A Look at Consumer Confidence and Spending into 2011

|

|

|

- Winifred Short

- 5 years ago

- Views:

Transcription

1 A Look at Consumer Confidence and Spending into

2 Minneapolis London San Francisco New York Chicago Hong Kong Specialty Retail, Apparel & Footwear Brands, & Mass Merchants Sean Naughton, CFA Vice President Senior Research Analyst October 7 th 2010

3 DISCLOSURES Disclosures for universe of Jeff Klinefelter & Sean Naughton 1. I or a household member have a financial interest in the securities of the following companies: none 2. I or a household member is an officer, director, or advisory board member of the following companies: none 3. I have received compensation within the past 12 months from the following companies: none 4. Piper Jaffray or its affiliates beneficially own 1% or more of any class of common equities of the following companies: none 5. The following companies have been investment banking clients of Piper Jaffray during the past 12 months: GIII, GMAN, RUE 6. Piper Jaffray expects to have the following companies as investment banking clients within the next three months: none 7. Other material conflicts of interest for Jeff Klinefelter and Sean Naughton or Piper Jaffray regarding companies in my universe for which I am aware include: GIII, GMAN, RUE: underwriting 8. Piper Jaffray received non-investment banking securities-related compensation from the following companies during the past 12 months: none 9. Piper Jaffray makes a market in the securities of the following companies, and will buy and sell the securities of these companies on a principal basis: CROX, CTRN, DECK, GIII, HOTT, PSUN, ROST, VLCM, WTSLA, ZUMZ 10. Piper Jaffray usually provides bids and offers for the securities of the following companies and will, from time to time, buy and sell the securities of these companies on a principal basis: ANF, ARO, AEO, GCO, GES, GPS, JCG, JCP, KSS, PVH, RL, RUE, TGT, UA, VFC, WRC, ZQK 3

4 CONSUMER SECTOR INVESTMENT RISKS Risks include, but are not limited to: Reliance on key top management Changing consumer preferences; brand relevance Cycle transitions & seasonality Changes in input costs & raw materials; manufacturing risk Markdown risk Product flow; inventory disruptions; product recalls; health & safety concerns Competition; lack of pricing power Deleveraging of fixed expenses, R&D, and design costs Foreign exchange rate risk Government regulation Weather General macroeconomic uncertainty 4

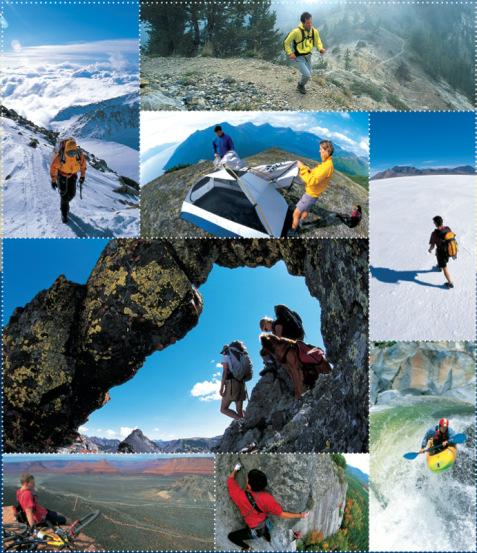

5 EXECUTIVE SUMMARY Thesis Declining asset values, combined with high unemployment rates and decreased access to capital, will continue to influence consumption of discretionary categories in 2011 as well as While difficult to predict, we think it s important to consider current trends in consumer spending, management outlook, and consumer psychology/demographics. We favor companies targeting high-income households and companies that offer value to middle-income consumers. Macroeconomic Trends Employment Situation Income Statement of the Consumer Balance Sheet of the Consumer Confidence of the Consumer Outdoor Industry Economic Sentiment Expectations Back-To To-School Implications for Holiday Opportunities: The Next Generation Consumer & International 5

6 EMPLOYMENT INITIAL UNEMPLOYMENT CLAIMS Initial unemployment claims down 15% year-over-year; Rolling 4 week numbers at 465k, have been rising since late-march 6

7 EMPLOYMENT TEMPORARY VS. NON-FARM PAYROLLS Temporary employment remains solid, up +22.1% Y/Y and up +0.8% in August; Y/Y growth in Non-Farm payrolls up +0.2% in August, second consecutive positive month 7

8 EMPLOYMENT REAL PCE VS. REAL HOURLY WAGE GROWTH Real hourly earnings up 0.7% y/y, down sequentially in July at -0.2%; Real PCE continues to move higher as July up 1.9% y/y. 8

9 DEBT SERVICE AND FINANCIAL OBLIGATION RATIOS Debt service at lowest levels since 2000; consumer has capacity to borrow 9

10 CONSUMER CAPACITY TO SPEND Income Statement for the consumer is improving, confidence will be next step 10

11 CONSUMER CONFIDENCE EXPECTATIONS Confidence Expectations Index has a.68 correlation with retail sales ex-autos w/ 6mo lead 11

12 PERSONAL SAVINGS RATE Personal Savings Rate continues to move higher after years of declines 12

13 HOME PRICES Home prices have declined y/y in 33 of the last 34 months 13

14 HOUSEHOLD NET WORTH Household net worth increased in Q409 to Q210 y/y after 7 quarters of y/y declines 14

15 SPENDING PATTERNS Spending on health care is displacing spending on discretionary categories such as clothing/footwear and furniture/equipment 15

16 DISPARITY IN INCOME GROWTH BY QUARTILE Wage Growth By Income Quintile 5.0% 4.0% 3.0% 2.0% 1.0% 0.0% -1.0% -2.0% May-10 Mar-07 May-07 Jul-07 Sep-07 Nov-07 Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09 Mar-09 May-09 Jul-09 Sep-09 Nov-09 Jan-10 Mar-10 Source: IRS, Piper Jaffray & Co. Highest Quintile Fourth Quintile Middle Quintile 16

17 HIGH-INCOME CONSUMER WAGE GROWTH OFFSETS TAXES THE 800-POUND DONKEY IN THE ROOM INCREMENTAL TAX BURDEN IN A POST-BUSH-TAX-CUT ERA Adjusted Gross Income Taxable Income Marginal Marginal Taxes Incremental AGI/Hhld Incr. Tax By Household Bracket Up To $250K* Tax Base (+460bps) Taxes/Hhld By Bracket % AGI $200,000 under $500,000 $693,238,200 $96,779,951 $4,451,878 $1,284 $227, % $500,000 under $1,000, ,669, ,907,915 8,689,764 15, , % $1,000,000 under $1,500,000 34,915, ,770,193 5,141,429 36,814 1,050, % $1,500,000 under $2,000,000 14,769,500 74,224,112 3,414,309 57,793 1,506, % $2,000,000 under $5,000,000 21,422, ,966,926 9,382, ,495 2,630, % $5,000,000 under $10,000,000 5,309, ,756,355 5,692, ,047 6,077, % $10,000,000 or more 3,350, ,888,323 15,864,863 1,183,680 25,982, % Total ($200K +) 916,674,450 $1,144,293,775 $52,637,514 $12,073 $472, % *Except the $200K under $500K bracket, in which we assumed $200K. All dollars in thousands, except household data; based on 2008 tax year. Source: IRS, Piper Jaffray & Co. research 17

