Farm Sector Income & Finances 2016 Outlook. By Ryan Kuhns and Kevin Patrick March 16, 2016

|

|

|

- Gilbert Spencer

- 6 years ago

- Views:

Transcription

1 Farm Sector Income & Finances 2016 Outlook By Ryan Kuhns and Kevin Patrick March 16, 2016

2 Background The Economic Research Service forecasts the farm sector s income statement and balance sheet Last released February 9 th Includes 2015 and 2016 forecasts of: Income statement Balance sheet Financial metrics Farm business-level outlook 2

3 Net cash income (NCI) forecast down 2.5% in

4 Crop receipts drive the expected decline in NCI from 2013 to

5 2016F crop receipts significantly lower than 2013, but flat from

6 Animal receipts are also expected to fall for most categories in

7 $ billion 14 Government payments are forecast to rise over 30 percent in F 2016F F= Forecast. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics using FSA, NRCS, and CCC data. Data as of February 9,

8 $ billion 14 Government payments based on price are a larger share in F 2016F F= Forecast. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics using FSA, NRCS, and CCC data. Data as of February 9, Fixed payments Crop price based payments All other payments PLC, ARC, ACRE, counter-cyclical payments, and other programs where payments vary with market prices. Fixed direct payments and cotton transition payments. Disaster relief payments, tobacco transition payments, dairy program payments, and conservation payments. 8

9 Cash expenses are expected to decline for the second consecutive year $ Billion F 2016F F = forecast. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9,

10 $ billion 60 Feed, fuel, fertilizer, and livestock expenses drive decline in Decreased Increased Feed Livestock & poultry Fertilizer Fuels & Oils Pesticides Labor Net rent Seeds Interest Property taxes/fees F = forecast 2014F Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9, F 2015F 2016F 10

11 Since our first 2015 forecast the outlook for crop receipts improved, and animal and product receipts declined net cash income forecast increased $3.8 billion from February 2015 to February 2016 Net cash income 2015F Crop receipts Animals and products receipts Cash farmrelated income Production Expenses All figures are in $ Billion 2014F Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9, Government Payments 2015F Net cash income 2015F 11

12 Improvement in 2015 crop receipt forecasts largely due to fruits/nuts $ billion Corn Soybeans Feed, food, & oil crops* F= Forecast. * Excluding corn and soybeans. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9, Fruits & nuts 2014F Vegetables & melons 2015F Cotton February 2015 August 2015 November 2015 February

13 Decline in 2015 animal and product receipt forecasts broad based, but largely due to cattle/calves $ billion Cattle and calves Dairy Broilers All other poultry F= Forecast Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9th, F February 2015 August 2015 November 2015 February F 13

14 Farm Sector Balance Sheet Outlook

15 Farm real estate* represents the majority of the sector s assets 15

16 Forecast drop in net cash income drives lower farm real estate values* 16

17 Drop in 2016F farm real estate assets drive change in total assets Percent change Total assets Real estate assets* % decline in real estate assets* from 2015F to 2016F F F= Forecast. *Real estate includes the value of land and buildings Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9,

18 Farm real estate and nonreal estate debt approaching historic levels $ billion (2009 Dollars) Real estate debt 100 Nonreal estate debt F F= Forecast. Values are adjusted using the chain-type GDP deflator, 2009=100. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9,

19 But below the late 70s early 80s peak in inflation-adjusted terms $ billion (2009 Dollars) Real estate debt 100 Nonreal estate debt F F= Forecast. Values are adjusted using the chain-type GDP deflator, 2009=100. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9,

20 Farm debt is forecast to grow rapidly from 2013 to

21 Leverage increased since 2012, but remains low relative to historic levels 21

22 Rate of return on farm assets (ROA) expected to remain flat in Rate of return on assets from income F F = forecast. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9,

23 Rate of return on farm assets (ROA) expected to remain flat in Rate of return on assets from income F F = forecast. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9, Decomposing the rate of return on farm assets (ROA) ROA = Asset Turnover Ratio Profit Margin Ratio Value of production that assets generate Profit margin on value of production 23

24 Rate of return on farm assets (ROA) expected to remain flat in Rate of return on assets from income F F = forecast. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9, Decomposing the rate of return on farm assets (ROA) ROA = Asset Turnover Ratio Profit Margin Ratio Value of production that assets generate Profit margin on value of production 24

25 Lower profit margins drive decline in ROA from 2013 to Rate of return on assets from income F 0.19 Asset Turnover Ratio Operating profit margin ratio F F = forecast. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9,

26 Lower profit margin ratio in 2015 and 2016 consistent with other low income years Asset Turnover Ratio Operating profit margin ratio F F = forecast. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9,

27 Farm Business Outlook

28 Farm businesses account for 45% of farms, but over 90% of production Operators report they are retired or have a major occupation other than farming. Gross cash farm income less than $350,000 and operators report farming as their major occupation. Farm Businesses Residence Intermediate Commercial Gross cash farm income greater than $350,000 and farms organized as nonfamily corporations or cooperatives. Source: 2014 Agricultural Resource Management Survey (ARMS) 28

29 Average net cash income up for most crop farm businesses 1/ F 2016F 29

30 Average net cash income expected to fall for most farm businesses specializing in animals and products 1/ F 2016F 30

31 All Farm Businesses $87,700 in

32 Share of highly leveraged crop farm businesses increased substantially since 2011 Percent of farm businesses 10% Crops 8% 6.1% 5% 5.0% 3% 0% F D/A (41-70) D/A (71 +) F = forecast. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9,

33 Share of highly leveraged animal and product farm businesses also trending upward since 2011 Percent of farm businesses 10% Animals and products 8% 5% 5.4% 3% 3.4% 0% F D/A (41-70) D/A (71 +) F = forecast. Source: USDA, Economic Research Service, Farm Income and Wealth Statistics. Data as of February 9,

