TAX REFORM AND THE BUDGET

|

|

|

- Dora Pope

- 5 years ago

- Views:

Transcription

1 TAX REFORM AND THE BUDGET Len Burman Daniel Patrick Moynihan Professor of Public Affairs, Maxwell School, Syracuse University OASIS February 9, 2011

2 Part I: About the Budget

3 How did you go bankrupt? Bill asked. Two ways, Mike said. Gradually and then suddenly. Ernest Hemingway, The Sun Also Rises (quoted in Auerbach and Gale, The Economic Crisis and the Fiscal Crisis: 2009 and Beyond ) 3

4 Deficit Projections for Obama Budget, in $billions , % 4.3% 3.8% 4.0% 3.8% 3.4% 3.4% 3.6% 3.8% -1,200-1,400-1, % of GDP 10.0% 9.2% cumulative deficit $8.5 trillion Source: Office of Management and Budget, "Midsession Review: Budget of the United States, Fiscal Year 2011," July 2010.

5 Ratio of Workers to Retirees 5

6 Total Public and Private Spending on Healthcare as Percent of GDP, Source: CBO, 2009, Long-Term Budget Outlook

7 7 Primary Spending as % of GDP, with and without Excess Health Costs,

8 Composition of Nondiscretionary Federal Spending, Percent of GDP Interest Medicare and Medicaid Social Security Source: CBO, The Long-Term Budget Outlook, June 2009.

9 Alternative Projections of Debt Held by the Public, Percent of GDP Alternative 100 Extended Year 9 Source: CBO

10 Alternative Projections of Debt Held by the Public, With GDP response With rate response Percent of GDP Alternative Extended Year 10

11 Federal, State, and Local Non-Interest Spending, as percent of GDP, including GDP Fed, state, and local 30 Federal (excluding Source: CBO, 2009, Long-Term Budget Options; GAO, 2008, "STATE AND LOCAL GOVERNMENTS: Growing Fiscal Challenges will Emerge during the Next 10 Years," GAO-

12 12 Major Foreign Holders of US Debt, in $billions, July China, Mainland Japan United Kingdom Carib Bnkng Ctrs Oil Exporters Brazil Russia Hong Kong Other countries Total = $3.4 trillion, of which about ¼ is T-bills. Source: US Treasury, Major Foreign Holders of Treasury Securities,

13 13 Distribution of Defaults or Restructurings by Debt Level, Middle-Income Countries, External Debt/GNP at end of first year of default or restructuring < > Source: Reinhart and Rogoff (2009), p. 24. % of total defaults or restructurings

14 Debt as Percent of GDP in OECD Countries, Source: OECD Stat.Extracts.

15 Figure 7. Debt Held by Public, by Maturity in Years, as of October , Debt Due in Year, in $Billions 2,500 2,000 1,500 1, Years Until Due Source: US Treasury, Monthly Statement of the Public Debt (MSPD), October 2009,

16 16 Part II. About our Tax System Graphic borrowed from Taxing Ourselves: A Citizen s Guide to Tax Reform, by Joel Slemrod and Jon Bakija.

17 Federal Revenues by Source as a Percentage of GDP, Estate tax and other Excise taxes Corporateincome tax Payroll tax Individual income tax Source: Office of Management and Budget, Budget of the US Government FY 2011, Historical Tables, Table 2.3; are projections.

18 State and Local Taxes by Source as Percentage of GDP Corporate income Personal income Sales Property Source: NIPA Table 3.2 and 1.1.5, accessed 2/4/11.

19 Federal, State, and Local Taxes as Percentage of GDP State and Local Tax Federal Tax Source: NIPA Tables 3.2, 3.3, and 1.1.5, accessed 2/4/11.

20 60 Tax as Percent of GDP, OECD Countries, Source: OECD, 2009, Revenue Statistics

21 Income Tax Rates Required to Cut Deficit to 2% of GDP in 2019, Administration Baseline Current Tax Raise All Raise Top Raise Top Rates Rates Three Rates Two Rates Source: Altshuler, Lim, and Williams, 2010, Desperately Seeking Revenue, Tax Policy Center.

22 Tax Expenditures Compared to Other Spending, FY 2011 Income Tax Expenditure Mandatory Discretionary Defense Nondefense $ Billions 1,177 2,165 1, Percent % of GDP

23 Tax Expenditures Compared to Other Taxes, FY 2011 Income Tax Expenditures Net Individual Income Tax Corporate Income Tax Payroll Tax Other $ Billions 1,177 1, Percent % of GDP

24 100 Shares of Non-Interest Spending FY Non Defense Discretionary 80 Defense Mandatory 20 Tax Expenditures 0 Source: GAO (via Lori Metcalf), FY 11 Budget, and authors' calculations.