18 RETAIL SALES TRENDS RETAIL SALES EX. AUTO (SA) VS. PRIOR YEARS 2009 vs. Prior Years 2010 vs. Prior Years ($ BILLIONS) January % -0.7% -2.9% -7.6% 14.0% 4.1% 1.8% -3.1% 4.9% February % -0.2% -2.6% -6.3% 14.2% 5.1% 2.5% -1.4% 5.3% March % -1.7% -5.1% -8.3% 15.4% 6.3% 2.5% -0.9% 8.1% April % -2.2% -4.3% -9.1% 14.2% 5.9% 3.6% -1.6% 8.3% May % -1.5% -5.2% -9.3% 13.3% 4.6% 0.6% -3.7% 6.1% June % -0.2% -3.4% -9.2% 12.0% 4.7% 1.3% -4.7% 4.9% July % -0.8% -4.3% -9.8% 12.0% 4.5% 0.8% -5.0% 5.3% August % -0.4% -2.9% -7.5% 11.1% 4.6% 2.0% -2.9% 5.0% September % 1.1% -3.0% -6.0% October % 1.3% -3.4% -3.2% November % 2.7% -4.1% 1.9% December % 1.3% -3.3% 5.8% Total 2,188 2,250 2,315 2,424 2,602 2,806 2,983 3,096 3,167 2, % -0.1% -3.7% -5.9% % Change 2.8% 2.9% 4.7% 7.3% 7.8% 6.3% 3.8% 2.3% -5.9% DPI* 7,327 7,649 8,010 8,378 8,889 9,277 9,916 10,403 10,806 10,924 % Change 4.4% 4.7% 4.6% 6.1% 4.4% 6.9% 4.9% 3.9% 1.1% % of DPI 30% 29% 29% 29% 29% 30% 30% 30% 29% 27% *Disposable Personal Income Source: Census Bureau and Bureau of Economic Analysis Retail sales have increased +6.1% YTD after steep decline in 2009; still below 2008 levels 18

19 RETAIL APPAREL SALES TRENDS TOTAL RETAIL CLOTHING STORE SALES (SA) VS. PRIOR YEARS 2009 vs. Prior Years 2010 vs. Prior Years ($ BILLIONS) January % -0.6% -6.8% -7.3% 8.9% 1.3% -5.0% -5.5% 1.9% February % 2.5% -2.4% -2.8% 7.7% 3.4% -1.6% -2.0% 0.8% March % -0.4% -7.5% -7.0% 13.2% 6.0% -1.5% -1.0% 6.4% April % -2.2% -5.4% -7.5% 9.5% 4.1% 0.7% -1.5% 6.5% May % -1.1% -6.8% -7.1% 9.6% 3.7% -2.3% -2.5% 4.9% June % -3.1% -6.7% -8.2% 7.7% 2.9% -1.0% -2.5% 6.2% July % -2.7% -6.7% -7.2% 9.6% 2.2% -2.0% -2.5% 5.0% August % -0.8% -4.7% -5.3% 9.1% 3.8% -0.3% -0.9% 4.7% September % -3.8% -4.8% -0.1% October % -3.7% -5.4% 1.4% November % -2.2% -6.7% 1.0% December % -6.0% -6.1% 3.1% Total % -2.0% -5.8% -4.0% % Change 0.2% 2.8% 3.4% 6.0% 6.0% 6.2% 4.0% -1.9% -4.0% DPI* 7,327 7,649 8,010 8,378 8,889 9,277 9,916 10,403 10,806 10,924 11,229 % Change 4.4% 4.7% 4.6% 6.1% 4.4% 6.9% 4.9% 3.9% 1.1% 2.8% % Apparel 2.3% 2.2% 2.2% 2.1% 2.1% 2.2% 2.1% 2.1% 2.0% 1.9% 1.9% *Disposable Personal Income Represents declining investment in apparel Source: Census Bureau and Bureau of Economic Analysis Est. apparel $s '10: % change from '09 2.8% 19

20 MACROECONOMIC REVIEW Thesis Declining asset values, combined with high unemployment rates and decreased access to capital, continue to influence consumption of discretionary categories in 2010 as we believe it is impacting the consumer psychology and confidence. Macroeconomic Trends Employment situation is improving, but not as quickly as was initially hoped Consumer has the capacity to spend, but will they? Home prices and net worth improving, but partially driven by stimulus Confidence will be key driver of consumer spending Non-Discretionary spending increasing as a portion of total Retail Sales excluding autos remains below 2008 levels 20

21 ECONOMIC CONCERN FROM OIA COMMUNITY Respondents Very Concerned About the Economy 60% 50% 47% 57% 55% 40% 37% 37% 30% 20% 23% 10% 0% Fall '08 Spring '09 Summer '09 Fall '09 Winter '09 Spring '10 Source: Piper Jaffray & Co. 21

22 EXPECTATIONS FROM OIA COMMUNITY Expectations Index Spring '09 Summer '09 Fall '09 Winter '09 Spring '10 14% 12% 10% 8% 6% 4% 2% 0% -2% Source: Piper Jaffray & Co. Expectations Index 22 Q/Q Change

23 RETAIL SALES TRENDS Source: Census Bureau, Piper Jaffray & Co. Strong August retail sales suggests holiday sales growth ~ +5% Y/Y 23

24 IDENTIFYING POTENTIAL OPPORTUNITIES Piper Jaffray Taking Stock with Teens Survey Spending by category (apparel, food, entertainment, etc.) Total spending per teen Market size for apparel and footwear products Brand preferences Environmental awareness Higher Profitability in International Markets Favorable operating margin differential Higher price points 24

25 TEEN SPENDING BY CATEGORY 25

26 TEEN MARKET SIZE X = $71 billion 28.2 million $2,500/person Apparel Shoes Accessories = 39% $71 billion X = 39% 39% $28 billion Source: Census Bureau and Piper Jaffray & Co. 26

