SFSA Business Outlook Raymond Monroe

|

|

|

- Mae Riley

- 5 years ago

- Views:

Transcription

1 SFSA Business Outlook 2010 Raymond Monroe

2

3

4 Agriculture Workers

5 Population

6 Industrial Workers

7 Service Workers

8

9

10

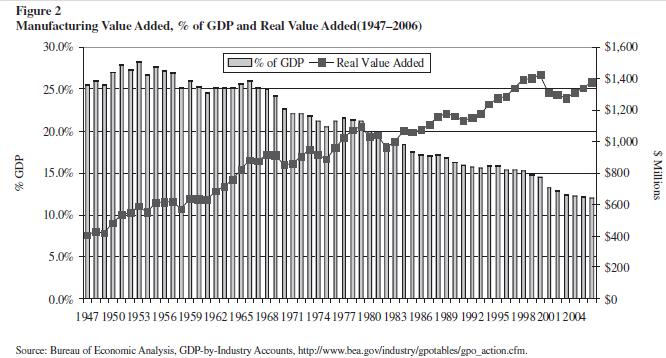

11 U.S. Manufacturing 2008 manufacturing was $1.4 trillion 9 th largest economy/ size of Canada 70% R&D $147 billion 90% of patents $1.00 produces $1.37 of activity 3.4%/year productivity for 20 yrs compared to 2.2%/yr for others 22% higher wages than services manufacturing framework final_embargoed.pdf

12

13

14

15

16

17

18 Steel Casting Production in the U.S. million tons Million Tons U.S Year

19 Steel Foundries in North America

20 Production and Capacity production capacity 2000 thousand tons

21 United States Steel Production 160,000, ,000, ,000, ,000,000 80,000,000 60,000,000 40,000,000 20,000, Tons 2004 R^2= 0.72 Slope = 0.02

22 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan Carbon & Low Alloy Casting Market Trends Shipments steel shipments Percent Change %

23 Cast Shipments R^2 =0.51 Slope= '55 '75 '

24 Interest Rates %change Prime Rate R^2=0.33 Slope = 0.37 %change Moody s aaa R^2=0.002

25 Price Index

26 Ratio of nondurable good to GDP implicit price deflator

27 Price of Oil

28

29 Nondefense Capital Goods New orders Air %change R^2=0.32 Slope = 0.37

30 Profits v production steel foundries with assets $2 10MM Gross Profit Operating Profit Profit before Taxes

31 Return on Assets steel foundries with assets $2 10MM

32 Profits v. ROA steel foundries with assets $2 10MM Gross Profits Operating Profits Profit before taxes

33 Return on Net Worth steel foundries with assets $2 10MM

34 Current Ratio Steel Foundries $2-10 Million Assets Total Current Assets / Total Current Liabilities Target = Current Ratio Current-Median Upper Current-Median Current-Median Lower Year

35 Quick Ratio Steel Foundries $2-10 Million Assets Cash & Equivalents & Trade Receivable (Net) / Total Current Liabilities Target = Quick Ratio 1.5 Quick-Median Upper Quick Median 1.0 Quick Median Lower Year

36 Fixed/Worth Steel Foundries $2-10 Million Assets Net Fixed Assets / Tangible Net Worth Target = Fixed/Worth Fixed / Worth-Median Upper Fixed / Worth-Median 1.0 Fixed / Worth-Median Lower Year

37 Fixed Assets as a function of Net Worth steel foundries with assets $2 10MM

38 The laws of thermodynamics in very basic lay person language are thus: 1. You cannot win. 2. You cannot break even. 3. You must play the game and lose badly every time.

39 Thanks! Questions? Raymond Monroe

40 Return on Net Worth steel foundries with sales $10 25MM median upper median median lower

41 Return on Assets steel foundries with sales $10 25MM upper median median lower median

42 Profits and ROA steel foundries with sales $10 25MM gross profit operating profit profit before taxes

43 Profits v production steel foundries with sales $10 25MM gross profit operating profit profit before taxes

44 Other factors and ROA steel foundries with sales $10 25MM ebit/interest return on net worth sales/net fixed assets

45 25.0 EBIT/Interest steel foundries with assets $2 10MM

46 Correlation of production and finances steel foundries with assets $2 10MM net worth Operating Profit

47 Correlation of production and finances steel foundries with sales $10 25 MM total current assets operating profit

48 Trade Receivables Turnover Steel Foundries $2-10 Million Assets Net Sales / Trade Receivables (Net) Target = At or Slightly Above Industry Average Trade Receivables Turnover Trade Receivables Turnover - Median Upper Trade Receivables Turnover - Median Trade Receivables Turnover - Median Lower Year