25 18 Consumption Tax as Percentage of GDP, OECD Countries, OECD Average

26 26 Who Doesn t Pay Income Tax? Source:

27 27 Income Share of Top 1 Percent, % 25% 20% 15% 10% 5% 0% Source: Thomas Picketty and Emmanuel Saez, "Income Inequality in the United States, ," Quarterly Journal of Economics, 118(1), 2003, Updated data at

28 Tax Policy Center 28 Top Tax Rate on Individual Income, % 90% 80% 70% 60% 50% 40% 30% 20% 10% 0%

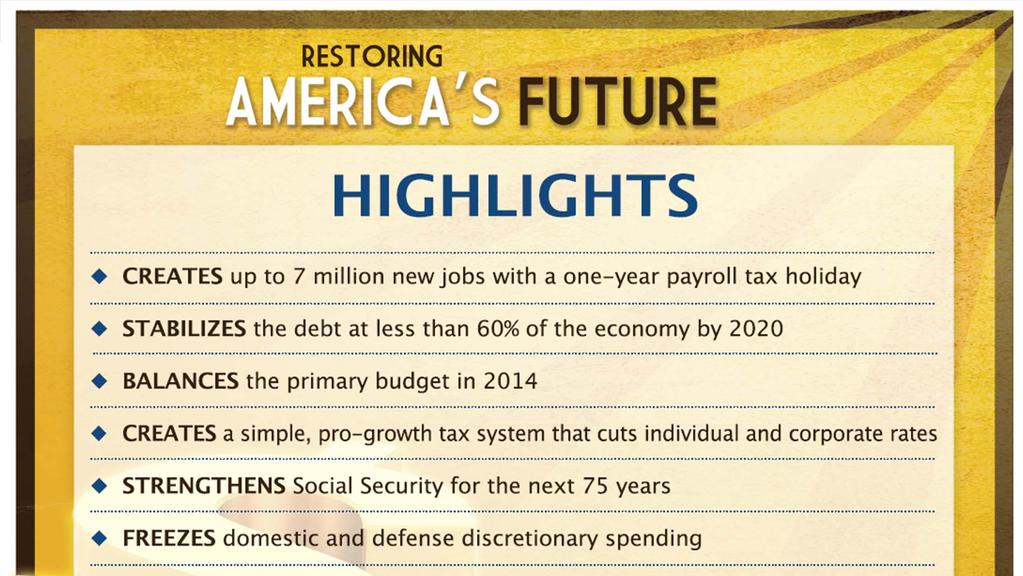

29 29

30 Effective Federal Tax Rates by Economic Income Class, Average = Percent Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile Top 10 Percent Top 5 Percent Top 1 Percent Top 0.5 Percent Top 0.1 Percent Income Class Source: Estate Corporate Payroll Individual Income

31 What is the AMT? 31

32 Part III. A Reform Plan 32

33 33

34 Overview of Tax Reform Debt reduction sales tax (VAT) at 7% Cut top individual and corporate income tax rates to 27% Return-free 15% PIT for most taxpayers Fully refundable child tax credit and payroll tax credit replace personal exemption, standard deduction, child-related credits (including EITC) 15% withholding on wage&salaries, dividends, interest Nonfilers could receive credits through employers or via smart card

35 Eliminate most tax expenditures, simplify others Mortgage interest, IRA, and charity deductions replaced with 15% refundable credit, payable directly to institutions Like UK gift aid Eliminate state and local tax deduction Replace education tax subsidies with expanded Pell grants and subsidized student loans

36 Restoring America s Future: Breakdown of Budget Savings 200% % of GDP 150% 100% Debt Service Savings Other Spending Healthcare Social Security Savings 50% New 0%

37 Revenue Breakdown 5% % of GDP 4% 3% 2% Net New Revenues Eliminate or restructure most tax Other Tax Debt Reductio n Sales Tax 1% Restructure Itemized Deductions 0% Employer Health Benefit Corporate Tax Rate Cut -1% Income Tax -2%

CBO s January Baseline Sets the Stage. CRFB.org

CBO s January Baseline Sets the Stage 1 Trillion-Dollar Deficits Are Returning $1,600 Billions $1,400 $1,200 $1,000 $800 Deficits Increased Almost 800% Deficits Fell 69% Deficits Triple to Nearly $1.4

CBO s January Baseline Sets the Stage 1 Trillion-Dollar Deficits Are Returning $1,600 Billions $1,400 $1,200 $1,000 $800 Deficits Increased Almost 800% Deficits Fell 69% Deficits Triple to Nearly $1.4

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

The Federal Budget Now and In the Future THE CONCORD COALITION. presented by Joshua Gordon, Policy Director.