34 Presentation takeaways Net cash income expected down slightly in 2016, but relatively flat from Large declines in net cash income since 2013 are driven by lower crop receipts paired with increasing expenses. Lower income is expected to put modest downward pressure on farm real estate asset values. Changes in farm real estate asset values drive changes in total farm assets. Farm debt, particularly nonreal estate debt, has grown rapidly since Inflation-adjusted debt nearing historic highs, but remains below 1970s-1980s peak. Financial metrics indicate the farm sector remains in good standing. An increasing but small group of farms is highly leveraged. 34

35 Additional analysis and data Farm Sector Income and Wealth Statistics Data product updated 3 times per year. Next update: August 30th, Historical State Estimates Historical National Estimates National Forecasts 35

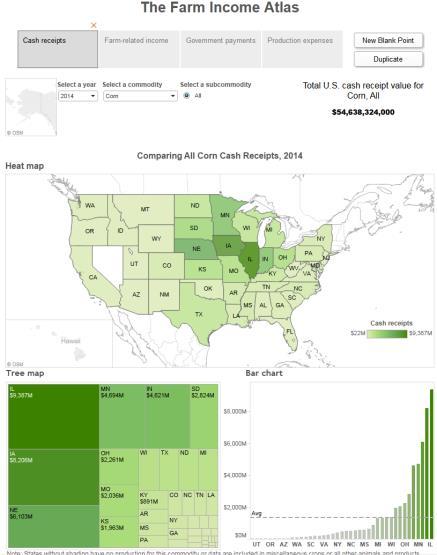

36 Explore the data Visualizations let you dive into the financials of the farm sector Get to Know Your State Digging into the Farm Balance Sheet Farm Income Atlas 36

37 QUESTIONS? Ryan Kuhns Kevin Patrick Farm Income Team 37

An Agricultural Update

An Agricultural Update May 22, 2018 Indianapolis, IN David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Personal consumption shares 40% 30% 20% 10% 0% 1950 1960 1970 1980

An Agricultural Update May 22, 2018 Indianapolis, IN David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Personal consumption shares 40% 30% 20% 10% 0% 1950 1960 1970 1980

2016 Farm Income and 2017 Cost Outlook

2016 Farm Income and 2017 Cost Outlook Dr. Paul D. Mitchell Associate Professor, UW Ag and Applied Economics Extension State Specialist, Cropping Systems Management Director, Renk Agribusiness Institute

2016 Farm Income and 2017 Cost Outlook Dr. Paul D. Mitchell Associate Professor, UW Ag and Applied Economics Extension State Specialist, Cropping Systems Management Director, Renk Agribusiness Institute

Macro and Agricultural Economic Outlook FCL 2017 Annual Meeting. Tanner Ehmke, Manager Knowledge Exchange Division

Macro and Agricultural Economic Outlook FCL 2017 Annual Meeting Tanner Ehmke, Manager Knowledge Exchange Division Today s presentation Macro Economy Agricultural Economy 2 The Market Cycle (we ve been

Macro and Agricultural Economic Outlook FCL 2017 Annual Meeting Tanner Ehmke, Manager Knowledge Exchange Division Today s presentation Macro Economy Agricultural Economy 2 The Market Cycle (we ve been

Agriculture and the Economy: A View from the Chicago Fed

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Outlook for U.S. Retail Food Prices and Inflation in 2009

Outlook for U.S. Retail Food Prices and Inflation in 2009 Ephraim Leibtag, PhD Food Markets Branch, Food Economics Division ERS-USDA Presented at the 2009 Agricultural Outlook Forum Global Agriculture

Outlook for U.S. Retail Food Prices and Inflation in 2009 Ephraim Leibtag, PhD Food Markets Branch, Food Economics Division ERS-USDA Presented at the 2009 Agricultural Outlook Forum Global Agriculture

Page 1. USDA s Mandatory Farm Programs CBO s January 2019 Baseline

USDA s Mandatory Farm Programs CBO s January 2019 Baseline Page 1 The federal Commodity Credit Corporation (CCC) accounts for a significant portion of mandatory federal spending for agriculture through

USDA s Mandatory Farm Programs CBO s January 2019 Baseline Page 1 The federal Commodity Credit Corporation (CCC) accounts for a significant portion of mandatory federal spending for agriculture through

A Primer on Factors Affecting Farmland Values

A Primer on Factors Affecting Farmland Values Federal Reserve Bank of Chicago David Oppedahl Business Economist 312-322-6122 david.oppedahl@chi.frb.org The economy hit bottom in June 2009, with hesitant

A Primer on Factors Affecting Farmland Values Federal Reserve Bank of Chicago David Oppedahl Business Economist 312-322-6122 david.oppedahl@chi.frb.org The economy hit bottom in June 2009, with hesitant

OUTLOOK FOR US AGRICULTURE. Rob Johansson Acting Chief Economist 19 February 2015

OUTLOOK FOR US AGRICULTURE Rob Johansson Acting Chief Economist 19 February 2015 Fig 1 Next boost to productivity: Big Data? Index: 1948 = 1.0 $million (2006 dollars) 3.0 $12,000 2.5 2.0 $R&D Output Input

OUTLOOK FOR US AGRICULTURE Rob Johansson Acting Chief Economist 19 February 2015 Fig 1 Next boost to productivity: Big Data? Index: 1948 = 1.0 $million (2006 dollars) 3.0 $12,000 2.5 2.0 $R&D Output Input

The Changing Business Climate for Agriculture The Outlook for 2015

The Changing Business Climate for Agriculture The Outlook for 2015 Chris Hurt, Professor of Ag. Economics & Extension Economist James Mintert, Director, Center for Commercial Agriculture Michael Langemeier,

The Changing Business Climate for Agriculture The Outlook for 2015 Chris Hurt, Professor of Ag. Economics & Extension Economist James Mintert, Director, Center for Commercial Agriculture Michael Langemeier,

Presentation from the USDA Agricultural Outlook Forum 2017

Presentation from the USDA Agricultural Outlook Forum 2017 United States Department of Agriculture 93 rd Annual Agricultural Outlook Forum A New Horizon: The Future of Agriculture February 23-24, 2017

Presentation from the USDA Agricultural Outlook Forum 2017 United States Department of Agriculture 93 rd Annual Agricultural Outlook Forum A New Horizon: The Future of Agriculture February 23-24, 2017

Agricultural Outlook: Rebalancing U.S. Agriculture

Agricultural Outlook: Rebalancing U.S. Agriculture Michael J. Swanson Ph.D. Agricultural Economist January 2018 2018 Wells Fargo Bank, N.A. All rights reserved. For public use. The U.S. Ag Sector renormalizes!

