From Recession to Recovery

|

|

|

- Roberta Marcia Lambert

- 5 years ago

- Views:

Transcription

1 From Recession to Recovery Monday, April 26, :00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific Investment Management Co. (PIMCO) Steve Forbes, Chairman and CEO, Forbes Media; Editor-in-Chief, Forbes Kenneth Griffin, Founder, President and CEO, Citadel Investment Group LLC Marc Lasry, Chairman and CEO, Avenue Capital Group 1

2 A lost decade The U.S. economy had its worst decade since the 1930s % Real GDP growth (%) % 4.4% 3.3% 3.1% 3.2% 2 1.3% 1.9% s 1940s 1950s 1960s 1970s 1980s 1990s 2000s Source: The U.S. Bureau of Economic Analysis. 2

3 8.2 million total job losses Thousands of nonfarm workers 400 Average monthly change in employment 8.2 million workers lost their jobs December 2007-March Q1: Q1: 2010 Source: U.S. Bureau of Labor Statistics. 3

4 Americans net worth is down by 12 trillion from its 2007 peak US$ trillions Household's net worth Pre-recession peak: 70 $65.9 trillion Fourth quarter, 2009 $54.2 trillion Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Source: Federal Reserve

5 Deep recession, strong recovery? Average real GDP growth rates (%) in the four quarters following each recession Periods of Recession % % XX? 1.9% 2.6% 7.8% Real GDP grew 10.9% in 1934, the year after the Great Depression ended Sources: U.S. Bureau of Economic Analysis; the Milken Institute. 5

6 Large reductions in the world real GDP growth Real GDP (% change, year-to-year) Projected 10 Emerging and 8 developing economies World Advanced economies

7 World stock market capitalization still 23% below its peak level (as of April 20, 2010) US$ trillions Highest point: $62.6 trillion on October 31, 2007 Lowest point: $25.6 trillion on March 9, 2009 $48 trillion as of April 20, Source: Bloomberg. 7

8 Forecasts of positive real GDP growth rates Real GDP growth (%) (Quarterly ypercentage change, seasonally adjusted at an annual rate) Note: Composite forecasts are average forecasts of 27 private organizations. Sources: U.S. Bureau of Economic Analysis; Bloomberg Composite forecasts Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q

9 Decline in initial claims for unemployment insurance Thousands million people receiving jobless benefits as of June, million (as of March 31, 2010) Source: U.S. Bureau of Labor Statistics. 9

10 Retail sales climbed in March A sign showing American consumers were beginning to spend more US$ billions 400 Monthly total retail sales, seasonally adjusted +1.6% in March Shade area indicates recession Source: U.S. Department of Commerce. 10

11 Turnaround stock markets 15,000 12,500 Nasdaq (right scale) ,800 1,600 Russell 2000 (right scale) 1, ,000 7,500 Dow Jones (left scale) ,200 1, S&P 500 (left scale) , Source: DataStream. 11

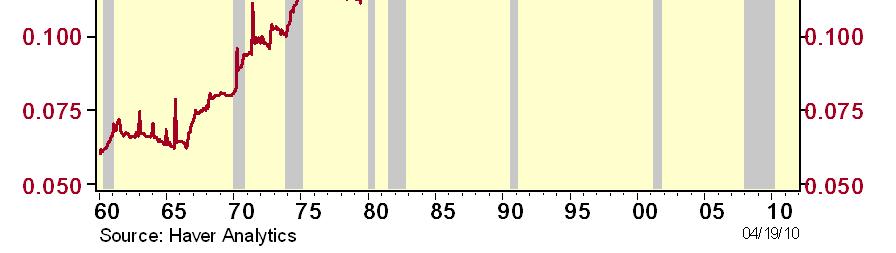

12 Narrowing risk spread Indicative of the reduced stress in the debt markets Percentage points 5 Oct10, TED spread 3 2 BAA-AAA spread 1 0 Note: The TED spread is the difference between 3-month LIBOR rates and the yield on 3-month U.S. Treasury bills. The BAA-AAA spread is the difference between the interest rates on high-grade and medium-grade corporate bonds. Sources: Bloomberg, Federal Reserve. 12

13 Unemployment rate near the highest level since Great Depression % Unemployment rate: 10.8% 12 Unemploymentrate:9.7% during the recession in March, Source: U.S. Bureau of Labor Statistics. 13

14 Involuntary part-time or underemployed hits the highest level in 50 years Thousands ,000 6,000 5,000 4,000 Part-time employment for economic reasons Part-time due to slack work or business conditions 3, ,000 1, Source: U.S. Bureau of Labor Statistics. Could only find part-time work

