Financial assets. The need to raise money vertebrates economies

|

|

|

- Noreen Little

- 6 years ago

- Views:

Transcription

1 1 8 March 2016

2 2 8 March 2016

3 Financial assets The need to raise money vertebrates economies Financial asset = promise of payment in the future in exchange for receiving money now Function: way of saving / getting purchasing power Properties: maturity / risk / liquidity / return Types: tradable (securities) / non-tradable Securitization Trade-offs between properties 3 8 March 2016

4 Vulnerability of the financial sector 4 8 March 2016

5 Financial sector instability/fragility /1 Reckless and/or excessive lending by banks? Possibility of bank runs Stability relies on the belief that the sector is stable Shadow banking sector that sidesteps regulations Speculation contributes to magnify outcomes and create bubbles (Ponzi schemes) Abuse of leverage? 5 8 March 2016

6 Financial sector instability/fragility /2 Financial activities increase interdependence long chains of connections Contagion effects Myopic decisions ignorance of systemic risks (belief that what holds locally, holds globally) Emergent properties larger scale, new banking and/or derivatives risks (banks too big to fail) Minsky s instability hypothesis overoptimism 6 8 March 2016

7 NASDAQ (5 Feb Feb 2016) /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ March /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/ /02/2009 last: 4, /02/ /02/ /02/ /02/ /02/ /02/ /02/2016

8 Dow Jones (1 Oct Feb 2016) /12/ /03/ /05/ /07/ /10/ /12/ /03/ /05/ /07/ /10/ /12/ /03/ /05/ /07/ /10/ /12/ /03/ /05/ /08/ /10/ /12/ /03/ /05/ /07/ /10/ /12/ /02/ /05/ /07/ /09/ /11/ /02/ /04/ /07/ /10/ /12/ /02/ /05/ /07/ /09/ /11/ /02/ /04/ /06/ /08/ /11/ /01/ /03/ /05/ /08/ /10/ /12/ /02/ /05/ /07/ /09/ /11/ /01/ /04/ /06/ /08/ /11/ /01/ /03/ /06/ /08/ /10/ /01/ /03/ /05/ /07/ /10/ /12/ /02/ March

9 Dow Jones (1 Oct Dec 1953) 01/10/ /02/ /07/ /12/ /05/ /10/ /03/ /08/ /01/ /06/ /11/ /04/ /09/ /02/ /07/ /11/ /04/ /09/ /02/ /07/ /12/ /05/ /10/ /03/ /08/ /01/ /06/ /11/ /04/ /08/ /01/ /06/ /11/ /04/ /09/ /02/ /07/ /12/ /05/ /10/ /03/ /08/ /12/ /05/ /10/ /03/ /08/ /01/ /06/ /11/ /04/ /09/ /02/ /07/ /12/ /05/ /10/ /02/ /07/ /12/ /05/ /10/ March 2016

10 19000 Dow Jones (2 Jan Feb 2016) /05/ /08/ /10/ /12/ /02/ /05/ /07/ /09/ /11/ /01/ /04/ /06/ /08/ /11/ March /01/ /03/ /06/ /08/ /10/ /01/ /03/ /05/ /07/ /10/ /12/ /02/

11 26/01/ /06/1999 Dow Jones (4 Jan Feb 2016) 09/11/ /04/ /08/ /01/ /06/ /11/ /04/ /08/ /01/ /06/ /11/ /03/ /08/ /01/ /06/ /10/ /03/ /08/ /01/ /06/ /10/ /03/ March /08/ /01/ /05/ /10/ /03/ /08/ /12/ /05/ /10/ /03/ /07/ /12/ /05/ /10/ /03/ /07/ /12/ /05/ /10/ /02/

12 IBEX-35 (5 Jan Mar 2016) last: 8,611 05/01/ /07/ /02/ /08/ /03/ /10/ /04/ /11/ /05/ /12/ /06/ /01/ /08/ /02/ /09/ /03/ /10/ /04/ /11/ /06/ /12/ /07/ /01/ /08/ /02/ /09/ /04/ /10/ /05/ /11/ /06/ /12/ /07/ /01/ /08/ /03/ /09/ /04/ /10/ /05/ /11/ /06/ /01/ /07/ /02/ /08/ /03/ /09/ /04/ /11/ /05/ /12/ /06/ /01/ March 2016

13 IBEX-35 (daily, 5 January February 2015) Last: 11,152 05/01/ /06/ /11/ /03/ /08/ /01/ /06/ /11/ /04/ /09/ /02/ /07/ /12/ /05/ /10/ /03/ /08/ /12/ /05/ /10/ /03/ /08/ /01/ /06/ /11/ /04/ /09/ /02/ /07/ /12/ /05/ /09/ /02/ /07/ /12/ /05/ /10/ /03/ /08/ /01/ /06/ /11/ /04/ /09/ /01/ /06/ /11/ /04/ /09/ /02/ /07/ /12/ /05/ /10/ /03/ /08/ /01/ /06/ /10/ /03/ /08/ /01/ /06/ /11/ /04/ /09/ /02/ /07/ /12/ March 2016

14 Robert Menschel (2002): Markets, Mobs, and Mayhem. A Modern Look at the Madness of Crowds, p March 2016

15 900 LOANS (TOTAL) LENDING FOR HOUSE PURCHASE Spain (outstanding amount at the end of the period, EUR billions) CREDIT FOR CONSUMPTION SPAIN Nominal GDP trillion (2012) Mar 2003Jun 2003Sep 2003Dec 2004Mar 2004Jun 2004Sep 2004Dec 2005Mar 2005Jun 2005Sep 2005Dec 2006Mar 2006Jun 2006Sep 2006Dec 2007Mar 2007Jun 2007Sep 2007Dec 2008Mar 2008Jun 2008Sep 2008Dec 2009Mar 2009Jun 2009Sep 2009Dec 2010Mar 2010Jun 2010Sep 2010Dec 2011Mar 2011Jun 2011Sep 2011Dec 2012Mar 2012Jun 2012Sep 2012Dec 2013Mar 2013Jun 2013Sep 2013Dec 15 8 March

16 Eurozone (outstanding amount at the end of the period, EUR trillions) EUROZONE Nominal GDP 9.5 trillion (2012) LOANS (TOTAL) LENDING FOR HOUSE PURCHASE EUROPEAN UNION Nominal GDP 12.9 trillion (2012) Largest economy of the world CREDIT FOR CONSUMPTION 1997Dec 1998Apr 1998Aug 1998Dec 1999Apr 1999Aug 1999Dec 2000Apr 2000Aug 2000Dec 2001Apr 2001Aug 2001Dec 2002Apr 2002Aug 2002Dec 2003Apr 2003Aug 2003Dec 2004Apr 2004Aug 2004Dec 2005Apr 2005Aug 2005Dec 2006Apr 2006Aug 2006Dec 2007Apr 2007Aug 2007Dec 2008Apr 2008Aug 2008Dec 2009Apr 2009Aug 2009Dec 2010Apr 2010Aug 2010Dec 2011Apr 2011Aug 2011Dec 2012Apr 2012Aug 2012Dec 2013Apr 2013Aug 2013Dec 16 8 March ,5 5,25 5 4,75 4,5 4,25 4 3,75 3,5 3,25 3 2,75 2,5 2,25 2 1,75 1,5 1,25 1 0,75 0,5 0,25 0