Agricultural Outlook: Rebalancing U.S. Agriculture Michael J. Swanson Ph.D. Agricultural Economist January 2018 2018 Wells Fargo Bank, N.A. All rights reserved. For public use. The U.S. Ag Sector renormalizes!

Toward an Outlook for California Agriculture Relevant to GHG Emissions Mitigation. April 30, Daniel A. Sumner

Toward an Outlook for California Agriculture Relevant to GHG Emissions Mitigation April 30, 2013 Daniel A. Sumner University of California Agricultural Issues Center and UC Davis, Agricultural and Resource

Toward an Outlook for California Agriculture Relevant to GHG Emissions Mitigation April 30, 2013 Daniel A. Sumner University of California Agricultural Issues Center and UC Davis, Agricultural and Resource

State of the Ag Economy

State of the Ag Economy June 10, 2017 Chad Hart Associate Professor/Crop Marketing Specialist chart@iastate.edu 515-294-9911 Ag Productivity and Usage Using corn as an example Source: USDA Ag Prices Using

State of the Ag Economy June 10, 2017 Chad Hart Associate Professor/Crop Marketing Specialist chart@iastate.edu 515-294-9911 Ag Productivity and Usage Using corn as an example Source: USDA Ag Prices Using

Issues Driving the Outlook for Specialty Crops December 3, 2012

Issues Driving the Outlook for Specialty Crops December 3, 2012 Daniel A. Sumner University of California Agricultural Issues Center, and UC Davis Department of Agricultural and Resource Economics Core

Issues Driving the Outlook for Specialty Crops December 3, 2012 Daniel A. Sumner University of California Agricultural Issues Center, and UC Davis Department of Agricultural and Resource Economics Core

Farmland Booms and Busts: Will the Cycle be Broken?

Farmland Booms and Busts: Will the Cycle be Broken? Kansas Society of Farm Managers and Rural Appraisers Salina, KS February 23 rd, 2012 Brian C. Briggeman Associate Professor and Director of the Arthur

Farmland Booms and Busts: Will the Cycle be Broken? Kansas Society of Farm Managers and Rural Appraisers Salina, KS February 23 rd, 2012 Brian C. Briggeman Associate Professor and Director of the Arthur

colorado.edu/business/brd

colorado.edu/business/brd Big Changes, Unknown Impacts Southwest Business Forum Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January

colorado.edu/business/brd Big Changes, Unknown Impacts Southwest Business Forum Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January

Economic Analysis of Farmland Market: An Introduction

Economic Analysis of Farmland Market: An Introduction Dr. Wendong Zhang Assistant Professor of Economics wdzhang@iastate.edu FIN 450X, Feb 17 th, 2017 A Quick Introduction: Dr. Wendong Zhang Grown up in

Economic Analysis of Farmland Market: An Introduction Dr. Wendong Zhang Assistant Professor of Economics wdzhang@iastate.edu FIN 450X, Feb 17 th, 2017 A Quick Introduction: Dr. Wendong Zhang Grown up in

AG OUTLOOK 2019: GROWING LOCALLY, SELLING GLOBALLY

AG OUTLOOK 2019: GROWING LOCALLY, SELLING GLOBALLY http://www.goldenrice.org/ Robert Johansson Chief Economist, USDA Feb 2019 Credit: COURTESY OF NIC BENNER University of Missouri 2 Outline https://finance.yahoo.com/chart

AG OUTLOOK 2019: GROWING LOCALLY, SELLING GLOBALLY http://www.goldenrice.org/ Robert Johansson Chief Economist, USDA Feb 2019 Credit: COURTESY OF NIC BENNER University of Missouri 2 Outline https://finance.yahoo.com/chart

Outlook for the U.S. Livestock and Poultry Sectors in 2012 Presented By Shayle D. Shagam World Agricultural Outlook Board, USDA

Outlook for the U.S. Livestock and Poultry Sectors in 2012 Presented By Shayle D. Shagam World Agricultural Outlook Board, USDA USDA Outlook Forum Washington, D.C. February 24, 2012 Situation Facing Livestock

Outlook for the U.S. Livestock and Poultry Sectors in 2012 Presented By Shayle D. Shagam World Agricultural Outlook Board, USDA USDA Outlook Forum Washington, D.C. February 24, 2012 Situation Facing Livestock

Commodity Market Outlook: Corn, Forage, Wheat & Cattle

Commodity Market Outlook: Corn, Forage, Wheat & Cattle Stephen R. Koontz Professor & extension economist Department of Agricultural & Resource Economics Colorado State University Stephen.Koontz@ColoState.Edu

Commodity Market Outlook: Corn, Forage, Wheat & Cattle Stephen R. Koontz Professor & extension economist Department of Agricultural & Resource Economics Colorado State University Stephen.Koontz@ColoState.Edu

Exhibit #MH-156. ELECTRIC OPERATIONS (MH10-2) PROJECTED OPERATING STATEMENT (In Millions of Dollars) For the year ended March 31 REVENUES

PROJECTED OPERATING STATEMENT (In Millions of Dollars) For the year ended March 31 REVENUES") PROJECTED OPERATING STATEMENT 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 REVENUES General Consumers at approved rates 1,194 1,223 1,235 1,254 1,265 1,279 1,296 1,307 1,320 1,336 additional * - 42