15 One in four black, Hispanic workers is underemployed (%) Underemployment rates by race 26 Hispanic or Latino 23.2% African American 23.1% White 13.7% Dec-07 Apr-08 Aug-08 Dec-08 Apr-09 Aug-09 Nov-09 Note: the shown underemployment data are from November, Underemployed includes the unemployed, involuntary part-time, and discouraged workers. Source: The Economic Policy Institute. 15

16 Job creation still a problem Rate of job creation and destruction Percent Job destruction Job creation Sources: Bureau of Labor Statistics, Moody s Economy.com 16

17 Small businesses account for nearly half the decline in job creation Change between 2007 and Q >1000 employees 27.1% Total change in job creation = -1,648 ths employees 48.5% employees 24.5% Sources: Bureau of Labor Statistics, Moody s Economy.com 17

18 60 percent of current decline in job creation stems from small businesses versus 26 percent in previous recession Percent Job creation with <100 employees Job destruction with <100 employees Q Q Sources: Bureau of Labor Statistics, Moody s Economy.com Q Q

19 Nearly 1 in 4 homeowners underwater % negative equity Q3, Q4, States with negative equity share > 20% as of Q4: % 24% Note: The data only include properties with a mortgage. Source: First American CoreLogic. 19

20 Banks are still pulling back on lending No bank lending, no recovery US$ trillions 8 Lending by the U.S. commercial banks fell by 7.5% in Q1, 2008 Q2, 2008 Q3, 2008 Q4, 2008 Q1, 2009 Q2, 2009 Q3, 2009 Q4, 2009 Note: The data are loan balances (net loans and leases ) of all U.S. commercial banks. Source: Quarterly Banking Profile, Federal Deposit Insurance Corporation. 20

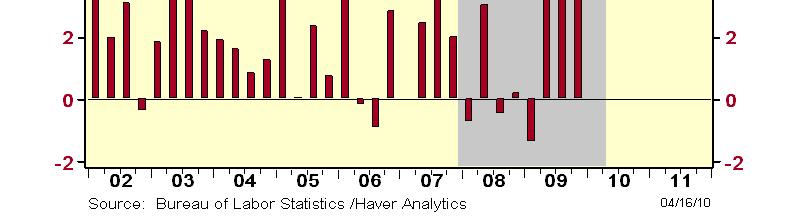

21 Households are deleveraging U.S. households need to reduce their debt to more manageable level U.S. household debt (% of disposable personal income) Economists see 100% as a sustainable level 50 Total household debt stood at 123% as of the end of Source: Federal Reserve. 21

22 Upward trend of U.S. saving rate % U.S. personal saving rate (% of disposable personal income) The saving rate has started to increase following a decadeslong decline Q Q Q Q Q Q Source: U.S. Bureau of Economic Analysis. 22

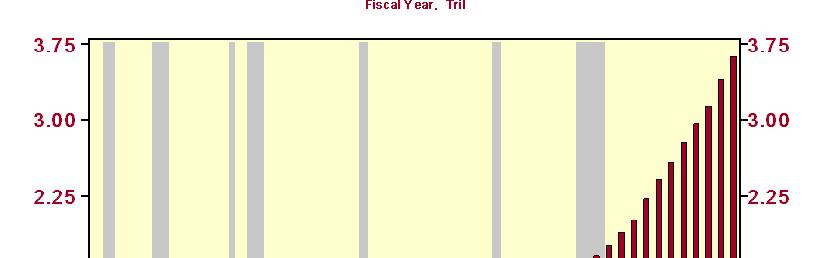

23 Consumer borrowing still declined % change of total consumer credit % from a previous year, seasonally adjusted % in 6 January % in February Jan-08 Jul-08 Jan-09 Jul-09 Feb-10 Source: Federal Reserve. 23

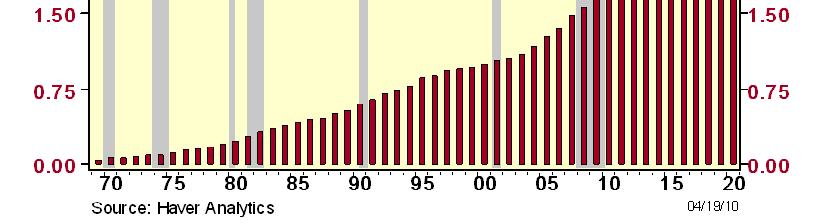

24 Growing personal bankruptcy filings The total number of bankruptcy filings = 1.47 million in 2009 Thousands 800 The number of quarterly bankruptcy filings in the federal courts Business bankruptcy filings Personal bankruptcy filings Total Q Q Q Q Q Q Q Q Source: Administrative Office of the U.S. Courts. 24

