COMMERCIAL POLICY STUDY UPDATE

|

|

|

- Chloe Whitehead

- 5 years ago

- Views:

Transcription

1 BACKGROUND & ANALYSIS REPORT for the Community of Stouffville COMMERCIAL POLICY STUDY UPDATE October 2012 AND W. SCOTT MORGAN & ASSOCIATES

2 Community of Stouffville Commercial Policy Study Update Background and Analysis Report Table of Contents 1. Why is The Town undertaking a Commercial Policy Study Update? What is the purpose of the Commercial Policy Study Update? What is the Study Process? How does the Update relate to the 2005 Commercial Policy Study? What are the components of the Community of Stouffville s Existing Retail Commercial Hierarchy? Existing Hierarchy Stouffville s Closest Competition How adequate is the supply of lands set aside for commercial purposes? Who is shopping in the Community of Stouffville and what are they shopping for? Market Study Conclusions Implications for the Current Commercial Planning Policy Framework APPENDIX I: Projections of Residual Market Demands

3 Community of Stouffville Commercial Policy Study Update Background and Analysis Report 1. Why is The Town undertaking a Commercial Policy Study Update? In 2005, Council adopted a Commercial Policy Study, which assessed the commercial land use requirements of the Community of Stouffville in the context of emerging residential growth. The strategy projected commercial land use needs through to the 2011 time period based upon the growth projections at that time. Given that the Commercial Policy Study is now over five (5) years old, the Town determined that it was necessary to revisit the original study assumptions to confirm their validity and to maintain a responsive commercial policy framework in the Stouffville Secondary Plan to assess future commercial development applications and to guide commercial land use policy. In particular, the Study is being undertaken in the context of updated population forecasts (York Region, May 31, 2012) which indicate that current population levels in the Town of Whitchurch-Stouffville will increase by about 50% over the next 19 years ( ) from 41,235 in 2012 to 60,600 in What is the purpose of the Commercial Policy Study Update? The Update to the Study is to assess the implications of growth to date on the commercial area, and to examine commercial land use requirements through to the year This comprehensive review will assess the adequacy of the supply of lands set aside for commercial purposes and recommend whether any revisions are required to land use designations and policies/zone standards to protect the planned function of each commercial area in the Community. 3. What is the Study Process? The Commercial Policy Study Update involves the following tasks: Phase 1: Task 1.1 Project Initiation This Task involved the initiation of the study process including the initial public notice and stakeholder consultation. This task is complete. Task 1.2 Background Analysis Task 1.2 involved a comprehensive market study to identify retail commercial needs, in particular the magnitude, timing and mix of any required future additions to the Community of Stouffville s existing commercial development 1

4 Community of Stouffville Commercial Policy Study Update Background and Analysis Report that are warranted in the long and short term. The results of the market work are reflected in this Background and Analysis Report, with the detailed analysis found in Appendix I, Projections of Residual Market Demands. The release of this report concludes the work in Task 1.2. Task 1.3 Draft Background Report Initial Review The review of the Background and Analysis Report will be carried out with the public and key stakeholders in Task 1.3. This input will inform the work in Phase 2. Phase 2: Task 2.1 Official Plan and Zoning By-law Amendments A report outlining specific recommendations for amendments to the Official Plan and Zoning By-law will be developed based on the input in Task 1.3. The report will then be submitted to Council. Based on Council s direction, formal Secondary Plan and Zoning By-law amendments will be prepared and released for public review. Task 2.2 Public Review A formal public review of the amendments will be carried out before they are submitted to Council for approval. 2