17 LENDING FOR HOUSE PURCHASE Spain (annual change, %) browse.do?node= LOANS (TOTAL) -5 CREDIT FOR CONSUMPTION Mar 2004Jun 2004Sep 2004Dec 2005Mar 2005Jun 2005Sep 2005Dec 2006Mar 2006Jun 2006Sep 2006Dec 2007Mar 2007Jun 2007Sep 2007Dec 2008Mar 2008Jun 2008Sep 2008Dec 2009Mar 2009Jun 2009Sep 2009Dec 2010Mar 2010Jun 2010Sep 2010Dec 2011Mar 2011Jun 2011Sep 2011Dec 2012Mar 2012Jun 2012Sep 2012Dec 2013Mar 2013Jun 2013Sep 2013Dec 17 8 March

18 LENDING FOR HOUSE PURCHASE LOANS (TOTAL) Eurozone (annual change, %) browse.do?node= CREDIT FOR CONSUMPTION 1998Dec 1999Apr 1999Aug 1999Dec 2000Apr 2000Aug 2000Dec 2001Apr 2001Aug 2001Dec 2002Apr 2002Aug 2002Dec 2003Apr 2003Aug 2003Dec 2004Apr 2004Aug 2004Dec 2005Apr 2005Aug 2005Dec 2006Apr 2006Aug 2006Dec 2007Apr 2007Aug 2007Dec 2008Apr 2008Aug 2008Dec 2009Apr 2009Aug 2009Dec 2010Apr 2010Aug 2010Dec 2011Apr 2011Aug 2011Dec 2012Apr 2012Aug 2012Dec 2013Apr 2013Aug 2013Dec 18 8 March

19 Spain (EUR billions amounts at the end of the period) browse.do?node= LOANS TO GOVERNMENT /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ March 2016

20 1,25 1,2 1,15 1,1 1,05 1 0,95 0,9 0,85 0,8 0,75 0,7 0,65 0,6 0,55 0,5 0,45 0,4 0,35 0,3 0,25 0,2 0,15 0,1 0,05 0 LOANS TO GOVERNMENT Eurozone (EUR trillions amounts at the end of the period) browse.do?node= /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ March 2016

21 Spain Debt to GDP (%) March 2016

22 Spain Debt to GDP ratio March 2016

23 Spain Government debt (EUR million) Spain, 2015 Q4 : 1,069,876 EUR million (98,95%) March 2016

24 Spain, public debt (millions of euros) March

25 Spain, public debt (debt-to-gdp ratio, millions of euros) debt-to-gdp ratio 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0 0% March

26 Spain, per capita public debt (euros) March

27 Allianz Global Wealth Report 2013 EUR trillion World GDP 2012 USD 72 trillion Average rate USD/EUR 2012 = World GDP 2012 EUR 92.5 trillion End of 2012 (share) 32% 36% 30% economic_research/publications/specials/en/agwr2013e.pdf 27 8 March 2016

28 Allianz Global Wealth Report March 2016

29 global_capital_markets/mapping_global_ capital_markets_ March 2016

30 Financial depth financial sector size debt_and_not_much_deleveraging 30 8 March 2016

31 global_capital_markets/uneven_progress _on_the_path_to_growth 31 8 March 2016

32 32 8 March 2016

33 12, , ,5 10 9,5 9 8,5 8 7,5 7 6,5 6 5,5 5 4,5 4 3,5 3 2,5 2 1,5 1 0, M M M M M M M M M01 Spain, interest rates (January 1995 November 2011) CONSUMER LOANS (banks) 10 yr BONDS CONSUMER LOANS (savings banks) MORTGAGES PREFERENTIAL RATE (banks) EURIBOR M M M M M M M M M March M M M M M M M M M M M M M M M M M M07

34 5,75 5,5 5,25 5 4,75 4,5 4,25 4 3,75 3,5 3,25 3 2,75 2,5 2,25 2 1,75 1,5 1,25 1 0,75 0,5 0,25 0-0,25-0,5 Jan99 Jan00 Jan01 Jan02 Jan03 Jan04 Lending MRO Deposit Jan05 Jan06 Jan March 2016 Jan08 Jan09 Jan10 ECB key interest rates 1 Jan Feb 2016 Jan11 Jan12 Jan13 Jan14 Jan15 Jan16

35 5,6 5,4 5,2 5,0 4,8 4,6 4,4 4,2 4,0 3,8 3,6 3,4 3,2 3,0 2,8 2,6 2,4 2,2 2,0 1,8 1,6 1,4 1,2 1,0 0,8 0,6 0,4 0,2 0,0-0,2 Euribor (2 January February 2015) 1 MONTH 02/01/ /02/ /03/ /05/ /06/ /08/ /09/ /10/ /12/ /01/ /03/ /04/ /06/ /07/ /08/ /10/ /11/ /01/ /02/ /03/ /05/ /06/ /08/ /09/ /10/ /12/ /01/ /03/ /04/ /05/ /07/ /08/ /10/ /11/ /01/ /02/ /03/ /05/ /06/ /08/ /09/ /10/ /12/ /01/ /03/ /04/ /05/ /07/ /08/ /10/ /11/ /12/ /02/ /03/ /05/ /06/ /07/ /09/ /10/ /12/ /01/ /03/ /04/ /05/ /07/ /08/ /10/ /11/ /12/ /02/ March YEAR 1 WEEK

36 5,6 5,4 5,2 5,0 4,8 4,6 4,4 4,2 4,0 3,8 3,6 3,4 3,2 3,0 2,8 2,6 2,4 2,2 2,0 1,8 1,6 1,4 1,2 1,0 0,8 0,6 0,4 0,2 0,0-0,2-0,4 1 MONTH Euribor (2 January February 2016) 1 WEEK 02/01/ /02/ /03/ /05/ /06/ /08/ /09/ /10/ /12/ /01/ /03/ /04/ /06/ /07/ /08/ /10/ /11/ /01/ /02/ /03/ /05/ /06/ /08/ /09/ /10/ /12/ /01/ /03/ /04/ /05/ /07/ /08/ /10/ /11/ /01/ /02/ /03/ /05/ /06/ /08/ /09/ /10/ /12/ /01/ /03/ /04/ /05/ /07/ /08/ /10/ /11/ /12/ /02/ /03/ /05/ /06/ /07/ /09/ /10/ /12/ /01/ /03/ /04/ /05/ /07/ /08/ /10/ /11/ /12/ /02/ /03/ /05/ /06/ /07/ /09/ /10/ /12/ /01/ March YEAR