27 TEEN SPENDING ON FASHION PER TEEN 27

28 BRANDS TEENS PREFER IN ATHLETIC/PERFORMANCE APPAREL PREFERRED ATHLETIC CLOTHING BRAND - UPPER INCOME STUDENT SURVEY Fall 2010 Spring 2010 Fall 2009 Spring 2009 Fall 2008 Rank Sport % Total Rank Sport % Total Rank Sport % Total Rank Sport % Total Rank Sport % Total 1 Nike 51% 1 Nike 47% 1 Nike 48% 1 Nike 43% 1 Nike 38% 2 Under Armour 18% 2 Under Armour 25% 2 Under Armour 25% 2 Under Armour 26% 2 Under Armour 23% 3 adidas 6% 3 adidas 7% 3 adidas 6% 3 adidas 6% 3 adidas 8% 4 The North Face 2% 4 The North Face 3% 4 Soffe 2% 4 The North Face 4% 4 Puma 3% 5 Mizuno 1% 5 Soffe 2% 5 Jordan 2% 5 Champion 2% 5 Jordan 1% Puma 2% PREFERRED ATHLETIC CLOTHING BRAND (F) - UPPER INCOME STUDENT SURVEY Fall 2010 Spring 2010 Fall 2009 Spring 2009 Fall 2008 Rank Sport % Total Rank Sport % Total Rank Sport % Total Rank Sport % Total Rank Sport % Total 1 Nike 49% 1 Nike 48% 1 Nike 46% 1 Nike 41% 1 Nike 39% 2 Under Armour 16% 2 Under Armour 19% 2 Under Armour 23% 2 Under Armour 26% 2 Under Armour 18% 3 Adidas 7% 3 adidas 8% 3 adidas 7% 3 adidas 6% 3 adidas 10% 4 The North Face 2% 4 The North Face 4% 4 Soffe 3% 4 The North Face 5% 4 Soffe 4% 5 Mizuno 2% 5 Soffe 3% 5 The North Face 2% 5 Champion 2% 5 Puma 4% PREFERRED ATHLETIC CLOTHING BRAND (M) - UPPER INCOME STUDENT SURVEY Fall 2010 Spring 2010 Fall 2009 Spring 2009 Fall 2008 Rank Sport % Total Rank Sport % Total Rank Sport % Total Rank Sport % Total Rank Sport % Total 1 Nike 52% 1 Nike 46% 1 Nike 49% 1 Nike 46% 1 Nike 38% 2 Under Armour 19% 2 Under Armour 30% 2 Under Armour 27% 2 Under Armour 26% 2 Under Armour 29% 3 Adidas 6% 3 adidas 5% 3 adidas 5% 3 adidas 6% 3 adidas 7% 4 The North Face 2% 4 Jordan 2% 4 Jordan 2% 4 The North Face 3% 4 Jordan 2% 5 Jordan 2% 5 Puma 1% 5 Reebok 1% 5 Puma 2% 5 Reebok 1% Puma 1% Source: Piper Jaffray & Co. 28

29 TEENS CONCERNED ABOUT GLOBAL WARMING 29

30 TEENS WHO RECYCLE AT HOME 30

31 TEENS WHO HAVE PURCHASED ORGANIC PRODUCTS 31

32 TEENS WILLING TO PAY MORE FOR ORGANIC 32

33 YOUNG ADULT POPULATION CONTINUES TO GROW Population Trend year old age group Millions of persons % CAGR U.S. Census Bureau & NCHS Compared to 0.85% estimated growth rate for total U.S. population from

34 INT L REVENUE VS. INT L OPERATING INCOME 34

35 REVIEW OF OPPORTUNITIES SUMMARY 1) Teen and youth markets - Teens spend about $28B annually on discretionary categories - Demographics favor young adult, growth exceeds rest of population - Teens care about the environment 2) Higher profitability in international markets - Higher margins and price points 35

36 Analyst Certification Jeff P. Klinefelter, Senior Research Analyst, Sean P. Naughton, CFA, Senior Research Analyst The views expressed in this report accurately reflect my personal views about the subject company and the subject security. In addition, no part of my compensation was, is, or will be directly or indirectly related to the specific recommendations or views contained in this report. Affiliate Disclosures: This report has been prepared by Piper Jaffray & Co. and/or its affiliates Piper Jaffray Ltd., and Piper Jaffray Asia Securities Limited, all of which are subsidiaries of Piper Jaffray Companies (collectively Piper Jaffray). Piper Jaffray & Co. is regulated by FINRA, NYSE and the United States Securities and Exchange Commission, and its headquarters is located at 800 Nicollet Mall, Minneapolis, MN Piper Jaffray Ltd. is registered in England, no , and its headquarters is located at One South Place, London, EC2M 2RB. Piper Jaffray Ltd. is authorised and regulated by the UK Financial Services Authority ( FSA ), entered on the FSA's register, no and is a member of the London Stock Exchange. Piper Jaffray Asia Securities Limited is a licensed corporation regulated by the Securities and Futures Commission of Hong Kong ( SFC ), entered on the SFC s register, no. ABO154, and is an exchange participant of The Stock Exchange of Hong Kong Limited. Its headquarters is located at 39/F Tower 1 Lippo Centre, 89 Queensway, Hong Kong. Disclosures in this section and in the Other Important Information section referencing Piper Jaffray include all affiliated entities unless otherwise specified. Piper Jaffray research analysts receive compensation that is based, in part, on the firm's overall revenues, which include investment banking revenues. Ratings and Other Definitions Stock Ratings: Piper Jaffray ratings are indicators of expected total return (price appreciation plus dividend) within the next 12 months. At times analysts may specify a different investment horizon or may include additional investment time horizons for specific stocks. Stock performance is measured relative to the group of stocks covered by each analyst. Lists of the stocks covered by each are available at Stock ratings and/or stock coverage may be suspended from time to time in the event that there is no active analyst opinion or analyst coverage, but the opinion or coverage is expected to resume. Research reports and ratings should not be relied upon as individual investment advice. As always, an investor s decision to buy or sell a security must depend on individual circumstances, including existing holdings, time horizons and risk tolerance. Piper Jaffray sales and trading personnel may provide written or oral commentary, trade ideas, or other information about a particular stock to clients or internal trading desks reflecting different opinions than those expressed by the research analyst. In addition, Piper Jaffray technical research products are based on different methodologies and may contradict the opinions contained in fundamental research reports. Overweight (OW): Anticipated to outperform relative to the median of the group of stocks covered by the analyst. Neutral (N): Anticipated to perform in line relative to the median of the group of stocks covered by the analyst. Underweight (UW): Anticipated to underperform relative to the median of the group of stocks covered by the analyst. An industry outlook represents the analyst s view of the industry represented by the stocks in the analyst s coverage group. A Favorable industry outlook generally means that the analyst expects the fundamentals and/or valuations of the industry to improve over the investment time horizon. A Neutral industry outlook generally means that the analyst does not expect the fundamentals and/or valuations of the industry to either improve or deteriorate meaningfully from its current state. An Unfavorable industry outlook generally means that the analyst expects the fundamentals and/or valuations of the industry to deteriorate meaningfully over the investment time horizon.