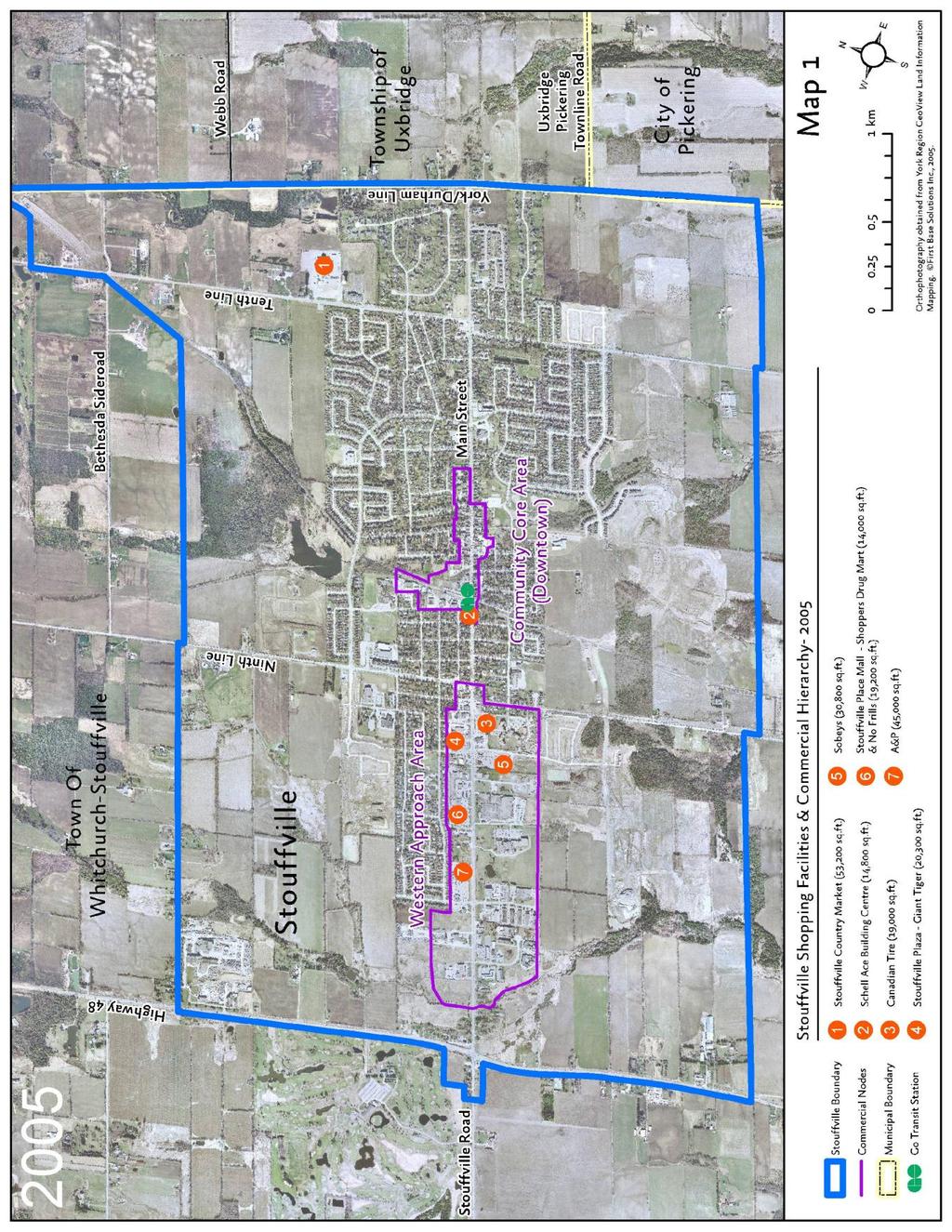

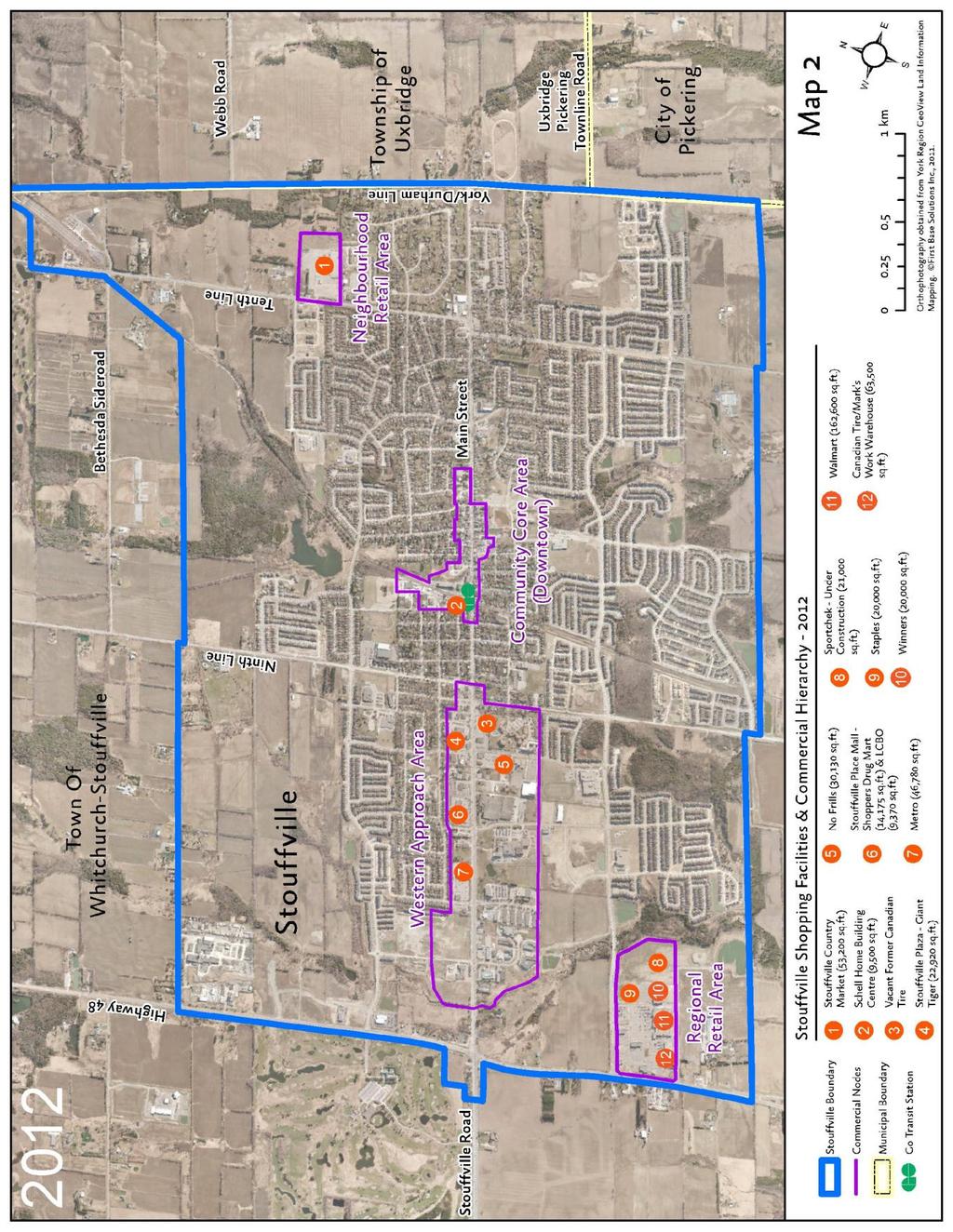

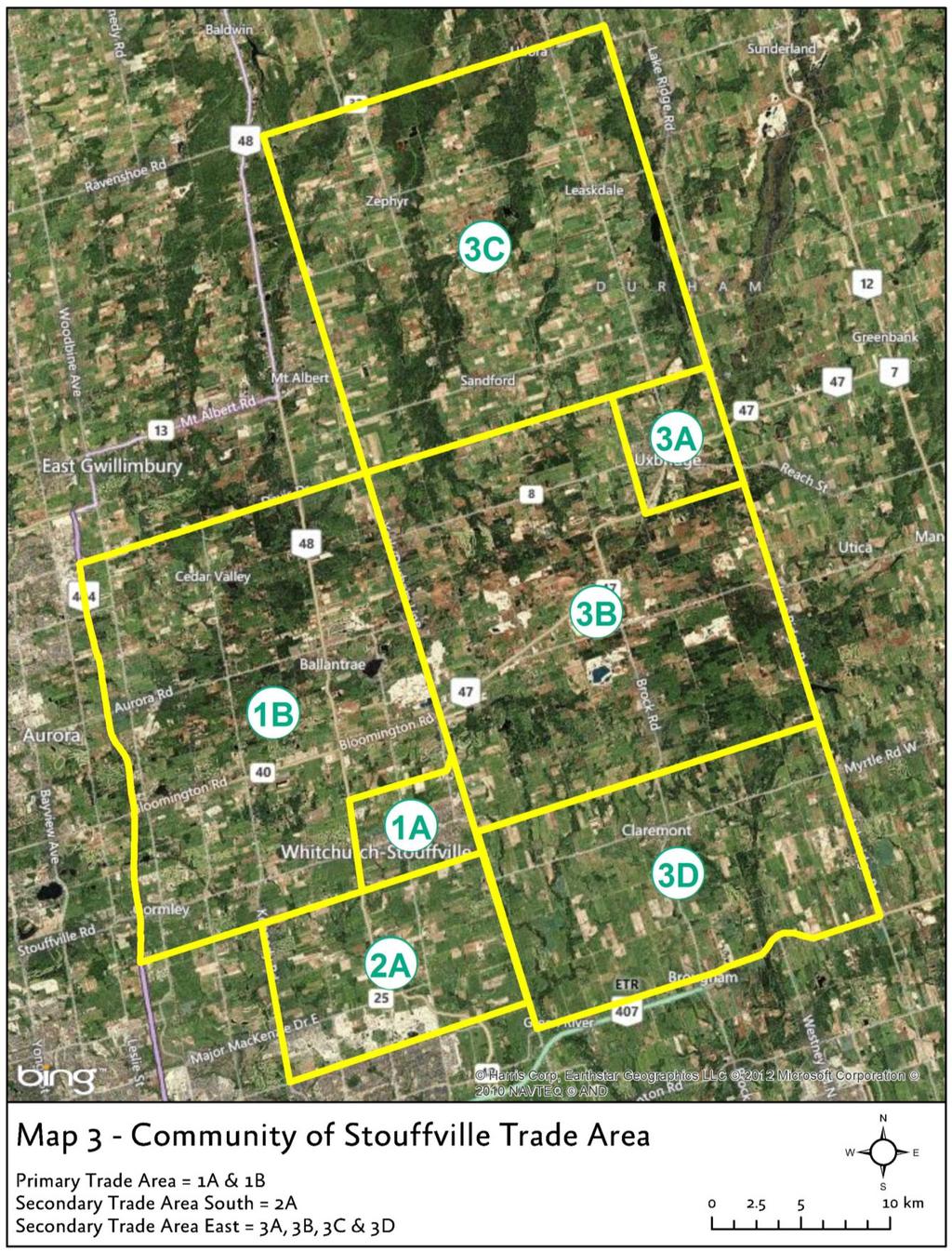

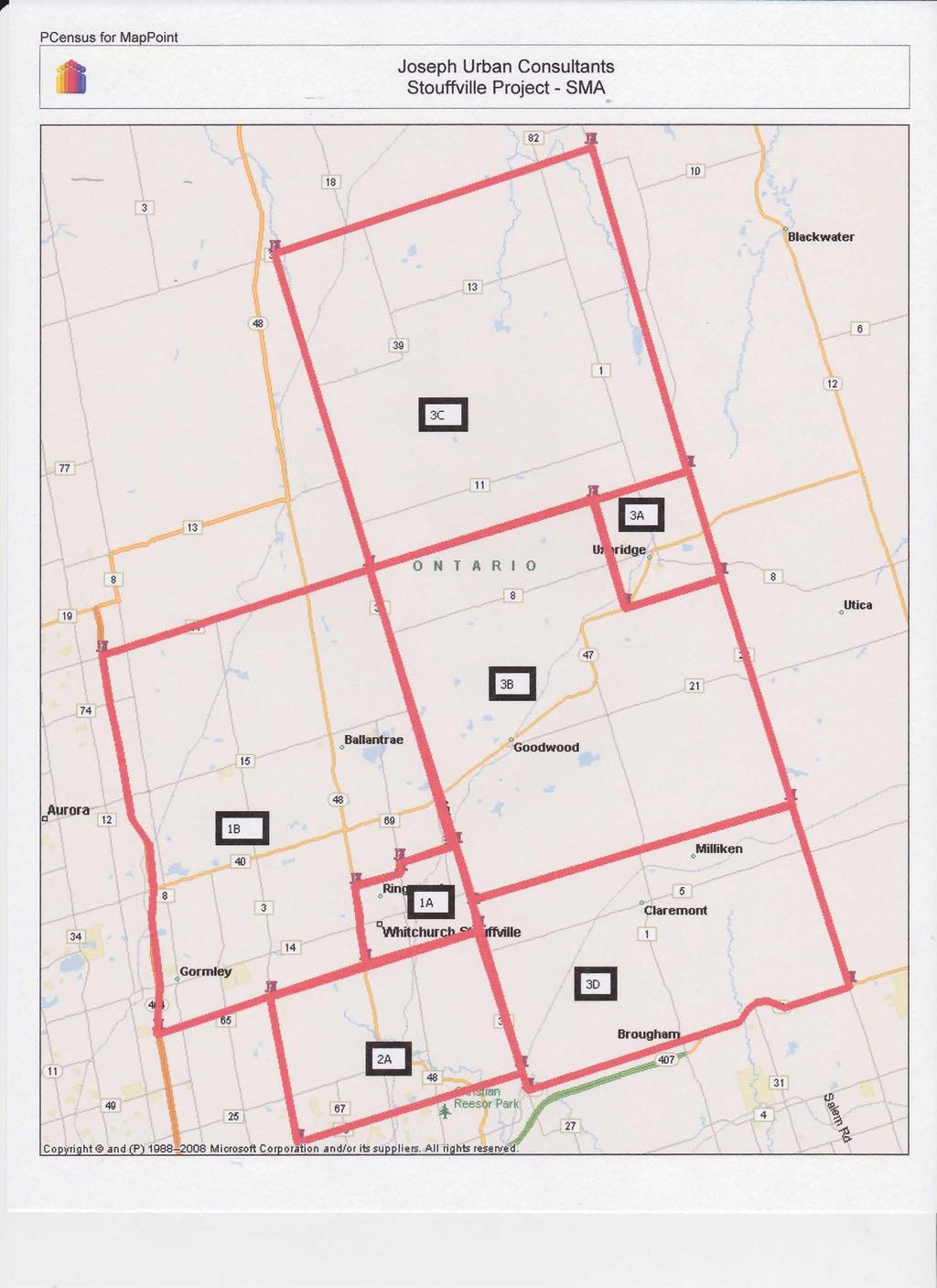

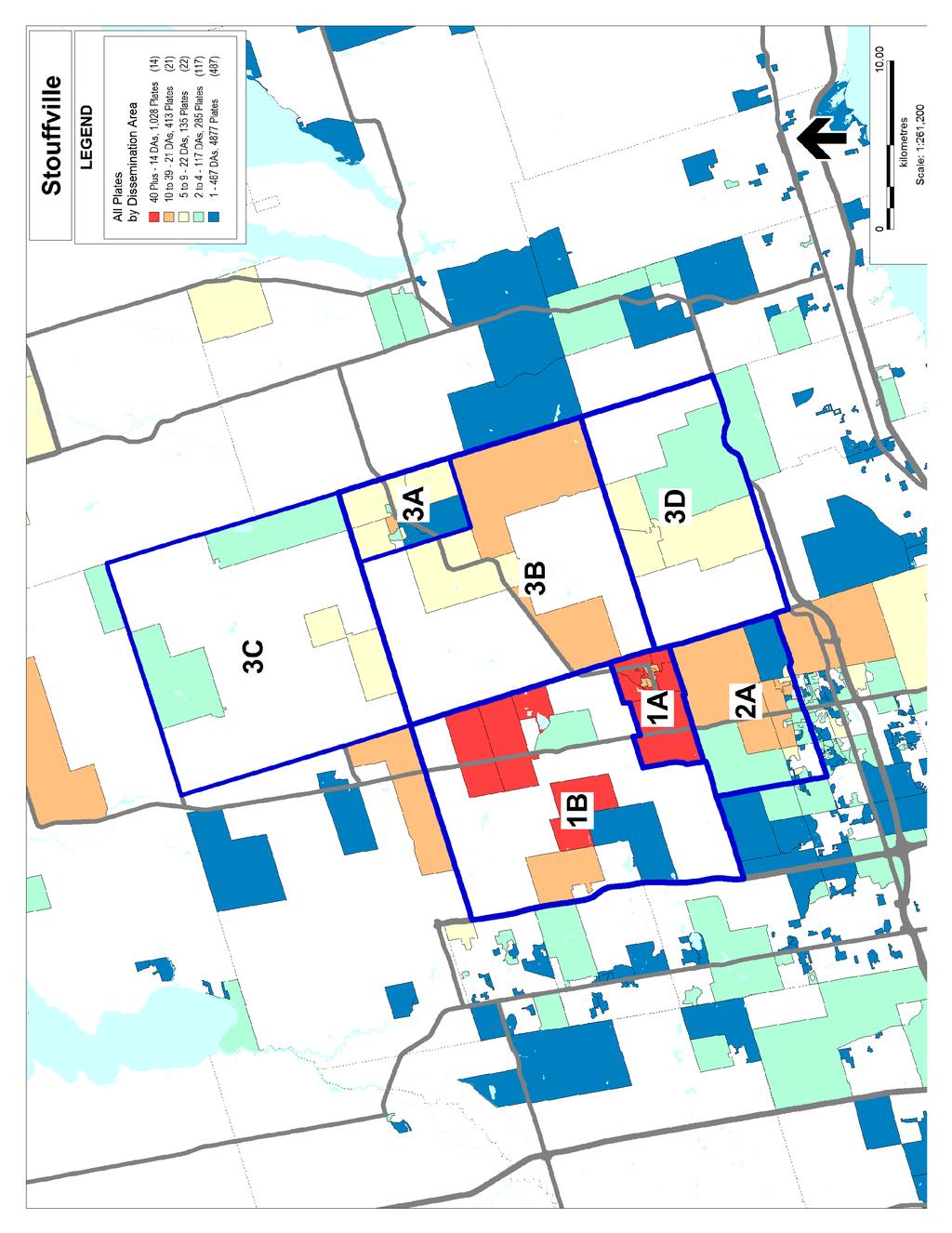

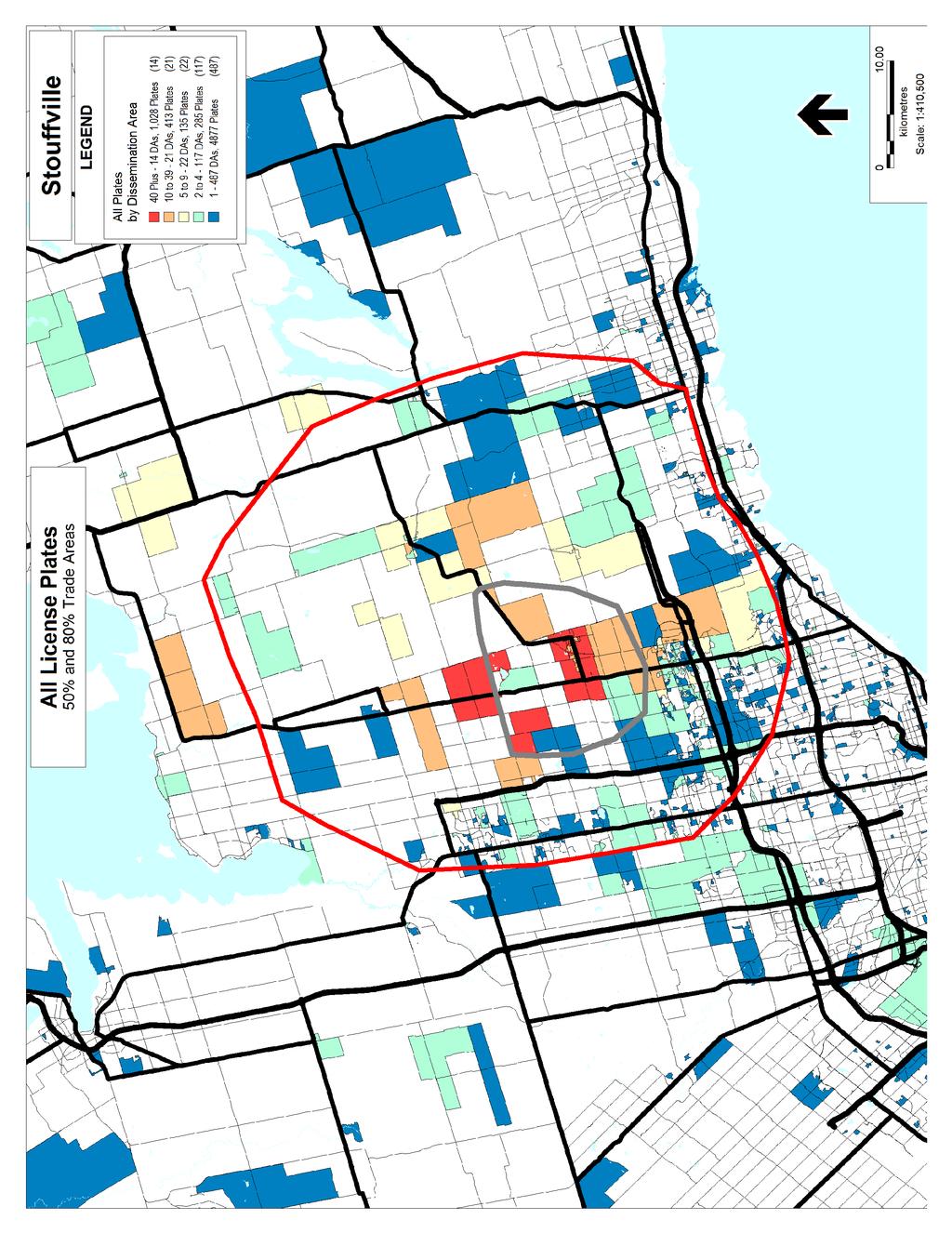

5 Community of Stouffville Commercial Policy Study Update Background and Analysis Report 4. How does the Update relate to the 2005 Commercial Policy Study? The 2005 Commercial Policy Study took the form of a peer review by the Town s consultants of market studies submitted by proponents of two major commercial developments. Those market studies were carried out by Malone Given Parsons Ltd. and urbanmetrics inc. The 2005 review resulted in the establishment of a new regional commercial designation at Hoover Park Drive and Highway 48 (Hoover Park Town Centre), and policies that would protect and preserve commercial development opportunities in the Community Core Area (Downtown Stouffville) and the Western Approach Area (see Maps 1 & 2). In addition, a Neighbourhood Retail Area to permit the development of a node of neighbourhood focused commercial activity was identified on the eastern side of the Community. The updated market projections underlying the current Study Update found in Appendix I to this report, repeat the empirical research undertaken in 2005 by Malone Given Parsons Ltd. (MGP). MGP tested a trade area for the Community of Stouffville that included Whitchurch-Stouffville as the Primary Trade Area and secondary zones in Northeast Markham (Secondary Trade Area South) and Uxbridge/North Pickering (Secondary Zone East) (see Map 3). The updated empirical research includes licence plate surveys that confirm the previously defined trade area, and a consumer telephone survey within those same trade area boundaries. An updated floor space inventory has also been compiled. 5. What are the components of the Community of Stouffville s Existing Retail Commercial Hierarchy? 5.1 Existing Hierarchy The commercial hierarchy is spread over three key nodes - the Downtown, the Western Approach Area, and the Hoover Park Town Centre power centre. There is also a Neighbourhood Retail Area on the eastern side of the Community (See Map 2). These nodes are differentiated by function, separated by distance, yet distributed to facilitate cross-shopping and outflow reduction. 3

6 Community of Stouffville Commercial Policy Study Update Background and Analysis Report 4

7 Community of Stouffville Commercial Policy Study Update Background and Analysis Report 5

8 Community of Stouffville Commercial Policy Study Update Background and Analysis Report 6

has about 150,000 square feet of remaining development potential.")

9 Community of Stouffville Commercial Policy Study Update Background and Analysis Report With respect to significant new commercial development potential within the existing designations: Hoover Park Town Centre (Regional Retail Area) has about 150,000 square feet of remaining development potential. Hoover Park Town Centre Photo Credit: Google Streetview April 2009 The Western Approach Area includes the former Anderson Haulage site (now Minto/Trinity) 1 which has zoning approvals for about 70,000 square feet of commercial space, as well as 12,190 square feet of commercial space as part of a mixed use development. Western Approach Area and Anderson Haulage Site Photo Credit: Google Streetview April 2009 The Western Approach Area also has a number of other sites which have over 100,000 square feet of commercial development potential including the vacant former Canadian Tire site (about 2 acres on the south side of Main Street at Winona where the former 19,000 square foot facility has been razed), Houston Motors auto dealership (about 4 acres), and the Town s Works Yard (about 4.75 acres). 1 Note: Previously this site was zoned to permit a total gross floor area between 17,000 and 30,657 square metres (182, ,000 square feet) of commercial space. Town Council adopted a zoning by-law amendment which reduced the amount of commercial space to 6,425 square metres (70,000 square feet) on September 4, In addition, a mixed commercial residential development is proposed which includes 1,133 square metres (12,190 square feet) of commercial space. 7

has small lot potential")

10 Community of Stouffville Commercial Policy Study Update Background and Analysis Report Former Canadian Tire Site in Western Approach Area - Photo Credit: Google Streetview June 2009 The Gateway Mixed Use Area (Ringwood area) has small lot potential for restaurants, boutiques, and offices, notwithstanding flood plain, environmental, access and property fragmentation constraints. Ringwood Mixed Used Area Photo Credit: Google Streetview April 2009 The Stouffville Country Market in the east end has a protected allocation of 125,000 square feet, and there is some remaining potential for additional development in the Neighbourhood Commercial Area designation which applies to the Market site. Stouffville Country Market Photo Credit: Google Streetview April

.")

