 County Conference. Richard Wobbekind. Executive Director Business Research Division & Senior Associate Dean Leeds School of Business

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

The U.S. & World Economy: The Good, the Bad, and the Ugly

The U.S. & World Economy: The Good, the Bad, and the Ugly Michael Strauss Chief Economist and Chief Investment Strategist Commonfund October 16, 2012 The U.S. & World Economy: The Good, the Bad, and the

The U.S. & World Economy: The Good, the Bad, and the Ugly Michael Strauss Chief Economist and Chief Investment Strategist Commonfund October 16, 2012 The U.S. & World Economy: The Good, the Bad, and the

Maximizing Tourism Marketing Investments A Canadian Perspective

Maximizing Tourism Marketing Investments A Canadian Perspective Understanding the potential of markets Economics: GDP; Inflation; Unemployment; Employment; Disposable Income; Private Consumption; Consumer

Maximizing Tourism Marketing Investments A Canadian Perspective Understanding the potential of markets Economics: GDP; Inflation; Unemployment; Employment; Disposable Income; Private Consumption; Consumer

Canadian Housing In Flux

Dr. Sherry Cooper Chief Economist Dominion Lending Centres The Title of the presentation Second line if needed Third line if needed Canadian Housing In Flux Today s date Location of presentation March

Dr. Sherry Cooper Chief Economist Dominion Lending Centres The Title of the presentation Second line if needed Third line if needed Canadian Housing In Flux Today s date Location of presentation March

National and Regional Economic Outlook. Central Southern CAA Conference

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

The outlook: what we know, the known unknowns and the unknown unknowns

The outlook: what we know, the known unknowns and the unknown unknowns 24 April 2017 Seoul Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1

The outlook: what we know, the known unknowns and the unknown unknowns 24 April 2017 Seoul Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

Airlines, the economy and air transport demand

Airlines, the economy and air transport demand Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 Returns for airlines investors lower this year;

Airlines, the economy and air transport demand Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 Returns for airlines investors lower this year;

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis. May 8 th, Presented by:

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis May 8 th, 2008 Presented by: Patricia Croft, Vice President & Chief Economist Phillips, Hager & North Investment Management Limited

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis May 8 th, 2008 Presented by: Patricia Croft, Vice President & Chief Economist Phillips, Hager & North Investment Management Limited

Emerging from the euro debt crisis Making the single currency work

Emerging from the euro debt crisis Making the single currency work Dr. Michael Heise, Allianz SE American Institute for Contemporary German Studies Johns Hopkins University Washington D.C., August 20,

Emerging from the euro debt crisis Making the single currency work Dr. Michael Heise, Allianz SE American Institute for Contemporary German Studies Johns Hopkins University Washington D.C., August 20,

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Trade Growth - Fundamental Driver of Port Operations and Development Strategies

Trade Growth - Fundamental Driver of Port Operations and Development Strategies Marine Terminal Management Training Program October 15, 2007 Long Beach, CA Paul Bingham Global Insight, Inc. 1 Agenda Economic

Trade Growth - Fundamental Driver of Port Operations and Development Strategies Marine Terminal Management Training Program October 15, 2007 Long Beach, CA Paul Bingham Global Insight, Inc. 1 Agenda Economic

Dr. Greg Hallman Director, Real Estate Finance and Investment Center (REFIC) McCombs School of Business University of Texas at Austin

McCombs School of Business University of Texas at Austin") Dr. Greg Hallman Director, Real Estate Finance and Investment Center (REFIC) McCombs School of Business University of Texas at Austin POWERPOINT PARTNER The US Economy today, with a close look at jobs

Dr. Greg Hallman Director, Real Estate Finance and Investment Center (REFIC) McCombs School of Business University of Texas at Austin POWERPOINT PARTNER The US Economy today, with a close look at jobs

Composition of Federal Spending

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

Chief Economist s Report

Chief Economist s Report 22 February 2017 IATA Legal Symposium, Washington Brian Pearce Chief Economist, IATA Airline Industry Economics Advisory Workshop 2016 1 Themes 1. World economy still stuck on

Chief Economist s Report 22 February 2017 IATA Legal Symposium, Washington Brian Pearce Chief Economist, IATA Airline Industry Economics Advisory Workshop 2016 1 Themes 1. World economy still stuck on

Southern California Economic Forecast & Industry Outlook

2016-17 Southern California Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Sr. VP/Chief Economist, LAEDC February 17, 2016 Outline U.S. Economy California Economy Southern California Economy

2016-17 Southern California Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Sr. VP/Chief Economist, LAEDC February 17, 2016 Outline U.S. Economy California Economy Southern California Economy