49 Days' Receivable Steel Foundries $2-10 Million Assets 365 / Trade Receivables Turnover Target = At or Lower Than Industry Average Days' Receivable Days Receivable - Median Upper Days Receivable - Median Days Receivable - Median Lower Year

50 27.0 Inventory Turnover Steel Foundries $2-10 Million Assets Cost of Sales / Inventory Target = At or Slightly Above Industry Average 22.0 Inventory Turnover Inventory Turnover -Median Upper Inventory Turnover -Median Inventory Turnover -Median Lower Year

51 Days' Inventory Steel Foundries $2-10 Million Assets 365 / Inventory Turnover Target = At or Slightly Below Industry Average Days' Inventory Days' Inventory - Median Upper Days' Inventory - Median Days' Inventory - Median Lower Year

52 Trade Payables Turnover Steel Foundries $2-10 Million Assets Cost of Sales / Trade Payables Target = Industry Average Trade Payables Turnover Trade Payables Turnover-Median Upper Trade Payables Turnover-Median Trade Payables Turnover-Median Lower Year

53 Days' Payable Steel Foundries $2-10 Million Assets 365 / Trade Payables Turnover Target = Industry Average Days Payable Days' Payable-Median Upper Days' Payable-Median 30.0 Days' Payable-Median Lower Year

54 Working Capital Turnover Steel Foundries $2-10 Million Assets Net Sales / Net Working Capital Target = At or Above Industry Average Working Capital Turnover Working Capital Turnover -Median Upper Working Capital Turnover -Median Working Capital Turnover -Median Lower Year

55 Return on Net Worth Steel Foundries $2-10 Million Assets Profit Before Taxes / Tangible Net Worth Target = Industry Average Return on Net Worth 40.0 Return on Net Worth-Median Upper Return on Net Worth-Median Return on Net Worth-Median Lower Year

56 Return on Assets Steel Foundries $2-10 Million Assets Profit Before Taxes / Total Assets Target = Industry Average Return on Assets Return on Assets- Median Upper Return on Assets- Median Return on Assets- Median Lower Year

57 Asset Turnover Steel Foundries $2-10 Million Assets Sales / Total Assets Target = Industry Average Asset Turnover Sales/Total Assets-Median Upper Sales/Total Assets-Median 1.5 Sales/Total Assets-Median Lower Year

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Real Estate and Economic Outlook

Real Estate and Economic Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation at Inforum Outlook Conference University of Maryland College Park, MD December 12, 2013

Real Estate and Economic Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation at Inforum Outlook Conference University of Maryland College Park, MD December 12, 2013

More of the Same; Or now for Something Completely Different?

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

The US Economic Outlook

IHS ECONOMICS US Outlook The US Economic Outlook November 2014 ihs.com Rafael Amiel, Director latin America Economics +1 215 789 7405, rafael.amiel.ihs.com 2014 IHS The US economy is gaining momentum Growth

IHS ECONOMICS US Outlook The US Economic Outlook November 2014 ihs.com Rafael Amiel, Director latin America Economics +1 215 789 7405, rafael.amiel.ihs.com 2014 IHS The US economy is gaining momentum Growth

Farm Sector Income & Finances 2016 Outlook. By Ryan Kuhns and Kevin Patrick March 16, 2016

Farm Sector Income & Finances 2016 Outlook By Ryan Kuhns and Kevin Patrick March 16, 2016 Background The Economic Research Service forecasts the farm sector s income statement and balance sheet Last released

Farm Sector Income & Finances 2016 Outlook By Ryan Kuhns and Kevin Patrick March 16, 2016 Background The Economic Research Service forecasts the farm sector s income statement and balance sheet Last released

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies Chief Economist, PAGI Group, JLL (Port, Airport & Global Infrastructure) Agenda Where are we in the cycle? What are the barriers

The Changing Global Economy Impacts on Seaports and Trade Dr. Walter Kemmsies Chief Economist, PAGI Group, JLL (Port, Airport & Global Infrastructure) Agenda Where are we in the cycle? What are the barriers

State of American Trucking

State of American Trucking October 11, 2018 Rod Suarez Economic Analyst American Trucking Associations rsuarez@trucking.org Business Cycles U.S. Expansions Duration October 1949 - July 1953 May 1954 -

State of American Trucking October 11, 2018 Rod Suarez Economic Analyst American Trucking Associations rsuarez@trucking.org Business Cycles U.S. Expansions Duration October 1949 - July 1953 May 1954 -

The U.S. Economic Outlook

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

A comment on recent events, and...