PROJECTED OPERATING STATEMENT 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 REVENUES General Consumers at approved rates 1,194 1,223 1,235 1,254 1,265 1,279 1,296 1,307 1,320 1,336 additional * - 42

Land Values and Chinese Agriculture

Land Values and Chinese Agriculture Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 2016 Pro-Ag Meetings, Clarinda, IA, December 15 th, 2016 The

Land Values and Chinese Agriculture Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 2016 Pro-Ag Meetings, Clarinda, IA, December 15 th, 2016 The

Iowa Land Values. Wendong Zhang Assistant Professor of Economics and Extension Economist

Iowa Land Values Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 2017 U.S. Bank Ag Summit, Ames, IA, January 10 th, 2017 The new Mike Duffy 30 29

Iowa Land Values Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 2017 U.S. Bank Ag Summit, Ames, IA, January 10 th, 2017 The new Mike Duffy 30 29

Iowa Farmland Market Update: What s Ahead?

Iowa Farmland Market Update: What s Ahead? Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 April 4 th, 2017 The new Mike Duffy since Aug 2015 30

Iowa Farmland Market Update: What s Ahead? Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 April 4 th, 2017 The new Mike Duffy since Aug 2015 30

Outlook for the U.S. Livestock and Poultry Sectors in 2011

Outlook for the U.S. Livestock and Poultry Sectors in 2011 Presented By Shayle D. Shagam World Agricultural Outlook Board, USDA USDA Outlook Forum Washington, D.C. February 25, 2011 Situation Facing Livestock

Outlook for the U.S. Livestock and Poultry Sectors in 2011 Presented By Shayle D. Shagam World Agricultural Outlook Board, USDA USDA Outlook Forum Washington, D.C. February 25, 2011 Situation Facing Livestock

SFSA Business Outlook Raymond Monroe

SFSA Business Outlook 2010 Raymond Monroe 815-455-8240 monroe@sfsa.org http://blog.american.com/?p=2991 Agriculture Workers http://www.worldmapper.org/display.php?selected=128 Population http://www.worldmapper.org/display.php?selected=2

SFSA Business Outlook 2010 Raymond Monroe 815-455-8240 monroe@sfsa.org http://blog.american.com/?p=2991 Agriculture Workers http://www.worldmapper.org/display.php?selected=128 Population http://www.worldmapper.org/display.php?selected=2

Farm Bill Economics and Expectations

Farm Bill Economics and Expectations Bradley D. Lubben, Ph.D. Extension Associate Professor, Policy Specialist, Faculty Fellow, Rural Futures Institute, and Director, North Central Extension Risk Management

Farm Bill Economics and Expectations Bradley D. Lubben, Ph.D. Extension Associate Professor, Policy Specialist, Faculty Fellow, Rural Futures Institute, and Director, North Central Extension Risk Management

2018 Farm Bill Update and Agricultural Outlook

2018 Farm Bill Update and Agricultural Outlook August 23, 2018 Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences brownsc@missouri.edu http://amap.missouri.edu 2018 Farm

2018 Farm Bill Update and Agricultural Outlook August 23, 2018 Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences brownsc@missouri.edu http://amap.missouri.edu 2018 Farm

Shifting International Trade Routes A National Economic Outlook. February 1, 2011

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

2018(?) FARM BILL DISCUSSION

FARM BILL DISCUSSION") 2018(?) FARM BILL DISCUSSION Jonathan Coppess Gardner Agricultural Policy Program ISPFMRA Annual Meeting (February 8, 2018) www.farmdocdaily.illinois.edu www.farmdoc.illinois.edu Part 1. FARM BILL HISTORICAL

2018(?) FARM BILL DISCUSSION Jonathan Coppess Gardner Agricultural Policy Program ISPFMRA Annual Meeting (February 8, 2018) www.farmdocdaily.illinois.edu www.farmdoc.illinois.edu Part 1. FARM BILL HISTORICAL

USDA National Agricultural Statistics Service

USDA National Agricultural Statistics Service Bruce Eklund, State Statistician New Jersey Field Office NASS Reports Over 400 National reports published annually Over 9,000 State-level reports annually

USDA National Agricultural Statistics Service Bruce Eklund, State Statistician New Jersey Field Office NASS Reports Over 400 National reports published annually Over 9,000 State-level reports annually

California Agriculture and Global Challenges: Resources Prices and Prospects 2012 California Ag Summit January 27, 2012

California Agriculture and Global Challenges: Resources Prices and Prospects 2012 California Ag Summit uary 27, 2012 Daniel A. Sumner University of California Agricultural Issues Center Outline and Main

California Agriculture and Global Challenges: Resources Prices and Prospects 2012 California Ag Summit uary 27, 2012 Daniel A. Sumner University of California Agricultural Issues Center Outline and Main

California Agriculture 2001: Trends and Issues

California Agriculture 2001: Trends and Issues Daniel A. Sumner Professor, Department of Agricultural and Resource Economics, UC Davis Director, University of California Agricultural Issues Center The

California Agriculture 2001: Trends and Issues Daniel A. Sumner Professor, Department of Agricultural and Resource Economics, UC Davis Director, University of California Agricultural Issues Center The

Profile and Economic Impacts of Agriculture and Natural Resource Industries in the Suwannee River Basin Counties of Florida

FE622 Profile and Economic Impacts of Agriculture and Natural Resource Industries in the River Basin Counties of Florida M. Rahmani, A.W. Hodges, and W.D. Mulkey University of Florida/Institute of Food

FE622 Profile and Economic Impacts of Agriculture and Natural Resource Industries in the River Basin Counties of Florida M. Rahmani, A.W. Hodges, and W.D. Mulkey University of Florida/Institute of Food

Cattle & Beef Outlook

Cattle & Beef Outlook Glynn Tonsor Dept. of Agricultural Economics, Kansas State University Overarching Beef Industry Economic Outlook Supplies Peak herd size may extend given 17 returns Demand Key to

Cattle & Beef Outlook Glynn Tonsor Dept. of Agricultural Economics, Kansas State University Overarching Beef Industry Economic Outlook Supplies Peak herd size may extend given 17 returns Demand Key to

Big Changes, Unknown Impacts

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Agriculture Outlook. Rich Pottorff Doane Advisory Services

Agriculture Outlook Rich Pottorff Doane Advisory Services General Outline An overview of U.S. crop markets Corn, soybeans, wheat & cotton Some factors shaping the outlook World Ag Situation Conclusions

Agriculture Outlook Rich Pottorff Doane Advisory Services General Outline An overview of U.S. crop markets Corn, soybeans, wheat & cotton Some factors shaping the outlook World Ag Situation Conclusions

Iowa Farmland Market Update: What s Ahead?