Big Changes, Unknown Impacts

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Panel on Post-Crisis Growth Performance Determinants, Effects and Policy Implications

Panel on Post-Crisis Growth Performance Determinants, Effects and Policy Implications Carmen M. Harvard University Bank of Canada and European Central Bank Conference Ottawa, June 8-9, 2015 1 Outline (i)

Panel on Post-Crisis Growth Performance Determinants, Effects and Policy Implications Carmen M. Harvard University Bank of Canada and European Central Bank Conference Ottawa, June 8-9, 2015 1 Outline (i)

Better in than out? Economic performance inside and outside the European monetary union. Roma, Rapporto Europa 2015

Better in than out? Economic performance inside and outside the European monetary union Rapporto Europa 2015 Roma, 9.7.2015 1 Table of Content I. The political threat Why European monetary union? II. Europe

Better in than out? Economic performance inside and outside the European monetary union Rapporto Europa 2015 Roma, 9.7.2015 1 Table of Content I. The political threat Why European monetary union? II. Europe

Hopes and Worries in an Election Year. Gregory Daco Principal US Economist April 2012

Economic Outlook: Hopes and Worries in an Election Year Gregory Daco Principal US Economist April 2012 Global Perspective: Bright Spots in Clouds of Uncertainty Global Economy US growth: on a better track

Economic Outlook: Hopes and Worries in an Election Year Gregory Daco Principal US Economist April 2012 Global Perspective: Bright Spots in Clouds of Uncertainty Global Economy US growth: on a better track

Prowess Investment Managers

gathering clouds: South Africa's economic situation and how it affects you Kelebogile Moloko Prowess Investment Managers what to expect ~ how to identify a recession ~ what are the implications for South

gathering clouds: South Africa's economic situation and how it affects you Kelebogile Moloko Prowess Investment Managers what to expect ~ how to identify a recession ~ what are the implications for South

Why Is the Recovery from the Financial Crisis So Sluggish?

Why Is the Recovery from the Financial Crisis So Sluggish? Robert E. Hall Hoover Institution and Department of Economics Stanford University Keynote Address Agricultural and Applied Economics Association

Why Is the Recovery from the Financial Crisis So Sluggish? Robert E. Hall Hoover Institution and Department of Economics Stanford University Keynote Address Agricultural and Applied Economics Association

Economic development the challenge of the new normal

Economic development the challenge of the new normal Neil Gibson, Director of Regional Services 24th November 2010 Overview The new normal globally The new normal in Northern Ireland Inequalities and imbalances

Economic development the challenge of the new normal Neil Gibson, Director of Regional Services 24th November 2010 Overview The new normal globally The new normal in Northern Ireland Inequalities and imbalances

Trade and Economic Trends

Trade and Economic Trends Marine Terminal Management Training Program Paul Bingham Managing Director, Global Commerce & Transportation IHS Global Insight Long Beach, CA September 21, 2009 The Global Recession

Trade and Economic Trends Marine Terminal Management Training Program Paul Bingham Managing Director, Global Commerce & Transportation IHS Global Insight Long Beach, CA September 21, 2009 The Global Recession

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

+44 (0) FOOTFALL: GLOBAL SHOPPER TRENDS REPORT Bringing you the latest consumer behaviour trends throughout the globe

FOOTFALL: GLOBAL SHOPPER TRENDS REPORT Bringing you the latest consumer behaviour trends throughout the globe") www.footfall.com +44 (0) 121 711 4652 FOOTFALL: GLOBAL SHOPPER TRENDS REPORT Bringing you the latest consumer behaviour trends throughout the globe Q1 2015 intro Welcome to FootFall s brand new Global

www.footfall.com +44 (0) 121 711 4652 FOOTFALL: GLOBAL SHOPPER TRENDS REPORT Bringing you the latest consumer behaviour trends throughout the globe Q1 2015 intro Welcome to FootFall s brand new Global

MUSTAFA MOHATAREM Chief Economist, General Motors

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

US imports from emerging economies have grown rapidly

US imports from emerging economies have grown rapidly Ratio to GDP (current dollars) 0.07 US merchandise imports, 1978 2008 0.06 0.05 0.04 0.03 0.02 Industrial Non-OPEC other 0.01 0 OPEC = Organization

US imports from emerging economies have grown rapidly Ratio to GDP (current dollars) 0.07 US merchandise imports, 1978 2008 0.06 0.05 0.04 0.03 0.02 Industrial Non-OPEC other 0.01 0 OPEC = Organization

Demographic change, long-run housing demand and the related challenges for the Irish banking sector

Demographic change, long-run housing demand and the related challenges for the Irish banking sector December 5 th, 2016 esri.ie David Duffy, Daniel Foley, Kieran McQuinn and Niall McInerney Outline: Addresses