37 2,2 2,0 1,8 Euribor (4 January February 2016) euribor-org/euribor-rates.html 1,6 1 YEAR 1,4 1,2 1,0 0,8 1 MONTH 0,6 0,4 1 WEEK 0,2 0,0-0,2-0,4 04/01/ /02/ /03/ /05/ /06/ /08/ /09/ /10/ /12/ /01/ /03/ /04/ /06/ /07/ /08/ /10/ /11/ /12/ /02/ /03/ /05/ /06/ /07/ /09/ /10/ /12/ /01/ /03/ /04/ /05/ /07/ /08/ /10/ /11/ /12/ /02/ /03/ /05/ /06/ /07/ /09/ /10/ /12/ /01/ /03/ /04/ /05/ /07/ /08/ /10/ /11/ /12/ /02/ March 2016

38 qe_and_ultra_low_interest_rates_distributional_effects_and_risks 38 8 March 2016

39 Prices of financial assets and Justifications of the inverse relationship financial arbitrage prices of financial assets as present values equalization of rates of return 39 8 March 2016

40 Financial arbitrage 40 8 March 2016

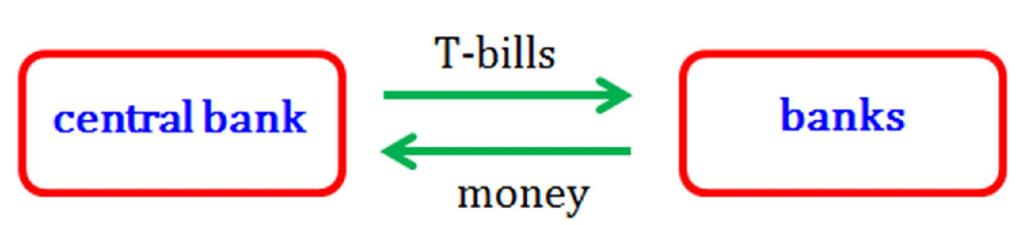

41 Central bank Monetary authority of an economy Monetary policy instruments Open market operations Standing facilities: lending / deposit Reserve requirements Policy interest rate Credit controls Tension between controlling and M March 2016

42 Expansionary OMO Contractionary OMO 42 8 March 2016

43 Reverse-repo 43 8 March 2016

44 Effects of a contractionary OMO The central bank cannot simultaneously control M1 and the interest rate March 2016

45 Central bank and the payment system 45 8 March 2016

46 A liquidity market model Supply of liquidity: direct / indirect Supply of liquidity function Demand for liquidity: direct / indirect Demand for liquidity function Market equilibrium Comparative statics 46 8 March 2016

47 = interest rate in a period = volume of liquidity supplied in the period 47 8 March 2016

48 = interest rate in a period = volume of liquidity supplied in the period 48 8 March 2016

49 = interest rate in a period = volume of liquidity supplied in the period 49 8 March 2016

50 = interest rate in a period = volume of liquidity supplied in the period 50 8 March 2016

51 = interest rate in a period Supply of liquidity function = volume of liquidity supplied in the period 51 8 March 2016

52 52 8 March 2016

53 = interest rate in a period = volume of liquidity demanded in the period 53 8 March 2016

54 = interest rate in a period = volume of liquidity demanded in the period 54 8 March 2016

55 = interest rate in a period = volume of liquidity demanded in the period 55 8 March 2016

56 = interest rate in a period = volume of liquidity demanded in the period 56 8 March 2016

57 = interest rate in a period = volume of liquidity demanded in the period Demand for liquidity function 57 8 March 2016

58 58 8 March 2016

59 * * 59 8 March 2016

60 * * 60 8 March 2016

61 Equilibrium effect of a demand shift This is a demand-side explanation of a rise in the interest rate: more liquidity wanted March 2016

62 Equilibrium effect of a supply shift This is a supply-side explanation of a rise in the interest rate: less liquidity available. L 62 8 March 2016

but the")

63 Effect of simultaneous shifts /1 The effect on is certain (a reduction) but the effect on is ambiguous. The precise effect on depends on the magnitude of the shifts March 2016

64 Effect of simultaneous shifts /2 Now the effect on is ambiguous but the effect on is certain: an increase March 2016

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*

CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*") COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun Jul

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun Jul

The Herzliya Conference The Economic Dimension Prof. Rafi Melnick Provost, Interdisciplinary Center (IDC) Herzliya

Herzliya") The Herzliya Conference The Economic Dimension 2009 Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

The Herzliya Conference The Economic Dimension 2009 Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

The Israeli Economy 2009 The Caesarea Center Conference

The Israeli Economy 2009 The Caesarea Center Conference Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

The Israeli Economy 2009 The Caesarea Center Conference Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

A comment on recent events, and...

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

Utility Debt Securitization Authority 2013 T/TE Billed Revenues Tracking Report

Utility Debt Securitization Authority 2013 T/TE Billed Revenues Tracking Report Billing Budgeted Billed Dollar Percent Month Revenues Revenues Variance Variance Jan 2018 11,943,180.68 12,697,662.47 754,481.79

Utility Debt Securitization Authority 2013 T/TE Billed Revenues Tracking Report Billing Budgeted Billed Dollar Percent Month Revenues Revenues Variance Variance Jan 2018 11,943,180.68 12,697,662.47 754,481.79

Deutsche Bundesbank Interest rate statistics

Methodological notes on interest rates statistics interest rates for savings deposits with agreed notice of 3 months The term standard savings rate originally referred to the interest restricted basis.

Methodological notes on interest rates statistics interest rates for savings deposits with agreed notice of 3 months The term standard savings rate originally referred to the interest restricted basis.

Outline. Overview of globalization. Global outlook for real economic activity & inflation. Risks to the outlook

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

Farmland Booms and Busts: Will the Cycle be Broken?

Farmland Booms and Busts: Will the Cycle be Broken? Kansas Society of Farm Managers and Rural Appraisers Salina, KS February 23 rd, 2012 Brian C. Briggeman Associate Professor and Director of the Arthur

Farmland Booms and Busts: Will the Cycle be Broken? Kansas Society of Farm Managers and Rural Appraisers Salina, KS February 23 rd, 2012 Brian C. Briggeman Associate Professor and Director of the Arthur

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Macroeconomic Research and Statistics Department Vol. XVIl, No.3 March 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02 Table

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Macroeconomic Research and Statistics Department Vol. XVIl, No.3 March 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02 Table

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.9 September 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.9 September 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

Global growth forecasts Key countries/regions,

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.11 November 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.11 November 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

Reading the Tea Leaves: Investing for 2010 and Beyond

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

United Nations Conference on Trade and Development

United Nations Conference on Trade and Development 11 th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 15-16 April 2019, Geneva Saudi economic growth strategy on the face of oil price uncertainty

United Nations Conference on Trade and Development 11 th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 15-16 April 2019, Geneva Saudi economic growth strategy on the face of oil price uncertainty

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD?