11 5.2 Stouffville s Closest Competition Community of Stouffville Commercial Policy Study Update Background and Analysis Report The Community of Stouffville s closest retail commercial competition is found in Markham at the Metrus and former Emerson Electric sites a little more than 3 miles to the south of the Town boundary (see Map 4). These power centres have attracted a limited number of anchor stores, but have a range of banking and small store permissions. 9

12 Community of Stouffville Commercial Policy Study Update Background and Analysis Report 6. How adequate is the supply of lands set aside for commercial purposes? There has been an increase in the amount of retail commercial space in the Community of Stouffville since The 2005 inventory in the Community of Stouffville identified approximately 475,000 square feet of retail commercial space. In comparison to the 2005 inventory, the current study s 2012 inventory in the Community of Stouffville consists of approximately 900,000 square feet of retail commercial space as illustrated in Figure 1. However, the differences between the 2005 and 2012 inventory in part reflect the fact that non-retail space (personal and other services, bank, and Liquor/beer/wine space) were tallied only in the Downtown area in Excluding the non-retail categories, the greatest square footage gains have been in the Department Store and Non-Department Store Non-Food Store Retail (NFSR) categories. In addition, vacant space has declined significantly. The Supermarket/Grocery category has changed modestly as a result of Wal-mart s food component replacing the Sobey s closure. Overall, the retail inventory, including vacant space, has increased by over 235,000 square feet since The inventory indicates that with respect to existing development, vacancies now make up less than 1% of existing retail commercial space -- well below the normal range of 5% to 7% typical of most markets. This low vacancy rate appears to point to the relative good health of the retail commercial hierarchy, and the generally productive performance levels of existing space (i.e. sales per square foot)would appear to suggest that the market is under-stored. 10

13 Community of Stouffville Commercial Policy Study Update Background and Analysis Report Figure Floorspace Inventory (Total: 910,120 ft 2 ) *Includes 27,000 square feet of supermarket-equivalent space in Walmart Other Space NEC, 26,908sf, 3.0% Liquor/Beer/Wine, 13,770sf, 1.5% Vacancy, 4,000sf, 0.4% Bank/Trust, 24,215sf, 2.7% Supermarket/ Grocery *, 103,911sf, 11.4% Specialty Food, 21,900sf, 2.4% Restaurants, 117,747sf, 12.9% Other Services, 59,232sf, 6.5% Dep't Store (nonfood), 135,600sf, 14.9% Professional Services, 45,240sf, 5.0% Personal Services, 37,670sf, 4.1% HI, 26,860sf, 3.0% Non-Dep t Store, 293,067sf, 32.2% As a result of these significant inventory changes, the retail market shares obtained in the 2005 consumer telephone survey have also changed significantly. The current supply of vacant commercially designated lands, including the remaining 150,000 square feet at Hoover Park Town Centre and the 82,000 square feet of commercial development approved on the former Anderson Haulage lands in the Western Approach, would appear to exceed demands until 2021 based on the projections of residual market demands for retail and selected commercial uses found in Appendix I to this report. However, by 2031 there would appear to be a supply deficit of approximately 14 acres (150,000 square feet at 25% coverage), recognizing that market projections beyond five years cannot be regarded as conclusive. 11

14 Community of Stouffville Commercial Policy Study Update Background and Analysis Report 7. Who is shopping in the Community of Stouffville and what are they shopping for? The licence plate survey and the consumer survey confirm that the Community of Stouffville continues to draw customers (post-power centre) from the same trade area defined by the 2005 study (pre-power centre). The Hoover Park Town Centre attracts the highest level of inflow (40%) followed by the Downtown (35%), followed by the Western Approach Area (30%). These inflow levels are higher than those obtained in the 2005 MGP study. This appears to indicate that the expansion of the commercial hierarchy to include the regional node (Hoover Park Town Centre) has been beneficial to the Community of Stouffville as a whole with respect to inflow. However, high local capture rates from Primary Trade Area residents of more than 60% are confined to generally lower order goods (with some exceptions). These high capture rates are also found primarily at the anchor stores at Hoover Park Town Centre. For example, although the average department store capture is 56.7%, Wal-Mart s local capture is 94.4% of the Primary Trade Area residents spending in all Wal-Mart stores. Significant merchandising gaps are evident where local capture rates from Primary Trade Area residents are low or negligible (i.e. less than 40%), primarily for medium to higher order comparison goods shopping categories. These include: most fashion categories; certain specialty retail categories including books, camera/photo supply, gifts/novelty, hobby/toy/craft, art supply/gallery, fabric/yarn and musical instruments; certain home furnishings and interior décor categories including furniture/appliances, TV/electronics/computer, bath/bedding/linen, lighting/carpet/other décor and antiques; and, home improvement. This indicates that the Community still has a large outflow of dollars. It also suggests understoring and the need for the Community of Stouffville to attract certain types of new retail stores to catch up with population growth. Past gains in local capture rates have come through the attraction of new anchor stores at the Hoover Park Town Centre. Future gains may be a combination of attracting anchor and non-anchor specialty stores in the weaker categories. The findings indicate that Stouffville retailers have good opportunities for increased sales from both the Primary and Secondary Trade Areas. 12

15 Community of Stouffville Commercial Policy Study Update Background and Analysis Report Some suggested opportunities (see Figure 2) include: Small department store in the medium term such as a Marshall s; Regional chain store anchor use such as a TSC in the medium term; New format drug store in the medium term; Fashion and accessory space in the short to medium term; A small infusion of home furnishings space; and, Electronics and computer space in the short term. Figure 2: Local Capture Rates by Stouffville Stores 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Supermarket Specialty Food Department Store General Merchandise Home and Auto Supply (HAAS) (Canadian Tire / TSC Store) Tires, Batteries, Accessories /Automotive Specialty Store Men s & Ladies Wear Family Wear / Unisex Children s Wear Shoes Jewellery Clothing Accessories Luggage & Leather Goods Stationery / Office Supply Book Store / News Dealer Record / CD / Tape Camera / Photo Supply Gift / Novelty / Greeting Card / Party Supply Sporting Goods Hobby / Toy / Craft Art Gallery & Artist Supply Musical Instruments Pet / Pet Supply Fabric or Yarn Shop Florist Drug / Discount Drug Furniture & Appliances TV / Stereo / Electronics / Computer Lighting / Carpet / Other Interior Décor China / Glassware / Kitchenware / Cutlery Bath / Bedding / Linen Telephone/Cell Phone/Vacuum/Sewing Machine Antiques Home Improvement / Lumber / Building Supply Hardware/Paint/Paper/Glass/Electrical/Plumbing Nursery / Garden Centre Primary Trade Area Secondary Trade Area South Secondary Trade Area East 13

16 Community of Stouffville Commercial Policy Study Update Background and Analysis Report 8. Market Study Conclusions The purpose of this commercial study update is to investigate whether the existing commercial policies are succeeding in achieving a balanced yet maturing commercial hierarchy. The maturation process involves filling out the remaining development capacity at the Hoover Park Town Centre and the Western Approach Area with medium to higherorder retail uses, and the development of the Gateway Mixed Use Area designation at Highway 48 and Main Street. The rate of maturation of the commercial hierarchy is a consideration in policy terms and at play in economic terms. The general conclusion of the analysis is that, in market terms, the commercial policies are succeeding, but slowly based on the following indicators: In a slowing retail development environment, Stouffville continues to serve a consistent trade area with a shift to increased regional draws. Placed in an overall economic context, the retail commercial development market in the GTA has been in general malaise (inconsistent/mushy) for some time. Even before the effects of the 2008 economic contraction, there were signs that the retail development industry was slowing, as was evident in longstanding power centre approvals in high growth markets not being built out in a timely manner. While caught up in that economic context, the results of this current analysis indicates that the Community of Stouffville continues to serve a consistent trade area, but with a shift to increased regional draws. Current market shares obtained by Stouffville retailers are drawn mostly from the Community of Stouffville, supplemented by moderate yet consistent support coming from Stouffville s secondary market areas. Increased regional draws are generally specific to the Hoover Park Town Centre, but are shared by the other commercial nodes to a much lesser degree. Regional draws have improved since the regional centre (Hoover Park Town Centre) began development. This is primarily due to the draws of the new anchor stores. However, new smaller-scale non-anchor space has not shared a similar expansion in other parts of the community, particularly in the Western Approach Area, notwithstanding the increased regional draws and inflow that the new anchor stores have brought into the local market. 14

17 Community of Stouffville Commercial Policy Study Update Background and Analysis Report The retail commercial hierarchy is in relative good heath with a low vacancy rate and productive performance levels of existing space, but this is off-set by significant merchandising gaps. The low vacancy rate appears to point to the relative good health of the retail commercial hierarchy. This, together with the generally productive performance levels of the existing space (i.e. good sales per square foot), suggest that the market is understored. This is coincidental with the fact that significant merchandising gaps are evident primarily for medium to higher order comparison goods shopping categories such as most fashion categories, and electronics and computer goods. Despite the merchandising gaps, the current under-storing, and today s low vacancy rates, the analysis does not identify a significant supply deficit until after 2021 (by 2026 and 2031). At the macro level, the supply of vacant commercially designated lands, including the 82,000 square feet of commercial development currently approved on the former Anderson Haulage lands in the Western Approach, would be sufficient to meet market demands until 2021 when the market would be in relative equilibrium. By 2026 a supply deficit of approximately 10.5 acres (rounded) would emerge. At 25% coverage, this supply surplus would translate into 115,000 square feet. By 2031, the supply deficit would approximate 14 acres, which at 25% coverage would translate into 150,000 square feet. Therefore, it can be concluded that the 2005 Commercial Policy Update which resulted in the creation of the regional node, and the efforts the Town has made in support of the Downtown, appear to have created a generally healthy commercial hierarchy. The support for the Downtown has resulted in a stronger centre, while the addition of the regional node has significantly reduced the outflow for lower order goods. At the same time, there are a number of factors at play which affect the rate of maturation, and are evidenced in the difficulty in leasing out space at Hoover Park Town Centre, and the lack of interest in development of major potential commercial sites in the Western Approach Area. Some of the factors affecting the rate of maturation of the commercial hierarchy include population growth and policy controls on the regional node and the Western Approach. Other factors are those affecting developers and tenants including: 15

18 Community of Stouffville Commercial Policy Study Update Background and Analysis Report current leasing competition between developers (e.g. Hoover Park Town Centre versus Emerson Electric/Metrus in Markham); previous and prospective leasing deals with tenants (e.g. rental trade-offs depending on the strength of individual markets); tenant fears of cannibalizing the sales of their existing stores in proximate markets; tenant concerns over the rate of local population growth in smaller markets; tenant reluctance to commit to riskier development models (e.g. mixed use buildings) in smaller markets; and, lack of tenants appropriate for the market (e.g. new-format tenants are already in the market, few U.S. entry prospects, limited second store options). Other less tangible factors may affect consumers. For example, residents new to the Community of Stouffville might still have ties to other locales because they work in other communities or still go to their current doctors or dentists or other special services outside of Stouffville and continue to shop outside Stouffville as well. In addition, the lack of interest in development in the Western Approach Area may also reflect a lack of perceived identity for the Western Approach Area. The recent application for a reduction in the amount of commercial space on the former Anderson Haulage site in the Western Approach Area was a result of a lack of anchor tenant interest. This may reflect the fact that, despite the strong policy direction in the Secondary Plan, the Western Approach Area is not perceived by retailers to have a retail commercial identity similar to the regional node and the Downtown. This factor may also be explain why no proposals have come forward for other significant sites in this Area including the vacant former Canadian Tire lands at 9 th and Main, the Houston Motors site, or the Town s Works Yard site. The lack of development in the Gateway Mixed Use Area designation at Highway 48 and Main Street because of a range of constraints (e.g. floodplain, property fragmentation) may also be a consideration. This area would serve as the entrance to the Western Approach Area, and the lack of a gateway and related exposure on Highway 48 contributes to a lack of identity in the Western Approach Area. In summary, despite the apparent slow maturation of the commercial hierarchy in the Community of Stouffville, the hierarchy is serving a high income area with good population growth prospects. However, the Community of Stouffville must contend with market issues that affect longer term market projections to Therefore, while a supply deficit has been identified post 2021 which is projected to increase to 150,000 square feet by 2031, consideration has to be given to these market issues in determining whether there is an actual need to designate additional commercial space to replace the reduced supply at the 16

19 Community of Stouffville Commercial Policy Study Update Background and Analysis Report current time. This is particularly the case as market projections beyond five years cannot be regarded as conclusive. Given the uncertainties in the market, consideration should be given as to whether it would be premature to designate additional lands for commercial development at the current time which might put at risk the achievement of the planned function of the current three nodes and the Neighbourhood Retail Area. Based on the available information, it may be preferable to continue to monitor the situation and to encourage commercial intensification in the Downtown and Western Approach Area (i.e. through continued implementation of the Downtown Community Improvement Plan and support for investments in transit supportive mixed-use / multi storey, higher density intensification, infill, development / redevelopment, and expansion / relocation); and to work with Hoover Park Town Centre to encourage the completion of that development. In particular, consideration needs to be given to assessing how to better position the Western Approach Area in the market to capitalize on the identified merchandising gaps. The longer term strategy should seek to achieve a market equilibrium position (neither under-stored nor over-stored) through incremental expansion in line with emerging market opportunities, most notably through the market absorption of the remaining lands at the Hoover Park Town Centre; through the market absorption of other vacant commercially designated lands or other suitable lands (e.g. the Town s Works Yard); and through other intensification along the commercial corridor in the Western Approach Area and in the Downtown. 17