Demographic change, long-run housing demand and the related challenges for the Irish banking sector December 5 th, 2016 esri.ie David Duffy, Daniel Foley, Kieran McQuinn and Niall McInerney Outline: Addresses

The US Economic Outlook

IHS ECONOMICS US Outlook The US Economic Outlook November 2014 ihs.com Rafael Amiel, Director latin America Economics +1 215 789 7405, rafael.amiel.ihs.com 2014 IHS The US economy is gaining momentum Growth

IHS ECONOMICS US Outlook The US Economic Outlook November 2014 ihs.com Rafael Amiel, Director latin America Economics +1 215 789 7405, rafael.amiel.ihs.com 2014 IHS The US economy is gaining momentum Growth

Current Hawaii Economic Conditions. Eugene Tian

Current Hawaii Economic Conditions Eugene Tian Department of Business, Economic Development & Tourism At the PATA/TTRA 2016 Annual Outlook & Economic Forecast Forum February 3, 2016 Positive Signs in the

Current Hawaii Economic Conditions Eugene Tian Department of Business, Economic Development & Tourism At the PATA/TTRA 2016 Annual Outlook & Economic Forecast Forum February 3, 2016 Positive Signs in the

Global Construction Outlook: Laura Hanlon Product Manager, Global Construction Outlook May 21, 2009

Global Construction Outlook: Short-term term Pain, Long-term Gain Laura Hanlon Product Manager, Global Construction Outlook May 21, 2009 What This Means for You The world is set to be hit this year with

Global Construction Outlook: Short-term term Pain, Long-term Gain Laura Hanlon Product Manager, Global Construction Outlook May 21, 2009 What This Means for You The world is set to be hit this year with

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

Canada s economy on track for a solid 2018 although policy uncertainty lingers

Canada s economy on track for a solid 2018 although policy uncertainty lingers Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com March 2018 Canada is facing a challenging

Canada s economy on track for a solid 2018 although policy uncertainty lingers Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com March 2018 Canada is facing a challenging

Understanding the. Dr. Christopher Waller. Federal Reserve Bank of St. Louis

Understanding the Unemployment Picture Dr. Christopher Waller Senior Vice President and Director of fresearch Federal Reserve Bank of St. Louis By David Andolfatto and Marcela Williams A Look at Unemployment

Understanding the Unemployment Picture Dr. Christopher Waller Senior Vice President and Director of fresearch Federal Reserve Bank of St. Louis By David Andolfatto and Marcela Williams A Look at Unemployment

Despite geopolitical woes Lithuania s economy enjoys balanced growth

Lithuanian Economic Outlook Despite geopolitical woes Lithuania s economy enjoys balanced growth Indrė Genytė-Pikčienė Chief analyst Economic Research Department DNB Markets 30 th of May, 2014 2000 I 2000

Lithuanian Economic Outlook Despite geopolitical woes Lithuania s economy enjoys balanced growth Indrė Genytė-Pikčienė Chief analyst Economic Research Department DNB Markets 30 th of May, 2014 2000 I 2000

Can China Pilot a Soft Landing? 2017 Article IV Consultation Analysis, Outlook, and Policy Advice

Can China Pilot a Soft Landing? 2017 Article IV Consultation Analysis, Outlook, and Policy Advice September 2017 1 KEY RECENT DEVELOPMENTS China has had strong growth momentum which Real GDP Real GDP Stabilizes

Can China Pilot a Soft Landing? 2017 Article IV Consultation Analysis, Outlook, and Policy Advice September 2017 1 KEY RECENT DEVELOPMENTS China has had strong growth momentum which Real GDP Real GDP Stabilizes

Economic Outlook. Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project

Economic Outlook Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project League of California Cities Monterey, CA December 3, 2014 Economic Update economic

Economic Outlook Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project League of California Cities Monterey, CA December 3, 2014 Economic Update economic

Steel: A Buyer s Market for the Worst of Reasons. John Anton Director, IHS Global Insight Steel Service August 2009

Steel: A Buyer s Market for the Worst of Reasons John Anton Director, IHS Global Insight Steel Service August 2009 The U.S. Recession Is Bottoming Out This recession has been the most severe of the postwar

Steel: A Buyer s Market for the Worst of Reasons John Anton Director, IHS Global Insight Steel Service August 2009 The U.S. Recession Is Bottoming Out This recession has been the most severe of the postwar

A comment on recent events, and...