25 Global economic forecasts Emerging market economies will lead the world growth % Real GDP growth forecasts by key countries/regions 9 (average ) 2014) Western Japan United Latin MENA Brazil Asia India China Europe States America Source: Economist Intelligence Unit. 25

26 The U.S. dollar Trade weight exchange index (January 1997 = 100) Euro/US$ (right axis) Euro/US$ Trade weighted (left axis) Source: Federal Reserve

27 U.S. current account deficit US$ billions 50 U.S. current account, seasonally adjusted Source: The U.S. Bureau of Economic Analysis. 27

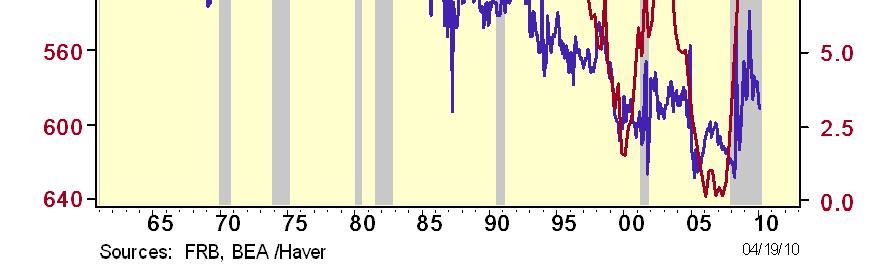

28 Parallel relationship between stock market performance and the unemployment rate Dow Jones hits 11,000; Unemployment rate (%) unemployment rate nears 10% (right- axis) Dow Jones (left- axis) Sources: U.S. Bureau of Labor Statistics; DataStream. 28

29 U.S. fiscal position is in a free fall US$ billions Federal surplus [+] or deficit [-], fiscal year ,000-1,200 Shade area indicates recession -1,400-1, Source: The Office of Management and Budget, White House. 29

30 President Obama's budget will generate nearly $10 trillion in budget deficits over the next 10 years Federal Budget (US$ billions) ,000-1,200-1,400-1,600 US$9.761 trillion total deficit from 2011 to 2020 Actual CBO's estimate of federal budget for fiscal year Source: Congressional Budget Office (CBO). 30

31 National debt will reach 90% of GDP in the next decade % of GDP Federal debt held by public % of GDP, or $9.2 trillion % of GDP, or $20.3 trillion 10 CBO's estimate Source: Congressional Budget Office (CBO). 31

32 Change in the world economic power China and India are larger in the world economy Real GDP (PPP dollars), share of world total 1991 United States 22% 2009 United States 20% Rest of the world 48% U.K. 4% France 4% China 4% Japan 9% India 3% Germany 6% Rest of the world 47% China 12% Japan U.K. 6% 3% India France 5% Germany 3% 4% Sources: International Monetary Fund, The Milken Institute. 32

33 Kenneth Griffin s Slides 33

34 Residential real estate loan delinquency rate 34

35 Personal transfer payments 35

36 Household s net worth (as a % of disposable personal income) 36

37 Unemployment and underemployment 37

38 Continuing claims and insured unemployment 38

39 Federal outlays: interest 39

40 Entitlements and interest 40

41 Federal on-budget surplus/deficit [-] 41

42 Share of individual income tax liabilities: top 10 percent 42

43 Share of income: highest 5 percent of families 43

44 Share of individual income tax liabilities: middle income quintile 44

45 Median income of households 45

46 Establishment survey of employment 46

47 Wage and salary disbursements 47

48 Nonfarm business productivity: Output per person 48

49 Nonfarm business: output per person 49

50 Consumer loans: credit cards and other revolving plans 50

51 ICSC-Goldman Sachs weekly retail chain store sales 51

52 Home equity withdrawal: mortgages less residential construction 52

53 When will Americans total net worth return to the peak it saw in the middle of 2007? Your choices are: A. By the end of 2010 B. First 2011 C. Second Half 2011 D E or Later 53

54 In the 79 years from 1930 to 2008, how many years did the U.S. Government have a budget surplus? A. 2 B. 9 C. 13 D. 22 E

Reading the Tea Leaves: Investing for 2010 and Beyond

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

ABA Commercial Real Estate Lending Committee

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H. Parker Willis Lecture in Political Economics

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

More of the Same; Or now for Something Completely Different?