20 Community of Stouffville Commercial Policy Study Update Background and Analysis Report 9. Implications for the Current Commercial Planning Policy Framework The Community of Stouffville Secondary Plan which is found in Section 12 of the Town s Official Plan establishes the policy framework for commercial development in the Community of Stouffville. The key current commercial policy directions are outlined below together with questions/directions for consideration in the context of the current update of the market study findings: Downtown Policy Direction: Maintain the downtown as a central meeting place and shopping area for the community recognizing its important contribution to the character of the community. Discussion The maintenance and enhancement of the Downtown as a shopping area is a key direction throughout the Plan found in the Community Vision, as well as the land use and design policies. The market study results appear to indicate that the policy framework and the efforts of the Town and the business community to implement the directions in the Plan have been successful. However, past experience in the community and elsewhere indicates that the maintenance of that success can be a challenge. At the same time, the role of the Downtown as a shopping area continues to be important to implement a key part of the Community Vision. Questions/Future Directions Are the current policy directions with respect to the Downtown which provide for its protection and enhancement sufficient to ensure its continued success as a shopping area for the community? Regional Retail Centre (Hoover Park Town Centre) Policy Direction: Major retail uses may be permissible in a manner that is complementary to, and does not undermine, the function of the Western Approach Area, the Core Area, or the Neighbourhood Retail Area. Discussion The policies for the Regional Retail Center found in Section A of the Plan, establish minimum floor areas for large retail stores to assist in ensuring that the 18

21 Community of Stouffville Commercial Policy Study Update Background and Analysis Report development in this area fulfills its function which is to act as a trade centre and specialty retailing node serving a broad regional market. The policies are also designed to ensure that uses which could undermine the planned function of other commercial areas are not permitted or are limited in size. These policies prohibit: large retail stores that are under 371 square metres in gross floor area; recreational vehicle sales and service; financial institutions until such time as an office building with a minimum gross floor area of 4,460 square metres and a height of a minimum of three storeys is constructed; liquor and/or beer retail stores and outlets; food supermarkets, food stores or grocery stores except that the sale of groceries or similar food or retail products is permitted in a portion of a large retail store where the store has a minimum gross floor area of 10,000 square metres and no more than 2,500 square metres gross floor area of the store is devoted to the sale of groceries or similar food or retail products. In addition, the policies require a minimum of two retail operations having a minimum commercial floor area of 10,000 square metres and 5,575 square metres respectively. Further, personal service establishments are permitted provided they have a gross floor area of not less than 92 square metres; and eating establishments are permitted provided that they do not exceed an aggregate gross floor area of 2,370 square metres. Questions/Future Directions Is a minimum size of 371 square metres (4,000 square feet) for large retail stores still appropriate? Are financial institutions still important anchors for the Downtown and Western Approach Area? Should such uses still continue to be prohibited in the Regional Retail Centre until an office building is located in the area? Are liquor and beer retail stores and outlets still important anchors for the Downtown and Western Approach Area? Should such uses still continue to be prohibited in the Regional Retail Centre? Can exceptions be made for small outlets which form part of a larger store? Are food supermarkets, food stores and grocery stores still important anchors for the Downtown and Western Approach Area? Should such uses still continue to be prohibited in the Regional Retail Centre? Can additional 19

22 Community of Stouffville Commercial Policy Study Update Background and Analysis Report exceptions be made similar to the 2,500 square metres of floor area permitted in a store over 10,000 square metres? Can personal service establishments of less than 92 square metres be permitted in the Regional Retail Centre? Are restaurants still important anchors in the Downtown and Western Approach Area? Should additional restaurants be permitted in the Regional Retail Centre above the current 2,730 square metre cap? Western Approach Area The intent for the Western Approach Area is to create a diverse, thriving commercial district combined with a range of uses including employment, entertainment and residential uses. Discussion The Western Approach Area includes the Western Approach Mixed Use and the Western Approach Commercial designations. The general policy direction is the same with a focus on mixed use development, and strong policy direction with respect to urban design. However, the permitted uses are slightly broader in the Mixed Use Area including data processing, education and training, medium density residential and automotive campus, while the Commercial designation is more focused on commercial uses. Questions/Future Directions What additional or refined policy direction is required to encourage redevelopment of the major vacant sites in the Western Approach Area? Would combining the two existing land use designations which are similar assist in creating a clearer identity for the area? What other additional or refined policy direction would assist in clarifying identity of this area and its role in the community? Gateway Mixed Use Area The policy direction for this area is the creation of a unique and special mixed use district which promotes commercial development integrated with residential uses. Special architectural and landscaping treatment is required to strengthen the area s identity and improve the quality of the public realm. 20

23 Community of Stouffville Commercial Policy Study Update Background and Analysis Report Discussion The lack of development in the Gateway Mixed Use Area designation at Highway 48 and Main Street because of a range of constraints (e.g. floodplain, property fragmentation) is an issue given that this is the main entrance to the community from Highway 48. Further, this area also serves as the entrance to the Western Approach Area. The lack of a gateway and related exposure on Highway 48 may contribute to a lack of identity in the Western Approach Area. Questions/Future Directions Is the lack of development in this area and the lack of an established gateway to the community in this location hindering development in the Western Approach area and contributing to its lack of identity? What additional or refined policy direction or other action by the Town is required to resolve the constraints to development in this area? Would a detailed tertiary plan which includes a detailed approach for addressing constraints to development assist in resolving the situation? Should a Community Improvement Plan be considered to assist in the redevelopment of this area? Neighbourhood Retail Area The Neighbourhood Retail Area designation currently applies only to a site on the east side of 10 th Line north of Main Street, although the policies recognize the potential for the designation of additional areas. The planned function is as a commercial district which provides a range of goods and services designed to meet the day to day requirements of the area residential neighbourhoods. Mixed use is promoted as part of this designation. Discussion The lands in the Neighbourhood Retail Area designation are currently utilized for the Stouffville Country Market. It is unclear when or if redevelopment will occur. At the same time, commercial development has occurred at the intersection of the 10 th Line and Main Street particularly in the northeast quadrant which provides some of the services intended for the Neighbourhood Retail Area. However, the Town is currently carrying out a Growth Management Strategy to evaluate the need for additional growth 21

24 Community of Stouffville Commercial Policy Study Update Background and Analysis Report in Phase 3 of the Coummunity of Stouffville. If additional growth is approved, the subject site will be more centrally located to the expanded urban area and its potential for redevelopment may increase. Questions/Future Directions Should the lands at Main Street and 10 th Line or other sites be recognized as a Neighbourhood Retail Area? What is the potential for the development of the current Neighbourhood Retail Area considering future development of Phase 3 of the Community of Stouffville? 22

25 APPENDIX I COMMUNITY OF STOUFFVILLE COMMERCIAL POLICY STUDY UPDATE PROJECTIONS OF RESIDUAL MARKET DEMANDS 2014, 2016, 2021, 2026, & 2031 RETAIL & SELECTED COMMERCIAL USES OCTOBER 2012 Acronyms: FSR: NFSR: GAFO: HAAS: TBA: HI: FIRE: SBM: GLA: NAICS: Food Store Retail Non-Food Store Retail General Merchandise / Apparel / Furnishings / Other Retail Home and Auto Supply Tires, Batteries & Accessories Home Improvement Finance / Insurance / Real Estate Services to Business Management Gross Leasable Area North American Industrial Classification System - 1 -

26 1. Introduction -- Planning and Market Study Context: The Town of Whitchurch-Stouffville is currently conducting an update of the Community of Stouffville Commercial Policy Study (Study Update). The Study Update is to assess the implications of growth to date on the commercial districts, and to examine commercial land use requirements through to the Year This comprehensive review will assess the adequacy of the supply of lands set aside for commercial purposes and recommend whether any revisions are required to land use designations and policies/zone standards to protect the planned function of each commercial area in the Community. The Study is being undertaken in the context of population forecasts (York Region, May 31, 2012) which indicate that current population levels in the Town of Whitchurch-Stouffville will increase by about 50% over the next 19 years ( ): up from to to 41,235 in the 2012 base year (Watson & Associates), 55,800 by 2021 (York Region), and 60,600 by 2031 (York Region) The Town last undertook such a commercial policy study in The 2005 study took the form of a peer review by the Town s consultants of market studies submitted by proponents of two major commercial developments. Those market studies were carried out by Malone Given Parsons Ltd. and urbanmetrics inc. The 2005 review resulted in the establishment of a new regional commercial designation at Hoover Park Drive and Highway 48 (Hoover Park Town Centre), and policies that would protect and preserve commercial development opportunities in the Community Core Area (Downtown Stouffville) and the Western Approach Area. In addition, a Neighbourhood Retail Area to permit the development of a node of neighbourhoodfocused commercial activity was identified on the eastern side of the Community (See Maps 1 & 2). The updated market projections underlying the current Commercial Policy Study Update repeat the empirical research undertaken in 2005 by Malone Given Parsons Ltd. (MGP). MGP tested a trade area for the Community of Stouffville that included Whitchurch-Stouffville as the Primary Trade Area and secondary zones in Northeast Markham (Secondary Trade Area South) and Uxbridge/North Pickering (Secondary Zone East) (see Map 3). The updated empirical research includes licence plate surveys that confirm the previously defined trade area, and a consumer telephone survey within those same trade area boundaries. An updated floor space inventory has also been compiled. The results of this research are summarized in the following sections