Iowa Farmland Market Update: What s Ahead? Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 Ag Credit School, June 14 th, 2017 The new Mike Duffy

Iowa Farmland Market Update: What s Ahead? Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 Ag Credit School, June 14 th, 2017 The new Mike Duffy

USDA National Agricultural Statistics Service

USDA National Agricultural Statistics Service Bruce Eklund, State Statistician New Jersey Field Office Data Products Find NASS Data Methodology Relevance Networking / Humility Know Thy Data Multi Tasking?

USDA National Agricultural Statistics Service Bruce Eklund, State Statistician New Jersey Field Office Data Products Find NASS Data Methodology Relevance Networking / Humility Know Thy Data Multi Tasking?

Indiana Electricity Projections: The 2018 Forecast Update

Indiana Electricity Projections: The 2018 Forecast Update State Utility Forecasting Group The Energy Center at Discovery Park Purdue University West Lafayette, Indiana October 2018 Summary This report

Indiana Electricity Projections: The 2018 Forecast Update State Utility Forecasting Group The Energy Center at Discovery Park Purdue University West Lafayette, Indiana October 2018 Summary This report

Real GDP Growth Quarterly Real GDP

Real GDP Growth Quarterly Real GDP Percent Change, SAAR 10.0 8.0 6.0 4.0 2.0 0.0-2.0-4.0-6.0-8.0-10.0 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 Sources: Bureau of Economic Analysis

Real GDP Growth Quarterly Real GDP Percent Change, SAAR 10.0 8.0 6.0 4.0 2.0 0.0-2.0-4.0-6.0-8.0-10.0 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 Sources: Bureau of Economic Analysis

Economic Outlook. Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project

Economic Outlook Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project League of California Cities Monterey, CA December 3, 2014 Economic Update economic

Economic Outlook Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project League of California Cities Monterey, CA December 3, 2014 Economic Update economic

President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H. Parker Willis Lecture in Political Economics

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

CBO s January Baseline Sets the Stage. CRFB.org

CBO s January Baseline Sets the Stage 1 Trillion-Dollar Deficits Are Returning $1,600 Billions $1,400 $1,200 $1,000 $800 Deficits Increased Almost 800% Deficits Fell 69% Deficits Triple to Nearly $1.4

CBO s January Baseline Sets the Stage 1 Trillion-Dollar Deficits Are Returning $1,600 Billions $1,400 $1,200 $1,000 $800 Deficits Increased Almost 800% Deficits Fell 69% Deficits Triple to Nearly $1.4

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

BMO Capital Markets 2014 Farm to Market Conference New York, New York. May 21, 2014

0 BMO Capital Markets 2014 Farm to Market Conference New York, New York May 21, 2014 1 Forward Looking Statement Warning This presentation contains forward-looking statements about the business, financial

0 BMO Capital Markets 2014 Farm to Market Conference New York, New York May 21, 2014 1 Forward Looking Statement Warning This presentation contains forward-looking statements about the business, financial

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

A Distant Mirror: Credit contraction, monetary policy and commodity prices during the Great Depression. John Kemp Reuters 30 January 2009

A Distant Mirror: Credit contraction, monetary policy and commodity prices during the Great Depression John Kemp Reuters 3 January 29 BORROWING BOOM IN 192s. FOLLOWED BY DE-LEVERAGING IN 193s U.S.$ bn

A Distant Mirror: Credit contraction, monetary policy and commodity prices during the Great Depression John Kemp Reuters 3 January 29 BORROWING BOOM IN 192s. FOLLOWED BY DE-LEVERAGING IN 193s U.S.$ bn

More of the Same; Or now for Something Completely Different?

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

2017/18 Soybean Outlook

217/18 Soybean Outlook 217 Ag Econ In service Training Dr. S. Aaron Smith, Assistant Professor, Department of Agricultural and Resource Economics, University of Tennessee https://ag.tennessee.edu/arec/pages/cropeconomics.aspx

217/18 Soybean Outlook 217 Ag Econ In service Training Dr. S. Aaron Smith, Assistant Professor, Department of Agricultural and Resource Economics, University of Tennessee https://ag.tennessee.edu/arec/pages/cropeconomics.aspx

Global Outlook for Agriculture Trend versus Cycle

Global Outlook for Agriculture Trend versus Cycle Michael Swanson Ph.D. Wells Fargo October 2017 Everything is connected we just don t see how. Connection corollary: Nothing natural moves in a straight

Global Outlook for Agriculture Trend versus Cycle Michael Swanson Ph.D. Wells Fargo October 2017 Everything is connected we just don t see how. Connection corollary: Nothing natural moves in a straight

Economic Analysis of Farmland Market: An Introduction

Economic Analysis of Farmland Market: An Introduction Dr. Wendong Zhang Assistant Professor of Economics wdzhang@iastate.edu FIN 450X, October 4 th, 2017 A Quick Introduction: Dr. Wendong Zhang Grown up

Economic Analysis of Farmland Market: An Introduction Dr. Wendong Zhang Assistant Professor of Economics wdzhang@iastate.edu FIN 450X, October 4 th, 2017 A Quick Introduction: Dr. Wendong Zhang Grown up