The Federal Budget Now and In the Future presented by Joshua Gordon, Policy Director THE CONCORD COALITION www.concordcoalition.org America is on an Unsustainable Fiscal Path Debt Held by the Public, as

The Federal Budget Now and In the Future presented by Joshua Gordon, Policy Director THE CONCORD COALITION www.concordcoalition.org America is on an Unsustainable Fiscal Path Debt Held by the Public, as

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Tax Reform in a Trump World

Tax Reform in a Trump World Government Fleet Expo and Conference Kenneth J. Kies Managing Director The Federal Policy Group San Antonio, Texas June 14, 2017 Overview The 2016 Election did not Change Our

Tax Reform in a Trump World Government Fleet Expo and Conference Kenneth J. Kies Managing Director The Federal Policy Group San Antonio, Texas June 14, 2017 Overview The 2016 Election did not Change Our

Where We Were. CRFB.org

Where We Were 1 Trump Entered Office With Debt At Post WWII Record-High Levels 120% 100% Percent of GDP Truman 103% 80% Trump 77% 60% Bush Obama 40% 20% Eisenhower JFK Johnson Nixon Ford Carter Reagan

Where We Were 1 Trump Entered Office With Debt At Post WWII Record-High Levels 120% 100% Percent of GDP Truman 103% 80% Trump 77% 60% Bush Obama 40% 20% Eisenhower JFK Johnson Nixon Ford Carter Reagan

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

The Global Economy: Sustaining Momentum

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

RBC Economics Financial Update Dawn Desjardins

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

From Recession to Recovery

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six years of steady growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half Full

The Economic Outlook Economic Policy Division Glass Half Full Six years of steady growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half Full

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip?

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

Reading the Tea Leaves: Investing for 2010 and Beyond

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

The U. S. Economic Outlook: Robert J. Gordon

The U. S. Economic Outlook: Upside and Risks Robert J. Gordon Ottawa a Economics Association Ottawa, a, September 14, 2017 Immigration Medical Care My Policy Package: Be Like Canada d University Tuition

The U. S. Economic Outlook: Upside and Risks Robert J. Gordon Ottawa a Economics Association Ottawa, a, September 14, 2017 Immigration Medical Care My Policy Package: Be Like Canada d University Tuition

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

Why Is the Recovery from the Financial Crisis So Sluggish?

Why Is the Recovery from the Financial Crisis So Sluggish? Robert E. Hall Hoover Institution and Department of Economics Stanford University Keynote Address Agricultural and Applied Economics Association

Why Is the Recovery from the Financial Crisis So Sluggish? Robert E. Hall Hoover Institution and Department of Economics Stanford University Keynote Address Agricultural and Applied Economics Association

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes. Tom Rogers. Lead Economist, Oxford Economics.

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

The U.S. Debt Crisis: How it Happened and What Can be Done

The U.S. Debt Crisis: How it Happened and What Can be Done Updated Nov 2012 Pat Obi 1 OUTLINE 1. 2007 Mortgage crisis 2. Federal budget 3. Debt buildup 4. The debt crisis 5. Failed attempts by Congress

The U.S. Debt Crisis: How it Happened and What Can be Done Updated Nov 2012 Pat Obi 1 OUTLINE 1. 2007 Mortgage crisis 2. Federal budget 3. Debt buildup 4. The debt crisis 5. Failed attempts by Congress

ABA Commercial Real Estate Lending Committee

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

More of the Same; Or now for Something Completely Different?

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

Real gross domestic growth

Real gross domestic growth United States, 2000 prices Compound annual growth rate 10 5 0-5 -10 81 83 85 87 89 91 93 95 97 99 01 03 05 07 Sources: BEA, Global Insight. Consumer sentiment University of Michigan,

Real gross domestic growth United States, 2000 prices Compound annual growth rate 10 5 0-5 -10 81 83 85 87 89 91 93 95 97 99 01 03 05 07 Sources: BEA, Global Insight. Consumer sentiment University of Michigan,

The U.S. Economic Outlook

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

The US Economic Outlook

IHS ECONOMICS US Outlook The US Economic Outlook November 2014 ihs.com Rafael Amiel, Director latin America Economics +1 215 789 7405, rafael.amiel.ihs.com 2014 IHS The US economy is gaining momentum Growth

IHS ECONOMICS US Outlook The US Economic Outlook November 2014 ihs.com Rafael Amiel, Director latin America Economics +1 215 789 7405, rafael.amiel.ihs.com 2014 IHS The US economy is gaining momentum Growth

PROVINCE OF SASKATCHEWAN INVESTOR PRESENTATION

PROVINCE OF SASKATCHEWAN INVESTOR PRESENTATION May 2018 THE SASKATCHEWAN DIFFERENCE Economic Stability Diversified economy balances cyclicality of resources Growing population Majority government with

PROVINCE OF SASKATCHEWAN INVESTOR PRESENTATION May 2018 THE SASKATCHEWAN DIFFERENCE Economic Stability Diversified economy balances cyclicality of resources Growing population Majority government with

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Trends. September 10, 2013

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Economic Outlook: fear over fundamentals

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States?

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

France : Economic developments and reforms, where are we heading?