37 Piper Jaffray does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decisions. This report should be read in conjunction with important disclosure information, including an attestation under Regulation Analyst Certification, found at the following site: Other Important Information The material regarding the subject company is based on data obtained from sources deemed to be reliable; it is not guaranteed as to accuracy and does not purport to be complete. This report is solely for informational purposes and is not intended to be used as the primary basis of investment decisions. Piper Jaffray has not assessed the suitability of the subject company for any person. Because of individual client requirements, it is not, and it should not be construed as, advice designed to meet the particular investment needs of any investor. This report is not an offer or the solicitation of an offer to sell or buy any security. Unless otherwise noted, the price of a security mentioned in this report is the market closing price as of the end of the prior business day. Piper Jaffray does not maintain a predetermined schedule for publication of research and will not necessarily update this report. Piper Jaffray policy generally prohibits research analysts from sending draft research reports to subject companies; however, it should be presumed that the analyst(s) who authored this report has had discussions with the subject company to ensure factual accuracy prior to publication, and has had assistance from the company in conducting diligence, including visits to company sites and meetings with company management and other representatives. This report is published in accordance with a conflicts management policy, which is available at Notice to customers: This material is not directed to, or intended for distribution to or use by, any person or entity if Piper Jaffray is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available to such person or entity. Customers in any of the jurisdictions where Piper Jaffray and its affiliates do business who wish to effect a transaction in the securities discussed in this report should contact their local Piper Jaffray sales representative. Europe: This material is for the use of intended recipients only and only for distribution to professional and institutional investors, i.e. persons who are authorized persons or exempted persons within the meaning of the Financial Services and Markets Act 2000 of the United Kingdom, or persons who have been categorized by Piper Jaffray Ltd. as professional clients under the rules of the Financial Services Authority. Asia: This report is distributed in Hong Kong by Piper Jaffray Asia Securities Limited, which is regulated by the Hong Kong SFC. This report is intended only for distribution to professional investors as defined in the Hong Kong Securities and Futures Ordinance and is for the use of intended recipients only. United States: This report is distributed in the United States by Piper Jaffray & Co., member SIPC, FINRA and NYSE, Inc., which accepts responsibility for its contents. The securities described in this report may not have been registered under the U.S. Securities Act of 1933 and, in such case, may not be offered or sold in the United States or to U.S. persons unless they have been so registered, or an exemption from the registration requirements is available. This report is produced for the use of Piper Jaffray customers and may not be reproduced, re-distributed or passed to any other person or published in whole or in part for any purpose without the written consent of Piper Jaffray. Additional information is available upon request Piper Jaffray. All rights reserved.

Grains, Beans and Farmland: The True Diversifiers

Grains, Beans and Farmland: The True Diversifiers Sumit Roy, Moderator Managing Editor HardAssetsInvestor.com Greyson Colvin, Panelist Managing Partner Colvin & Co Michael Cox, Panelist Managing Partner,

Grains, Beans and Farmland: The True Diversifiers Sumit Roy, Moderator Managing Editor HardAssetsInvestor.com Greyson Colvin, Panelist Managing Partner Colvin & Co Michael Cox, Panelist Managing Partner,

Presentation to the Petroleum Equipment & Services Association

April 2018 Presentation to the Petroleum Equipment & Services Association April 26, 2018 John M. Daniel SENIOR EQUITY RESEARCH ANALYST Tel: +1 713-546-7215 Email: john.m.daniel@pjc.com John H. Watson SENIOR

April 2018 Presentation to the Petroleum Equipment & Services Association April 26, 2018 John M. Daniel SENIOR EQUITY RESEARCH ANALYST Tel: +1 713-546-7215 Email: john.m.daniel@pjc.com John H. Watson SENIOR

Xcel Energy (Baa3/BBB-)

") January 28, 2004 Fixed Income Research Recommendation: Market Perform Credit Trend: Improving Jacob P. Mercer, CFA Senior Research Analyst 612-303-1609 jacob.p.mercer@pjc.com Mark D. Churchill Associate

January 28, 2004 Fixed Income Research Recommendation: Market Perform Credit Trend: Improving Jacob P. Mercer, CFA Senior Research Analyst 612-303-1609 jacob.p.mercer@pjc.com Mark D. Churchill Associate

(712 HK - HK$2.47) Comtec. Overweight. More New Orders to Provide Downside Protection. Company Note 5 October 2010

Comtec. Overweight. More New Orders to Provide Downside Protection. Company Note 5 October 2010") COMPANY BACKGROUND, which commenced its solar business in 2004, manufactures and sells monocrystalline wafers to solar cell manufacturers worldwide. Based in Nanhui District, Shanghai, it had 741 employees

COMPANY BACKGROUND, which commenced its solar business in 2004, manufactures and sells monocrystalline wafers to solar cell manufacturers worldwide. Based in Nanhui District, Shanghai, it had 741 employees

Fufeng Group Ltd. Overweight

COMPANY BACKGROUND Founded in 1999, Fufeng Group (Fufeng) is the largest manufacturer of glutamic acid (GA) (raw material for monosodium glutamate, or MSG) with a 30% market share in China, and one of

COMPANY BACKGROUND Founded in 1999, Fufeng Group (Fufeng) is the largest manufacturer of glutamic acid (GA) (raw material for monosodium glutamate, or MSG) with a 30% market share in China, and one of

Fufeng Group Ltd. Overweight. (Continued on page 2)

") COMPANY BACKGROUND Founded in 1999, Fufeng Group (Fufeng) is the largest manufacturer of glutamic acid (GA) (raw material for monosodium glutamate, or MSG) with a 30% market share in China, and one of

COMPANY BACKGROUND Founded in 1999, Fufeng Group (Fufeng) is the largest manufacturer of glutamic acid (GA) (raw material for monosodium glutamate, or MSG) with a 30% market share in China, and one of

The Software Field Guide Volume 3, Number 5 Subscribe at softwaresubscribe

C. Eugene Munster Senior Research Analyst, Security & Design 612-303-6452, gene.a.munster@pjc.com Tad W. Piper, CFA Senior Research Analyst, Software Applications 650-838-1393, tad.w.piper@pjc.com David

C. Eugene Munster Senior Research Analyst, Security & Design 612-303-6452, gene.a.munster@pjc.com Tad W. Piper, CFA Senior Research Analyst, Software Applications 650-838-1393, tad.w.piper@pjc.com David

A Giant Producer, & An Emerging Giant Consumer/Investor. Hong Liang

A Giant Producer, & An Emerging Giant Consumer/Investor China s Role in Global Trade and Investment Hong Liang Chief Economist, Head of Research October, 2016 I China: A global manufacturing power house,

A Giant Producer, & An Emerging Giant Consumer/Investor China s Role in Global Trade and Investment Hong Liang Chief Economist, Head of Research October, 2016 I China: A global manufacturing power house,

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

ECONOMIC CALENDAR 2010

J.P. Morgan ECONOMIC CALENDAR 2010 Release dates for US economic indicators and Treasury auctions J.P. Morgan ECONOMIC CALENDAR 2010 Release dates for US economic indicators and Treasury auctions This

J.P. Morgan ECONOMIC CALENDAR 2010 Release dates for US economic indicators and Treasury auctions J.P. Morgan ECONOMIC CALENDAR 2010 Release dates for US economic indicators and Treasury auctions This

Fufeng Group Ltd. Overweight

22 March 211 COMPANY BACKGROUND Founded in 1999, Fufeng Group (Fufeng) is the largest manufacturer of glutamic acid (GA) (raw material for monosodium glutamate, or MSG) with a 3% market share in China,