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

Agricultural Outlook: Rebalancing U.S. Agriculture

Agricultural Outlook: Rebalancing U.S. Agriculture Michael J. Swanson Ph.D. Agricultural Economist January 2018 2018 Wells Fargo Bank, N.A. All rights reserved. For public use. The U.S. Ag Sector renormalizes!

Agricultural Outlook: Rebalancing U.S. Agriculture Michael J. Swanson Ph.D. Agricultural Economist January 2018 2018 Wells Fargo Bank, N.A. All rights reserved. For public use. The U.S. Ag Sector renormalizes!

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six years of steady growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half Full

The Economic Outlook Economic Policy Division Glass Half Full Six years of steady growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half Full

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Real gross domestic growth

Real gross domestic growth United States, 2000 prices Compound annual growth rate 10 5 0-5 -10 81 83 85 87 89 91 93 95 97 99 01 03 05 07 Sources: BEA, Global Insight. Consumer sentiment University of Michigan,

Real gross domestic growth United States, 2000 prices Compound annual growth rate 10 5 0-5 -10 81 83 85 87 89 91 93 95 97 99 01 03 05 07 Sources: BEA, Global Insight. Consumer sentiment University of Michigan,

Colorado Economic Update

Colorado Economic Update Steamboat Economic Summit Place cover image here Brian Lewandowski Associate Director, Business Research Division October 21, 2016 Recession 8 Months Recession 18 Months Real GDP

Colorado Economic Update Steamboat Economic Summit Place cover image here Brian Lewandowski Associate Director, Business Research Division October 21, 2016 Recession 8 Months Recession 18 Months Real GDP

Big Changes, Unknown Impacts

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Indian Economy in Graphs. Arvind Panagariya Columbia University

Indian Economy in Graphs Growth in GDP and Per-capita GDP 9 8.3 8 7 6.7 6 5.8 5 4 3 2 4.1 2.2 3.2 4.6 2.2 3.7 1 0.8 0 Phase I (1951-64) Phase II (1965-81) Phase III (1981-88) Phase IV (1988-03) Phase V

Indian Economy in Graphs Growth in GDP and Per-capita GDP 9 8.3 8 7 6.7 6 5.8 5 4 3 2 4.1 2.2 3.2 4.6 2.2 3.7 1 0.8 0 Phase I (1951-64) Phase II (1965-81) Phase III (1981-88) Phase IV (1988-03) Phase V

BC Pension Forum. Economic Outlook. Presented by: Ben Homsy, CFA Portfolio Manager

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

Europe June Craig Menear. Chairman, CEO & President. Diane Dayhoff. Vice President, Investor Relations

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

Q PRESENTATION 18 OCTOBER 2018

Q3 2018 PRESENTATION 18 OCTOBER 2018 Group Highlights Q3 2018 Very strong growth in revenue and operating profit outside of Denmark. In Denmark, acceptance of self-cleaning in September allows Atea to

Q3 2018 PRESENTATION 18 OCTOBER 2018 Group Highlights Q3 2018 Very strong growth in revenue and operating profit outside of Denmark. In Denmark, acceptance of self-cleaning in September allows Atea to

The Global Economy: Sustaining Momentum

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

Northwest Economic Research Center College of Urban and Public Affairs Forecast Breakfast Economic Outlook

Northwest Economic Research Center College of Urban and Public Affairs 2019 Forecast Breakfast Economic Outlook 1/10/2019 2 U.S. ECONOMY 1/10/2019 3 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Northwest Economic Research Center College of Urban and Public Affairs 2019 Forecast Breakfast Economic Outlook 1/10/2019 2 U.S. ECONOMY 1/10/2019 3 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Shifting International Trade Routes A National Economic Outlook. February 1, 2011

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

India: Can the Tiger Economy Continue to Run?

India: Can the Tiger Economy Continue to Run? India s GDP is on the rise US$ trillions Nominal GDP (left axis) GDP growth (right axis) 3.0 2.5 2.0 1.5 1.0 0.5 0.0 1990 1992 1994 1996 1998 2000 2002 2004

India: Can the Tiger Economy Continue to Run? India s GDP is on the rise US$ trillions Nominal GDP (left axis) GDP growth (right axis) 3.0 2.5 2.0 1.5 1.0 0.5 0.0 1990 1992 1994 1996 1998 2000 2002 2004

Global Outlook for Agriculture Trend versus Cycle

Global Outlook for Agriculture Trend versus Cycle Michael Swanson Ph.D. Wells Fargo October 2017 Everything is connected we just don t see how. Connection corollary: Nothing natural moves in a straight

Global Outlook for Agriculture Trend versus Cycle Michael Swanson Ph.D. Wells Fargo October 2017 Everything is connected we just don t see how. Connection corollary: Nothing natural moves in a straight

Agriculture and the Economy: A View from the Chicago Fed

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States?