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

The Global Economy: Sustaining Momentum

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six years of steady growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half Full

The Economic Outlook Economic Policy Division Glass Half Full Six years of steady growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half Full

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Muhlenkamp & Company. Webinar December 1, Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Economic & Financial Market Outlook

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

RBC Economics Financial Update Dawn Desjardins

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States?

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Kevin Thorpe Financial Economist & Principal Cassidy Turley

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip?

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Trends. September 10, 2013

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes. Tom Rogers. Lead Economist, Oxford Economics.

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

Economy On The Rebound

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Babson Capital/UNC Charlotte Economic Forecast. May 13, 2014

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Real gross domestic growth

Real gross domestic growth United States, 2000 prices Compound annual growth rate 10 5 0-5 -10 81 83 85 87 89 91 93 95 97 99 01 03 05 07 Sources: BEA, Global Insight. Consumer sentiment University of Michigan,

Real gross domestic growth United States, 2000 prices Compound annual growth rate 10 5 0-5 -10 81 83 85 87 89 91 93 95 97 99 01 03 05 07 Sources: BEA, Global Insight. Consumer sentiment University of Michigan,

National and Regional Economic Outlook. Central Southern CAA Conference

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

Economic Overview. Melissa K. Peralta Senior Economist April 27, 2017

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Global economy maintaining solid growth momentum. Canada leading the pack

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office The views expressed in this presentation are strictly those of the author and do not necessarily

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office The views expressed in this presentation are strictly those of the author and do not necessarily

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Big Changes, Unknown Impacts

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

SA economic review Kevin Lings. August 2018

SA economic review Kevin Lings August 2018 South Africa real GDP growth year-on-year %y/y 8 7 6 5 Ave 4.3% 4 Ave 2.5% 3 2 Ave 0.9% 1 0-1 -2-3 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 2

SA economic review Kevin Lings August 2018 South Africa real GDP growth year-on-year %y/y 8 7 6 5 Ave 4.3% 4 Ave 2.5% 3 2 Ave 0.9% 1 0-1 -2-3 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 2

Zions Bank Economic Overview

Zions Bank Economic Overview Intermountain Credit Education League May 10, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around

Zions Bank Economic Overview Intermountain Credit Education League May 10, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around

A comment on recent events, and...

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

Composition of Federal Spending

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

10 County Conference. Richard Wobbekind. Executive Director Business Research Division & Senior Associate Dean Leeds School of Business

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

Economic Update: Accelerating Growth and Increasing Risk

Economic Update: Accelerating Growth and Increasing Risk Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business May 23, 2018 The forecasts and commentary do

Economic Update: Accelerating Growth and Increasing Risk Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business May 23, 2018 The forecasts and commentary do

Southwest Ohio Regional Economy in Context. Richard Stock, PhD. Business Research Group

Southwest Ohio Regional Economy in Context Richard Stock, PhD. Business Research Group State of the Metro Area (in January Each Year) Total Employment has slowly increased in the last three years after

Southwest Ohio Regional Economy in Context Richard Stock, PhD. Business Research Group State of the Metro Area (in January Each Year) Total Employment has slowly increased in the last three years after

BC Pension Forum. Economic Outlook. Presented by: Ben Homsy, CFA Portfolio Manager

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

Global Economic Outlook. Kellie Maske, Sr. Economics Fellow FedEx Corporate Economics September 2011

Kellie Maske, Sr. Economics Fellow FedEx Corporate Economics U.S. Outlook: Moderate Growth Overall 6 4 US Real GDP Growth 2 % Change 0 (2) (4) Forecast (6) (8) Bars = QOQ% Annualized Line = YOY% (10) 2005

Kellie Maske, Sr. Economics Fellow FedEx Corporate Economics U.S. Outlook: Moderate Growth Overall 6 4 US Real GDP Growth 2 % Change 0 (2) (4) Forecast (6) (8) Bars = QOQ% Annualized Line = YOY% (10) 2005

Global growth forecasts Key countries/regions,

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

Southern California Economic Forecast & Industry Outlook

2016-17 Southern California Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Sr. VP/Chief Economist, LAEDC February 17, 2016 Outline U.S. Economy California Economy Southern California Economy

2016-17 Southern California Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Sr. VP/Chief Economist, LAEDC February 17, 2016 Outline U.S. Economy California Economy Southern California Economy

India: Can the Tiger Economy Continue to Run?