France : Economic developments and reforms, where are we heading? The Economic Club of New York : 18 April 2018 François VILLEROY de GALHAU, Governor of the Banque de France 1 WHERE ARE WE STARTING FROM?

France : Economic developments and reforms, where are we heading? The Economic Club of New York : 18 April 2018 François VILLEROY de GALHAU, Governor of the Banque de France 1 WHERE ARE WE STARTING FROM?

Big Changes, Unknown Impacts

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

2019 Economic Outlook: Will the Recovery Ever End?

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

Economic & Financial Market Outlook

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

The Debt is on an Unsustainable Long-Term Path

Debt Held By the Public The Debt is on an Unsustainable Long-Term Path 90% Percent of GDP 80% Current Law with War Drawdown 77 Percent of GDP 70% 60% 2010 2012 2014 2016 2018 2020 2022 2024 Source: CBO

Debt Held By the Public The Debt is on an Unsustainable Long-Term Path 90% Percent of GDP 80% Current Law with War Drawdown 77 Percent of GDP 70% 60% 2010 2012 2014 2016 2018 2020 2022 2024 Source: CBO

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

The U.S. Economic Outlook

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

Federal Safety Net Big Dollars. FederalSafetyNet.com

Federal Safety Net Big Dollars Federal Expenditures FY 2012 In Billions Defense 902 Social Security 779 Medicare 485 Welfare Programs 357 Medicaid 269 Unemployment 109 Interest on Debt 225 All other 510

Federal Safety Net Big Dollars Federal Expenditures FY 2012 In Billions Defense 902 Social Security 779 Medicare 485 Welfare Programs 357 Medicaid 269 Unemployment 109 Interest on Debt 225 All other 510

Economic Growth in the Trump Economy

Economic Growth in the Trump Economy Presented to State Data Center Conference William F. Fox, Director November 18, 2016 GDP Grows, Though Slowly 10.0 8.0 Percentage Change, Previous Qtr, SAAR 6.0 4.0

Economic Growth in the Trump Economy Presented to State Data Center Conference William F. Fox, Director November 18, 2016 GDP Grows, Though Slowly 10.0 8.0 Percentage Change, Previous Qtr, SAAR 6.0 4.0

The United States: Fiscal Facts and Fantasies. Presented by: Nigel Gault Chief U.S. Economist IHS Global Insight

The United States: Fiscal Facts and Fantasies Presented by: Nigel Gault Chief U.S. Economist IHS Global Insight Subdued Recovery: Tailwinds Battling Headwinds The U.S. Recovery: Tailwinds More sectors

The United States: Fiscal Facts and Fantasies Presented by: Nigel Gault Chief U.S. Economist IHS Global Insight Subdued Recovery: Tailwinds Battling Headwinds The U.S. Recovery: Tailwinds More sectors

Composition of Federal Spending

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

Federal Reserve Bank of Dallas, FIRM (Financial Institution Relationship Management)

") The Economic Roller Coaster: Where Have We Been? And Where Are We Going? Thomas F. Siems, Ph.D. Senior Economist and Director of Economic Outreach Federal Reserve Bank of Dallas Economic Summit Dallas

The Economic Roller Coaster: Where Have We Been? And Where Are We Going? Thomas F. Siems, Ph.D. Senior Economist and Director of Economic Outreach Federal Reserve Bank of Dallas Economic Summit Dallas

Seven Lean Years Explaining Persistent Global Economic Weakness

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Forecast evaluation report Robert Chote Chairman

Forecast evaluation report 2017 Robert Chote Chairman Background to the FER The FER is an annual report looking at the performance of past EFO forecasts against the latest outturn data Rationale Accountability

Forecast evaluation report 2017 Robert Chote Chairman Background to the FER The FER is an annual report looking at the performance of past EFO forecasts against the latest outturn data Rationale Accountability

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Government finances A long term assessment. Presented by Edwina Matos Pereira

Government finances A long term assessment Presented by Edwina Matos Pereira Walter Mosher June 22, 2010 Structure 1. Aruba s current fiscal landscape 2. Long term outlook & scenarios 3. Aruba s GDP volatility

Government finances A long term assessment Presented by Edwina Matos Pereira Walter Mosher June 22, 2010 Structure 1. Aruba s current fiscal landscape 2. Long term outlook & scenarios 3. Aruba s GDP volatility

Global economy maintaining solid growth momentum. Canada leading the pack

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

School of international and Public Affairs. Columbia University Manuel Pinho

School of international and Public Affairs Columbia University Manuel Pinho SPHERE WITH CORE What matters to China matters to the world Do not give lessons to China: Europe and the US The challenges: Growth

School of international and Public Affairs Columbia University Manuel Pinho SPHERE WITH CORE What matters to China matters to the world Do not give lessons to China: Europe and the US The challenges: Growth

Labor Markets and Cost- Growth in Healthcare. Amitabh Chandra HARVARD UNIVERSITY

Labor Markets and Cost- Growth in Healthcare Amitabh Chandra HARVARD UNIVERSITY Houston...we have a problem... Think of the United States government as a gigantic insurance company with a sideline business

Labor Markets and Cost- Growth in Healthcare Amitabh Chandra HARVARD UNIVERSITY Houston...we have a problem... Think of the United States government as a gigantic insurance company with a sideline business

A comment on recent events, and...