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Lawrence J. Lau 刘遵义. CSIS Forum Washington, D.C., 22nd May 2013

U.S.-China Economic Relations in the Next Ten Years: Towards Deeper Engagement and Mutual Benefit Lawrence J. Lau 刘遵义 Ralph and Claire Landau Professor of Economics, The Chinese Univ. of Hong Kong and

U.S.-China Economic Relations in the Next Ten Years: Towards Deeper Engagement and Mutual Benefit Lawrence J. Lau 刘遵义 Ralph and Claire Landau Professor of Economics, The Chinese Univ. of Hong Kong and

Fact Sheet for Q3 and January-September 2012 October 24, 2012

Fact Sheet for Q3 and January-September 2012 October 24, 2012 Contents Daimler Group Stock Market Information 3 Earnings and Financial Situation 4-13 Information for Divisions Mercedes-Benz Cars 14-17

Fact Sheet for Q3 and January-September 2012 October 24, 2012 Contents Daimler Group Stock Market Information 3 Earnings and Financial Situation 4-13 Information for Divisions Mercedes-Benz Cars 14-17

Figure 1: Canadian Real Exports and Imports 1981Q1 2009Q2, Quarterly

Figure 1: Canadian Real Exports and Imports 1981Q1 2009Q2, Quarterly Exports and Imports (Millions of 2002 $) 100000 300000 500000 1981 1985 1989 1993 1997 2001 2005 2009 Exports Imports Exports and Imports

Figure 1: Canadian Real Exports and Imports 1981Q1 2009Q2, Quarterly Exports and Imports (Millions of 2002 $) 100000 300000 500000 1981 1985 1989 1993 1997 2001 2005 2009 Exports Imports Exports and Imports

How Much Wind Is in the Sails?

How Much Wind Is in the Sails? Erie Chamber of Commerce Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations September 20, 2017 Real GDP Growth

How Much Wind Is in the Sails? Erie Chamber of Commerce Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations September 20, 2017 Real GDP Growth

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

MBA Economic and Mortgage Finance Outlook

MBA Economic and Mortgage Finance Outlook MBA of Alabama Annual Conference June 7, 2017 Presented by Lynn Fisher Mortgage Bankers Association 1 Summary of the MBA Outlook 2016 2017 2018 2019 GDP Growth

MBA Economic and Mortgage Finance Outlook MBA of Alabama Annual Conference June 7, 2017 Presented by Lynn Fisher Mortgage Bankers Association 1 Summary of the MBA Outlook 2016 2017 2018 2019 GDP Growth

Cattle Market Outlook & Important Profit Factors for Cattle Producers

Cattle Market Outlook & Important Profit Factors for Cattle Producers Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences brownsc@missouri.edu http://amap.missouri.edu $

Cattle Market Outlook & Important Profit Factors for Cattle Producers Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences brownsc@missouri.edu http://amap.missouri.edu $

Date: Place: Term: Your ref. order No.:

Page 1 of 7 Date: Place: Term: Your ref. order No.: ******** Vilnius UAB XXXXXXXXXXX UAB XXXXXXXXXXX Algirdo G. xxxxx Vilniaus M., Vilniaus M. Sav. LT-03216 Lithuania Tel.: Fax.: Email: Webpage: +370 5

Page 1 of 7 Date: Place: Term: Your ref. order No.: ******** Vilnius UAB XXXXXXXXXXX UAB XXXXXXXXXXX Algirdo G. xxxxx Vilniaus M., Vilniaus M. Sav. LT-03216 Lithuania Tel.: Fax.: Email: Webpage: +370 5

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

Economic Outlook. Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project

Economic Outlook Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project League of California Cities Monterey, CA December 3, 2014 Economic Update economic

Economic Outlook Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project League of California Cities Monterey, CA December 3, 2014 Economic Update economic

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Update.

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Update February 26, 2013 The Worst Recession Since the Great Depression 0% Loss from Peak

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Update February 26, 2013 The Worst Recession Since the Great Depression 0% Loss from Peak

PROVINCE OF SASKATCHEWAN INVESTOR PRESENTATION

PROVINCE OF SASKATCHEWAN INVESTOR PRESENTATION May 2018 THE SASKATCHEWAN DIFFERENCE Economic Stability Diversified economy balances cyclicality of resources Growing population Majority government with

PROVINCE OF SASKATCHEWAN INVESTOR PRESENTATION May 2018 THE SASKATCHEWAN DIFFERENCE Economic Stability Diversified economy balances cyclicality of resources Growing population Majority government with

Presentation half-year results 2012

Presentation half-year results 2012 Okura Hotel, Amsterdam 26 July 2012 René J. Takens, CEO Hielke H. Sybesma, CFO Jeroen M. Snijders Blok, COO Agenda 1. Accell Group in H1 2012 2. Accell Group share 3.