Outlook for Livestock and Poultry. Michael Jewison World Agricultural Outlook Board, USDA

Outlook for Livestock and Poultry Michael Jewison World Agricultural Outlook Board, USDA USDA Agricultural Outlook Forum February 20, 2015 About Those Forecasts Everything makes sense in hindsight, a fact

Outlook for Livestock and Poultry Michael Jewison World Agricultural Outlook Board, USDA USDA Agricultural Outlook Forum February 20, 2015 About Those Forecasts Everything makes sense in hindsight, a fact

Potash Outlook. Kevin Stone Natural Resources Canada. TFI Fertilizer Outlook and Technology Conference Fort Lauderdale, Florida November 16, 2016

1 Potash Outlook Kevin Stone Natural Resources Canada TFI Fertilizer Outlook and Technology Conference Fort Lauderdale, Florida November 16, 2016 2 Outline Historical Consumption and Supply Outlook for

1 Potash Outlook Kevin Stone Natural Resources Canada TFI Fertilizer Outlook and Technology Conference Fort Lauderdale, Florida November 16, 2016 2 Outline Historical Consumption and Supply Outlook for

Cattle Market Outlook & Important Profit Factors for Cattle Producers

Cattle Market Outlook & Important Profit Factors for Cattle Producers Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences brownsc@missouri.edu http://amap.missouri.edu $

Cattle Market Outlook & Important Profit Factors for Cattle Producers Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences brownsc@missouri.edu http://amap.missouri.edu $

The U.S. Economic Outlook

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

PROVINCE OF SASKATCHEWAN INVESTOR PRESENTATION

PROVINCE OF SASKATCHEWAN INVESTOR PRESENTATION May 2018 THE SASKATCHEWAN DIFFERENCE Economic Stability Diversified economy balances cyclicality of resources Growing population Majority government with

PROVINCE OF SASKATCHEWAN INVESTOR PRESENTATION May 2018 THE SASKATCHEWAN DIFFERENCE Economic Stability Diversified economy balances cyclicality of resources Growing population Majority government with

What Lies Beyond The Horizon For Farm Incomes:

What Lies Beyond The Horizon For Farm Incomes: The Case For Volatility With An Upward Bias Sterling Liddell Rabo AgriFinance 314 317 8038 Sterling.Liddell@RaboAg.com July 16, 2012 KC FED Agricultural Symposium

What Lies Beyond The Horizon For Farm Incomes: The Case For Volatility With An Upward Bias Sterling Liddell Rabo AgriFinance 314 317 8038 Sterling.Liddell@RaboAg.com July 16, 2012 KC FED Agricultural Symposium

Beef Outlook. Regional Dealer Event. February 9, Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences

Beef Outlook Regional Dealer Event February 9, 2018 Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences brownsc@missouri.edu http://amap.missouri.edu $ Per Cwt. MED. & LRG.

Beef Outlook Regional Dealer Event February 9, 2018 Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences brownsc@missouri.edu http://amap.missouri.edu $ Per Cwt. MED. & LRG.

Market Update. Randy Tinseth Vice President, Marketing Boeing Commercial Airplanes. Copyright 2016 Boeing. All rights reserved.

Market Update The statements contained herein are based on good faith assumptions are to be used for general information purposes only. These statements do not constitute an offer, promise, warranty or

Market Update The statements contained herein are based on good faith assumptions are to be used for general information purposes only. These statements do not constitute an offer, promise, warranty or

Cattle Situation and Outlook

Photo courtesy of Judy Jacobson, Watford City Cattle Situation and Outlook Tim Petry Livestock Economist www.ndsu.edu/livestockeconomics September 2, 2015 Washburn Livestock Outlook-9-1-15.pptx TO ALL

Photo courtesy of Judy Jacobson, Watford City Cattle Situation and Outlook Tim Petry Livestock Economist www.ndsu.edu/livestockeconomics September 2, 2015 Washburn Livestock Outlook-9-1-15.pptx TO ALL

2017/18 Corn Outlook

217/18 Corn Outlook 217 Ag Econ In service Training Dr. S. Aaron Smith, Assistant Professor, Department of Agricultural and Resource Economics, University of Tennessee https://ag.tennessee.edu/arec/pages/cropeconomics.aspx

217/18 Corn Outlook 217 Ag Econ In service Training Dr. S. Aaron Smith, Assistant Professor, Department of Agricultural and Resource Economics, University of Tennessee https://ag.tennessee.edu/arec/pages/cropeconomics.aspx

The U.S. Economic Recovery: Why so weak and what should be done? William J. Crowder Ph.D.

The U.S. Economic Recovery: Why so weak and what should be done? William J. Crowder Ph.D. Weak Recovery? It s no secret that the U.S. economy has still not fully recovered from the financial crisis and

The U.S. Economic Recovery: Why so weak and what should be done? William J. Crowder Ph.D. Weak Recovery? It s no secret that the U.S. economy has still not fully recovered from the financial crisis and

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

Real Estate: Investing for the Future. Sponsored By:

Real Estate: Investing for the Future Sponsored By: Percent Change, Year Ago 6 5 4 3 2 1 Real GDP Growth United States, 2000 Prices 0 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 U.S. Employment

Real Estate: Investing for the Future Sponsored By: Percent Change, Year Ago 6 5 4 3 2 1 Real GDP Growth United States, 2000 Prices 0 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 U.S. Employment

2019 Economic Outlook: Will the Recovery Ever End?

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

Cattle & Beef Outlook

Cattle & Beef Outlook Friday, August 18, 2017 Glynn Tonsor Dept. of Agricultural Economics, Kansas State University Overarching Beef Industry Economic Outlook Supplies Expansion continues, but has moderated

Cattle & Beef Outlook Friday, August 18, 2017 Glynn Tonsor Dept. of Agricultural Economics, Kansas State University Overarching Beef Industry Economic Outlook Supplies Expansion continues, but has moderated

10 County Conference. Richard Wobbekind. Executive Director Business Research Division & Senior Associate Dean Leeds School of Business

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

Europe June Craig Menear. Chairman, CEO & President. Diane Dayhoff. Vice President, Investor Relations

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

The global economic climate and impact on SA Mining during a downward phase in the commodity cycle.