27 - 3 -

28 - 4 -

29 - 5 -

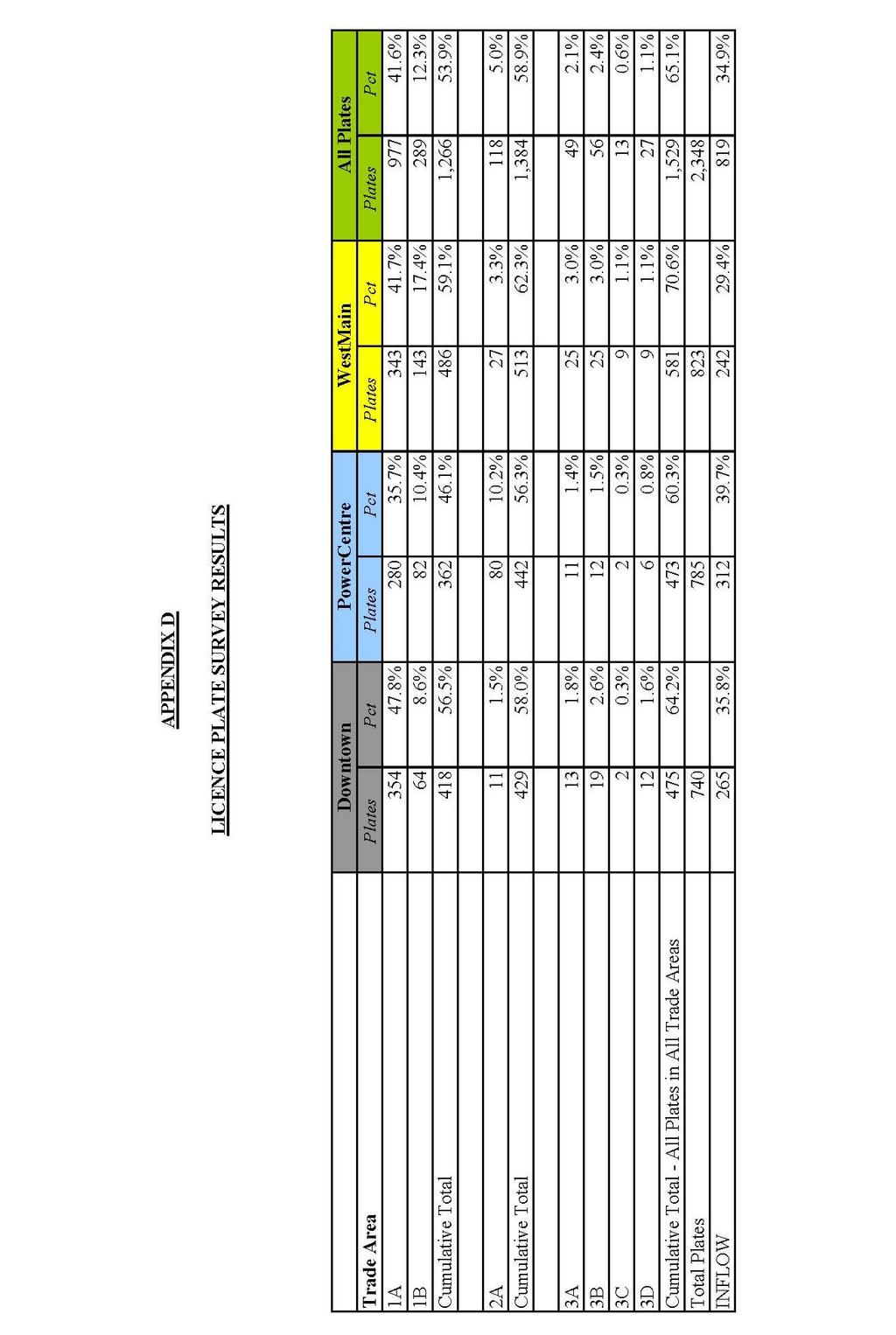

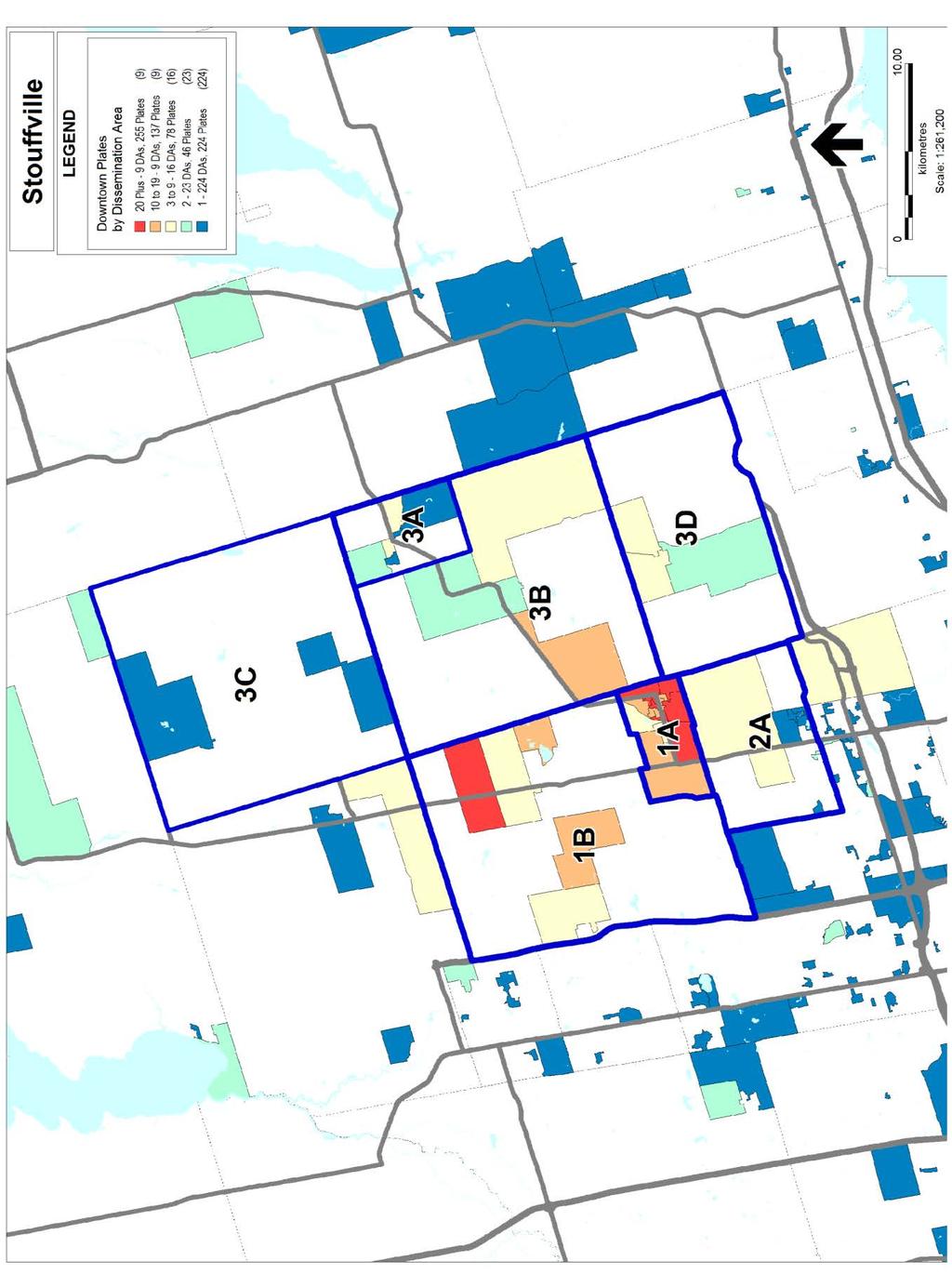

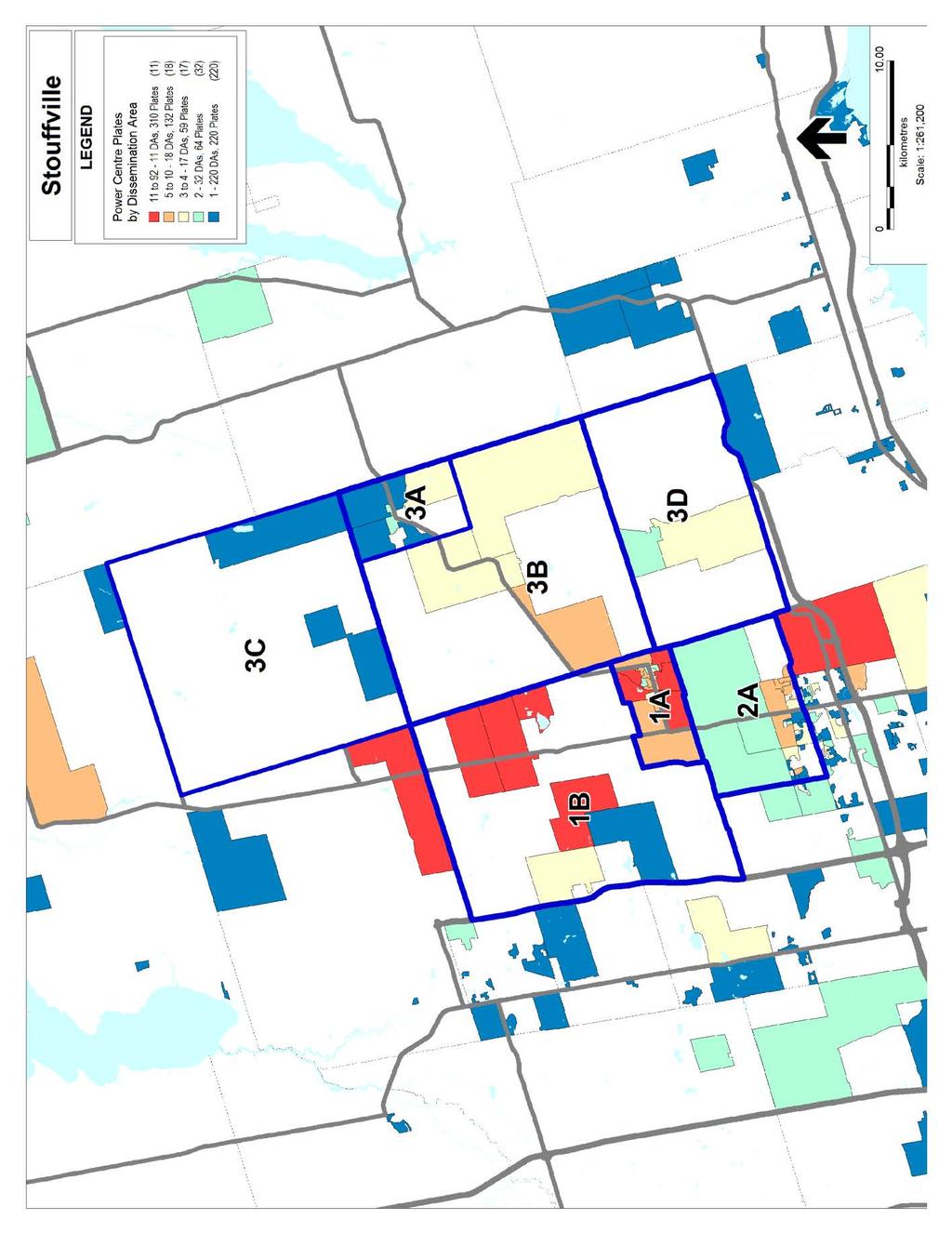

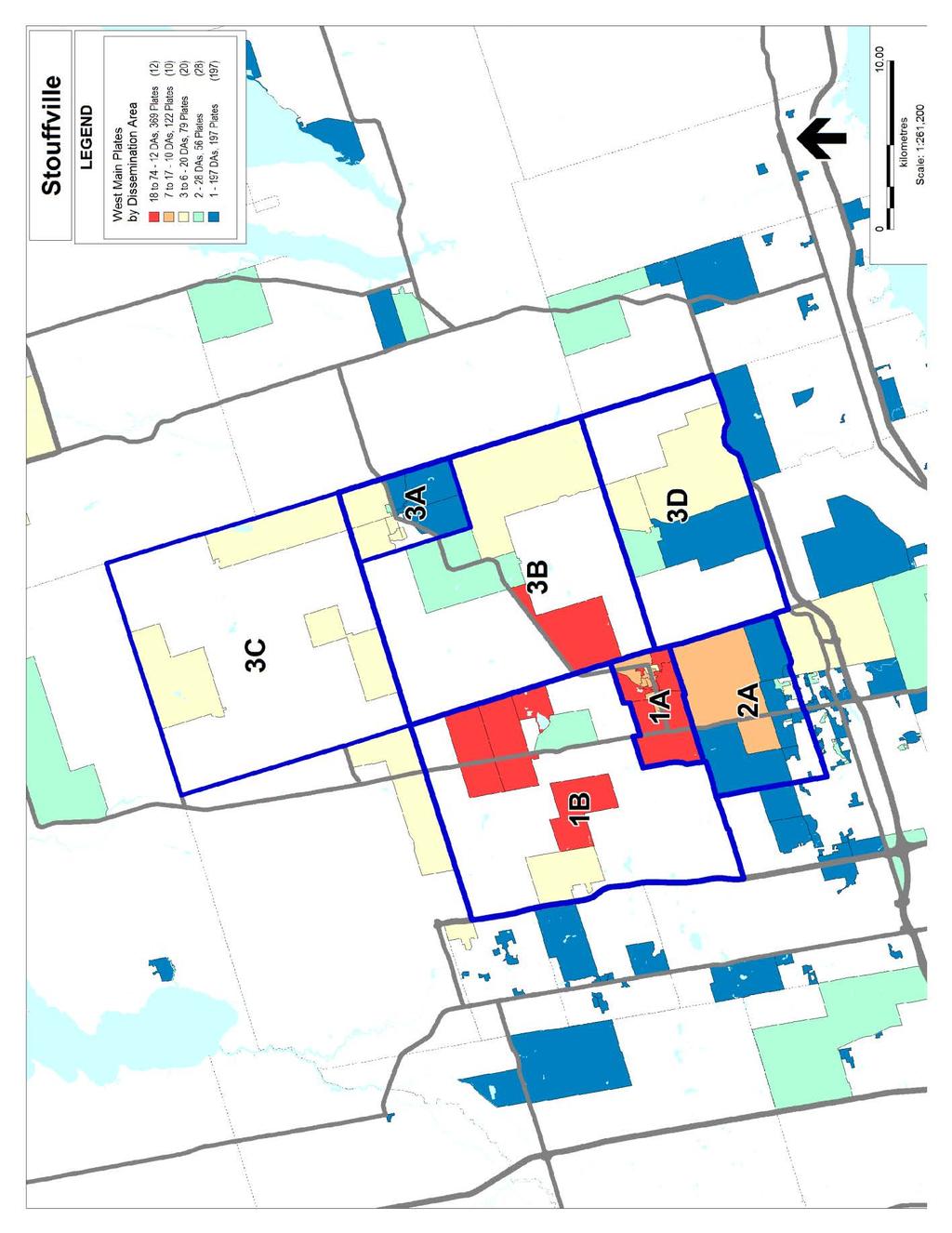

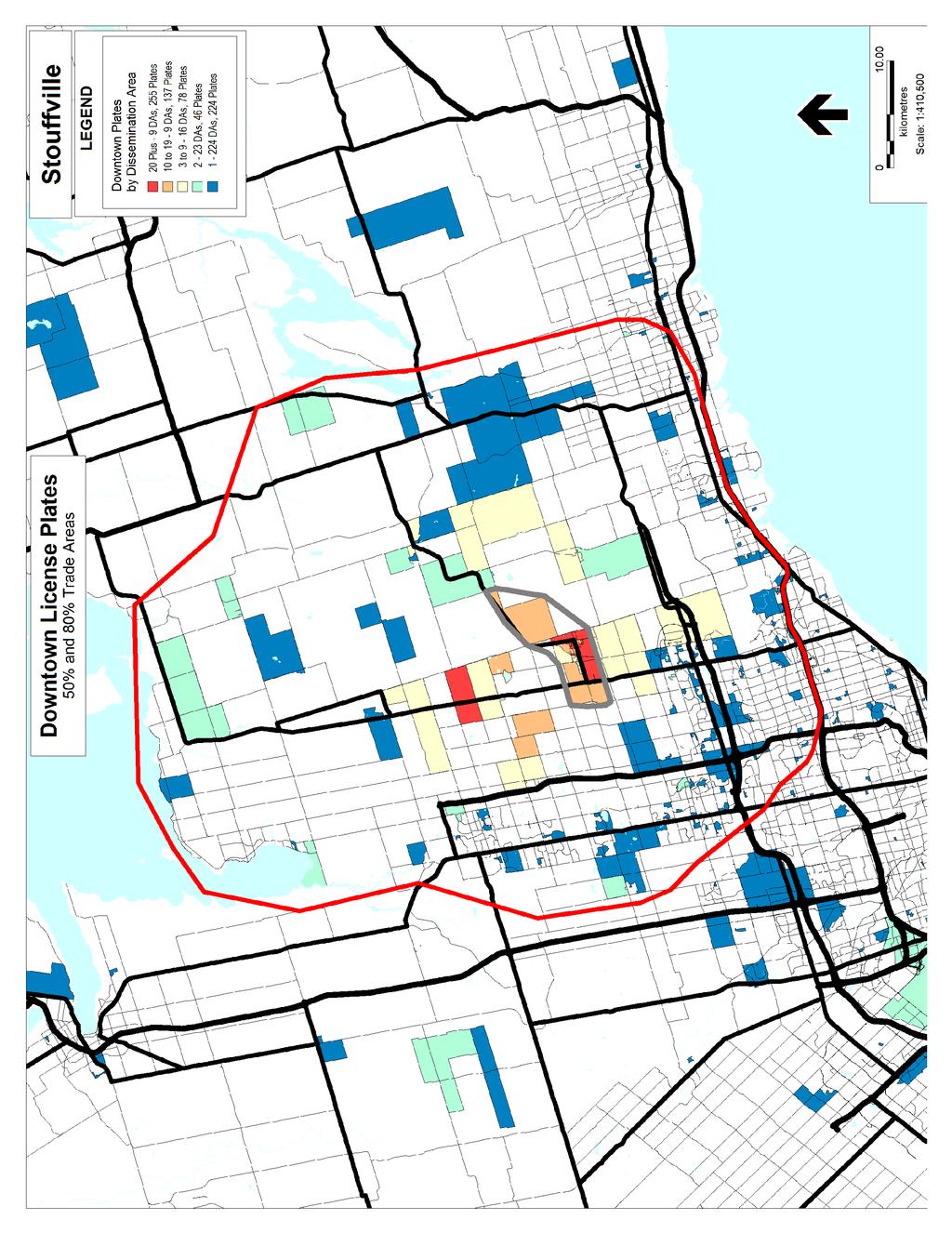

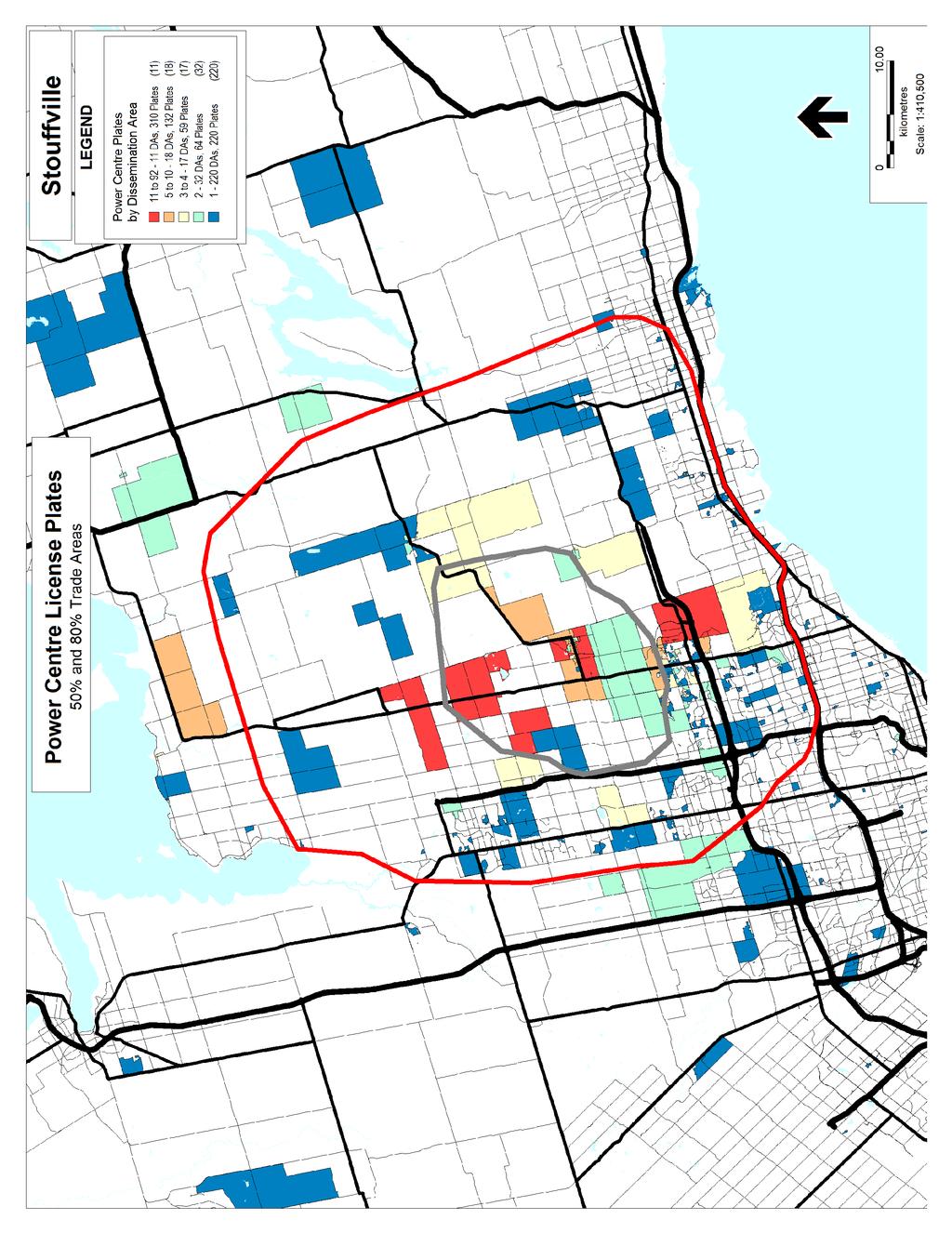

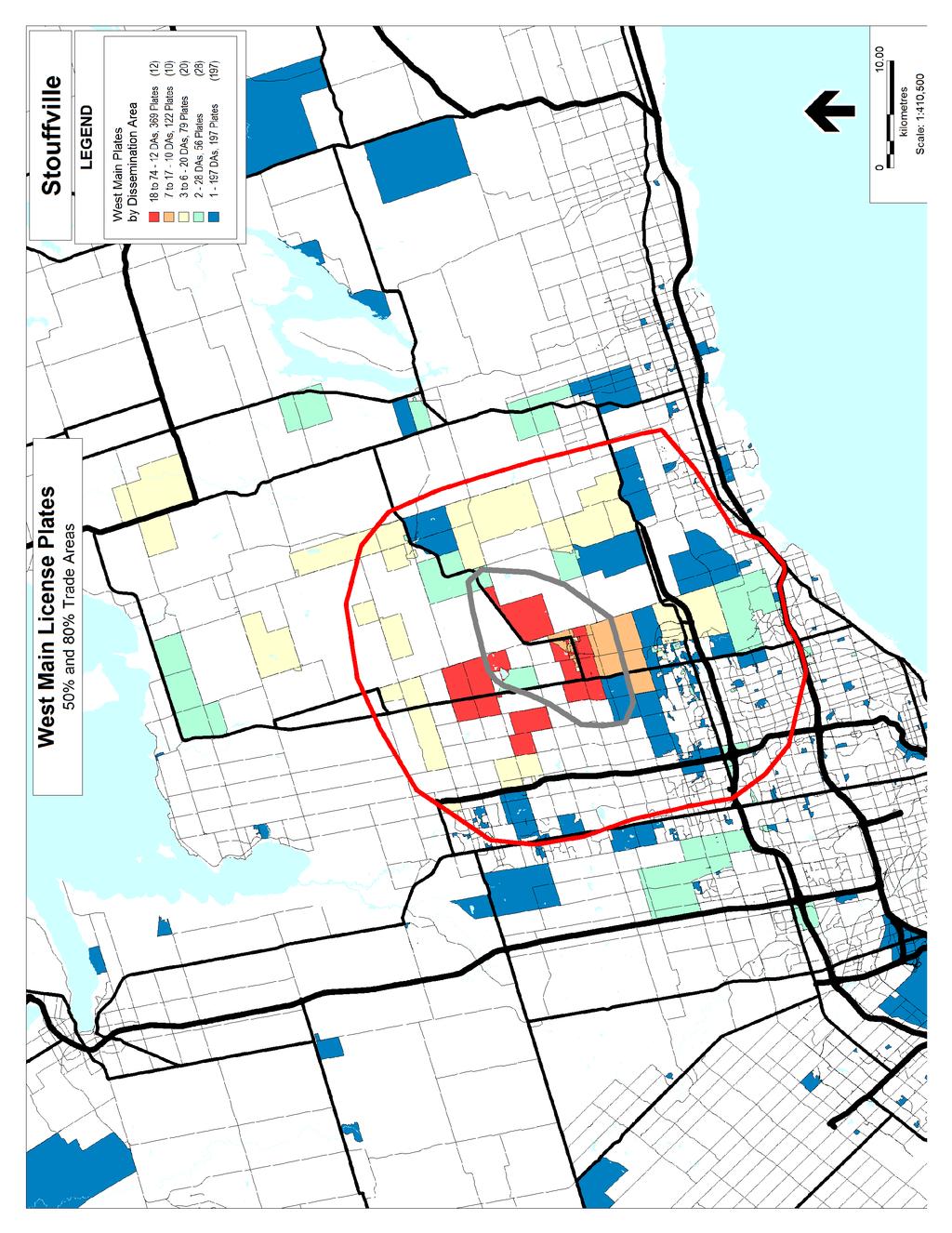

30 2. Licence Plate Surveys: Licence plate surveys (proxies for customer origins) were conducted by Corey F. Doyle, Research Consultant, on Thursday, Friday and Saturday, May 22, 23, and 24, The licence plate survey data (coded by the Ontario Ministry of Transportation, and compiled and mapped by GEOmarketing Solutions Inc.) are featured in Appendix D of the Study Update. The percentage of customer origins derived by the three existing commercial nodes is summarized in Figure 1 as follows 1 : Figure 1: 2012 Customer Origins by Existing Commercial Nodes 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 1A 1B 2A Downtown Power Centre Western Approach All Plates 3A 3B 3C 3D TRADE AREA INFLOW 1 Note: Tables on which Figures are based are found in Appendix E to the report

31 These data confirm that the Community of Stouffville continues to draw customers (postpower centre) from the same trade area defined by the 2005 MGP study (pre-power centre). The Hoover Park Town Centre attracts the highest level of inflow (40%) followed by the Downtown (35%), followed by the Western Approach Area (30%). These inflow levels are higher than those obtained in the 2005 MGP study (as seen in Figure 2). This indicates that the expansion of the commercial hierarchy to include the regional node (Hoover Park Town Centre) has been beneficial to the Community of Stouffville. Figure 2: 2005 Customer Origins by Existing Commercial Nodes 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 1A 1B Downtown Can. Tire former A&P former No Frills former Sobeys former 2A 3A+3B+3C+ 3D TRADE AREA INFLOW 3. Consumer Telephone Survey: - 7 -

32 3.1 Survey Methodology The professional survey firm of Network Research Field Services conducted a consumer telephone survey of the retail expenditure patterns of Trade Area residents over the month of June Sample sizes for the Primary Trade Area (Zones 1A + 1B) and Secondary Trade Area East (Zones 3A + 3B + 3C + 3D) are proportionate to the distribution of population in these zones in A separate stand-alone survey of 200 was conducted in the Secondary Trade Area South (Markham Zone 2A) because of this zone s high population level. By gender, the sampling was split roughly 75% female and 25% male. The survey asked respondents where and how much they spent over a prescribed recall period (calibrated at 3 months) in 36 retail store categories, including FSR (2 food store categories) + NFSR (1 department store category plus 30 non-department store GAFO categories) + HI spending (3 categories including garden supply/nursery). The results of the Consumer Telephone Survey are compiled in Appendix C of the Study as follows: Appendix C-1 Primary Trade Area Expenditures (Row and Column Totals) Appendix C-2 Secondary Trade Area East Expenditures (Row and Column Totals) Appendix C-3 Secondary Trade Area South Expenditures (Row and Column Totals) Appendix C-4 Head of Household (Gender) Appendix C-5 Average Size of Household Appendix C-6 Respondent Age Profile Appendix C-7 Respondent Employment Profile Appendix C-8 Head of Household Shopping Frequency by Store Type Appendix C-9 Head of Household Average Amount Spent by Store Type - 8 -

33 The total sample size of 850 completed surveys was split numerically as follows: TRADE AREA No. of Surveys Primary Trade Area: Total 400 Community of Stouffville Zone 1A 265 Rural Whitchurch- Stouffville Zone 1B 135 Secondary Trade Area East: Total 250 Urban Uxbridge Zone 3A 135 Rural Uxbridge South Zone 3B 46 Rural Uxbridge North Zone 3C 50 Pickering - N. of Hwy. 7 Zone 3D 19 Secondary Trade Area South: 200 Markham - N. of 16 th /E. of Kennedy Zone 2A 200 TOTAL SURVEYS 850 Local capture rates by Stouffville merchants are derived from these survey results. These are subsequently applied as base year capture rates in the calculations of residual (warranted) square footages. 3.2 Local Capture Rates by Stouffville Merchants Figure 3 features the local capture rates that Stouffville merchants obtain from residents of the Primary Trade Area, the Secondary Trade Area South, and the Secondary Trade Area East (as summarized from Appendices C-1 to C-3): - 9 -