Presentation half-year results 2012 Okura Hotel, Amsterdam 26 July 2012 René J. Takens, CEO Hielke H. Sybesma, CFO Jeroen M. Snijders Blok, COO Agenda 1. Accell Group in H1 2012 2. Accell Group share 3.

From Recession to Recovery

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

2019 Economic Outlook: Will the Recovery Ever End?

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee The U.S. economy has now enjoyed 7 years of economic growth since the Great Recession Real GDP grew by 1.2% in

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee The U.S. economy has now enjoyed 7 years of economic growth since the Great Recession Real GDP grew by 1.2% in

The Wisconsin and Minnesota Economies: What can we learn from each other? Noah Williams

The Economies: What can we learn from each other? Noah University of Wisconsin - Madison Future Wisconsin Summit 2016 Economies Location, size, demographics, and history make Wisconsin and Minnesota natural

The Economies: What can we learn from each other? Noah University of Wisconsin - Madison Future Wisconsin Summit 2016 Economies Location, size, demographics, and history make Wisconsin and Minnesota natural

MAINTAINING MOMENTUM:

MAINTAINING MOMENTUM: 2018 National Economic Update September 12, 2018 noun mo men tum \ mō-ˈmen-təm, mə- \ 1 b : the strength or force that allows something to continue or to grow stronger or faster as

MAINTAINING MOMENTUM: 2018 National Economic Update September 12, 2018 noun mo men tum \ mō-ˈmen-təm, mə- \ 1 b : the strength or force that allows something to continue or to grow stronger or faster as

Source: Statistics Canada. World Trade Analyzer, Source: Statistics Canada. World Trade Analyzer,

Table 1 Mexican Merchandise Exports Average 1982 1983 1984 1985 1986 1982-86 Total 22610 25497 26996 25890 15159 23230 of which: US 11965 15915 16636 16630 10138 14257 Canada 657 659 683 664 269 586 ROW

Table 1 Mexican Merchandise Exports Average 1982 1983 1984 1985 1986 1982-86 Total 22610 25497 26996 25890 15159 23230 of which: US 11965 15915 16636 16630 10138 14257 Canada 657 659 683 664 269 586 ROW

10 County Conference. Richard Wobbekind. Executive Director Business Research Division & Senior Associate Dean Leeds School of Business

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

Beef Outlook. Regional Dealer Event. February 9, Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences

Beef Outlook Regional Dealer Event February 9, 2018 Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences brownsc@missouri.edu http://amap.missouri.edu $ Per Cwt. MED. & LRG.

Beef Outlook Regional Dealer Event February 9, 2018 Dr. Scott Brown Agricultural Markets and Policy Division of Applied Social Sciences brownsc@missouri.edu http://amap.missouri.edu $ Per Cwt. MED. & LRG.

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Trends. September 10, 2013

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Presentation first-half results 2010

Presentation first-half results 2010 Okura Hotel, Amsterdam 23 July 2010 René J. Takens, CEO Hielke H. Sybesma, CFO Jeroen M. Snijders Blok, COO Agenda 1. Accell Group in H1 2010 2. Segments and countries

Presentation first-half results 2010 Okura Hotel, Amsterdam 23 July 2010 René J. Takens, CEO Hielke H. Sybesma, CFO Jeroen M. Snijders Blok, COO Agenda 1. Accell Group in H1 2010 2. Segments and countries

Crefo No Registration No. J40/13885/2013 Tax No. RO Status Active 275 S

Page 1 from 11 Company identification E-P RAIL SRL Telephone +40 31 4229315 +40 723 393243 B-dul Lacul Tei 31-33 E-mail office@e-prail.ro 20796 Bucuresti Sector 2 WEB www.e-prail.ro Romania Crefo No. 893269

Page 1 from 11 Company identification E-P RAIL SRL Telephone +40 31 4229315 +40 723 393243 B-dul Lacul Tei 31-33 E-mail office@e-prail.ro 20796 Bucuresti Sector 2 WEB www.e-prail.ro Romania Crefo No. 893269

Business Outlook Report 2017

Business Outlook Report 217 Adam Davey Market Intelligence Manager Sponsored By: 7.3.217 Agenda 1 Oil and Gas Markets 2 Supply Chain Outlook - Revenues - Share Price 3 Upstream Outlook - Capex - Opex -

