The UK residential development market: Are we building enough homes and what is the pipeline of land to put them on?

|

|

|

- Jordan Hood

- 5 years ago

- Views:

Transcription

1 The UK residential development market: Are we building enough homes and what is the pipeline of land to put them on? Lucy Greenwood, Savills Residential Research 16th March 2016

2 Housing market Supply Who is building the new homes? What is affecting the delivery of new homes? Development land Strategic land

3 Housing market

4 The shape of price growth

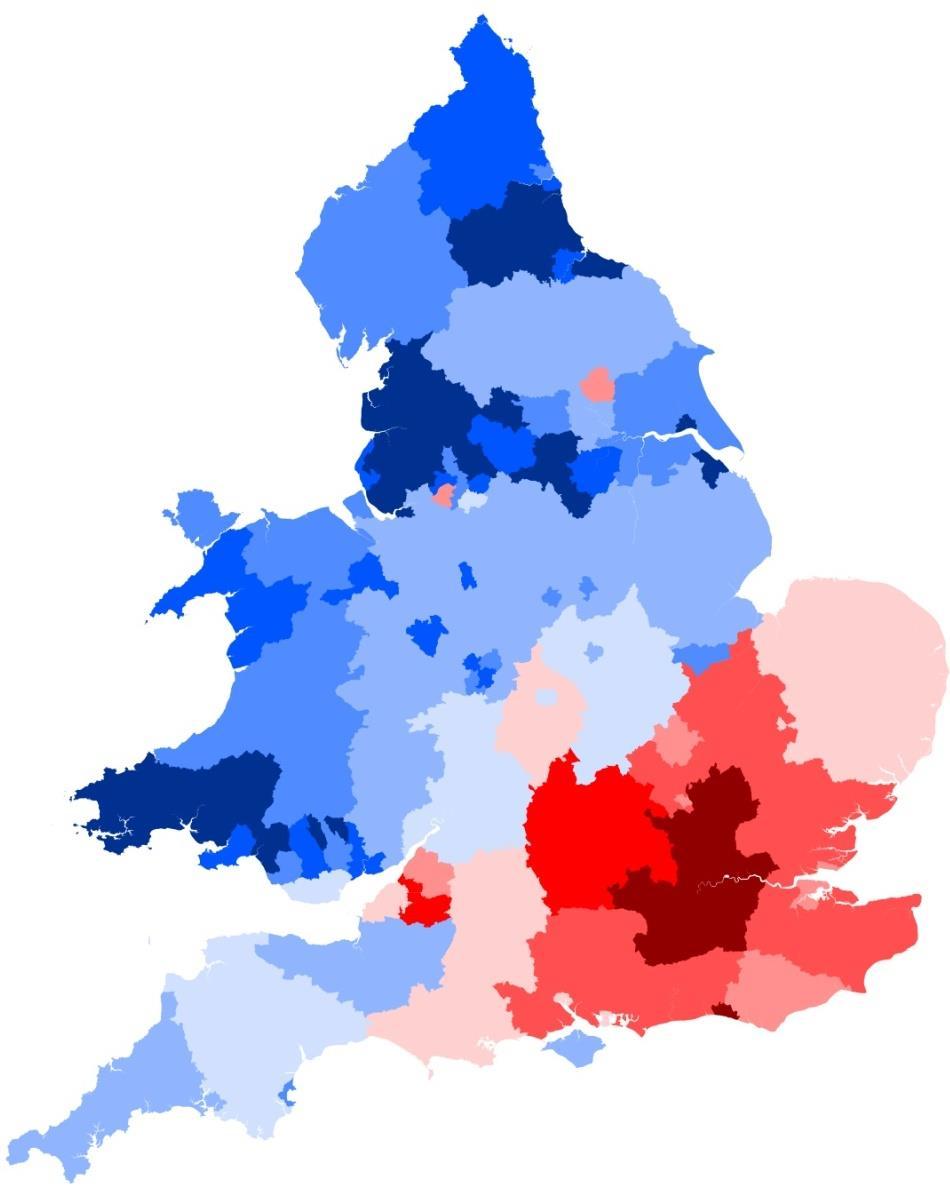

5 5 Price and transaction volume recovery Source: Land Registry 150% 140% London 130% Price vs peak 120% South East 110% East 100% England & Wales South West West Midlands (region) East Midlands 90% Wales North West Yorks & Humber 80% North East 70% 60% 65% 70% 75% 80% 85% 90% 95% Transactions vs pre-crunch average

6 Mid cycle reference point in the residential market? Source: Savills London to UK Prime central London to UK house price London to UK House Price Prime Central London to UK