India: Can the Tiger Economy Continue to Run? India s GDP is on the rise US$ trillions Nominal GDP (left axis) GDP growth (right axis) 3.0 2.5 2.0 1.5 1.0 0.5 0.0 1990 1992 1994 1996 1998 2000 2002 2004

India: Can the Tiger Economy Continue to Run? India s GDP is on the rise US$ trillions Nominal GDP (left axis) GDP growth (right axis) 3.0 2.5 2.0 1.5 1.0 0.5 0.0 1990 1992 1994 1996 1998 2000 2002 2004

Airline industry outlook 2019

Airline industry outlook 2019 Brian Pearce Chief Economist 12 December 2018 Million barrels a day US$ per barrel Are the markets signalling recession ahead? 60 55 Business confidence (left scale) FTSE

Airline industry outlook 2019 Brian Pearce Chief Economist 12 December 2018 Million barrels a day US$ per barrel Are the markets signalling recession ahead? 60 55 Business confidence (left scale) FTSE

The U.S. Economic Outlook

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

Muhlenkamp & Company. Webcast August 30, Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President

Muhlenkamp & Company Webcast August 30, 2018 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Muhlenkamp & Company Webcast August 30, 2018 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

Old Dominion University 2017 Regional Economic Forecast. Strome College of Business

Old Dominion University 2017 Regional Economic Forecast January 25, 2017 Professor Vinod Agarwal Director, Economic Forecasting Project Strome College of Business www.odu.edu/forecasting The views expressed

Old Dominion University 2017 Regional Economic Forecast January 25, 2017 Professor Vinod Agarwal Director, Economic Forecasting Project Strome College of Business www.odu.edu/forecasting The views expressed

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee The U.S. economy has now enjoyed 7 years of economic growth since the Great Recession Real GDP grew by 1.2% in

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee The U.S. economy has now enjoyed 7 years of economic growth since the Great Recession Real GDP grew by 1.2% in

Outline. Overview of globalization. Global outlook for real economic activity & inflation. Risks to the outlook

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

Outlook for growth, traffic and airline profits

Outlook for growth, traffic and airline profits Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 50 = no change in output expected Widespread

Outlook for growth, traffic and airline profits Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 50 = no change in output expected Widespread

Economic Growth in the Trump Economy

Economic Growth in the Trump Economy Presented to State Data Center Conference William F. Fox, Director November 18, 2016 GDP Grows, Though Slowly 10.0 8.0 Percentage Change, Previous Qtr, SAAR 6.0 4.0

Economic Growth in the Trump Economy Presented to State Data Center Conference William F. Fox, Director November 18, 2016 GDP Grows, Though Slowly 10.0 8.0 Percentage Change, Previous Qtr, SAAR 6.0 4.0

Colorado Economic Update

Colorado Economic Update Steamboat Economic Summit Place cover image here Brian Lewandowski Associate Director, Business Research Division October 21, 2016 Recession 8 Months Recession 18 Months Real GDP

Colorado Economic Update Steamboat Economic Summit Place cover image here Brian Lewandowski Associate Director, Business Research Division October 21, 2016 Recession 8 Months Recession 18 Months Real GDP

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Update.

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Update February 26, 2013 The Worst Recession Since the Great Depression 0% Loss from Peak

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Update February 26, 2013 The Worst Recession Since the Great Depression 0% Loss from Peak

Shifting International Trade Routes A National Economic Outlook. February 1, 2011

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

Airlines, the economy and air transport demand

Airlines, the economy and air transport demand Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 Returns for airlines investors lower this year;

Airlines, the economy and air transport demand Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 Returns for airlines investors lower this year;

As Good as it Gets. The Aging Expansion Powers On... but for How Much Longer? Andrew J. Nelson Chief Economist USA, Colliers International

As Good as it Gets The Aging Expansion Powers On... but for How Much Longer? Andrew J. Nelson Chief Economist USA, Colliers International #NMHCstudent @ApartmentWire Ten Years After: A Full if Imperfect

As Good as it Gets The Aging Expansion Powers On... but for How Much Longer? Andrew J. Nelson Chief Economist USA, Colliers International #NMHCstudent @ApartmentWire Ten Years After: A Full if Imperfect

The Herzliya Conference The Economic Dimension Prof. Rafi Melnick Provost, Interdisciplinary Center (IDC) Herzliya

Herzliya") The Herzliya Conference The Economic Dimension 2009 Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