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD? FROM BUST TO BOOM. AN EPIC BUST After 16 years of growth with a short pause for breath in 2002, the Icelandic economy entered

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD? FROM BUST TO BOOM. AN EPIC BUST After 16 years of growth with a short pause for breath in 2002, the Icelandic economy entered

The Eurozone integration, des-integration and possible future developments

The Eurozone integration, des-integration and possible future developments 18 th Monetary Policy Workshop at the Berlin School of Economcs and Law, 12 13 October 2017 Overview Position 1: The euro itself

The Eurozone integration, des-integration and possible future developments 18 th Monetary Policy Workshop at the Berlin School of Economcs and Law, 12 13 October 2017 Overview Position 1: The euro itself

Real Estate and Economic Outlook

Real Estate and Economic Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation at Inforum Outlook Conference University of Maryland College Park, MD December 12, 2013

Real Estate and Economic Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation at Inforum Outlook Conference University of Maryland College Park, MD December 12, 2013

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 2 OVERVIEW OF THE GREAT DEPRESSION January 22, 2018 I. THE 1920S A. GDP growth and inflation B.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 2 OVERVIEW OF THE GREAT DEPRESSION January 22, 2018 I. THE 1920S A. GDP growth and inflation B.

After the British referendum

Future of Europe After the British referendum Broader issues for the UK and the EU David Marsh, Managing Director, OMFIF 27 October 2016 Nicosia 1 European politics moves against integration A new phase

Future of Europe After the British referendum Broader issues for the UK and the EU David Marsh, Managing Director, OMFIF 27 October 2016 Nicosia 1 European politics moves against integration A new phase

Future Global Trade Trends - Risks & Opportunities. Pulse of the Ports: Peak Season Forecast March 21, 2013

1 Future Global Trade Trends - Risks & Opportunities Pulse of the Ports: Peak Season Forecast March 21, 2013 June 2012 Dr. Walter Kemmsies Chief Economist Summary Higher economic growth in 2013, possible

1 Future Global Trade Trends - Risks & Opportunities Pulse of the Ports: Peak Season Forecast March 21, 2013 June 2012 Dr. Walter Kemmsies Chief Economist Summary Higher economic growth in 2013, possible

A Distant Mirror: Credit contraction, monetary policy and commodity prices during the Great Depression. John Kemp Reuters 30 January 2009

A Distant Mirror: Credit contraction, monetary policy and commodity prices during the Great Depression John Kemp Reuters 3 January 29 BORROWING BOOM IN 192s. FOLLOWED BY DE-LEVERAGING IN 193s U.S.$ bn

A Distant Mirror: Credit contraction, monetary policy and commodity prices during the Great Depression John Kemp Reuters 3 January 29 BORROWING BOOM IN 192s. FOLLOWED BY DE-LEVERAGING IN 193s U.S.$ bn

Global Economic Outlook

Global Economic Outlook Mark A. Wynne Vice President & Associate Director of Research Director, Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas Presentation to Vistas Conference

Global Economic Outlook Mark A. Wynne Vice President & Associate Director of Research Director, Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas Presentation to Vistas Conference

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies Chief Economist, PAGI Group, JLL (Port, Airport & Global Infrastructure) Agenda Where are we in the cycle? What are the barriers

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies Chief Economist, PAGI Group, JLL (Port, Airport & Global Infrastructure) Agenda Where are we in the cycle? What are the barriers

From Recession to Recovery

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

The Current Restructuring Cycle: Meltdown or Metamorphosis? Monday, April 27, :00 PM - 5:15 PM

The Current Restructuring Cycle: Meltdown or Metamorphosis? Monday, April 27, 29 4: PM - 5:15 PM Today s Speakers: Michael Henkin (Moderator) Managing Director and Co-Head of Recapitalization & Restructuring

The Current Restructuring Cycle: Meltdown or Metamorphosis? Monday, April 27, 29 4: PM - 5:15 PM Today s Speakers: Michael Henkin (Moderator) Managing Director and Co-Head of Recapitalization & Restructuring

Colombia: Economic Adjustment and Outlook. Andres-Mauricio Velasco Technical Deputy Minister of Finance, Republic of Colombia February 2018

Colombia: Economic Adjustment and Outlook Andres-Mauricio Velasco Technical Deputy Minister of Finance, Republic of Colombia February 2018 What is Colombian Ministry of Finance s outlook and funding strategies

Colombia: Economic Adjustment and Outlook Andres-Mauricio Velasco Technical Deputy Minister of Finance, Republic of Colombia February 2018 What is Colombian Ministry of Finance s outlook and funding strategies

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Europe June Craig Menear. Chairman, CEO & President. Diane Dayhoff. Vice President, Investor Relations

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

Economic Overview. Melissa K. Peralta Senior Economist April 27, 2017

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H. Parker Willis Lecture in Political Economics

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

Further Opening Up and Reform of China s Capital Market

Further Opening Up and Reform of China s Capital Market Haizhou Huang January 7, 2016 China economy and capital market: Finding new normal 1 Macro: We expect China GDP to grow 6.9% in 2015 and 6.8% in

Further Opening Up and Reform of China s Capital Market Haizhou Huang January 7, 2016 China economy and capital market: Finding new normal 1 Macro: We expect China GDP to grow 6.9% in 2015 and 6.8% in

US Economic Activity

US Economic Activity GDP has been in positive territory for seven consecutive quarters, and the advance estimate shows the US economy grew at a 1.0% rate in the fourth quarter 2015. US Economic Activity

US Economic Activity GDP has been in positive territory for seven consecutive quarters, and the advance estimate shows the US economy grew at a 1.0% rate in the fourth quarter 2015. US Economic Activity

2018 Soybean, Corn, & Wheat Outlook KY and TN Grain Conference

2018 Soybean, Corn, & Wheat Outlook KY and TN Grain Conference S. Aaron Smith, Crop Marketing Specialist, Assistant Professor, Department of Agricultural and Resource Economics, University of Tennessee

2018 Soybean, Corn, & Wheat Outlook KY and TN Grain Conference S. Aaron Smith, Crop Marketing Specialist, Assistant Professor, Department of Agricultural and Resource Economics, University of Tennessee

MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION

OXYGEN EVENTS CONFERENCE GALA PERFORMANCE 2017 MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION - THE CASE OF ROMANIA - Ph.D. Andrei RĂDULESCU Senior Economist, Banca Transilvania Researcher, Institute