22 March 211 COMPANY BACKGROUND Founded in 1999, Fufeng Group (Fufeng) is the largest manufacturer of glutamic acid (GA) (raw material for monosodium glutamate, or MSG) with a 3% market share in China,

Economy On The Rebound

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

10 County Conference. Richard Wobbekind. Executive Director Business Research Division & Senior Associate Dean Leeds School of Business

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

THE BLUE SKY REPORT A KERRIGAN QUARTERLY. Third Quarter 2018 December 2018

THE BLUE SKY REPORT A KERRIGAN QUARTERLY Third Quarter 2018 December 2018 Contact Erin Kerrigan: (949) 439-6768 erin@kerriganadvisors.com Contact Ryan Kerrigan: (949) 728-8849 ryan@kerriganadvisors.com

THE BLUE SKY REPORT A KERRIGAN QUARTERLY Third Quarter 2018 December 2018 Contact Erin Kerrigan: (949) 439-6768 erin@kerriganadvisors.com Contact Ryan Kerrigan: (949) 728-8849 ryan@kerriganadvisors.com

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States?

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Global economy maintaining solid growth momentum. Canada leading the pack

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Economic Overview. Melissa K. Peralta Senior Economist April 27, 2017

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

More of the Same; Or now for Something Completely Different?

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

The U.S. Economic Outlook

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder Member FDIC VectraBank.com Economic Outlook 2015 Richard

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder Member FDIC VectraBank.com Economic Outlook 2015 Richard

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Trends. September 10, 2013

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Carol Tomé CFO and Executive Vice President, Corporate Services

Carol Tomé CFO and Executive Vice President, Corporate Services Financial Overview December 6, 2017 1 Discussion Overview Fiscal 2017 Financial Guidance Our View of the Economy and State of the U.S. Housing

Carol Tomé CFO and Executive Vice President, Corporate Services Financial Overview December 6, 2017 1 Discussion Overview Fiscal 2017 Financial Guidance Our View of the Economy and State of the U.S. Housing

Big Changes, Unknown Impacts

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

The China Analyst: Wireless Sector Becoming Increasingly Positive; Time To Buy

Safa Rashtchy, Senior Research Analyst 650 838-1347, safa.a.rashtchy@pjc.com Aaron M. Kessler, Sr Research Analyst 650 838-1434, aaron.m.kessler@pjc.com Reason for Report: Industry Overview Related Companies:

Safa Rashtchy, Senior Research Analyst 650 838-1347, safa.a.rashtchy@pjc.com Aaron M. Kessler, Sr Research Analyst 650 838-1434, aaron.m.kessler@pjc.com Reason for Report: Industry Overview Related Companies:

A comment on recent events, and...

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

Europe June Craig Menear. Chairman, CEO & President. Diane Dayhoff. Vice President, Investor Relations

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

Presentation half-year results 2012

Presentation half-year results 2012 Okura Hotel, Amsterdam 26 July 2012 René J. Takens, CEO Hielke H. Sybesma, CFO Jeroen M. Snijders Blok, COO Agenda 1. Accell Group in H1 2012 2. Accell Group share 3.

Presentation half-year results 2012 Okura Hotel, Amsterdam 26 July 2012 René J. Takens, CEO Hielke H. Sybesma, CFO Jeroen M. Snijders Blok, COO Agenda 1. Accell Group in H1 2012 2. Accell Group share 3.

How to Explain Car Rental to Banks and Investors

How to Explain Car Rental to Banks and Investors Scott White Senior Managing Director, Head of Investment Banking C.L. King & Associates March 8-9, 2011 Las Vegas Hilton 1 My Background 18 Years Advising

How to Explain Car Rental to Banks and Investors Scott White Senior Managing Director, Head of Investment Banking C.L. King & Associates March 8-9, 2011 Las Vegas Hilton 1 My Background 18 Years Advising

5. Golf Industry Trends and Developments in the US 6. The US Macro Economy Factors and Impact over Golf Industry

TABLE OF CONTENTS 1. Golf Industry Performance Worldwide 1.1. Overview 1.2. Global Golf Equipment Demand and Economy 2. The US Golf Industry Overview 2.1. Industry Segmentation 3. Industry Performance

TABLE OF CONTENTS 1. Golf Industry Performance Worldwide 1.1. Overview 1.2. Global Golf Equipment Demand and Economy 2. The US Golf Industry Overview 2.1. Industry Segmentation 3. Industry Performance

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office The views expressed in this presentation are strictly those of the author and do not necessarily

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office The views expressed in this presentation are strictly those of the author and do not necessarily

The Global Economy: Sustaining Momentum

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

Global economy s strong momentum intact despite elevated level of uncertainty. Canada headed for another year of solid growth

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

SA economic review Kevin Lings. August 2018

SA economic review Kevin Lings August 2018 South Africa real GDP growth year-on-year %y/y 8 7 6 5 Ave 4.3% 4 Ave 2.5% 3 2 Ave 0.9% 1 0-1 -2-3 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 2

SA economic review Kevin Lings August 2018 South Africa real GDP growth year-on-year %y/y 8 7 6 5 Ave 4.3% 4 Ave 2.5% 3 2 Ave 0.9% 1 0-1 -2-3 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 2

Economic Outlook for Canada: Economy Confronting Capacity Limits

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

ABA Commercial Real Estate Lending Committee

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

The U.S. Economic Outlook

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

The Wisconsin and Minnesota Economies: What can we learn from each other? Noah Williams

The Economies: What can we learn from each other? Noah University of Wisconsin - Madison Future Wisconsin Summit 2016 Economies Location, size, demographics, and history make Wisconsin and Minnesota natural

The Economies: What can we learn from each other? Noah University of Wisconsin - Madison Future Wisconsin Summit 2016 Economies Location, size, demographics, and history make Wisconsin and Minnesota natural

U.S. Economy in a Snapshot

U.S. Economy in a Snapshot Economic Press Briefing: May 19, 2016 The views expressed here are those of the presenter and do not necessarily represent the views of the Federal Reserve Bank of New York or

U.S. Economy in a Snapshot Economic Press Briefing: May 19, 2016 The views expressed here are those of the presenter and do not necessarily represent the views of the Federal Reserve Bank of New York or

Pacific Sunwear. 35th Annual Bank of America Consumer Conference

Pacific Sunwear 35th Annual Bank of America Consumer Conference Safe Harbor Disclaimer This presentation will include forward looking statements within the meaning of the safe harbor provisions of Federal

Pacific Sunwear 35th Annual Bank of America Consumer Conference Safe Harbor Disclaimer This presentation will include forward looking statements within the meaning of the safe harbor provisions of Federal

Zions Bank Economic Overview

Zions Bank Economic Overview Kenworth National Dealers Conference November 8, 2018 1 National Economic Conditions 2 Volatility Returns to the Stock Market 27,000 Dow Jones Industrial Average October 10,

Zions Bank Economic Overview Kenworth National Dealers Conference November 8, 2018 1 National Economic Conditions 2 Volatility Returns to the Stock Market 27,000 Dow Jones Industrial Average October 10,

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

11 th Annual Oregon Economic Forum!