The Herzliya Conference The Economic Dimension 2009 Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis. May 8 th, Presented by:

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis May 8 th, 2008 Presented by: Patricia Croft, Vice President & Chief Economist Phillips, Hager & North Investment Management Limited

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis May 8 th, 2008 Presented by: Patricia Croft, Vice President & Chief Economist Phillips, Hager & North Investment Management Limited

Understanding the. Dr. Christopher Waller. Federal Reserve Bank of St. Louis

Understanding the Unemployment Picture Dr. Christopher Waller Senior Vice President and Director of fresearch Federal Reserve Bank of St. Louis By David Andolfatto and Marcela Williams A Look at Unemployment

Understanding the Unemployment Picture Dr. Christopher Waller Senior Vice President and Director of fresearch Federal Reserve Bank of St. Louis By David Andolfatto and Marcela Williams A Look at Unemployment

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Macroeconomic Research and Statistics Department Vol. XVIl, No.3 March 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02 Table

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Macroeconomic Research and Statistics Department Vol. XVIl, No.3 March 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02 Table

2019 Economic Outlook: Will the Recovery Ever End?

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

Economic Outlook: fear over fundamentals

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

The US Economic Outlook

IHS ECONOMICS US Outlook The US Economic Outlook November 2014 ihs.com Rafael Amiel, Director latin America Economics +1 215 789 7405, rafael.amiel.ihs.com 2014 IHS The US economy is gaining momentum Growth

IHS ECONOMICS US Outlook The US Economic Outlook November 2014 ihs.com Rafael Amiel, Director latin America Economics +1 215 789 7405, rafael.amiel.ihs.com 2014 IHS The US economy is gaining momentum Growth

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.9 September 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.9 September 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies Chief Economist, PAGI Group, JLL (Port, Airport & Global Infrastructure) Agenda Where are we in the cycle? What are the barriers

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies Chief Economist, PAGI Group, JLL (Port, Airport & Global Infrastructure) Agenda Where are we in the cycle? What are the barriers

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.11 November 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.11 November 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

Current Hawaii Economic Conditions. Eugene Tian

Current Hawaii Economic Conditions Eugene Tian Department of Business, Economic Development & Tourism At the PATA/TTRA 2016 Annual Outlook & Economic Forecast Forum February 3, 2016 Positive Signs in the

Current Hawaii Economic Conditions Eugene Tian Department of Business, Economic Development & Tourism At the PATA/TTRA 2016 Annual Outlook & Economic Forecast Forum February 3, 2016 Positive Signs in the

U.S. REITs have rebounded strongly Dow Jones Equity REIT Total Return Index

U.S. REITs have rebounded strongly Dow Jones Equity REIT Total Return Index Index, 2005 = 100 250 200 150 100 50 0 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Sources: Bloomberg, Dow Jones. Affordability

U.S. REITs have rebounded strongly Dow Jones Equity REIT Total Return Index Index, 2005 = 100 250 200 150 100 50 0 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Sources: Bloomberg, Dow Jones. Affordability

Zions Bank Economic Overview

Zions Bank Economic Overview Kenworth National Dealers Conference November 8, 2018 1 National Economic Conditions 2 Volatility Returns to the Stock Market 27,000 Dow Jones Industrial Average October 10,

Zions Bank Economic Overview Kenworth National Dealers Conference November 8, 2018 1 National Economic Conditions 2 Volatility Returns to the Stock Market 27,000 Dow Jones Industrial Average October 10,

The Israeli Economy 2009 The Caesarea Center Conference

The Israeli Economy 2009 The Caesarea Center Conference Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

The Israeli Economy 2009 The Caesarea Center Conference Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

Canadian Housing In Flux

Dr. Sherry Cooper Chief Economist Dominion Lending Centres The Title of the presentation Second line if needed Third line if needed Canadian Housing In Flux Today s date Location of presentation March

Dr. Sherry Cooper Chief Economist Dominion Lending Centres The Title of the presentation Second line if needed Third line if needed Canadian Housing In Flux Today s date Location of presentation March

Zions Bank Economic Overview

Zions Bank Economic Overview Veteran Owned Business Conference May 11, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around Correction

Zions Bank Economic Overview Veteran Owned Business Conference May 11, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around Correction

11 th Annual Oregon Economic Forum!