OXYGEN EVENTS CONFERENCE GALA PERFORMANCE 2017 MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION - THE CASE OF ROMANIA - Ph.D. Andrei RĂDULESCU Senior Economist, Banca Transilvania Researcher, Institute

NOVEMBER [Date]

![NOVEMBER [Date]](/thumbs/84/89533926.jpg "NOVEMBER [Date]") NOVEMBER [Date] TABLE OF CONTENTS SELECTED ECONOMIC INDICATORS 1 STOCK MARKET DEVELOPMENTS 2 MONETARY DEVELOPMENTS 3 INFLATION OUTTURN 4 Annual Inflation 4 Monthly Inflation 4 NATIONAL PAYMENTS SYSTEM

NOVEMBER [Date] TABLE OF CONTENTS SELECTED ECONOMIC INDICATORS 1 STOCK MARKET DEVELOPMENTS 2 MONETARY DEVELOPMENTS 3 INFLATION OUTTURN 4 Annual Inflation 4 Monthly Inflation 4 NATIONAL PAYMENTS SYSTEM

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States?

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Manufacturers continue capacity expansion as technology orders grow

Contact: Penny Brown, AMT, 703-827-5275 pbrown@amtonline.org For Release: September 10, 2018 Manufacturers continue capacity expansion as technology orders grow Manufacturing technology orders for July

Contact: Penny Brown, AMT, 703-827-5275 pbrown@amtonline.org For Release: September 10, 2018 Manufacturers continue capacity expansion as technology orders grow Manufacturing technology orders for July

Babson Capital/UNC Charlotte Economic Forecast. May 13, 2014

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Figures & facts around Austrian Government Bonds. Quarterly Report

Figures & facts around Austrian Government Bonds Quarterly Report September 2018 Primary Market for Government Bonds Auction Calendar 2018 Auction date 09 Jan 2018 06 Feb 2018 06 Mar 2018 10 Apr 2018 08

Figures & facts around Austrian Government Bonds Quarterly Report September 2018 Primary Market for Government Bonds Auction Calendar 2018 Auction date 09 Jan 2018 06 Feb 2018 06 Mar 2018 10 Apr 2018 08

Dick Vos Senior Manager Research & Strategy

Dick Vos Senior Manager Research & Strategy! House prices now falling at fastest rate since early 1990s House prices will fall 7% in 'uncertain' market IMF warns on global house prices House prices Through

Dick Vos Senior Manager Research & Strategy! House prices now falling at fastest rate since early 1990s House prices will fall 7% in 'uncertain' market IMF warns on global house prices House prices Through

Mexico sugar towards 2014/15. Forget the inflexion point?

Mexico sugar towards 20 Forget the inflexion point? Pablo Sherwell VP, Food & Agribusiness Research & Advisory pablo.sherwell@rabobank.com September 2014 1 Rabobank: Food & Agribusiness Research and Advisory

Mexico sugar towards 20 Forget the inflexion point? Pablo Sherwell VP, Food & Agribusiness Research & Advisory pablo.sherwell@rabobank.com September 2014 1 Rabobank: Food & Agribusiness Research and Advisory

MUSTAFA MOHATAREM Chief Economist, General Motors

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

Post-Bubble Global Trends. AAPA Webinar. February 18, Dr. Walter Kemmsies, Chief Economist Moffatt & Nichol Commercial Analysis Group

Post-Bubble Global Trends AAPA Webinar February 18, 2009 Dr. Walter Kemmsies, Chief Economist Moffatt & Nichol Commercial Analysis Group Takeaways The world economy is circling the drain World is wealthier

Post-Bubble Global Trends AAPA Webinar February 18, 2009 Dr. Walter Kemmsies, Chief Economist Moffatt & Nichol Commercial Analysis Group Takeaways The world economy is circling the drain World is wealthier

Calendar On US Federal Reserve Holidays, no settlements will take place for USD.

NASDAQ Dubai Notice No: NASDAQ Dubai Trading Holidays and Settlement Calendar 2012 Date of Issue: NASDAQ Dubai TRADING HOLIDAYS AND SETTLEMENT CALENDAR 2012 For Derivatives, Exchange Traded Commodities,

NASDAQ Dubai Notice No: NASDAQ Dubai Trading Holidays and Settlement Calendar 2012 Date of Issue: NASDAQ Dubai TRADING HOLIDAYS AND SETTLEMENT CALENDAR 2012 For Derivatives, Exchange Traded Commodities,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

Dr. James P. Gaines Research Economist recenter.tamu.edu

Texas Uncertain Economy in a World of Uncertain Oil Prices Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 U.S. Outlook Expected GDP growth still modest:

Texas Uncertain Economy in a World of Uncertain Oil Prices Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 U.S. Outlook Expected GDP growth still modest:

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

Nasdaq Dubai AED TRADING HOLIDAYS AND SETTLEMENT CALENDAR 2018 For Equities Outsourced to the DFM (T+2)

") NasdaqDubai Circular No: 14 /2018 Date of Issue: 13 March 2018 Date of Expiry : Upon issue of replacement Circular Nasdaq Dubai AED TRADING HOLIDAYS AND SETTLEMENT CALENDAR 2018 For Equities Outsourced

NasdaqDubai Circular No: 14 /2018 Date of Issue: 13 March 2018 Date of Expiry : Upon issue of replacement Circular Nasdaq Dubai AED TRADING HOLIDAYS AND SETTLEMENT CALENDAR 2018 For Equities Outsourced

FIVE GREAT STAGNATIONS

FIVE GREAT STAGNATIONS Paper to Treasury Seminar: 26 July, 2011 Brian Easton Economic and Social Trust On New Zealand Introduction Definitions Beginnings Stagnation 1: The Long Depression Stagnation 2:

FIVE GREAT STAGNATIONS Paper to Treasury Seminar: 26 July, 2011 Brian Easton Economic and Social Trust On New Zealand Introduction Definitions Beginnings Stagnation 1: The Long Depression Stagnation 2:

The Shifts and the Shocks Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

The Shifts and the Shocks Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times Peterson Institute for International Economics 9 th October 2014 Washington DC The Shifts and the

The Shifts and the Shocks Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times Peterson Institute for International Economics 9 th October 2014 Washington DC The Shifts and the

URBAN LAND INSTITUTE

URBAN LAND INSTITUTE 2012 ULI FALL MEETING (Denver, 18 October 2012) The Global Economic Outlook Dark clouds on the horizon Andrea Boltho Magdalen College University of Oxford Oxford Economics and REAG

URBAN LAND INSTITUTE 2012 ULI FALL MEETING (Denver, 18 October 2012) The Global Economic Outlook Dark clouds on the horizon Andrea Boltho Magdalen College University of Oxford Oxford Economics and REAG

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

India: Can the Tiger Economy Continue to Run?