11 th Annual Oregon Economic Forum! (almost) Beyond! Macroeconomics Portland, OR! October 16, 2014! Expansion Continues! Five Years and More!! Recession Indicators Nonfarm Payrolls Real Personal Income

11 th Annual Oregon Economic Forum! (almost) Beyond! Macroeconomics Portland, OR! October 16, 2014! Expansion Continues! Five Years and More!! Recession Indicators Nonfarm Payrolls Real Personal Income

Economic & Market Outlook

Economic & Market Outlook August 2017 The investments described herein are: NOT FDIC INSURED NOT BANK GUARANTEED MAY LOSE VALUE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL OR STATE GOVERNMENT AGENCY Average

Economic & Market Outlook August 2017 The investments described herein are: NOT FDIC INSURED NOT BANK GUARANTEED MAY LOSE VALUE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL OR STATE GOVERNMENT AGENCY Average

Washington Public Ports Association

May 17, 2017 Washington Public Ports Association Underwriting Process Lindsay Sovde MANAGING DIRECTOR Tel: +1 206-628-2875 Email: lindsay.a.sovde@pjc.com MINNEAPOLIS BOISE CHICAGO LONDON LOS ANGELES NEW

May 17, 2017 Washington Public Ports Association Underwriting Process Lindsay Sovde MANAGING DIRECTOR Tel: +1 206-628-2875 Email: lindsay.a.sovde@pjc.com MINNEAPOLIS BOISE CHICAGO LONDON LOS ANGELES NEW

Zions Bank Economic Overview

Zions Bank Economic Overview Intermountain Credit Education League May 10, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around

Zions Bank Economic Overview Intermountain Credit Education League May 10, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around

Muhlenkamp & Company. Webinar December 1, Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Canada s economy on track for a solid 2018 although policy uncertainty lingers

Canada s economy on track for a solid 2018 although policy uncertainty lingers Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com March 2018 Canada is facing a challenging

Canada s economy on track for a solid 2018 although policy uncertainty lingers Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com March 2018 Canada is facing a challenging

The Great Economic Reset

The Great Economic Reset CMTA Annual Conference Squaw Creek Lake Tahoe April 13, 2016 Presented by Douglas C. Robinson, RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory

The Great Economic Reset CMTA Annual Conference Squaw Creek Lake Tahoe April 13, 2016 Presented by Douglas C. Robinson, RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory

Charting a Path to Lift Off? Understanding the Shifting Economic Winds

Charting a Path to Lift Off? Understanding the Shifting Economic Winds Thomas F. Siems, Ph.D. Assistant Vice President and Senior Economist Federal Reserve Bank of Dallas Government Finance Officers Arlington,

Charting a Path to Lift Off? Understanding the Shifting Economic Winds Thomas F. Siems, Ph.D. Assistant Vice President and Senior Economist Federal Reserve Bank of Dallas Government Finance Officers Arlington,

MUSTAFA MOHATAREM Chief Economist, General Motors

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

Agriculture and the Economy: A View from the Chicago Fed

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Future Global Trade Trends - Risks & Opportunities. Pulse of the Ports: Peak Season Forecast March 21, 2013

1 Future Global Trade Trends - Risks & Opportunities Pulse of the Ports: Peak Season Forecast March 21, 2013 June 2012 Dr. Walter Kemmsies Chief Economist Summary Higher economic growth in 2013, possible

1 Future Global Trade Trends - Risks & Opportunities Pulse of the Ports: Peak Season Forecast March 21, 2013 June 2012 Dr. Walter Kemmsies Chief Economist Summary Higher economic growth in 2013, possible

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

North American Forging Shipment Forecast (Using FIA bookings information through December 2013)

") North American Forging Shipment Forecast 2014-2018 (Using FIA bookings information through December 2013) Percent Change Year Ago Best leading indicator combination for impression die bookings used to

North American Forging Shipment Forecast 2014-2018 (Using FIA bookings information through December 2013) Percent Change Year Ago Best leading indicator combination for impression die bookings used to

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

Colorado Economic Update

Colorado Economic Update Steamboat Economic Summit Place cover image here Brian Lewandowski Associate Director, Business Research Division October 21, 2016 Recession 8 Months Recession 18 Months Real GDP

Colorado Economic Update Steamboat Economic Summit Place cover image here Brian Lewandowski Associate Director, Business Research Division October 21, 2016 Recession 8 Months Recession 18 Months Real GDP

The United States: Fiscal Facts and Fantasies. Presented by: Nigel Gault Chief U.S. Economist IHS Global Insight

The United States: Fiscal Facts and Fantasies Presented by: Nigel Gault Chief U.S. Economist IHS Global Insight Subdued Recovery: Tailwinds Battling Headwinds The U.S. Recovery: Tailwinds More sectors

The United States: Fiscal Facts and Fantasies Presented by: Nigel Gault Chief U.S. Economist IHS Global Insight Subdued Recovery: Tailwinds Battling Headwinds The U.S. Recovery: Tailwinds More sectors

The Anatomy of Bull and Bear Markets. Tom Vernon/James Hutton

The Anatomy of Bull and Bear Markets Tom Vernon/James Hutton Recent market correction in context of long-term returns S&P 500 2900 DURATION: 9 DAYS 2850 2800 2750 2700 2650 MAGNITUDE: -10.2% 2600 2550

The Anatomy of Bull and Bear Markets Tom Vernon/James Hutton Recent market correction in context of long-term returns S&P 500 2900 DURATION: 9 DAYS 2850 2800 2750 2700 2650 MAGNITUDE: -10.2% 2600 2550

Wenlin Liu, Senior Economist. Stateof Wyoming. Economic Analysis Division State of Wyoming 1

WYOMING DEMOGRAPHIC AND ECONOMIC TREND LCCC LIFE Program April 7, 2012 Cheyenne, Wyoming Wenlin Liu, Senior Economist Economic Analysis Division Stateof Wyoming Economic Analysis Division State of Wyoming

WYOMING DEMOGRAPHIC AND ECONOMIC TREND LCCC LIFE Program April 7, 2012 Cheyenne, Wyoming Wenlin Liu, Senior Economist Economic Analysis Division Stateof Wyoming Economic Analysis Division State of Wyoming

India: Can the Tiger Economy Continue to Run?