7 Mar-06 Sep-06 Mar-07 Sep-07 Mar-08 Sep-08 Mar-09 Sep-09 Mar-10 Sep-10 Mar-11 Sep-11 Mar-12 Sep-12 Mar-13 Sep-13 Mar-14 House prices and transactions Source: HMRC, Nationwide, Halifax, HM Land Registry (England and Wales) Index (100=2007 Peak) UK Transactions Nationwide Halifax Land Registry Sep-14 Mar-15 Sep-15 2,000,000 1,800,000 1,600,000 1,400,000 1,200,000 1,000, , , , ,000 0 Number of Transactions in UK

8 Price growth to spread out from London 5 Year house price inflation Source: Savills forecasts for house price growth 5yrs Published Nov 2015

9 % 70% 60% 50% 40% 30% 20% 10% 0% Proportion of housing in England Rental demand is here to stay Source: Savills, DCLG Owner Occupied Social Rented Private Rented

10 Spread of PRS, areas with more than 15% of households in PRS Spread of PRS, areas with more than 15% of households in PRS Source: Census

11 Supply

12 Mar-06 Sep-06 Mar-07 Sep-07 Mar-08 Sep-08 Mar-09 Sep-09 Mar-10 Ongoing shortfall of supply Source: Savills using DCLG data, HBF and TCPA 300, , , , ,000 50,000 0 Additional homes per annum in England Permissions Sep-10 Mar-11 Sep-11 Mar-12 Sep-12 Mar-13 Sep-13 Mar-14 TCPA need projection (Holmans) Sep-14 Mar-15 Sep-15 Mar-16 Sep-16 Other starts New build starts

13 Transactions and private housing starts in England have been at a 10 to 1 ratio over the last 25 years Source: HMRC, DCLG 0 Annual transactions 2,500,000 2,000,000 1,500,000 1,000, ,000 Annual Transactions (lhs) Annual Private Housebuilding Starts (rhs) 250, , , ,000 50,000 0 Annual private housebuilding starts

14 More than just housebuilding conversions and change of use Source: DCLG Net additional dwellings 2014/15 35,000 30,000 25,000 20,000 15,000 10,000 5, ,000 South East London South West East of England North West West Midlands New build Net conversions Net change of use Net other gains and losses Demolitions Total net additional dwellings East Midlands Yorkshire and The Humber North East

15 Last years data on regional shortfalls Source: DCLG, HBF using Glenigan, TCPA Net additional dwellings Consents Housing need Shortfall (net additional vs need) Number of homes (year to Q1 2015) 60,000 50,000 40,000 30,000 20,000 10,000-52% 32% 34% London South East East of England South West 8% 17% West Midlands 33% Yorkshire 24% East Midlands North West 5% 16% North East 60% 50% 40% 30% 20% 10% 0% Shortfall

16 Who is building?

17 Private sector have been building the majority of homes Source: DCLG, NB: This uses adjusted quarterly completions data to 2006, applies the proportions of private, RSL and LA from quarterly data and assumes all LA and RSL completions are affordable Unsupported market sale Implied affordable delivered by private sector Local authorities Supported sales (Help to Buy and New Buy) Housing associations Number of new homes completed (England) 200, , , , ,000 75,000 50,000 25,000 0 Year to March

18 Larger housebuilders are building increasing proportions of new homes Source: NHBC New homes registered 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% 500+ units units units

19 More than 50% of new homes from top 9 plc housebuilders Source: Housebuilder annual report, financial year 80,000 Barratt Developments PLC Persimmon PLC Taylor Wimpey PLC Bellway PLC Redrow PLC Bovis Homes Group PLC Berkeley Group Holdings PLC Galliford Try PLC Crest Nicholson Holdings PLC Number of homes completed 70,000 60,000 50,000 40,000 30,000 20,000 10,

20 Constraints

21 Starter Homes Help to Buy Shared ownership Buy to Let Direct commissioning Planning

22 At least 57% Housebuilder constraints of Local Planning Authorities lack a five year land supply Source: HBF 2015 Survey 65% 41% 32% 18% 15% Planning delays Labour availability Labour costs Land availability Land prices

23 Development land market

24 Wide variation in land market strength Source: Savills Index (100=2007 peak) London UK Greenfield UK Urban Land price versus '07/'08 peak -60% -40% -20% 0% 20% 40% Oxford Sevenoaks Cambridge Reading/Bracknell Below peak UK Above peak Milton Keynes Rugby Leeds Peterborough

25 Land market competition most notable in the most constrained markets Source: Savills, HM Land Registry Lincoln Strong markets with more land choice Luton Lagging markets with land choice Reading/Bracknell Milton Keynes Aberdeen Cambridge 20% Sevenoaks Bristol Central London Strong markets with little land choice Solihull 0% Land value vs '07/'08 peak -70% Nottingham -50% -30% -10% 10% 30% 50% Bradford Telford Leeds Wolverhampton -10% -20% 60% 50% 40% 30% 10% -30% House price vs '07/'08 peak Oxford City and East of City Brighton Crawley Haywards Heath Existing Wealth Belts