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

Retrenchment or Stagnation: Lessons from Japan s Lost Decades. Andrew Smithers. UK-Japan 21 st Century Group Conference 3 rd May, 2013

Retrenchment or Stagnation: Lessons from Japan s Lost Decades. Andrew Smithers UK-Japan 21 st Century Group Conference 3 rd May, 2013 Slide 1. The Conventional Wisdom. Japan has suffered from two lost

Retrenchment or Stagnation: Lessons from Japan s Lost Decades. Andrew Smithers UK-Japan 21 st Century Group Conference 3 rd May, 2013 Slide 1. The Conventional Wisdom. Japan has suffered from two lost

The Eurozone integration, des-integration and possible future developments

The Eurozone integration, des-integration and possible future developments 18 th Monetary Policy Workshop at the Berlin School of Economcs and Law, 12 13 October 2017 Overview Position 1: The euro itself

The Eurozone integration, des-integration and possible future developments 18 th Monetary Policy Workshop at the Berlin School of Economcs and Law, 12 13 October 2017 Overview Position 1: The euro itself

RISI LATIN AMERICAN CONFERENCE. (São Paulo, 16 August 2016) The Latin American Economy: Some Successes, Many Disappointments

The Latin American Economy: Some Successes, Many Disappointments") RISI LATIN AMERICAN CONFERENCE (São Paulo, 16 August 2016) The Latin American Economy: Some Successes, Many Disappointments Andrea Boltho Magdalen College University of Oxford and Oxford Economics GDP

RISI LATIN AMERICAN CONFERENCE (São Paulo, 16 August 2016) The Latin American Economy: Some Successes, Many Disappointments Andrea Boltho Magdalen College University of Oxford and Oxford Economics GDP

US Light Vehicle Outlook. George Magliano Senior Principal Auto Economist Americas, HIS May 31, 2012

US Light Vehicle Outlook George Magliano Senior Principal Auto Economist Americas, HIS May 31, 2012 External Shocks to The Global Auto Industry - A Critical Timeline Sub-Prime Crisis Bear Sterns Oil Hits

US Light Vehicle Outlook George Magliano Senior Principal Auto Economist Americas, HIS May 31, 2012 External Shocks to The Global Auto Industry - A Critical Timeline Sub-Prime Crisis Bear Sterns Oil Hits

Recent Fiscal Developments and Outlook: The April 2014 IMF Fiscal Monitor Julio Escolano

Recent Fiscal Developments and Outlook: The April 214 IMF Fiscal Monitor Julio Escolano Division Chief, Fiscal Policy and Surveillance Fiscal Affairs Department, IMF Joint Vienna Institute, Vienna, June,

Recent Fiscal Developments and Outlook: The April 214 IMF Fiscal Monitor Julio Escolano Division Chief, Fiscal Policy and Surveillance Fiscal Affairs Department, IMF Joint Vienna Institute, Vienna, June,

Montreal Real Estate Forum. Economic Outlooks for March 31, Cooperating in building the future

Montreal Real Estate Forum March 31, 2015 Economic Outlooks for 2015 François Dupuis Vice-President and Chief Economist Desjardins Group Cooperating in building the future Outline The global economy and

Montreal Real Estate Forum March 31, 2015 Economic Outlooks for 2015 François Dupuis Vice-President and Chief Economist Desjardins Group Cooperating in building the future Outline The global economy and

The World and U.S. Economy and San Pedro Bay Container Trade Outlook Forecast Review

The World and U.S. Economy and San Pedro Bay Container Trade Outlook Forecast Review Michael Keenan Harbor Planning and Economic Analyst Port of Los Angeles October 5, 2009 Review of 2007 Container Trade

The World and U.S. Economy and San Pedro Bay Container Trade Outlook Forecast Review Michael Keenan Harbor Planning and Economic Analyst Port of Los Angeles October 5, 2009 Review of 2007 Container Trade

European Stagnation: Private sector structural balance + fiscal policy

European Stagnation: Private sector structural balance + fiscal policy Jesper Jespersen, Jesperj@ruc. dk Roskilde University & Aalborg University 21 st April 2017 Secular(?) stagnation in EU 1. Persistently

European Stagnation: Private sector structural balance + fiscal policy Jesper Jespersen, Jesperj@ruc. dk Roskilde University & Aalborg University 21 st April 2017 Secular(?) stagnation in EU 1. Persistently

Stocks and Bonds Track Aging Population:

Stocks and Bonds Track Aging Population: 1952-2008 8 85.00% 7 6 5 4 3 2 1 Correlation: 93% Stocks and Bonds as a Percentage of Household Liquid Financial Assets (left scale) Population 35 Years and Over

Stocks and Bonds Track Aging Population: 1952-2008 8 85.00% 7 6 5 4 3 2 1 Correlation: 93% Stocks and Bonds as a Percentage of Household Liquid Financial Assets (left scale) Population 35 Years and Over