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Update.

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Update February 26, 2013 The Worst Recession Since the Great Depression 0% Loss from Peak

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Update February 26, 2013 The Worst Recession Since the Great Depression 0% Loss from Peak

Old Dominion University 2017 Regional Economic Forecast. Strome College of Business

Old Dominion University 2017 Regional Economic Forecast January 25, 2017 Professor Vinod Agarwal Director, Economic Forecasting Project Strome College of Business www.odu.edu/forecasting The views expressed

Old Dominion University 2017 Regional Economic Forecast January 25, 2017 Professor Vinod Agarwal Director, Economic Forecasting Project Strome College of Business www.odu.edu/forecasting The views expressed

2017 PNG Economic Survey. Rohan Fox (ANU), Stephen Howes (ANU), Nelson Atip Nema (UPNG), Marcel Schröder (UPNG and ANU)

, Stephen Howes (ANU), Nelson Atip Nema (UPNG), Marcel Schröder (UPNG and ANU)") 2017 PNG Economic Survey Rohan Fox (ANU), Stephen Howes (ANU), Nelson Atip Nema (UPNG), Marcel Schröder (UPNG and ANU) Introduction New government, new plan Short-term challenges: recession, falling government

2017 PNG Economic Survey Rohan Fox (ANU), Stephen Howes (ANU), Nelson Atip Nema (UPNG), Marcel Schröder (UPNG and ANU) Introduction New government, new plan Short-term challenges: recession, falling government

The Aftermath of Global Financial Crises

The Aftermath of Global Financial Crises Carmen M. Reinhart, University of Maryland, NBER, and CEPR Brookings Institution Washington DC, April 20, 2009 This talk is based on several works with Kenneth

The Aftermath of Global Financial Crises Carmen M. Reinhart, University of Maryland, NBER, and CEPR Brookings Institution Washington DC, April 20, 2009 This talk is based on several works with Kenneth

SA economic review Kevin Lings. August 2018

SA economic review Kevin Lings August 2018 South Africa real GDP growth year-on-year %y/y 8 7 6 5 Ave 4.3% 4 Ave 2.5% 3 2 Ave 0.9% 1 0-1 -2-3 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 2

SA economic review Kevin Lings August 2018 South Africa real GDP growth year-on-year %y/y 8 7 6 5 Ave 4.3% 4 Ave 2.5% 3 2 Ave 0.9% 1 0-1 -2-3 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 2

MAINTAINING MOMENTUM:

MAINTAINING MOMENTUM: 2018 National Economic Update September 12, 2018 noun mo men tum \ mō-ˈmen-təm, mə- \ 1 b : the strength or force that allows something to continue or to grow stronger or faster as

MAINTAINING MOMENTUM: 2018 National Economic Update September 12, 2018 noun mo men tum \ mō-ˈmen-təm, mə- \ 1 b : the strength or force that allows something to continue or to grow stronger or faster as

The Herzliya Conference The Economic Dimension Prof. Rafi Melnick Provost, Interdisciplinary Center (IDC) Herzliya

Herzliya") The Herzliya Conference The Economic Dimension 2009 Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

The Herzliya Conference The Economic Dimension 2009 Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

Grasshoppers, Ants and Locusts: the future of the world economy

Ralph Miliband Series on the Restructuring of World Power Grasshoppers, Ants and Locusts: the future of the world economy Martin Wolf Associate editor and chief economics commentator, Financial Times Professor

Ralph Miliband Series on the Restructuring of World Power Grasshoppers, Ants and Locusts: the future of the world economy Martin Wolf Associate editor and chief economics commentator, Financial Times Professor

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

Hopes and Worries in an Election Year. Gregory Daco Principal US Economist April 2012

Economic Outlook: Hopes and Worries in an Election Year Gregory Daco Principal US Economist April 2012 Global Perspective: Bright Spots in Clouds of Uncertainty Global Economy US growth: on a better track

Economic Outlook: Hopes and Worries in an Election Year Gregory Daco Principal US Economist April 2012 Global Perspective: Bright Spots in Clouds of Uncertainty Global Economy US growth: on a better track

East Bay Financial Planners Association Conference

East Bay Financial Planners Association Conference Is The New Normal Here to Stay? January 10, 2018 Rich Taylor Vice President Client Portfolio Manager Percent Change (%) Subpar Economic Growth Real GDP

East Bay Financial Planners Association Conference Is The New Normal Here to Stay? January 10, 2018 Rich Taylor Vice President Client Portfolio Manager Percent Change (%) Subpar Economic Growth Real GDP