India: Can the Tiger Economy Continue to Run? India s GDP is on the rise US$ trillions Nominal GDP (left axis) GDP growth (right axis) 3.0 2.5 2.0 1.5 1.0 0.5 0.0 1990 1992 1994 1996 1998 2000 2002 2004

India: Can the Tiger Economy Continue to Run? India s GDP is on the rise US$ trillions Nominal GDP (left axis) GDP growth (right axis) 3.0 2.5 2.0 1.5 1.0 0.5 0.0 1990 1992 1994 1996 1998 2000 2002 2004

Shifting International Trade Routes A National Economic Outlook. February 1, 2011

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

The ABA Advantage: Economic Issues Update & ABA Resources

The ABA Advantage: Economic Issues Update & ABA Resources aba.com 1-800-BANKERS Meet the team Jim Chessen Chief Economist Curtis Dubay Senior Economist Brittany Kleinpaste Vice President of Economic Policy

The ABA Advantage: Economic Issues Update & ABA Resources aba.com 1-800-BANKERS Meet the team Jim Chessen Chief Economist Curtis Dubay Senior Economist Brittany Kleinpaste Vice President of Economic Policy

Market Update. Randy Tinseth Vice President, Marketing Boeing Commercial Airplanes. Copyright 2016 Boeing. All rights reserved.

Market Update The statements contained herein are based on good faith assumptions are to be used for general information purposes only. These statements do not constitute an offer, promise, warranty or

Market Update The statements contained herein are based on good faith assumptions are to be used for general information purposes only. These statements do not constitute an offer, promise, warranty or

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Interim Management Statement and Details of change to licensing arrangements for the Betting Exchange in the UK

8 th March 2011 Betfair Group plc ( Betfair ) Interim Management Statement and Details of change to licensing arrangements for the Betting Exchange in the UK Betfair (LSE:BET), the world s biggest betting

8 th March 2011 Betfair Group plc ( Betfair ) Interim Management Statement and Details of change to licensing arrangements for the Betting Exchange in the UK Betfair (LSE:BET), the world s biggest betting

The US Economic Outlook

IHS ECONOMICS US Outlook The US Economic Outlook November 2014 ihs.com Rafael Amiel, Director latin America Economics +1 215 789 7405, rafael.amiel.ihs.com 2014 IHS The US economy is gaining momentum Growth

IHS ECONOMICS US Outlook The US Economic Outlook November 2014 ihs.com Rafael Amiel, Director latin America Economics +1 215 789 7405, rafael.amiel.ihs.com 2014 IHS The US economy is gaining momentum Growth

Stock Market Handbook

Stock Market Handbook May 11, 212 Dr. Edward Yardeni 516-972-7683 eyardeni@ Sailesh S Radha 83-786-1368 jabbott@ Please visit our sites at www. blog. thinking outside the box Table Of Contents Table Of

Stock Market Handbook May 11, 212 Dr. Edward Yardeni 516-972-7683 eyardeni@ Sailesh S Radha 83-786-1368 jabbott@ Please visit our sites at www. blog. thinking outside the box Table Of Contents Table Of

Brookfield Asset Management O AK T R E E ACQUISITION M A R C H 1 3,

Brookfield Asset Management O AK T R E E ACQUISITION M A R C H 1 3, 2 0 19 Transaction Summary On March 13, 2019, Brookfield Asset Management ( BAM ) and Oaktree Capital Group ( OAK ) announced an agreement

Brookfield Asset Management O AK T R E E ACQUISITION M A R C H 1 3, 2 0 19 Transaction Summary On March 13, 2019, Brookfield Asset Management ( BAM ) and Oaktree Capital Group ( OAK ) announced an agreement

RBC Economics Financial Update Dawn Desjardins

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

BC Pension Forum. Economic Outlook. Presented by: Ben Homsy, CFA Portfolio Manager

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

SPECIAL DIVIDEND OF MUELLER INDUSTRIES, INC.

MUELLER INDUSTRIES, INC. SPECIAL DIVIDEND OF MUELLER INDUSTRIES, INC. This document is being provided to stockholders of Mueller Industries, Inc. (a corporation that we refer to as Mueller, we, our or

MUELLER INDUSTRIES, INC. SPECIAL DIVIDEND OF MUELLER INDUSTRIES, INC. This document is being provided to stockholders of Mueller Industries, Inc. (a corporation that we refer to as Mueller, we, our or

Economic Outlook. Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project

Economic Outlook Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project League of California Cities Monterey, CA December 3, 2014 Economic Update economic

Economic Outlook Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project League of California Cities Monterey, CA December 3, 2014 Economic Update economic

President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H. Parker Willis Lecture in Political Economics

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

From Recession to Recovery

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

2010 Credit Suisse Holiday Conference December 7, 2010

2010 Credit Suisse Holiday Conference December 7, 2010 Forward Looking Statements The Company claims the protection of the safe-harbor for forward-looking statements within the meaning of the Private Securities

2010 Credit Suisse Holiday Conference December 7, 2010 Forward Looking Statements The Company claims the protection of the safe-harbor for forward-looking statements within the meaning of the Private Securities

WORKFORCE LOCAL AREA EMPLOYMENT STATISTICS (LAUS)

") AUGUST 2018 WORKFORCE LOCAL AREA EMPLOYMENT STATISTICS (LAUS) 1,200,000 1,100,000 1,000,000 900,000 Labor Force Employment 1,152,626 1,116,938 800,000 700,000 600,000 500,000 2016 to 2017: 35957 (3.1%)

AUGUST 2018 WORKFORCE LOCAL AREA EMPLOYMENT STATISTICS (LAUS) 1,200,000 1,100,000 1,000,000 900,000 Labor Force Employment 1,152,626 1,116,938 800,000 700,000 600,000 500,000 2016 to 2017: 35957 (3.1%)

How Much Wind Is in the Sails?

How Much Wind Is in the Sails? Erie Chamber of Commerce Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations September 20, 2017 Real GDP Growth

How Much Wind Is in the Sails? Erie Chamber of Commerce Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations September 20, 2017 Real GDP Growth

Demographics, Debt, Dollar and Deflation Is the next Great Reset coming?

Demographics, Debt, Dollar and Deflation Is the next Great Reset coming? CMTA Advanced Investment Workshop January 28, 20145 Presented by Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered

Demographics, Debt, Dollar and Deflation Is the next Great Reset coming? CMTA Advanced Investment Workshop January 28, 20145 Presented by Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered

Spring Press Conference February 23, Name of chairman

Spring Press Conference February 23, 2006 Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward looking statements involve

Spring Press Conference February 23, 2006 Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward looking statements involve

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

THE MOST INFORMATIVE EVENT COVERING REAL ESTATE INVESTMENTS

THE MOST INFORMATIVE EVENT COVERING REAL ESTATE INVESTMENTS 2014 U.S. Economic, Capital Markets, and Retail Market Overview and Outlook Retail Trends 2014 U.S. Economic Overview and Outlook Total Employment

THE MOST INFORMATIVE EVENT COVERING REAL ESTATE INVESTMENTS 2014 U.S. Economic, Capital Markets, and Retail Market Overview and Outlook Retail Trends 2014 U.S. Economic Overview and Outlook Total Employment

Deutsche Bank. Consensus Report. 13 March 2018

Deutsche Bank Consensus Report 13 March 2018 Deutsche Bank Group P&L (in m) Average Minimum Maximum # est. Average Minimum Maximum # est. Average Minimum Maximum # est. Average Minimum Maximum # est. Revenues