India: Can the Tiger Economy Continue to Run? India s GDP is on the rise US$ trillions Nominal GDP (left axis) GDP growth (right axis) 3.0 2.5 2.0 1.5 1.0 0.5 0.0 1990 1992 1994 1996 1998 2000 2002 2004

India: Can the Tiger Economy Continue to Run? India s GDP is on the rise US$ trillions Nominal GDP (left axis) GDP growth (right axis) 3.0 2.5 2.0 1.5 1.0 0.5 0.0 1990 1992 1994 1996 1998 2000 2002 2004

Turkey: Recent Developments and Future Prospects. ISBANK Economic Research Division November 2018

Turkey: Recent Developments and Future Prospects ISBANK Economic Research Division November 2018 Macroeconomic Outlook Strong Economic Growth Cycle GDP of 851 bn USD (2017), 10.6k USD (2017) per capita

Turkey: Recent Developments and Future Prospects ISBANK Economic Research Division November 2018 Macroeconomic Outlook Strong Economic Growth Cycle GDP of 851 bn USD (2017), 10.6k USD (2017) per capita

Financial Communication

Attijariwafa bank As of 31 December2017 Financial Communication 2017 Banking industry Growth and penetration % GDP CAGR Banking Penetration Total Banking Assets / GDP (in %) Total Assets US$ Bn Penetration

Attijariwafa bank As of 31 December2017 Financial Communication 2017 Banking industry Growth and penetration % GDP CAGR Banking Penetration Total Banking Assets / GDP (in %) Total Assets US$ Bn Penetration

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition May 7 and 8, 2013 İstanbul, Turkey Outline 1 The Financial System 2 Weak Growth 3 4 5 Unprecedented

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition May 7 and 8, 2013 İstanbul, Turkey Outline 1 The Financial System 2 Weak Growth 3 4 5 Unprecedented

2018 HR & PAYROLL Deadlines

th (by payment date) EPAF 3rd PARTY FEEDS WTE Approval 2018 HR & PAYROLL s Normal Payroll day s 2017 B1-26 3 * 13-Dec-17 15-Dec-17 n/a n/a n/a 28-Dec-17 29-Dec-17 11:00 AM 16-Dec-2017 29-Dec-2017 JAN 2018

th (by payment date) EPAF 3rd PARTY FEEDS WTE Approval 2018 HR & PAYROLL s Normal Payroll day s 2017 B1-26 3 * 13-Dec-17 15-Dec-17 n/a n/a n/a 28-Dec-17 29-Dec-17 11:00 AM 16-Dec-2017 29-Dec-2017 JAN 2018

Spanish Financial System: Main Features

Spanish Financial System: Main Features Amaya Altuzarra, Jesus Ferreiro, Catalina Gálvez, Carmen Gómez, Ana González, Patricia Peinado, Carlos Rodríguez, Felipe Serrano Department of Applied Economics

Spanish Financial System: Main Features Amaya Altuzarra, Jesus Ferreiro, Catalina Gálvez, Carmen Gómez, Ana González, Patricia Peinado, Carlos Rodríguez, Felipe Serrano Department of Applied Economics

Kevin Thorpe Financial Economist & Principal Cassidy Turley

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

Monitoring of graduating and graduated countries: Angola, Equatorial Guinea, Maldives, Samoa, and Vanuatu

Monitoring of graduating and graduated countries: Angola, Equatorial Guinea, Maldives, Samoa, and Vanuatu Namsuk Kim CDP Secretariat CDP 20 th plenary meeting 12 16 March 2018 Monitoring timeline Date

Monitoring of graduating and graduated countries: Angola, Equatorial Guinea, Maldives, Samoa, and Vanuatu Namsuk Kim CDP Secretariat CDP 20 th plenary meeting 12 16 March 2018 Monitoring timeline Date

National and Regional Economic Outlook. Central Southern CAA Conference

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

NASDAQ DUBAI TRADING HOLIDAYS AND SETTLEMENT CALENDAR 2018 For Equities Outsourced to the DFM (T+2)

") Nasdaq Dubai Circular No : 71/17 Date of Issue : 24 December 2017 Date of Expiry : Upon issue of replacement Circular NASDAQ DUBAI TRADING HOLIDAYS AND SETTLEMENT CALENDAR 2018 For Equities Outsourced

Nasdaq Dubai Circular No : 71/17 Date of Issue : 24 December 2017 Date of Expiry : Upon issue of replacement Circular NASDAQ DUBAI TRADING HOLIDAYS AND SETTLEMENT CALENDAR 2018 For Equities Outsourced

Market Insights. June 30, 2018

June 30, 2018 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.7% 1.2% 1.3% 2.1% 2.3% 1.7% 2.3%

June 30, 2018 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.7% 1.2% 1.3% 2.1% 2.3% 1.7% 2.3%

Chapter 10 Aggregate Demand I: Building the IS LM Model

Chapter 10 Aggregate Demand I: Building the IS LM Model Zhengyu Cai Ph.D. Institute of Development Southwestern University of Finance and Economics All rights reserved http://www.escience.cn/people/zhengyucai/index.html

Chapter 10 Aggregate Demand I: Building the IS LM Model Zhengyu Cai Ph.D. Institute of Development Southwestern University of Finance and Economics All rights reserved http://www.escience.cn/people/zhengyucai/index.html

Market Insights. March 29, 2019

March 29, 2019 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.2% 1.4% 2.1% 2.3% 1.7% 2.4% 2.3%

March 29, 2019 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.2% 1.4% 2.1% 2.3% 1.7% 2.4% 2.3%

DECLINE IN COMMODITY PRICES GCC OUTLOOK NOVEMBER 22 ND, 2015

DECLINE IN COMMODITY PRICES GCC OUTLOOK NOVEMBER 22 ND, 2015 1 EVERYONE HAS A PLAN UNTIL THEY GET PUNCHED IN THE FACE 2 HE WHO IS NOT COURAGEOUS ENOUGH TO TAKE RISKS WILL ACCOMPLISH NOTHING IN LIFE 3 IT

DECLINE IN COMMODITY PRICES GCC OUTLOOK NOVEMBER 22 ND, 2015 1 EVERYONE HAS A PLAN UNTIL THEY GET PUNCHED IN THE FACE 2 HE WHO IS NOT COURAGEOUS ENOUGH TO TAKE RISKS WILL ACCOMPLISH NOTHING IN LIFE 3 IT

The Party Is Over U.S. Automotive Outlooks

The Party Is Over U.S. Automotive Outlooks Yen Chen Senior Research Economist Center for Automotive Research Federal Reserve Bank of Chicago Economic Outlook Symposium December 1, 2017 U.S. Light Vehicle

The Party Is Over U.S. Automotive Outlooks Yen Chen Senior Research Economist Center for Automotive Research Federal Reserve Bank of Chicago Economic Outlook Symposium December 1, 2017 U.S. Light Vehicle