National and Regional Economic Outlook. Central Southern CAA Conference

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

Dr. Greg Hallman Director, Real Estate Finance and Investment Center (REFIC) McCombs School of Business University of Texas at Austin

McCombs School of Business University of Texas at Austin") Dr. Greg Hallman Director, Real Estate Finance and Investment Center (REFIC) McCombs School of Business University of Texas at Austin POWERPOINT PARTNER The US Economy today, with a close look at jobs

Dr. Greg Hallman Director, Real Estate Finance and Investment Center (REFIC) McCombs School of Business University of Texas at Austin POWERPOINT PARTNER The US Economy today, with a close look at jobs

BC Pension Forum. Economic Outlook. Presented by: Ben Homsy, CFA Portfolio Manager

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

How Capitalism Was Built

How Capitalism Was Built The Transformation of Central and Eastern Europe, Russia, and Central Asia Anders Åslund Senior Fellow Peterson Institute for International Economics Washington, DC, September

How Capitalism Was Built The Transformation of Central and Eastern Europe, Russia, and Central Asia Anders Åslund Senior Fellow Peterson Institute for International Economics Washington, DC, September

President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H. Parker Willis Lecture in Political Economics

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

Zions Bank Economic Overview

Zions Bank Economic Overview Utah Bankruptcy Lawyers Forum March 20, 2018 National Economic Conditions When Good News is Bad News Is Good News?? Dow Tops 26,000 Up 44% Since 2016 Election Source: Wall

Zions Bank Economic Overview Utah Bankruptcy Lawyers Forum March 20, 2018 National Economic Conditions When Good News is Bad News Is Good News?? Dow Tops 26,000 Up 44% Since 2016 Election Source: Wall

44 Economic Perspectives

44 Economic Perspectives Source: Kotlikoff (1988), p. 44 In Hundreds 70 Of Dollars 60 50.. 40. 30 ;-*** * s EARNINGS 20 -CONSUMPTION 10 10 20 30 40 50 60 70 Age 1910 1920 1930 1940 1950 1960 Year Fig.

44 Economic Perspectives Source: Kotlikoff (1988), p. 44 In Hundreds 70 Of Dollars 60 50.. 40. 30 ;-*** * s EARNINGS 20 -CONSUMPTION 10 10 20 30 40 50 60 70 Age 1910 1920 1930 1940 1950 1960 Year Fig.

Distributional National Accounts: Methods and Estimates for the United States

Distributional National Accounts: Methods and Estimates for the United States Thomas Piketty (PSE) Emmanuel Saez (UC Berkeley) Gabriel Zucman (UC Berkeley) November 2016 There is a large disconnect today

Distributional National Accounts: Methods and Estimates for the United States Thomas Piketty (PSE) Emmanuel Saez (UC Berkeley) Gabriel Zucman (UC Berkeley) November 2016 There is a large disconnect today

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD?

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD? FROM BUST TO BOOM. AN EPIC BUST After 16 years of growth with a short pause for breath in 2002, the Icelandic economy entered

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD? FROM BUST TO BOOM. AN EPIC BUST After 16 years of growth with a short pause for breath in 2002, the Icelandic economy entered

Rossana Merola ILO, Research Department

Raising tax revenues without harming equity and employment Rossana Merola ILO, Research Department G-24 Special Workshop on Growth and Reducing Inequality Geneva, 5 th - 6 th September 2017 The views expressed

Raising tax revenues without harming equity and employment Rossana Merola ILO, Research Department G-24 Special Workshop on Growth and Reducing Inequality Geneva, 5 th - 6 th September 2017 The views expressed

Telling Canada s story in numbers Elizabeth Richards Analytical Studies Branch April 20, 2017

Recent Developments in the Canadian Economy: How have the decline in oil prices and a weaker Canadian dollar affected Canada s economy? www.statcan.gc.ca Telling Canada s story in numbers Elizabeth Richards

Recent Developments in the Canadian Economy: How have the decline in oil prices and a weaker Canadian dollar affected Canada s economy? www.statcan.gc.ca Telling Canada s story in numbers Elizabeth Richards

This Time is Different: Eight Centuries of Financial Folly

This Time is Different: Eight Centuries of Financial Folly Carmen M. Reinhart, University of Maryland, NBER, and CEPR Kenneth S. Rogoff, Harvard University and NBER (Princeton University Press, forthcoming

This Time is Different: Eight Centuries of Financial Folly Carmen M. Reinhart, University of Maryland, NBER, and CEPR Kenneth S. Rogoff, Harvard University and NBER (Princeton University Press, forthcoming

THE ECONOMIC, CLIMATE, FISCAL, POWER, AND DEMOGRAPHIC IMPACT OF A NATIONAL FEE-AND- DIVIDEND CARBON TAX

THE ECONOMIC, CLIMATE, FISCAL, POWER, AND DEMOGRAPHIC IMPACT OF A NATIONAL FEE-AND- DIVIDEND CARBON TAX Regional Economic Models, Inc. Study Authors Scott Nystrom, M.A. Regional Economic Models, Inc. (REMI)