Business Outlook Report 217 Adam Davey Market Intelligence Manager Sponsored By: 7.3.217 Agenda 1 Oil and Gas Markets 2 Supply Chain Outlook - Revenues - Share Price 3 Upstream Outlook - Capex - Opex -

Outlook for airline markets and industry performance

Outlook for airline markets and industry performance June 2016 Brian Pearce Chief Economist International Air Transport Association % change over previous year Confidence index. 50 = no change The already

Outlook for airline markets and industry performance June 2016 Brian Pearce Chief Economist International Air Transport Association % change over previous year Confidence index. 50 = no change The already

colorado.edu/business/brd

colorado.edu/business/brd Big Changes, Unknown Impacts Southwest Business Forum Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January

colorado.edu/business/brd Big Changes, Unknown Impacts Southwest Business Forum Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks. Business Research Division Leeds School of Business

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks Presented by the Business Research Division Leeds School of Business University of Colorado at Boulder U.S. Economic

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks Presented by the Business Research Division Leeds School of Business University of Colorado at Boulder U.S. Economic

North American Forging Shipment Forecast (Using FIA bookings information through December 2013)

") North American Forging Shipment Forecast 2014-2018 (Using FIA bookings information through December 2013) Percent Change Year Ago Best leading indicator combination for impression die bookings used to

North American Forging Shipment Forecast 2014-2018 (Using FIA bookings information through December 2013) Percent Change Year Ago Best leading indicator combination for impression die bookings used to

Issues Driving the Outlook for Specialty Crops December 3, 2012

Issues Driving the Outlook for Specialty Crops December 3, 2012 Daniel A. Sumner University of California Agricultural Issues Center, and UC Davis Department of Agricultural and Resource Economics Core

Issues Driving the Outlook for Specialty Crops December 3, 2012 Daniel A. Sumner University of California Agricultural Issues Center, and UC Davis Department of Agricultural and Resource Economics Core

National and Regional Economic Outlook. Central Southern CAA Conference

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

Economic Overview. Melissa K. Peralta Senior Economist April 27, 2017

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Economic performance of the airline industry end-2017 update

Economic performance of the airline industry end-2017 update December 2017 Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 City-pair connections

Economic performance of the airline industry end-2017 update December 2017 Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 City-pair connections

President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H. Parker Willis Lecture in Political Economics

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

ANNUAL RESULTS PRESENTATION. 20 March, 2014 Hong Kong

ANNUAL RESULTS PRESENTATION 20 March, 2014 Hong Kong Content Ⅰ Ⅱ Financial Highlights Business Performance Ⅲ Trend and Objectives Ⅳ Outlook and Perspectives Financial Highlights Total Assets (RMB billion)

ANNUAL RESULTS PRESENTATION 20 March, 2014 Hong Kong Content Ⅰ Ⅱ Financial Highlights Business Performance Ⅲ Trend and Objectives Ⅳ Outlook and Perspectives Financial Highlights Total Assets (RMB billion)

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch June 2016

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch June 2016 Image from http://peoplesguidetohouston.wordpress.com/category/uncategorized/

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch June 2016 Image from http://peoplesguidetohouston.wordpress.com/category/uncategorized/

Economy On The Rebound

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Economic and Real Estate Outlook

Economic and Real Estate Outlook By Lawrence Yun, Ph.D. Chief Economist, National Association of REALTORS Presentation at Charlottesville Area Association of REALTORS October 13, 2016 1990 1991 1992 1993

Economic and Real Estate Outlook By Lawrence Yun, Ph.D. Chief Economist, National Association of REALTORS Presentation at Charlottesville Area Association of REALTORS October 13, 2016 1990 1991 1992 1993

Airline industry outlook 2019

Airline industry outlook 2019 Brian Pearce Chief Economist 12 December 2018 Million barrels a day US$ per barrel Are the markets signalling recession ahead? 60 55 Business confidence (left scale) FTSE

Airline industry outlook 2019 Brian Pearce Chief Economist 12 December 2018 Million barrels a day US$ per barrel Are the markets signalling recession ahead? 60 55 Business confidence (left scale) FTSE

Presentation First-half results 2007

Presentation First-half results 2007 Okura Hotel, Amsterdam 20 July 2007 René J. Takens, CEO Hielke H. Sybesma, CFO Jeroen M. Snijders Blok, COO 1 Agenda Summary Development segments and countries in first

Presentation First-half results 2007 Okura Hotel, Amsterdam 20 July 2007 René J. Takens, CEO Hielke H. Sybesma, CFO Jeroen M. Snijders Blok, COO 1 Agenda Summary Development segments and countries in first