34 Figure 3: Local Capture Rates by Stouffville Stores 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Supermarket Specialty Food Department Store General Merchandise Home and Auto Supply (HAAS) (Canadian Tire / TSC Store) Tires, Batteries, Accessories /Automotive Specialty Store Men s & Ladies Wear Family Wear / Unisex Children s Wear Shoes Jewellery Clothing Accessories Luggage & Leather Goods Stationery / Office Supply Book Store / News Dealer Record / CD / Tape Camera / Photo Supply Gift / Novelty / Greeting Card / Party Supply Sporting Goods Hobby / Toy / Craft Art Gallery & Artist Supply Musical Instruments Pet / Pet Supply Fabric or Yarn Shop Florist Drug / Discount Drug Furniture & Appliances TV / Stereo / Electronics / Computer Lighting / Carpet / Other Interior Décor China / Glassware / Kitchenware / Cutlery Bath / Bedding / Linen Telephone/Cell Phone/Vacuum/Sewing Machine Antiques Home Improvement / Lumber / Building Supply Hardware/Paint/Paper/Glass/Electrical/Plumbing Nursery / Garden Centre Primary Trade Area Secondary Trade Area South Secondary Trade Area East

35 Highest Local Capture Rates (60%-100%): High local capture rates from Primary Trade Area residents of more than 60% (meaning reciprocal outflow levels of less than 40%) are confined to generally lower order goods (with some higher order exceptions). Local capture rates in the 60% to 100% range are listed from highest to lowest as follows: Department Store (Wal-Mart only) 94.4% Stationery / Office Supply 93.8% General Merchandise 93.8% HAAS (Canadian Tire) 91.5% Drug / Discount Drug 89.9% Pet / Pet Supply 83.5% Supermarket 80.3% Jewellery 68.8% Florist 67.3% Family Wear 61.4% Specialty Food 60.9% High local capture rates of more than 60% have been induced largely but not exclusively by the anchor stores at the regional node. For example, although the average department store capture is 56.7%, Wal-Mart s local capture is very high at 94.4% of Primary Trade Area residents spending in all Wal-Mart stores. The introduction of Staples at Hoover Park Town Centre has resulted in the very high capture rate in the Stationery / Office Supply category. Winners and Canadian Tire/Marks Work Warehouse are other examples. Similarly, Sportchek (under construction at Hoover Park Town Centre) is expected to greatly improve on the very low 16.7% local capture rate in the Sporting Goods category. These results point to the success of the regional node in performing its regional function for certain but not all retail categories. Lowest Local Capture Rates (0%-40%): Merchandising gaps are evident where local capture rates from Primary Trade Area residents are low or negligible (here defined as less than 40%). Local capture rates of less than 40% are obtained generally in medium to higher order comparison goods shopping categories. These include:

36 Shopping Category Fashion Categories: Local Capture Rate by Stouffville Stores Percent of FSR + NFSR + HI Spending men s and ladies wear 19.3% representing 2.6% children s wear 1.7% representing 1.4% shoes 0.0% representing 1.5% clothing accessories 0.0% representing 0.8% luggage and leather goods 0.0% representing 1.1% Specialty Retail Categories: books 0.0% representing 0.9% records/cd/tape 0.0% representing 1.1% camera/photo supply 0.0% representing 3.6% gifts/novelty 3.5% representing 0.5% sporting goods 16.7% representing 2.3% hobby/toy/craft 38.2% representing 1.5% art supply/gallery 29.0% representing 1.1% fabric/yarn 15.4% representing 0.9% musical instruments 0.0% representing 1.5% Home Furnishings and Interior Décor Categories: furniture/appliances 30.9% representing 9.2% TV/electronics/computer 2.9% representing 3.2% lighting/carpet/other décor 23.3% representing 2.6% china/glass//kitchenware 0.0% representing 0.7% bath/bedding/linen 0.0% representing 1.4% Phone/Vacuum/Sew. Machi ne 33.8% representing 1.1% Antiques 25.3% representing 1.3% Home Improvement HI/lumber/building supply 34.1% representing 6.5% hrdwr/paint/glass/elect/plumb 31.1% representing 2.6% Total (less than 40% local capture) 49.4%