THE ECONOMIC, CLIMATE, FISCAL, POWER, AND DEMOGRAPHIC IMPACT OF A NATIONAL FEE-AND- DIVIDEND CARBON TAX Regional Economic Models, Inc. Study Authors Scott Nystrom, M.A. Regional Economic Models, Inc. (REMI)

Discussion of: The Rise, the Fall, and the Resurrection of Iceland by Benediksdottir, Eggertsson, Þorarinsson. Jón Steinsson Columbia University

Discussion of: The Rise, the Fall, and the Resurrection of Iceland by Benediksdottir, Eggertsson, Þorarinsson Jón Steinsson Columbia University Policy Failure 1: Banking Supervision Paper covers this very

Discussion of: The Rise, the Fall, and the Resurrection of Iceland by Benediksdottir, Eggertsson, Þorarinsson Jón Steinsson Columbia University Policy Failure 1: Banking Supervision Paper covers this very

Economic Update: Accelerating Growth and Increasing Risk

Economic Update: Accelerating Growth and Increasing Risk Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business May 23, 2018 The forecasts and commentary do

Economic Update: Accelerating Growth and Increasing Risk Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business May 23, 2018 The forecasts and commentary do

Economic and Real Estate Outlook

Economic and Real Estate Outlook By Lawrence Yun, Ph.D. Chief Economist, National Association of REALTORS Presentation at Charlottesville Area Association of REALTORS October 13, 2016 1990 1991 1992 1993

Economic and Real Estate Outlook By Lawrence Yun, Ph.D. Chief Economist, National Association of REALTORS Presentation at Charlottesville Area Association of REALTORS October 13, 2016 1990 1991 1992 1993

U.S Cement Outlook IEEE. Ed Sullivan Group VP, Chief Economist

U.S Cement Outlook IEEE Ed Sullivan Group VP, Chief Economist 1 Construction Activity Billion Real $ 1,400 1,200 1,000 2014 = 2.5% 2015 = 5.6% 800 600 400 200 0 12 Year Peak-to- Peak Recovery 1998 2000

U.S Cement Outlook IEEE Ed Sullivan Group VP, Chief Economist 1 Construction Activity Billion Real $ 1,400 1,200 1,000 2014 = 2.5% 2015 = 5.6% 800 600 400 200 0 12 Year Peak-to- Peak Recovery 1998 2000

Top incomes in historical and international perspective: Recent developments

Top incomes in historical and international perspective: Recent developments Facundo Alvaredo EMod/Nuffield College & Conicet & Paris School of Economics Inequality in the and Europe Top Incomes, Poverty

Top incomes in historical and international perspective: Recent developments Facundo Alvaredo EMod/Nuffield College & Conicet & Paris School of Economics Inequality in the and Europe Top Incomes, Poverty

RISI LATIN AMERICAN CONFERENCE. (São Paulo, 16 August 2016) The Latin American Economy: Some Successes, Many Disappointments

The Latin American Economy: Some Successes, Many Disappointments") RISI LATIN AMERICAN CONFERENCE (São Paulo, 16 August 2016) The Latin American Economy: Some Successes, Many Disappointments Andrea Boltho Magdalen College University of Oxford and Oxford Economics GDP

RISI LATIN AMERICAN CONFERENCE (São Paulo, 16 August 2016) The Latin American Economy: Some Successes, Many Disappointments Andrea Boltho Magdalen College University of Oxford and Oxford Economics GDP

Zions Bank Economic Overview

Zions Bank Economic Overview Intermountain Credit Education League May 10, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around

Zions Bank Economic Overview Intermountain Credit Education League May 10, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around

Economic Outlook for Canada: Economy Confronting Capacity Limits

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

China at a glance 2011

China at a glance 2011 GDP PPP Growth rate Per capita Value US$11.29 trillion 9.2% US$8,400 Ranking 3 7 119 Labor force Imports Exports Value 816.2 million US$1.74 trillion US$1.90 trillion Ranking 1 3

China at a glance 2011 GDP PPP Growth rate Per capita Value US$11.29 trillion 9.2% US$8,400 Ranking 3 7 119 Labor force Imports Exports Value 816.2 million US$1.74 trillion US$1.90 trillion Ranking 1 3

Exhibit 1. National Health Expenditures per Capita,

Exhibit 1. National Health Expenditures per Capita, 1980 2007 Average spending on health per capita ($US PPP) $7,500 $7,000 $6,500 $6,000 $5,500 $5,000 $4,500 $4,000 $3,500 $3,000 $2,500 $2,000 $1,500