11 th Annual Oregon Economic Forum! (almost) Beyond! Macroeconomics Portland, OR! October 16, 2014! Expansion Continues! Five Years and More!! Recession Indicators Nonfarm Payrolls Real Personal Income

11 th Annual Oregon Economic Forum! (almost) Beyond! Macroeconomics Portland, OR! October 16, 2014! Expansion Continues! Five Years and More!! Recession Indicators Nonfarm Payrolls Real Personal Income

Global economy s strong momentum intact despite elevated level of uncertainty. Canada headed for another year of solid growth

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

The United States: Fiscal Facts and Fantasies. Presented by: Nigel Gault Chief U.S. Economist IHS Global Insight

The United States: Fiscal Facts and Fantasies Presented by: Nigel Gault Chief U.S. Economist IHS Global Insight Subdued Recovery: Tailwinds Battling Headwinds The U.S. Recovery: Tailwinds More sectors

The United States: Fiscal Facts and Fantasies Presented by: Nigel Gault Chief U.S. Economist IHS Global Insight Subdued Recovery: Tailwinds Battling Headwinds The U.S. Recovery: Tailwinds More sectors

The Erie Economy: Performance, Opportunities, and Challenges

The Erie Economy: Performance, Opportunities, and Challenges Eggs n Issues Manufacturer and Business Association December 2015 Dr. Kenneth Louie The Economic Research Institute of Erie Sam and Irene Black

The Erie Economy: Performance, Opportunities, and Challenges Eggs n Issues Manufacturer and Business Association December 2015 Dr. Kenneth Louie The Economic Research Institute of Erie Sam and Irene Black

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

MUSTAFA MOHATAREM Chief Economist, General Motors

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

The U.S. & World Economy: The Good, the Bad, and the Ugly

The U.S. & World Economy: The Good, the Bad, and the Ugly Michael Strauss Chief Economist and Chief Investment Strategist Commonfund October 16, 2012 The U.S. & World Economy: The Good, the Bad, and the

The U.S. & World Economy: The Good, the Bad, and the Ugly Michael Strauss Chief Economist and Chief Investment Strategist Commonfund October 16, 2012 The U.S. & World Economy: The Good, the Bad, and the

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

US Economic Outlook IHS ECONOMICS. Paul Edelstein, Director NA Financial Economics, ,

IHS ECONOMICS US Outlook US Economic Outlook How long will the ride last? September 2014 ihs.com Paul Edelstein, Director NA Financial Economics, +1 781 301 9014, paul.edelstein@ihs.com The US economy

IHS ECONOMICS US Outlook US Economic Outlook How long will the ride last? September 2014 ihs.com Paul Edelstein, Director NA Financial Economics, +1 781 301 9014, paul.edelstein@ihs.com The US economy

Grasshoppers, Ants and Locusts: the future of the world economy

Ralph Miliband Series on the Restructuring of World Power Grasshoppers, Ants and Locusts: the future of the world economy Martin Wolf Associate editor and chief economics commentator, Financial Times Professor

Ralph Miliband Series on the Restructuring of World Power Grasshoppers, Ants and Locusts: the future of the world economy Martin Wolf Associate editor and chief economics commentator, Financial Times Professor

Forecast evaluation report Robert Chote Chairman

Forecast evaluation report 2017 Robert Chote Chairman Background to the FER The FER is an annual report looking at the performance of past EFO forecasts against the latest outturn data Rationale Accountability

Forecast evaluation report 2017 Robert Chote Chairman Background to the FER The FER is an annual report looking at the performance of past EFO forecasts against the latest outturn data Rationale Accountability

Friday, May 22, NAR Convention

NAR Convention 5-14-09 NAR Convention 5-14-09 Lawrence Yun, NAR Chief Economist NAR Marketing Tips!Provide Market Data to buyers!forbes Buyer Survey: Now good time to buy home!best Banner Ads: 1. Has Market

NAR Convention 5-14-09 NAR Convention 5-14-09 Lawrence Yun, NAR Chief Economist NAR Marketing Tips!Provide Market Data to buyers!forbes Buyer Survey: Now good time to buy home!best Banner Ads: 1. Has Market

The 2019 Economic Outlook Forum The Outlook for MS

The 2019 Economic Outlook Forum The Outlook for MS February 2019 Mississippi University Research Center Mississippi Institutions of Higher Learning Darrin Webb, State Economist dwebb@mississippi.edu (601)432-6556

The 2019 Economic Outlook Forum The Outlook for MS February 2019 Mississippi University Research Center Mississippi Institutions of Higher Learning Darrin Webb, State Economist dwebb@mississippi.edu (601)432-6556