ECONOMIC CALENDAR 2010

J.P. Morgan ECONOMIC CALENDAR 2010 Release dates for US economic indicators and Treasury auctions J.P. Morgan ECONOMIC CALENDAR 2010 Release dates for US economic indicators and Treasury auctions This

J.P. Morgan ECONOMIC CALENDAR 2010 Release dates for US economic indicators and Treasury auctions J.P. Morgan ECONOMIC CALENDAR 2010 Release dates for US economic indicators and Treasury auctions This

Have You Ever Heard the Phrase

Setting the Stage with Dairy Outlook Mark Stephenson Director of Dairy Policy Analysis Have You Ever Heard the Phrase! 3M Money Makes Milk! 5M More Money Makes More Milk! 7M Much More Money Makes Much

Setting the Stage with Dairy Outlook Mark Stephenson Director of Dairy Policy Analysis Have You Ever Heard the Phrase! 3M Money Makes Milk! 5M More Money Makes More Milk! 7M Much More Money Makes Much

2019 Market Outlook. Jeff Tumbarello Director SWFL REIA Broker/Owner Steelbridge Realty LLC

2019 Market Outlook Jeff Tumbarello Director SWFL REIA Broker/Owner Steelbridge Realty LLC Data from MLS (exported 1/14/2019 9:26 AM) and public records. Trended with Microsoft excel. Unless otherwise

2019 Market Outlook Jeff Tumbarello Director SWFL REIA Broker/Owner Steelbridge Realty LLC Data from MLS (exported 1/14/2019 9:26 AM) and public records. Trended with Microsoft excel. Unless otherwise

Demographic change, long-run housing demand and the related challenges for the Irish banking sector

Demographic change, long-run housing demand and the related challenges for the Irish banking sector December 5 th, 2016 esri.ie David Duffy, Daniel Foley, Kieran McQuinn and Niall McInerney Outline: Addresses

Demographic change, long-run housing demand and the related challenges for the Irish banking sector December 5 th, 2016 esri.ie David Duffy, Daniel Foley, Kieran McQuinn and Niall McInerney Outline: Addresses

RISI EUROPEAN CONFERENCE. (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last?

The European Economy Things look good just now. Can this last?") RISI EUROPEAN CONFERENCE (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last? Andrea Boltho Magdalen College University of Oxford and Oxford Economics CONCLUSIONS OF

RISI EUROPEAN CONFERENCE (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last? Andrea Boltho Magdalen College University of Oxford and Oxford Economics CONCLUSIONS OF

Conference Welcome and Introduction

Conference 2013 Welcome and Introduction Housing stock Present day Owner occupation Private renting 17.5m 4m 66% 15.1% Housing associations Council housing 2.8m 2.2m 26.5m 10.6% 8.3% > 2.8m Social Housing

Conference 2013 Welcome and Introduction Housing stock Present day Owner occupation Private renting 17.5m 4m 66% 15.1% Housing associations Council housing 2.8m 2.2m 26.5m 10.6% 8.3% > 2.8m Social Housing

Latin American Capital Markets:

Latin American Capital Markets: Stylized Facts, Recent Developments, and Issues FEDERAL RESERVE BANK OF NEW YORK October 18, 2007 Augusto de la Torre The World Bank Structure of presentation Medium-term

Latin American Capital Markets: Stylized Facts, Recent Developments, and Issues FEDERAL RESERVE BANK OF NEW YORK October 18, 2007 Augusto de la Torre The World Bank Structure of presentation Medium-term

OCEAN2012 Fish Dependence Day - UK

OCEAN2012 Fish Dependence Day - UK Europeans are now so dependent on fish products originating from external waters that half the fish they consume are sourced outside the EU Fish dependence: The EU s

OCEAN2012 Fish Dependence Day - UK Europeans are now so dependent on fish products originating from external waters that half the fish they consume are sourced outside the EU Fish dependence: The EU s

Manufacturers Continue Capacity Expansion as Technology Orders Grow

Contact: Penny Brown, AMT, 703-827-5275 pbrown@amtonline.org For Release: October 8th, 2018 Manufacturers Continue Capacity Expansion as Technology Orders Grow Manufacturing technology orders posted an

Contact: Penny Brown, AMT, 703-827-5275 pbrown@amtonline.org For Release: October 8th, 2018 Manufacturers Continue Capacity Expansion as Technology Orders Grow Manufacturing technology orders posted an

Macro-economic risk and the outlook for aviation

Macro-economic risk and the outlook for aviation 25 th January 2018, Dublin Brian Pearce, Chief Economist, IATA www.iata.org/economics Macro matters 24% 20% Global GDP and RPK growth 12% 10% 16% 12% 8%

Macro-economic risk and the outlook for aviation 25 th January 2018, Dublin Brian Pearce, Chief Economist, IATA www.iata.org/economics Macro matters 24% 20% Global GDP and RPK growth 12% 10% 16% 12% 8%

Opening address for dinner-debate

Opening address for dinner-debate Mohammed Barkindo Acting for the OPEC Secretary General European Parliament Strasbourg, France 4 July 2006 1 Outline Importance of EU-OPEC Energy Dialogue Current oil

Opening address for dinner-debate Mohammed Barkindo Acting for the OPEC Secretary General European Parliament Strasbourg, France 4 July 2006 1 Outline Importance of EU-OPEC Energy Dialogue Current oil

Lisbon, June 19, 2012

COLOMBIA: STABILITY FOR FINANCIAL DEVELOPMENT José Darío Uribe E. Governor Central Bank of Colombia Lisbon, June 19, 2012 Firstly, during the last decade d the Colombian economy seems to have entered a

COLOMBIA: STABILITY FOR FINANCIAL DEVELOPMENT José Darío Uribe E. Governor Central Bank of Colombia Lisbon, June 19, 2012 Firstly, during the last decade d the Colombian economy seems to have entered a

RBC Economics Financial Update Dawn Desjardins

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

Can China Pilot a Soft Landing? 2017 Article IV Consultation Analysis, Outlook, and Policy Advice

Can China Pilot a Soft Landing? 2017 Article IV Consultation Analysis, Outlook, and Policy Advice September 2017 1 KEY RECENT DEVELOPMENTS China has had strong growth momentum which Real GDP Real GDP Stabilizes

Can China Pilot a Soft Landing? 2017 Article IV Consultation Analysis, Outlook, and Policy Advice September 2017 1 KEY RECENT DEVELOPMENTS China has had strong growth momentum which Real GDP Real GDP Stabilizes

The Ongoing Recession: How Long and How Deep? Robert J. Gordon Northwestern University and NBER BAC Meeting October 22, 2008

The Ongoing Recession: How Long and How Deep? Robert J. Gordon Northwestern University and NBER BAC Meeting October 22, 2008 No Debate About Recession (1) So Why Hasn t the Recession been Officially Declared?