OPENING KEYNOTE SPEAKER

NIT LEAGUE TRANSPORTATION SUMMIT OPENING KEYNOTE SPEAKER Derek J. Leathers President and CEO Werner Enterprises Founded in 1956; grown from one-truck operation to a $2 billion company Among five largest

NIT LEAGUE TRANSPORTATION SUMMIT OPENING KEYNOTE SPEAKER Derek J. Leathers President and CEO Werner Enterprises Founded in 1956; grown from one-truck operation to a $2 billion company Among five largest

Canada s economy on track for a solid 2018 although policy uncertainty lingers

Canada s economy on track for a solid 2018 although policy uncertainty lingers Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com March 2018 Canada is facing a challenging

Canada s economy on track for a solid 2018 although policy uncertainty lingers Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com March 2018 Canada is facing a challenging

Products and Presence. First quarter 2010 Four Seasons Hotel, New York City

Products and Presence First quarter 2010 Four Seasons Hotel, New York City Vestas largest order ever Through this agreement, EDPR contracts from Vestas the wind turbine technology that optimises productivity

Products and Presence First quarter 2010 Four Seasons Hotel, New York City Vestas largest order ever Through this agreement, EDPR contracts from Vestas the wind turbine technology that optimises productivity

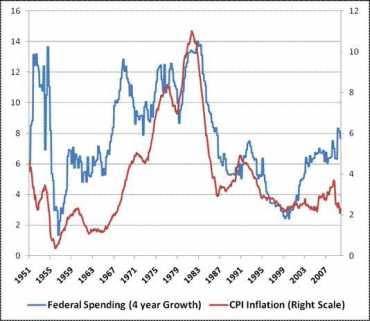

Composition of Federal Spending

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

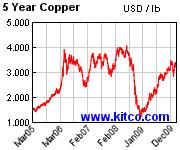

Index, nominal terms, 2010 = Energy. Agriculture Metals

Outline Broad commodity price trends Index, nominal terms, 2010 = 100 180 150 Energy 120 90 60 Agriculture Metals 30 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Source:

Outline Broad commodity price trends Index, nominal terms, 2010 = 100 180 150 Energy 120 90 60 Agriculture Metals 30 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Source:

Steel Market Outlook. AM/NS Calvert

Steel Market Outlook AM/NS Calvert Agenda Economic indicators Key steel consuming markets and forecasted demand Steel consumptions trends Global steel markets and raw materials Comments on trade 1 U.S.

Steel Market Outlook AM/NS Calvert Agenda Economic indicators Key steel consuming markets and forecasted demand Steel consumptions trends Global steel markets and raw materials Comments on trade 1 U.S.

Global economy maintaining solid growth momentum. Canada leading the pack

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch January 2017

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch January 2017 Image from http://peoplesguidetohouston.wordpress.com/category/uncategorized/

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch January 2017 Image from http://peoplesguidetohouston.wordpress.com/category/uncategorized/

Muhlenkamp & Company. Webinar December 1, Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Global growth forecasts Key countries/regions,

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

Outlook for the North American Softwood Lumber Industry

Outlook for the North American Softwood Lumber Industry North American Conference October 2017 David Fortin Director, Wood Products Copyright 2017 RISI, Inc. Proprietary Information Quick Bio Master s

Outlook for the North American Softwood Lumber Industry North American Conference October 2017 David Fortin Director, Wood Products Copyright 2017 RISI, Inc. Proprietary Information Quick Bio Master s

Not For Sale. An American Profile: The United States and Its People

An American Profile: The United States and Its People Not For Sale 1 759_EM_AmPro_ptg1.indd 1 Not For Sale 759_EM_AmPro_ptg1.indd 2 An American Profile: The United States and Its People 3 Table 1 Population,

An American Profile: The United States and Its People Not For Sale 1 759_EM_AmPro_ptg1.indd 1 Not For Sale 759_EM_AmPro_ptg1.indd 2 An American Profile: The United States and Its People 3 Table 1 Population,

Exhibit #MH-156. ELECTRIC OPERATIONS (MH10-2) PROJECTED OPERATING STATEMENT (In Millions of Dollars) For the year ended March 31 REVENUES

PROJECTED OPERATING STATEMENT (In Millions of Dollars) For the year ended March 31 REVENUES") PROJECTED OPERATING STATEMENT 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 REVENUES General Consumers at approved rates 1,194 1,223 1,235 1,254 1,265 1,279 1,296 1,307 1,320 1,336 additional * - 42