37 3.3 Implications of Survey with respect to Local Capture Rates: Stouffville retailers obtain relatively low local capture rates of less than 40% (i.e. from 0% to 40%) from Primary Trade Area residents for spending categories that comprise almost 50% of their spending (actually 49.4% in bar above). With so much outflow (60%+) across such a large proportion of spending (almost 50%), this is less than an optimal situation. It suggests current under-storing and the need for the Community of Stouffville to attract certain types of new retail stores to catch up with the population growth. Past gains in local capture rates have come through the attraction of new anchor stores at the regional node. Future gains may be a combination of attracting anchor and non-anchor specialty stores in the weaker categories. However, this implies that efforts by Stouffville retailers to increase local capture rates in spending categories that are now less than 40% would be targeting 5 of every 10 dollars (i.e. across all categories in the previous bullet points). The opportunity to target such a large proportion of spending is encouraging for the future maturing of the Community of Stouffville s commercial hierarchy as the population increases. This also implies that Stouffville retailers have weakest local capture rates from Secondary Trade Area residents in categories that represent half of their spending as well. These findings support the general proposition that Stouffville retailers have good opportunities for increased penetrations of both the Primary Trade Area and the two Secondary Trade Area zones. While most gaps are coincident with lower local capture rates, the proximity of competitive facilities will continue to moderate the prospects for outflow recovery. 3.4 Local Capture Rates for Agglomerated Retail Store Types: Local capture rates that Stouffville merchants obtain from each Trade Area zone for nine (9) agglomerated store types (i.e. agglomerated from the 36 store categories listed in Figure 3 above) are as follows:

38 Figure 4 - Percent Local Capture Rates by Stouffville Stores 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Department Store Other General Merchandise Drug and Personal Care Fashion & Accessories Home Furnishings/Electronics Primary Trade Area Secondary Trade Area South Secondary Trade Area East Other Specialty Non- Department Home Improvement Supermarket/Grocery Store Specialty Food Store These local capture rates are applied as base year shares in the residual calculations for the same nine (9) agglomerated spending categories (in Tables of this Study Update). 3.5 Respondent Shopping Frequency by Store Type: The following summary compares shopping frequency by store type and the percentage of total amount spent for the entire sample (Appendix C-9 reveals there is little variation in shopping frequency across the three Trade Area zones): Shopping Frequency By Store Type % of Total $ Spent 80% - 100% of Respondents Shopped at: Supermarket / Superstore incl. Costco food) 18.0% Major or Discount Department Store 3.6% Subtotal 21.6% 60% - 80% of Respondents Shopped at: Drug or Discount Drug Store 3.2% Home & Auto Supply / Canadian Tire/TSC 2.1% HI: Lumber / Building Supply 6.5% General Merchandise Including Costco 1.9% Subtotal 13.6% Subtotal 60% - 100% 35.2%

39 30% - 40% of Respondents Shopped at: HI: Nursery / Garden Ctr. 1.9% Stationery of Office Supply Store 1.3% Family Wear / Unisex Clothing 2.0% Subtotal 5.1% 20% - 30% of Respondents Shopped at: Book Store or News Dealer 0.9% Pet or Pet supply Store 1.2% Specialty Food Store 3.0% Shoe Store 1.5% Hobby/Toy/Craft Store 1.5% TV / Stereo / Electronics / Computer 3.2% Subtotal 11.3% 10% - 20% of Respondents Shopped at: Men's or Ladies' Wear Store 2.6% Sporting Goods Store 2.3% Gift/Novelty/Greeting Card/Party 0.5% Florist 0.9% HI: Hardware/ Paint/Paper/Electrical/Plu 2.6% Furniture / Appliance Store 9.2% Lighting / Carpet / Interior Décor 2.6% Telephone/Cell Phone/Vacuum/Sew. Machine 1.1% Subtotal 21.7% Fewer than 10% of Respondents Shopped at: Fabric of Yarn Store 0.9% Children's Wear Store 1.4% Bath/Bedding/Linen Store 0.7% Jewellery Store 6.5% Camera or Photographic Supply Store 3.6% TBA (Tires/Batteries/Accessories) 5.9% Art Gallery/Artists' Supply Store 1.1% China/Glassware/Kitchenware/Cutlery 0.7% Musical Instrument & Supply Store 1.5% Record / CD / Tape Store 1.1% Luggage and Leather Goods Store 1.1% Antiques Shop 1.3% Clothing Accessories Store 0.8% Subtotal 26.7% Total Amount Spent by Household Head 100%

40 Implications: Respondents generally have the highest frequency of shopping in lower-order anchor stores (including discount department stores) which represent about 1/3 rd of respondent spending. Respondents generally have the lowest frequency of shopping in non-anchor higher-order specialty stores which represent about 2/3 rds of respondent spending. These findings confirm that shoppers in the Stouffville market have typical/normal shopping patterns in terms of shopping frequency and percentage spent by store type. 4. Community of Stouffville Floorspace Inventory: & 2005 Inventories There has been an increase in the amount of retail commercial space in the Community of Stouffville since The 2005 inventory in the Community of Stouffville identified approximately 475,000 square feet of retail commercial space. In comparison to the 2005 inventory, the current study s 2012 inventory in the Community of Stouffville consists of approximately 900,000 square feet of retail commercial space broken down as follows (See Maps 1 & 2):

41 Figure Floorspace Inventory (Total: 910,120 ft 2 ) *Includes 27,000 square feet of supermarket-equivalent space in Walmart Other Space NEC, 26,908sf, 3.0% Liquor/Beer/Wine, 13,770sf, 1.5% Vacancy, 4,000sf, 0.4% Bank/Trust, 24,215sf, 2.7% Supermarket/ Grocery *, 103,911sf, 11.4% Specialty Food, 21,900sf, 2.4% Restaurants, 117,747sf, 12.9% Other Services, 59,232sf, 6.5% Dep't Store (nonfood), 135,600sf, 14.9% Professional Services, 45,240sf, 5.0% Personal Services, 37,670sf, 4.1% HI, 26,860sf, 3.0% Non-Dep t Store, 293,067sf, 32.2% The differences between the 2005 and 2012 inventory in part reflect the fact that non-retail space (personal and other services, bank, and Liquor/beer/wine space) were tallied only in the Downtown area in 2005, with the result that longitudinal comparisons to the current study are only available for the retail categories (FSR + NFSR + HI space). The 2005 inventory is broken down as follows (i.e. MGP s 2005 inventory is converted to NAICS nomenclature here to facilitate comparisons):

, 0, 0.")

42 Figure Floorspace Inventory (Total: 475,300 ft 2 ) Vacancy, 17,400sf, 3.7% Bank/Trust, 12,000sf, 2.5% Restaurants, 29,100sf, 6.1% Supermarket/ Grocery *, 95,000sf, 20.0% Other Services, 77,100sf, 16.2% Specialty Food, 29,300sf, 6.2% Dep't Store (non-food), 0, 0.0% Personal Services, 8,500sf, 1.8% HI, 24,500sf, 5.2% Non-Dep t Store, 182,400sf, 38.4%

43 4.2 Comparison between 2005 and 2012 The differences between the 2005 and 2012 FSR, NFSR, HI and Vacant space are as follows: Inventory Inventory Difference % Change 8, % Specialty -7, % Subtotal FSR 1, % Dep't 135, % Non-Dep t 110, % Subtotal 246, % 2, % -13, % TOTAL 236, % Excluding the non-retail categories, the greatest square footage gains have been in the Department Store and Non-Department Store NFSR categories. Vacant space has declined significantly. The Supermarket/Grocery category has changed modestly as a result of Wal-Mart s food component replacing the Sobeys closure. Overall, the retail inventory, including vacant space, has increased by over 235,000 square feet since the 2005 CPR. As a result of these significant inventory changes, the retail market shares obtained in the 2005 consumer telephone survey have also changed significantly. 4.3 Vacant Space The floorspace inventory indicates that with respect to existing development, vacancies now make up less than 1% of existing retail commercial space -- well below the normal range of 5% to 7% typical of most markets. This low vacancy rate appears to point to the relative good health of the retail commercial hierarchy, and the generally productive performance levels of existing space (i.e. sales per square foot) would appear to suggest that the market may be under-stored

44 5. Community of Stouffville s Existing Retail Commercial Hierarchy: 5.1 Commercial Nodes The existing commercial hierarchy is spread over three nodes (the Downtown, the Western Approach Area, and the Hoover Park Town Centre power centre ). There is also a site designated Neighbourhood Retail Area (Stouffville Country Market) on the east side of the Community. These nodes are differentiated by function, separated by distance, yet distributed to facilitate cross-shopping and outflow reduction. (See Map 2) 5.2 New Commercial Development Potential With respect to significant new commercial development potential: Hoover Park Town Centre (Regional Retail Area) has about 150,000 square feet of remaining development potential. The Western Approach Area includes the former Anderson Haulage site (now Minto/Trinity) 2 which has zoning approvals for about 70,000 square feet of commercial space, as well as 12,190 square feet of commercial space as part of a mixed use development. The Western Approach Area also has a number of other sites which have over 100,000 square feet of commercial development potential including the vacant former Canadian Tire site (about 2 acres on the south side of Main Street at Winona where the former 19,000 square foot facility has been razed), Houston Motors auto dealership (about 4 acres), and the Town s Works Yard (about 4.75 acres). The Gateway Mixed Use Area (Ringwood area) has small lot potential for restaurants, boutiques, and offices, notwithstanding flood plain, environmental, access and property fragmentation constraints. The Stouffville Country Market in the east end has a protected allocation of 125,000 square feet, and there is some remaining potential for additional development in the Neighbourhood Commercial Area designation which applies to the Market site. 2 Note: Previously this site was zoned to permit a total gross floor area between 17,000 and 30,657 square metres (182, ,000 square feet) of commercial space. Town Council adopted a zoning by-law amendment which reduced the amount of commercial space to 6,425 square metres (70,000 square feet) on September 4, In addition, a mixed commercial residential development is proposed which includes 1,133 square metres (12,190 square feet) of commercial space

45 6. Closest Retail Commercial Competition: The Community of Stouffville s closest retail commercial competition is found in Markham at the Metrus and former Emerson Electric sites a little more than 3 miles south of the Whitchurch-Stouffville / Markham boundary. (See Map 4) Like the Hoover Park Town Centre, the power centre uses at the Metrus and former Emerson Electric sites have entered the market late in the developmental life cycle of power centres. Like the Hoover Park Town Centre, the power centre uses at the Metrus and former Emerson Electric sites have attracted a limited number of anchor stores: Hoover Park Town Centre: Wal-Mart, Staples, Winners, Canadian Tire and its affiliates Mark s Work Warehouse and Sportchek (under construction) versus Metrus et al: Home Depot, The Brick, Shoppers, Food Basics, and Petsmart. Unlike the Hoover Park Town Centre, the power centre uses at the Metrus and former Emerson Electric sites are less restricted in terms of having banking and small store retail permissions. The following uses are located in and around Metrus Properties Power Centre on Markham Rd. /Hwy. 48 (square footages are rounded). S/W Quadrant Markham Rd. and Castlemore Ave. f/s Home Depot 102,500 sq. ft. f/s CIBC 7,000 f/s Vacant Unit 1,580 Henry s Photo 3,500 f/s Bank of Montreal 6,000 f/s Shoppers Drug Mart 18,000 N/E Quadrant Markham Rd. and Castlemore Ave. f/s The Brick 46,700 sq. ft. N/W Quadrant Markham Rd. and Castlemore Ave. Large Strip Food Basics 47,900 Petsmart 20,000 Vacant 30,000 f/s T.D. Canada Trust 6,500 CRU Strip Iris Optician 1,500 Great Clips (Barber) 1,

46 Nails & Spa 1,500 CRU Strip Pizza Nova 1,300 Subway 1,300 Sushi Sushi 1,300 EB Games 1,300 Popeyes Chicken 1,300 f/s Scotiabank 6,500 Upper Village Dental 2,000 CRU Strip Nothing But Noodles 1,500 Vacant 1,500 Salon Concepts 1,000 N.R. Medical Clinic 2,900 This node is differentiated from the Hoover Park Town Centre by having: 4 banks 1 supermarket 1 big-box home improvement store 1 big-box furniture / appliance / electronics store 1 mini-box drug store 1 mini-box pet food store 11 units below 1,500 square feet 1 medical + 1 dental with combined space of about 5,000 square feet

47 - 23 -

48 7. Analysis of Retail and Selected Commercial Space Demand and Supply 7.1 Methodology This study examines retail and selected commercial space demands and supply. This terminology is NAICS-based, and includes uses listed in Appendix B-2. 3 The study is what is termed a residual analysis. A residual analysis is defined as a projection over time of the ease with which new space can enter the market ( ease of entry calculations) in response to population and real expenditure growth without causing transfers of sales away from existing competitive stores. It is a conservative methodology based purely on growth in market demand without factoring in additional market opportunity through sales transfers. In carrying out the analysis of retail and selected commercial space demands and supply, the following methodology was used: the 2012 base year (current/reference) distribution of spending of Trade Area residents based on the local (Community of Stouffville) capture rates from the 2012 consumer telephone survey in Community s Trade Area, macro-level residual demands for new space in the Community of Stouffville (where residuals represent the ease of entry of new space without sales transfers away from existing retail and selected commercial operators) as tested in 2014, 2016, 2021, 2026, and 2031, within the Community of Stouffville, the current built supply (inventory) of retail and selected commercial floorspace (FSR + NFSR + HI + Restaurant + Liquor/Beer/Wine + Personal Services + Financial Services + Other Services + Local Office + Vacant space), 3 retail uses that correspond in Appendix B-2 to Study Codes 1 to 123, including food stores, pharmacies and personal care stores, GAFO stores (General merchandise and department stores, Apparel and accessories stores, Furniture, home furnishings, and electronics stores, and Other retail stores), and Building and Outdoor Home Supply stores; and selected commercial uses that correspond to Study Codes 124 to 130 (financial / banking services); 137 to 143 (professional services); 151 to 155 (doctor / dentist / other health services); 172 to 174 (restaurant / food services); and 184 to 196 (personal services)