Deutsche Bank Consensus Report 13 March 2018 Deutsche Bank Group P&L (in m) Average Minimum Maximum # est. Average Minimum Maximum # est. Average Minimum Maximum # est. Average Minimum Maximum # est. Revenues

Kevin Thorpe Financial Economist & Principal Cassidy Turley

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

Zions Bank Economic Overview

Zions Bank Economic Overview Veteran Owned Business Conference May 11, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around Correction

Zions Bank Economic Overview Veteran Owned Business Conference May 11, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around Correction

State of American Trucking

State of American Trucking October 11, 2018 Rod Suarez Economic Analyst American Trucking Associations rsuarez@trucking.org Business Cycles U.S. Expansions Duration October 1949 - July 1953 May 1954 -

State of American Trucking October 11, 2018 Rod Suarez Economic Analyst American Trucking Associations rsuarez@trucking.org Business Cycles U.S. Expansions Duration October 1949 - July 1953 May 1954 -

Reading the Tea Leaves: Investing for 2010 and Beyond

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

The U. S. Economic Outlook: Robert J. Gordon

The U. S. Economic Outlook: Upside and Risks Robert J. Gordon Ottawa a Economics Association Ottawa, a, September 14, 2017 Immigration Medical Care My Policy Package: Be Like Canada d University Tuition

The U. S. Economic Outlook: Upside and Risks Robert J. Gordon Ottawa a Economics Association Ottawa, a, September 14, 2017 Immigration Medical Care My Policy Package: Be Like Canada d University Tuition

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip?

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Global Economic Outlook. Kellie Maske, Sr. Economics Fellow FedEx Corporate Economics September 2011

Kellie Maske, Sr. Economics Fellow FedEx Corporate Economics U.S. Outlook: Moderate Growth Overall 6 4 US Real GDP Growth 2 % Change 0 (2) (4) Forecast (6) (8) Bars = QOQ% Annualized Line = YOY% (10) 2005

Kellie Maske, Sr. Economics Fellow FedEx Corporate Economics U.S. Outlook: Moderate Growth Overall 6 4 US Real GDP Growth 2 % Change 0 (2) (4) Forecast (6) (8) Bars = QOQ% Annualized Line = YOY% (10) 2005

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies Chief Economist, PAGI Group, JLL (Port, Airport & Global Infrastructure) Agenda Where are we in the cycle? What are the barriers

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies Chief Economist, PAGI Group, JLL (Port, Airport & Global Infrastructure) Agenda Where are we in the cycle? What are the barriers

SPECIAL DIVIDEND OF MUELLER INDUSTRIES, INC.

MUELLER INDUSTRIES, INC. SPECIAL DIVIDEND OF MUELLER INDUSTRIES, INC. This document is being provided to stockholders of Mueller Industries, Inc. (a corporation that we refer to as Mueller, we, our or

MUELLER INDUSTRIES, INC. SPECIAL DIVIDEND OF MUELLER INDUSTRIES, INC. This document is being provided to stockholders of Mueller Industries, Inc. (a corporation that we refer to as Mueller, we, our or

WORKFORCE LOCAL AREA EMPLOYMENT STATISTICS (LAUS)

") AUGUST 2016 WORKFORCE LOCAL AREA EMPLOYMENT STATISTICS (LAUS) 1,150,000 1,100,000 1,050,000 1,000,000 950,000 900,000 850,000 800,000 750,000 700,000 Labor Force Employment June 2015 to June 2016: 36,504

AUGUST 2016 WORKFORCE LOCAL AREA EMPLOYMENT STATISTICS (LAUS) 1,150,000 1,100,000 1,050,000 1,000,000 950,000 900,000 850,000 800,000 750,000 700,000 Labor Force Employment June 2015 to June 2016: 36,504

Dr. James P. Gaines Research Economist recenter.tamu.edu

Texas Uncertain Economy in a World of Uncertain Oil Prices Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 U.S. Outlook Expected GDP growth still modest:

Texas Uncertain Economy in a World of Uncertain Oil Prices Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 U.S. Outlook Expected GDP growth still modest:

Will 2016 Be the Last Hurrah for Commercial Real Estate? Presented By: John Chang First Vice-President Marcus & Millichap Research Services

Will 2016 Be the Last Hurrah for Commercial Real Estate? Presented By: John Chang First Vice-President Marcus & Millichap Research Services Rising Uncertainty Creating Headwinds for Commercial Real Estate

Will 2016 Be the Last Hurrah for Commercial Real Estate? Presented By: John Chang First Vice-President Marcus & Millichap Research Services Rising Uncertainty Creating Headwinds for Commercial Real Estate

Deutsche Bank. Consensus Report. 14 August 2018

Deutsche Bank Consensus Report 14 August 2018 Deutsche Bank Group P&L (in m) Average Minimum Maximum # est. Average Minimum Maximum # est. Average Minimum Maximum # est. Average Minimum Maximum # est.

Deutsche Bank Consensus Report 14 August 2018 Deutsche Bank Group P&L (in m) Average Minimum Maximum # est. Average Minimum Maximum # est. Average Minimum Maximum # est. Average Minimum Maximum # est.

East Bay Financial Planners Association Conference

East Bay Financial Planners Association Conference Is The New Normal Here to Stay? January 10, 2018 Rich Taylor Vice President Client Portfolio Manager Percent Change (%) Subpar Economic Growth Real GDP

East Bay Financial Planners Association Conference Is The New Normal Here to Stay? January 10, 2018 Rich Taylor Vice President Client Portfolio Manager Percent Change (%) Subpar Economic Growth Real GDP

Annual results 2017 and strategy update. 09 March 2018

Annual results 2017 and strategy update 09 March 2018 Agenda 1. Highlights & Group performance 2017 2. Strategy update 3. Outlook 2018 March 9, 2018 Accell Group N.V. presentation annual results 2017 1

Annual results 2017 and strategy update 09 March 2018 Agenda 1. Highlights & Group performance 2017 2. Strategy update 3. Outlook 2018 March 9, 2018 Accell Group N.V. presentation annual results 2017 1

United Nations Conference on Trade and Development

United Nations Conference on Trade and Development 11 th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 15-16 April 2019, Geneva Saudi economic growth strategy on the face of oil price uncertainty

United Nations Conference on Trade and Development 11 th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 15-16 April 2019, Geneva Saudi economic growth strategy on the face of oil price uncertainty

Curves On The Road Ahead

Curves On The Road Ahead Light Vehicle Market Outlook November 2018 Charles Chesbrough Senior Economist A g e n d a Economic Outlook and New Vehicle Sales Affordability Threat and the Used Vehicle Market

Curves On The Road Ahead Light Vehicle Market Outlook November 2018 Charles Chesbrough Senior Economist A g e n d a Economic Outlook and New Vehicle Sales Affordability Threat and the Used Vehicle Market