The global economic climate and impact on SA Mining during a downward phase in the commodity cycle. World Economy Real Long term commodity and employment data. Vanity sanity and reality of mining and investment

The global economic climate and impact on SA Mining during a downward phase in the commodity cycle. World Economy Real Long term commodity and employment data. Vanity sanity and reality of mining and investment

Wealth Inequality in the United States since 1913

Wealth Inequality in the United States since 1913 Emmanuel Saez (UC Berkeley) Gabriel Zucman (LSE) JRCPPF 4 th Annual Conference 19 February 2015 Is rising inequality in the United States only a labor

Wealth Inequality in the United States since 1913 Emmanuel Saez (UC Berkeley) Gabriel Zucman (LSE) JRCPPF 4 th Annual Conference 19 February 2015 Is rising inequality in the United States only a labor

An American Profile: The United States and Its People

An American Profile: The United States and Its People 1 153641_EM_AmPro.indd 1 12/16/8 11:1:32 PM An American Profile: The United States and Its People 3 Table 1 Population, Percentage Change, and Racial

An American Profile: The United States and Its People 1 153641_EM_AmPro.indd 1 12/16/8 11:1:32 PM An American Profile: The United States and Its People 3 Table 1 Population, Percentage Change, and Racial

US imports from emerging economies have grown rapidly

US imports from emerging economies have grown rapidly Ratio to GDP (current dollars) 0.07 US merchandise imports, 1978 2008 0.06 0.05 0.04 0.03 0.02 Industrial Non-OPEC other 0.01 0 OPEC = Organization

US imports from emerging economies have grown rapidly Ratio to GDP (current dollars) 0.07 US merchandise imports, 1978 2008 0.06 0.05 0.04 0.03 0.02 Industrial Non-OPEC other 0.01 0 OPEC = Organization

Iowa s Ag Economic Outlook in the

Iowa s Ag Economic Outlook in the Current Global Context Steve Elmore Chief Economist September 17 th, 2018 Iowa Bankers Association Des Moines, IA This presentation contains forward-looking statements

Iowa s Ag Economic Outlook in the Current Global Context Steve Elmore Chief Economist September 17 th, 2018 Iowa Bankers Association Des Moines, IA This presentation contains forward-looking statements

A comparative study of Australian agricultural household financial positions

A comparative study of Australian agricultural household financial positions Will Chancellor & Shiji Zhao Australian Bureau of Agricultural and Resource Economics and Sciences Disclaimer: This presentation

A comparative study of Australian agricultural household financial positions Will Chancellor & Shiji Zhao Australian Bureau of Agricultural and Resource Economics and Sciences Disclaimer: This presentation

FAPRI agricultural commodity outlook

FAPRI agricultural commodity outlook By William H. Meyers Howard Cowden Professor of Agricultural and Applied Economics FAPRI at MU UN DESA Expert Group Meeting on the World Economy 21 October 2013 New

FAPRI agricultural commodity outlook By William H. Meyers Howard Cowden Professor of Agricultural and Applied Economics FAPRI at MU UN DESA Expert Group Meeting on the World Economy 21 October 2013 New

FINANCIAL ANALYSIS. Stoby

FINANCIAL ANALYSIS Stoby INVESTMENTS AND FINANCING Investments planned over the period : Investments 2018 2019 2020 2021 Intangible assets Company creation 1 500 Web platform development 8 290 Accounting

FINANCIAL ANALYSIS Stoby INVESTMENTS AND FINANCING Investments planned over the period : Investments 2018 2019 2020 2021 Intangible assets Company creation 1 500 Web platform development 8 290 Accounting

THE NEW JERSEY EQUINE INDUSTRY Economic Impact

THE NEW JERSEY EQUINE INDUSTRY 2007 Economic Impact The Rutgers Published Equine by Science Rutgers Center Equine Science Center New Jersey Equine Industry, 2007 Introduction There is a reason the state

THE NEW JERSEY EQUINE INDUSTRY 2007 Economic Impact The Rutgers Published Equine by Science Rutgers Center Equine Science Center New Jersey Equine Industry, 2007 Introduction There is a reason the state

How to Explain Car Rental to Banks and Investors

How to Explain Car Rental to Banks and Investors Scott White Senior Managing Director, Head of Investment Banking C.L. King & Associates March 8-9, 2011 Las Vegas Hilton 1 My Background 18 Years Advising

How to Explain Car Rental to Banks and Investors Scott White Senior Managing Director, Head of Investment Banking C.L. King & Associates March 8-9, 2011 Las Vegas Hilton 1 My Background 18 Years Advising

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Nevada County Population Projections 2015 to 2034

Nevada County Population Projections 2015 to 2034 Prepared By: Jeff Hardcastle, AICP Nevada State Demographer Nevada Department of Taxation Reno Office: 4600 Kietzke Lane, Building L Suite 235 Reno, NV

Nevada County Population Projections 2015 to 2034 Prepared By: Jeff Hardcastle, AICP Nevada State Demographer Nevada Department of Taxation Reno Office: 4600 Kietzke Lane, Building L Suite 235 Reno, NV

The Economy: A View from the (Atlanta) Fed (Staff)

Fed (Staff)") The Economy: A View from the (Atlanta) Fed (Staff) 2018 Alabama Economic Outlook Montgomery, AL January 11, 2018 2 The new supply-side economics? In their discussion of monetary policy, participants saw

The Economy: A View from the (Atlanta) Fed (Staff) 2018 Alabama Economic Outlook Montgomery, AL January 11, 2018 2 The new supply-side economics? In their discussion of monetary policy, participants saw

Economic Outlook for Canada: Economy Confronting Capacity Limits

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

How Much Wind Is in the Sails?