49 the differences over time between projected supply (built supply + designated/zoned land supply + vacancy uptake) and macro-level demands that might warrant any future expansions of the retail commercial infrastructure, at the macro-level, the Community of Stouffville s future land requirements and phasing of the warranted square footages. 7.2 Inputs and Assumptions Inputs and assumptions on which the analysis is based include: Residuals versus Per Capita Space Planning Ratios: Residuals (or residual demands) are additional dollar amounts over and above the base year sales achieved by the existing competition that are available to new competition as a result of population growth and real expenditure growth in the defined market area. The residual dollar amounts translate into warranted square footages by dividing the available residual dollars by standardized sales performance levels. Residual demands can be expressed as dollar amounts or their square footage equivalents. Residual demands are projected for the following retail/commercial categories: Supermarket/Grocery portion of FSR Specialty Food portion of FSR Department Store portion of NFSR (= GAFO / DRUG) Non-Department Store portion of NFSR General Merchandise Stores Apparel & Accessories Stores Furniture / Home Furnishings / Electronics Stores Other Retail Stores Pharmacies and Personal Care Stores HAAS/TBA HI Personal Services (e.g. Barber/Beauty, Weight Loss, Shoe & Other Repair Services, Dry Cleaner/Laundromat) Restaurant L/B/W (Liquor/Beer/Wine) Per capita space planning ratios are standardized amounts of space (expressed in square footages per capita) that represent the physical space required to serve each person in a defined market area over a one year period (e.g. typically 1.0 square feet of financial institution space is required physically for each person to be served in a particular market area). Per capita space planning ratios are used to project macro-level space demands for Other Service, Financial Institution, and Local Office space (FIRE and SBM)

50 Data Assumptions: 2012 constant dollars (i.e dollars updated by one year s real growth to 2012) 2012 base year 2012 retail commercial floor space inventory - dated July 31, 2012 (existing market supply) 2012 licence plate surveys (proxy customer origins and inflow), and 2012 consumer telephone survey (current distribution of expenditures) A basic assumption underlying this study reflects the general marketplace expectation that the per capita income and expenditure levels of Trade Area residents will remain at current levels (i.e. no erosion by economic instability). Other assumptions or clarifications are made at appropriate points in the text. Any major change affecting the assumptions would warrant a re-visitation of this study s findings. Regional Trade Area Delineation: The Community of Stouffville-centered regional Trade Area defined and analyzed in this study has been investigated in market studies and peer reviews going back to The defined trade area represents a relatively large, growing, and consistent part of the Community of Stouffville s trading geography and population base from which the Community of Stouffville s 2012 inventory of retail commercial space is expected to derive consistent market support over the forecast period. The stability of this economic geography is linked to the strengthening of the Community of Stouffville s retail offerings over time to better serve its local and regional markets. Trade Area Per Capita Household Incomes: The average per capita household incomes in the Trade Area (2006 & 2001 Census data) compared to the provincial average (index = 100.0) are as follows: 2006 Census 2001 Census Primary Trade Area (W-S) Secondary Trade Area South (NE Markham) Secondary Trade Area East (Uxbridge/Pickering) Total Trade Area

51 Significant gains in the Primary Trade Area and the Secondary Trade Area East are in contrast to the declining incomes in the Secondary Trade Area South. Per capita household incomes in the Primary Trade Area (the Town of Whitchurch-Stouffville) are amongst the highest in the province. A number of factors contribute to this: The Town of Whitchurch-Stouffville s labour force participation rate (69.6%) and employment rate (66.6%) exceed the provincial averages (67% and 63% respectively) while the Town s unemployment rate (4.3%) falls below the provincial average (6%). The percentages of Town residents with university education (21%) and high school education 30%) are on par with the province (20% and 27% respectively), while the percentage of Town residents with college education (30%) exceeds the provincial average (27%). Home ownership in the Town of Whitchurch-Stouffville (85.3%) is well above the provincial average (71%). Trade Area Incomes / Expenditures and Projected Population Growth: Appendix A-1 provides regression equations that link per capita household incomes in the Primary and Secondary Zones to per capita FSR, NFSR, HAAS/TBA, HI, Personal Service, Restaurant, and Liquor/Beer/Wine expenditures. Appendix A-2 features preliminary revised 2011 Ontario per capita FSR, NFSR (GAFO + Drugs), and HI expenditures. Appendix A-3 calculates per capita household income indexes (2006 Census data for income earned in 2005) and per capita expenditure indexes for the Trade Area based on the footnoted regression equations and relative to the provincial average. Appendix A-4 calculates the resultant 2011 per capita expenditures by retail commercial space category (FSR, NFSR, HAAS/TBA, HI, Personal Service, Restaurant, and Liquor/Beer/Wine) for the Primary and Secondary Trade Area zones. Appendix A-5 provides detailed calculations of the projected population growth unadjusted and adjusted for the Census undercount for the Primary and Secondary Trade Area zones from 2012 to Trade Area Population Projections: Population projections (Table 1 attached 4 and Figure 7 below) are adjusted for the Census undercount. 4 Note: Tables 1-24 follow the text of the report, but precede the Appendices

52 The Primary Trade Area (Town of Whitchurch-Stouffville) is projected to grow from about 41,200 persons (rounded) in the 2012 base year to reach about 60,600 persons by 2031 (for rounded overall growth of 19,400 persons over 19 years, averaging about 1,000 persons per year). These Primary Trade Area population projections follow rapid growth seen in the period 2006 to 2011 (about 3,000 persons per year over 5 years). This means that over a broader 25-year time period 2006 to 2031, the Town s population will have increased almost two-and-a-half times (by about 35,000 persons over 25 years, averaging about 1,400 persons per year). STA South Area is projected to grow from about 50,000 persons (rounded) in 2012 to reach about 58,000 persons by 2031 (for rounded overall growth of less than 8,000 persons). STA East Area is projected to grow from about 24,000 persons (rounded) in 2012 to reach about 25,000 persons by 2031 (for rounded overall growth of less than 1,000 persons). Population Projections 70,000 60,000 50,000 40,000 30,000 20,000 10,000 PTA STA South STA East Figure 7 - Population Projections Year The Community of Stouffville s Trade Area as a whole is projected to grow by about 28,000 persons to raise the 2012 base year population from about 115,300 persons (rounded) to about 143,000 persons in

53 7.3 Analysis Based on the inputs and assumptions the following calculations were carried out: Trade Area Expenditure Potentials: Tables 2 to 9 calculate expenditure potentials for the following categories by multiplying the projected population base in Table 1 by corresponding per capita expenditures: NFSR (GAFO / DRUG) + HI, FSR, Personal Service, Restaurant, and Liquor/Beer/Wine (L/B/W) Per capita space planning ratios are also used to estimate the amount of warranted square footage in the Other Service, Financial Institution, and Local Office categories in Table 21. Real Expenditure Growth: Real growth factors (per annum compounded exclusive of inflation) beyond the 2012 base year are applied to the expenditure potentials as follows: 1.5% to NFSR (GAFO / DRUG) + HI expenditures to 2016, and 0% thereafter; 0.5% to FSR and Personal Service expenditures to 2016, 0.25% to 2021, and 0% thereafter; 0.25% to Restaurant expenditures to 2021, and 0% thereafter; and 0.25% to L/B/W expenditures to 2021, and 0% thereafter; and Market Demands: The base year Trade Area shares and future Trade Area shares of NFSR + HI and FSR spending for the three Trade Area zones are summarized in Table 10. The base year and future Trade Area shares of NFSR + HI spending in Table 10 are incorporated into the residual space calculations in Tables Tables deal with lower order spending on Personal Service, Restaurant, and Liquor/Beer/Wine, and hence deal only with the spending of Primary Trade Area residents. This is unlike Tables which deal with higher order NFSR + HI market support attracted from the three Trade Area zones

54 Residual Space Estimates: In the following discussions, the residual dollars available in the market are defined to mean the dollar amounts left over after the base year sales of the existing competition in the Community of Stouffville are reserved or held constant over the forecast period without sales transfers. The available residual dollars are translated into residual square footages warranted in the market in future years in line with market growth. This involves dividing the residual dollars available within each spending category under investigation by an appropriate sales performance level per square foot. Translating the available residual dollars into residual square footages provides the necessary guidance to calculate future commercial land requirements to meet the growth in market demands. Residual space calculations identify the amount of floor area which can be supported in the market to the year 2031 based on projected population and income growth. Residual space calculations are based on base year local capture rates (market shares) from the consumer telephone survey and rounded future market shares that reflect population growth as the principal driver of the warranted retail space additions. The residual space demands are set out below and summarized in Figure 8 which follows: Department Store Residuals (Table 11): The existing department store space (Wal-Mart 135,600 square feet) is performing at $345 per square foot. Residual department store square footages are calculated at $425 per square foot: 2016: 31,000 square feet (rounded) 2021: 43,000 square feet (rounded) 2026: 49,000 square feet (rounded) 2031: 51,000 square feet (rounded) These residuals might be sufficient to support an anchor use such as Marshall s (typically 20,000 square feet) in the medium term. The residuals would not be sufficient to support other U.S. entries such as Kohl s in the medium term (typically 60,000 square feet). Other General Merchandise Residuals (Table 12): Existing Other General Merchandise space (94,790 square feet) achieves productive base year sales of $447 per square foot. Residual square footages are calculated at $400 per square foot:

55 2016: 32,000 square feet (rounded) 2021: 47,000 square feet (rounded) 2026: 54,000 square feet (rounded) 2031: 58,000 square feet (rounded) These residuals might be sufficient to support a regional chain store anchor use such as a TSC store (Tractor Supply Company typically in the range of 20,000 square feet) in the medium term. Drug & Personal Care Residuals (Table 13): The existing Drug & Personal Care space (37,487 square feet) achieves productive base year sales of $990 per square foot. Drug & Personal Care residuals are calculated at $950 per square foot: 2016: 12,000 square feet (rounded) 2021: 20,000 square feet (rounded) 2026: 23,000 square feet (rounded) 2031: 25,000 square feet (rounded) These residuals might support a new format drug store in the range of 18,000 to 20,000 square feet in the medium term. Fashion & Accessories Residuals Table 14): The existing Fashion & Accessories space (40,180 square feet) achieves relatively low base year sales of $227 per square foot. Fashion & Accessories residuals are calculated at $300 per square foot: 2016: 22,000 square feet (rounded) 2021: 29,000 square feet (rounded) 2026: 31,000 square feet (rounded) 2031: 33,000 square feet (rounded) These residuals would support a needed infusion of Fashion & Accessories space in the short to medium term since this is one category where current local capture rates are relatively low and the current provision of such space is meager. Home Furnishings Residuals (Table 15): The existing Home Furnishings space (44,600 square feet) achieves base year sales of $271 per square foot. Home Furnishings residuals are calculated at $300 per square foot: 2016: 12,000 square feet (rounded) 2021: 17,000 square feet (rounded) 2026: 20,000 square feet (rounded) 2031: 21,000 square feet (rounded)

56 These residuals would support a relatively small infusion of new space compared to the current provision. The most vital infusion needed is in the electronics and computer category. Other Non-Department Store Residuals (Table 16): The existing Other Non-Department Store / Specialty space (75,980 square feet) achieves relatively low base year sales of $259 per square foot. Residuals are calculated at $350 per square foot: 2016: 22,000 square feet (rounded) 2021: 32,000 square feet (rounded) 2026: 36,000 square feet (rounded) 2031: 38,000 square feet (rounded) Home Improvement Residuals (Table 17): The existing HI space (26,860 square feet) achieves very productive base year sales of $1,052 per square foot (including contractor sales). HI residuals are calculated at $335 per square foot: 2016: 14,000 square feet (rounded) 2021: 29,000 square feet (rounded) 2026: 35,000 square feet (rounded) 2031: 38,000 square feet (rounded) Supermarket Residuals (Table 18): The existing Supermarket space (103,910 square feet including 27,000 square feet of Wal-Mart food space) achieves productive average base year sales of $757 per square foot. Supermarket residuals are calculated at $525 per square foot: 2016: 33,000 square feet (rounded) 2021: 56,000 square feet (rounded) 2026: 66,000 square feet (rounded) 2031: 71,000 square feet (rounded) Specialty Food Residuals (Table 19): The existing Specialty Food space (21,900 square feet) achieves productive base year sales of $460 per square foot. Specialty Food residuals are calculated at $275 per square foot: 2016: 4,000 square feet (rounded) 2021: 9,000 square feet (rounded) 2026: 11,000 square feet (rounded) 2031: 13,000 square feet (rounded)

57 Personal Service Residuals (Table 20): The existing Personal Service space (37,670 square feet) achieves average base year sales of $225 per square foot. Personal Service residuals are calculated at $225 per square foot: 2016: 8,000 square feet (rounded) 2021: 14,000 square feet (rounded) 2026: 18,000 square feet (rounded) 2031: 19,000 square feet (rounded) Restaurant Residuals (Table 21): The existing Restaurant space (117,750 square feet) achieves average base year sales of $250 per square foot. Restaurant residuals are calculated at $225 per square foot as follows: 2016: 31,000 square feet (rounded) 2021: 48,000 square feet (rounded) 2026: 56,000 square feet (rounded) 2031: 60,000 square feet (rounded) Liquor/Beer/Wine Residuals (Table 22): The existing Liquor/Beer/Wine space (13,770 square feet) achieves highly productive base year sales of $1,425 per square foot. L/B/W residuals are calculated at $900 per square foot as follows: 2016: 6,000 square feet (rounded) 2021: 9,000 square feet (rounded) 2026: 11,000 square feet (rounded) 2031: 12,000 square feet (rounded) Summary of Residual Retail & Selected Commercial + Other Space: Table 23 reproduces from Tables 11 to 22 the estimates of residual space warranted over the projection period. As well, space planning ratios for the Other Service, Financial Institution, and Local Office categories are applied to the population growth within Town over the forecast period. The total Retail and Selected Commercial residual demands plus demands for Other Space based on space planning ratios are featured in the lower box on Table 23 overleaf attached and chart below

58 Figure 8 - Stouffville Summary Demands and Residual Space Square Feet (Thousands) Department Store Space Other General Merchandise NFSR Space Drug & Personal Care NFSR Space Fashion & Accessories NFSR Space Home Furnishings NFSR Space Other Non-Dep't Store NFSR Space Home Improvement NFSR Space Supermarket FSR Space Specialty Food FSR Space Personal Service Space Restaurant Space Liquor / Beer / Wine Space Table 24(a) simply reproduces the demands for total Retail and Selected Commercial residual space plus for Other Space from the lower box in Table 23 overleaf as follows: o 2016: 285,000 square feet (rounded) o 2021: 455,000 square feet (rounded) o 2026: 535,000 square feet (rounded) o 2031: 570,000 square feet (rounded)