Exhibit 1. National Health Expenditures per Capita, 1980 2007 Average spending on health per capita ($US PPP) $7,500 $7,000 $6,500 $6,000 $5,500 $5,000 $4,500 $4,000 $3,500 $3,000 $2,500 $2,000 $1,500

Avoiding the Blind Alley China s Economic Overhaul and its Global Implications

Avoiding the Blind Alley China s Economic Overhaul and its Global Implications Daniel Rosen Partner dhrosen@rhg.com NYU Stern China Research Luncheon New York December 1, 2014 10 East 40 th Street, Suite

Avoiding the Blind Alley China s Economic Overhaul and its Global Implications Daniel Rosen Partner dhrosen@rhg.com NYU Stern China Research Luncheon New York December 1, 2014 10 East 40 th Street, Suite

Agriculture and the Economy: A View from the Chicago Fed

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Northwest Economic Research Center College of Urban and Public Affairs Forecast Breakfast Economic Outlook

Northwest Economic Research Center College of Urban and Public Affairs 2019 Forecast Breakfast Economic Outlook 1/10/2019 2 U.S. ECONOMY 1/10/2019 3 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Northwest Economic Research Center College of Urban and Public Affairs 2019 Forecast Breakfast Economic Outlook 1/10/2019 2 U.S. ECONOMY 1/10/2019 3 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

sector: recent developments VÍTOR CONSTÂNCIO

The economy and the banking sector: recent developments VÍTOR CONSTÂNCIO January 2006 Recent performance of the economy and prospects Factors behind the period of slow growth Challenges to the Banking

The economy and the banking sector: recent developments VÍTOR CONSTÂNCIO January 2006 Recent performance of the economy and prospects Factors behind the period of slow growth Challenges to the Banking

Federal R&D Investments in the 2009 Budget

Federal R&D Investments in the 2009 Budget Kei Koizumi October 24, 2008 for the University of Michigan Engineering Advisory Council AAAS R&D Budget and Policy Program http://www.aaas.org/spp/rd See the

Federal R&D Investments in the 2009 Budget Kei Koizumi October 24, 2008 for the University of Michigan Engineering Advisory Council AAAS R&D Budget and Policy Program http://www.aaas.org/spp/rd See the

Babson Capital/UNC Charlotte Economic Forecast. May 13, 2014

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

The Economics of Public Policy 2. Government Revenue and Expenditure in the USA and elsewhere

Fletcher School of Law and Diplomacy, Tufts University The Economics of Public Policy 2. Government Revenue and Expenditure in the USA and elsewhere Prof George Alogoskoufis The Size of the Public Sector

Fletcher School of Law and Diplomacy, Tufts University The Economics of Public Policy 2. Government Revenue and Expenditure in the USA and elsewhere Prof George Alogoskoufis The Size of the Public Sector

World real GDP growth in 2010 Annual percent change

World real GDP growth in 2010 Annual percent change 1 or more 6-1 3-6% 0-3% Less than No data Source: International Monetary Fund. World real GDP growth in 2011 Annual percent change 1 or more 6-1 3-6%

World real GDP growth in 2010 Annual percent change 1 or more 6-1 3-6% 0-3% Less than No data Source: International Monetary Fund. World real GDP growth in 2011 Annual percent change 1 or more 6-1 3-6%

Kevin Thorpe Financial Economist & Principal Cassidy Turley

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

10 County Conference. Richard Wobbekind. Executive Director Business Research Division & Senior Associate Dean Leeds School of Business

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

III. Importance of Revenue Administration

Outline of Presentation I. Trends in Revenue Mobilization II. Growth Friendly Tax Policy III. Importance of Revenue Administration 2 I. Trends in Revenue Mobilization Trends in Overall Revenues - Median

Outline of Presentation I. Trends in Revenue Mobilization II. Growth Friendly Tax Policy III. Importance of Revenue Administration 2 I. Trends in Revenue Mobilization Trends in Overall Revenues - Median

Federal R&D Funding in the 2009 Budget

Federal R&D Funding in the 2009 Budget Kei Koizumi April 8, 2008 for the Vanderbilt Federal Forum AAAS R&D Budget and Policy Program http://www.aaas.org/spp/rd See the What s New section for the latest

Federal R&D Funding in the 2009 Budget Kei Koizumi April 8, 2008 for the Vanderbilt Federal Forum AAAS R&D Budget and Policy Program http://www.aaas.org/spp/rd See the What s New section for the latest

US Economic Outlook IHS ECONOMICS. Paul Edelstein, Director NA Financial Economics, ,

IHS ECONOMICS US Outlook US Economic Outlook How long will the ride last? September 2014 ihs.com Paul Edelstein, Director NA Financial Economics, +1 781 301 9014, paul.edelstein@ihs.com The US economy

IHS ECONOMICS US Outlook US Economic Outlook How long will the ride last? September 2014 ihs.com Paul Edelstein, Director NA Financial Economics, +1 781 301 9014, paul.edelstein@ihs.com The US economy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,