The Ongoing Recession: How Long and How Deep? Robert J. Gordon Northwestern University and NBER BAC Meeting October 22, 2008 No Debate About Recession (1) So Why Hasn t the Recession been Officially Declared?

U.S. Oil & Gas Industry Chartbook

U.S. Oil & Gas Industry Chartbook BBVA Research USA Houston, TX July 2015 DISCLAIMER This document was prepared by Banco Bilbao Vizcaya Argentaria s (BBVA) BBVA Research U.S. on behalf of itself and its

U.S. Oil & Gas Industry Chartbook BBVA Research USA Houston, TX July 2015 DISCLAIMER This document was prepared by Banco Bilbao Vizcaya Argentaria s (BBVA) BBVA Research U.S. on behalf of itself and its

Emerging from the euro debt crisis Making the single currency work

Emerging from the euro debt crisis Making the single currency work Dr. Michael Heise, Allianz SE American Institute for Contemporary German Studies Johns Hopkins University Washington D.C., August 20,

Emerging from the euro debt crisis Making the single currency work Dr. Michael Heise, Allianz SE American Institute for Contemporary German Studies Johns Hopkins University Washington D.C., August 20,

International Investment Position of Malta: 2016

21 March 2017 1100 hrs 050/2017 As at the end of 2016, the Maltese economy recorded a net International Investment Position of 4.7 billion. International Investment Position of Malta: 2016 Cut-off date:

21 March 2017 1100 hrs 050/2017 As at the end of 2016, the Maltese economy recorded a net International Investment Position of 4.7 billion. International Investment Position of Malta: 2016 Cut-off date:

A Global Partnership For a Just Transition. Kevin P. Gallagher, Director

A Global Partnership For a Just Transition Kevin P. Gallagher, Director What is his point? The multilateral system stemming from the UN Charter and the United Nations Monetary and Financial Conference

A Global Partnership For a Just Transition Kevin P. Gallagher, Director What is his point? The multilateral system stemming from the UN Charter and the United Nations Monetary and Financial Conference

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six years of steady growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half Full

The Economic Outlook Economic Policy Division Glass Half Full Six years of steady growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half Full

Lost in Translation: (In)Coherence Between Agricultural and Development Policy

Coherence Between Agricultural and Development Policy") Lost in Translation: (In)Coherence Between Agricultural and Development Policy Eugenio Díaz-Bonilla Agricultural Trade Policy in the U.S. Can reform advance domestic policy objectives and sustainable development?

Lost in Translation: (In)Coherence Between Agricultural and Development Policy Eugenio Díaz-Bonilla Agricultural Trade Policy in the U.S. Can reform advance domestic policy objectives and sustainable development?

Curves On The Road Ahead

Curves On The Road Ahead Light Vehicle Market Outlook November 2018 Charles Chesbrough Senior Economist A g e n d a Economic Outlook and New Vehicle Sales Affordability Threat and the Used Vehicle Market

Curves On The Road Ahead Light Vehicle Market Outlook November 2018 Charles Chesbrough Senior Economist A g e n d a Economic Outlook and New Vehicle Sales Affordability Threat and the Used Vehicle Market

Iowa Farmland Market Update: What s Ahead?

Iowa Farmland Market Update: What s Ahead? Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 Ag Credit School, June 14 th, 2017 The new Mike Duffy

Iowa Farmland Market Update: What s Ahead? Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 Ag Credit School, June 14 th, 2017 The new Mike Duffy

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis. May 8 th, Presented by:

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis May 8 th, 2008 Presented by: Patricia Croft, Vice President & Chief Economist Phillips, Hager & North Investment Management Limited

Outlook 2008/09 Life In the Aftermath of the Great Global Credit Crisis May 8 th, 2008 Presented by: Patricia Croft, Vice President & Chief Economist Phillips, Hager & North Investment Management Limited

Composition of Federal Spending

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

MBA Economic and Mortgage Finance Outlook

MBA Economic and Mortgage Finance Outlook MBA of Alabama Annual Conference June 7, 2017 Presented by Lynn Fisher Mortgage Bankers Association 1 Summary of the MBA Outlook 2016 2017 2018 2019 GDP Growth

MBA Economic and Mortgage Finance Outlook MBA of Alabama Annual Conference June 7, 2017 Presented by Lynn Fisher Mortgage Bankers Association 1 Summary of the MBA Outlook 2016 2017 2018 2019 GDP Growth

Hotel Industry Update. Stephen Hennis, CHA, ISHC

Hotel Industry Update Stephen Hennis, CHA, ISHC 1 Through Aug 2012: Strong Results Despite Headwinds % Change Room Supply* 1.2 bn 0.4% Room Demand* 741 mm 3.3% Occupancy 63% 2.9% A.D.R. $106 4.3% RevPAR

Hotel Industry Update Stephen Hennis, CHA, ISHC 1 Through Aug 2012: Strong Results Despite Headwinds % Change Room Supply* 1.2 bn 0.4% Room Demand* 741 mm 3.3% Occupancy 63% 2.9% A.D.R. $106 4.3% RevPAR

Discussion of: The Rise, the Fall, and the Resurrection of Iceland by Benediksdottir, Eggertsson, Þorarinsson. Jón Steinsson Columbia University

Discussion of: The Rise, the Fall, and the Resurrection of Iceland by Benediksdottir, Eggertsson, Þorarinsson Jón Steinsson Columbia University Policy Failure 1: Banking Supervision Paper covers this very

Discussion of: The Rise, the Fall, and the Resurrection of Iceland by Benediksdottir, Eggertsson, Þorarinsson Jón Steinsson Columbia University Policy Failure 1: Banking Supervision Paper covers this very

SWISS reports stable load factors

SWISS Corporate Communications Phone: +41 (0)848 773 773 Fax: +41 (0)44 564 2127 communications@swiss.com SWISS.COM Media release Zurich Airport, October 10, 2008 SWISS reports stable load factors SWISS

SWISS Corporate Communications Phone: +41 (0)848 773 773 Fax: +41 (0)44 564 2127 communications@swiss.com SWISS.COM Media release Zurich Airport, October 10, 2008 SWISS reports stable load factors SWISS

Monetary policy in a fixedexchange-rate. Presentation by Anders Møller Christensen Assistant Governor, Danmarks Nationalbank May 2006

Monetary policy in a fixedexchange-rate regime Presentation by Anders Møller Christensen Assistant Governor, Danmarks Nationalbank May 2006 MONETARY-POLICY STRATEGIES 24-05-2006 DANMARKS NATIONALBANK 2

Monetary policy in a fixedexchange-rate regime Presentation by Anders Møller Christensen Assistant Governor, Danmarks Nationalbank May 2006 MONETARY-POLICY STRATEGIES 24-05-2006 DANMARKS NATIONALBANK 2