PROJECTED OPERATING STATEMENT 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 REVENUES General Consumers at approved rates 1,194 1,223 1,235 1,254 1,265 1,279 1,296 1,307 1,320 1,336 additional * - 42

Puget Sound Regional Forecast Chris Mefford Community Attributes

2015 Puget Sound Regional Forecast Chris Mefford Community Attributes 3 1,000s The Regional Economy has added jobs consistently for nearly 5 full years. In a few months, this will be the longest streak

2015 Puget Sound Regional Forecast Chris Mefford Community Attributes 3 1,000s The Regional Economy has added jobs consistently for nearly 5 full years. In a few months, this will be the longest streak

FINANCIAL ANALYSIS. Stoby

FINANCIAL ANALYSIS Stoby INVESTMENTS AND FINANCING Investments planned over the period : Investments 2018 2019 2020 2021 Intangible assets Company creation 1 500 Web platform development 8 290 Accounting

FINANCIAL ANALYSIS Stoby INVESTMENTS AND FINANCING Investments planned over the period : Investments 2018 2019 2020 2021 Intangible assets Company creation 1 500 Web platform development 8 290 Accounting

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

Your Texas Economy. Current through: Tuesday, Nov 20, 2018

Your Texas Economy Current through: Tuesday, Nov 20, 2018 Overview of Texas Economy The Texas economy is growing robustly in 2018 2018 job growth through October is 2.9 percent annualized compared to 2.1

Your Texas Economy Current through: Tuesday, Nov 20, 2018 Overview of Texas Economy The Texas economy is growing robustly in 2018 2018 job growth through October is 2.9 percent annualized compared to 2.1

Babson Capital/UNC Charlotte Economic Forecast. May 13, 2014

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Railroads and the Economy

Railroads and the Economy North East Association of Rail Shippers April 27, 2016 Railroads Help Keep Coal- Based Electricity A cynic is a man who, when he smells flowers, looks around for a coffin. -H.L.

Railroads and the Economy North East Association of Rail Shippers April 27, 2016 Railroads Help Keep Coal- Based Electricity A cynic is a man who, when he smells flowers, looks around for a coffin. -H.L.

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch February 2017

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch February 2017 Image from http://peoplesguidetohouston.wordpress.com/category/uncategorized/

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch February 2017 Image from http://peoplesguidetohouston.wordpress.com/category/uncategorized/

ABA Commercial Real Estate Lending Committee

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

THE MOST INFORMATIVE EVENT COVERING REAL ESTATE INVESTMENTS

THE MOST INFORMATIVE EVENT COVERING REAL ESTATE INVESTMENTS 2014 U.S. Economic, Capital Markets, and Retail Market Overview and Outlook Retail Trends 2014 U.S. Economic Overview and Outlook Total Employment

THE MOST INFORMATIVE EVENT COVERING REAL ESTATE INVESTMENTS 2014 U.S. Economic, Capital Markets, and Retail Market Overview and Outlook Retail Trends 2014 U.S. Economic Overview and Outlook Total Employment

32 nd Annual CanaData Construction Forecasts Conference

32 nd Annual CanaData Construction Forecasts Conference Economic Intelligence September 21 st, 2017 Toronto Peter Norman, VP & Chief Economist, Economic Consulting Our Company Structure at a Glance ARGUS

32 nd Annual CanaData Construction Forecasts Conference Economic Intelligence September 21 st, 2017 Toronto Peter Norman, VP & Chief Economist, Economic Consulting Our Company Structure at a Glance ARGUS

Annual Results 2002 Accell Group N.V. Amsterdam, 20 February 2003

Annual Results 2002 Accell Group N.V. Amsterdam, 20 February 2003 Agenda Summary results Important developments in 2002 Accell Group share Financials Sales & Marketing Outlook Summary results (x million)

Annual Results 2002 Accell Group N.V. Amsterdam, 20 February 2003 Agenda Summary results Important developments in 2002 Accell Group share Financials Sales & Marketing Outlook Summary results (x million)

Solid results first half year 2004 Accell Group

Solid results first half year 2004 Accell Group René Takens (CEO), Hielke Sybesma (CFO) Amsterdam, 21 July 2004 1 Business goes well Autonomous Strong positioning of Accell Group s brands Effective marketing

Solid results first half year 2004 Accell Group René Takens (CEO), Hielke Sybesma (CFO) Amsterdam, 21 July 2004 1 Business goes well Autonomous Strong positioning of Accell Group s brands Effective marketing

The U.S. Economic Outlook

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder Member FDIC VectraBank.com Economic Outlook 2015 Richard

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder Member FDIC VectraBank.com Economic Outlook 2015 Richard