Colorado Counties Treasurers Association

Colorado Counties Treasurers Association Place cover image here Richard Wobbekind Executive Director, Business Research Division June 21, 2016 Real GDP Growth Quarterly and Annualized Real GDP 1990-2016

Colorado Counties Treasurers Association Place cover image here Richard Wobbekind Executive Director, Business Research Division June 21, 2016 Real GDP Growth Quarterly and Annualized Real GDP 1990-2016

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

Impacts of the Global Economy on Asia Pacific Travel. 29 June 2007 John Walker

Impacts of the Global Economy on Asia Pacific Travel 29 June 2007 John Walker jwalker@oxfordeconomics.com Oxford Economics Founded in 1981 Over 300 clients including blue chip companies and government

Impacts of the Global Economy on Asia Pacific Travel 29 June 2007 John Walker jwalker@oxfordeconomics.com Oxford Economics Founded in 1981 Over 300 clients including blue chip companies and government

Why Is the Recovery from the Financial Crisis So Sluggish?

Why Is the Recovery from the Financial Crisis So Sluggish? Robert E. Hall Hoover Institution and Department of Economics Stanford University Keynote Address Agricultural and Applied Economics Association

Why Is the Recovery from the Financial Crisis So Sluggish? Robert E. Hall Hoover Institution and Department of Economics Stanford University Keynote Address Agricultural and Applied Economics Association

The Economy: A View from the (Atlanta) Fed (Staff)

Fed (Staff)") The Economy: A View from the (Atlanta) Fed (Staff) 2018 Alabama Economic Outlook Montgomery, AL January 11, 2018 2 The new supply-side economics? In their discussion of monetary policy, participants saw

The Economy: A View from the (Atlanta) Fed (Staff) 2018 Alabama Economic Outlook Montgomery, AL January 11, 2018 2 The new supply-side economics? In their discussion of monetary policy, participants saw

2015 Economic Forecast & Industry Outlook. Robert A. Kleinhenz, Ph.D. Chief Economist, Kyser Center for Economic Research, LAEDC October 8, 2014

2015 Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Chief Economist,, LAEDC October 8, 2014 Outline U.S. Economy California Economy Southern California Economy & Industries Five-Year Outlook

2015 Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Chief Economist,, LAEDC October 8, 2014 Outline U.S. Economy California Economy Southern California Economy & Industries Five-Year Outlook

The Current Restructuring Cycle: Meltdown or Metamorphosis? Monday, April 27, :00 PM - 5:15 PM

The Current Restructuring Cycle: Meltdown or Metamorphosis? Monday, April 27, 29 4: PM - 5:15 PM Today s Speakers: Michael Henkin (Moderator) Managing Director and Co-Head of Recapitalization & Restructuring

The Current Restructuring Cycle: Meltdown or Metamorphosis? Monday, April 27, 29 4: PM - 5:15 PM Today s Speakers: Michael Henkin (Moderator) Managing Director and Co-Head of Recapitalization & Restructuring

Economic Outlook for Canada: Economy Confronting Capacity Limits

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

Europe June Craig Menear. Chairman, CEO & President. Diane Dayhoff. Vice President, Investor Relations

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

Great Depressions of the Twentieth Century Project

Great Depressions of the Twentieth Century Project Timothy J. Kehoe and Edward C. Prescott www.greatdepressionsbook.com Cole and Ohanian, The Great Depression in the United States from a Neoclassical Perspective,

Great Depressions of the Twentieth Century Project Timothy J. Kehoe and Edward C. Prescott www.greatdepressionsbook.com Cole and Ohanian, The Great Depression in the United States from a Neoclassical Perspective,

It Was Never Going To Be Easy

It Was Never Going To Be Easy Stephen Toplis, Head of Research July 2010 Introduction Global power shift sustained Average outlook on the improve Fiscal constraints binding Domestic rebalance under way

It Was Never Going To Be Easy Stephen Toplis, Head of Research July 2010 Introduction Global power shift sustained Average outlook on the improve Fiscal constraints binding Domestic rebalance under way

Charting a Path to Lift Off? Understanding the Shifting Economic Winds

Charting a Path to Lift Off? Understanding the Shifting Economic Winds Thomas F. Siems, Ph.D. Assistant Vice President and Senior Economist Federal Reserve Bank of Dallas Government Finance Officers Arlington,

Charting a Path to Lift Off? Understanding the Shifting Economic Winds Thomas F. Siems, Ph.D. Assistant Vice President and Senior Economist Federal Reserve Bank of Dallas Government Finance Officers Arlington,