How Much Wind Is in the Sails? Erie Chamber of Commerce Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations September 20, 2017 Real GDP Growth

How Much Wind Is in the Sails? Erie Chamber of Commerce Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations September 20, 2017 Real GDP Growth

Livestock, Poultry, and Dairy: Situation and Outlook

Livestock, Poultry, and Dairy: Situation and Outlook AAEA Annual Meeting Extension Track August 14, 2012 James G. Robb Director james.robb@lmic.info 29 land Grant Universities: USDA Members: ERS APHIS

Livestock, Poultry, and Dairy: Situation and Outlook AAEA Annual Meeting Extension Track August 14, 2012 James G. Robb Director james.robb@lmic.info 29 land Grant Universities: USDA Members: ERS APHIS

Simply Put, Just too Much! Copyright AgResource Company. All All Rights Reserved.

Simply Put, Just too Much! Ag Market Driers for 2014? World Food inflation to rise 3.7% in 2014 (s. 2.9% in 2013) drien primarily by gains in liestock/dairy prices. Total 2014 world meat production down.8%.

Simply Put, Just too Much! Ag Market Driers for 2014? World Food inflation to rise 3.7% in 2014 (s. 2.9% in 2013) drien primarily by gains in liestock/dairy prices. Total 2014 world meat production down.8%.

Photo courtesy of Judy Jacobson, Watford City. Cattle Situation and Outlook Ag Lenders Conference

Photo courtesy of Judy Jacobson, Watford City Cattle Situation and Outlook Ag Lenders Conference Tim Petry Livestock Economist www.ndsu.edu/livestockeconomics Oct. 31, 2016 AGL16-Outlook 10-31-2016 TO

Photo courtesy of Judy Jacobson, Watford City Cattle Situation and Outlook Ag Lenders Conference Tim Petry Livestock Economist www.ndsu.edu/livestockeconomics Oct. 31, 2016 AGL16-Outlook 10-31-2016 TO

Dairy Outlook and Issues Facing The Dairy Industry

Dairy Outlook and Issues Facing The Dairy Industry Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences April 23, 2015 brownsc@missouri.edu http://amap.missouri.edu 2014

Dairy Outlook and Issues Facing The Dairy Industry Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences April 23, 2015 brownsc@missouri.edu http://amap.missouri.edu 2014

Livestock Market Trends

Livestock Market Trends Farm$mart Agricultural Conference January 18, 2014 John Bancroft Market Strategies Program Lead john.bancroft@ontario.ca 519-271-6974 Today s Discussion 2014 FCC Market Drivers

Livestock Market Trends Farm$mart Agricultural Conference January 18, 2014 John Bancroft Market Strategies Program Lead john.bancroft@ontario.ca 519-271-6974 Today s Discussion 2014 FCC Market Drivers

Real Estate and Economic Outlook

Real Estate and Economic Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation at Inforum Outlook Conference University of Maryland College Park, MD December 12, 2013

Real Estate and Economic Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation at Inforum Outlook Conference University of Maryland College Park, MD December 12, 2013

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six years of steady growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half Full

The Economic Outlook Economic Policy Division Glass Half Full Six years of steady growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half Full

Otero County Demographic Profile

Otero County Demographic Profile Prepared by Southern Colorado Economic Development District 1104 North Main Street Pueblo, CO 81003 719-545-8680 Table of Contents Otero County... 3 Transportation... 4

Otero County Demographic Profile Prepared by Southern Colorado Economic Development District 1104 North Main Street Pueblo, CO 81003 719-545-8680 Table of Contents Otero County... 3 Transportation... 4

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder Member FDIC VectraBank.com Economic Outlook 2015 Richard

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder Member FDIC VectraBank.com Economic Outlook 2015 Richard

Custer County Demographic Profile

Custer County Demographic Profile Prepared by Southern Colorado Economic Development District 1104 North Main Street Pueblo, CO 81003 719-545-8680 Table of Contents Custer County... 3 Transportation...

Custer County Demographic Profile Prepared by Southern Colorado Economic Development District 1104 North Main Street Pueblo, CO 81003 719-545-8680 Table of Contents Custer County... 3 Transportation...

National and Regional Economic Outlook. Central Southern CAA Conference

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

RBC Economics Financial Update Dawn Desjardins

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

1. HighQuest Partners + Soyatech

Key Fundamentals Driving Investor Interest in Global Agriculture Philippe de Lapérouse Managing Director HighQuest Partners LLC Les Perspectives 2014 Le 8 avril 2014 Boucherville, Québec 1. HighQuest Partners

Key Fundamentals Driving Investor Interest in Global Agriculture Philippe de Lapérouse Managing Director HighQuest Partners LLC Les Perspectives 2014 Le 8 avril 2014 Boucherville, Québec 1. HighQuest Partners

Grains, Beans and Farmland: The True Diversifiers

Grains, Beans and Farmland: The True Diversifiers Sumit Roy, Moderator Managing Editor HardAssetsInvestor.com Greyson Colvin, Panelist Managing Partner Colvin & Co Michael Cox, Panelist Managing Partner,

Grains, Beans and Farmland: The True Diversifiers Sumit Roy, Moderator Managing Editor HardAssetsInvestor.com Greyson Colvin, Panelist Managing Partner Colvin & Co Michael Cox, Panelist Managing Partner,

Not For Sale. An American Profile: The United States and Its People

An American Profile: The United States and Its People Not For Sale 1 759_EM_AmPro_ptg1.indd 1 Not For Sale 759_EM_AmPro_ptg1.indd 2 An American Profile: The United States and Its People 3 Table 1 Population,

An American Profile: The United States and Its People Not For Sale 1 759_EM_AmPro_ptg1.indd 1 Not For Sale 759_EM_AmPro_ptg1.indd 2 An American Profile: The United States and Its People 3 Table 1 Population,