26 Development land ownership Source: Savills Development Database Residential plots Housebuilder Other Developers Promoter and Investors Other Private Sector Public Registered Provider 400, , , , , , ,000 50,000 0 Outline Plans Submitted Outline Plans Granted Reserved Matters Detailed Plans Submitted Reserved Matters Granted Detailed Plans Granted Application process Detailed permission

27 Listed housebuilders permissioned land banks growing at c.10% per annum Source: Housebuilder annual report, financial year Galliford Try Crest Nicholson Redrow Bovis Bellway Berkeley Barratt Taylor Wimpey Persimmon 400,000 Number of plots with full planning permission 350, , , , , ,000 50,

28 Margin discipline maintained Source: Thomson Reuters 30 Operating margin net of exceptional items, % Barratt Bovis Redrow Taylor Wimpey Persimmon Crest Nicholson Bellway Berkeley Average

29 Strategic land market

30 Strategic and development land ownership Source: Savills Development Database, at January 2016 Residential plots Housebuilder Other Developers Promoter and Investors Other Private Sector Public Registered Provider 700, , , , , , ,000 0 Pre-Planning Outline Plans Submitted Outline Plans Granted Reserved Matters Detailed Plans Submitted Reserved Matters Granted Detailed Plans Granted Application process Detailed permission

31 Top housebuilders are increasing their volume of strategic land and have been increasingly bringing their own land through the planning system Source: Housebuilder annual reports, financial year Number of plots without full planning permission 300, , , , ,000 50,000 0 Berkeley Crest Nicholson Bellway Bovis Redrow Barratt Taylor Wimpey

32 Outlook

33 Household income Housing need 2014 delivery Likely future delivery Households able to afford market housing Households in need of sub-market housing Affordable rent Social rent Much reduced delivery of submarket rent funded by grant and Section 106 Future sub-market rent funded through crosssubsidy Market new homes Help to Buy: Equity Loan Shared ownership Market new homes Help to Buy: Equity Loan Starter Homes Shared ownership Buy to Let?

34 PRS is here to stay Buy to Let v First Time Buyers Source: Savills, CLG, CML (English Housing Survey) 400,000 Estimated growth in PRS (EHS) Savills Estimate of Growth in PRS (UK) BTL lending for HP 350,000 Number of households 300, , , , ,000 50,

35 Scenarios for development land values Source: Savills, NHBC, housebuilder annual reports Source: Savills SCENARIO 1 UK greenfield development land values (100= 2007 peak) Plc housebuilder operating margin peaks at average 17.7% UK completions peak at 226,000 a year 17,842 NHBC registered house builders Lehman Brothers go bust UK completions fall to 137,000 homes per year Negative operating profit for plc housebuilders on average 9,859 NHBC registered house builders Plcs operating margin close to target, averaging 16.5% Supply of land constrained Other players pushed out of the market and fewer homes delivered Static land values SCENARIO 2 Increased supply of land in the highest demand areas Space for all players in the land market and more homes delivered

36 What next? Macro Interest rates lower for longer Brexit uncertainty Business investment Construction labour Household formation Housing & planning policy 1. Home ownership 2. Housing supply Starter homes Buy to let restrictions Direct commissioning on public land Local Plan led v Appeals Garden villages PDR Brownfield registers Density on transport

37 Savills 2016

Cross Sector Property Update

Ian Cross Sector Property Update Johnny Dudgeon, FRICS Savills Lincoln Email: jdudgeon@savills.com Tel: 01522 508952 UK Housing Market Residential Rural Commercial Strategic Land East Midlands West Midlands

Ian Cross Sector Property Update Johnny Dudgeon, FRICS Savills Lincoln Email: jdudgeon@savills.com Tel: 01522 508952 UK Housing Market Residential Rural Commercial Strategic Land East Midlands West Midlands

Conference Welcome and Introduction

Conference 2013 Welcome and Introduction Housing stock Present day Owner occupation Private renting 17.5m 4m 66% 15.1% Housing associations Council housing 2.8m 2.2m 26.5m 10.6% 8.3% > 2.8m Social Housing

Conference 2013 Welcome and Introduction Housing stock Present day Owner occupation Private renting 17.5m 4m 66% 15.1% Housing associations Council housing 2.8m 2.2m 26.5m 10.6% 8.3% > 2.8m Social Housing

Friday, May 22, NAR Convention

NAR Convention 5-14-09 NAR Convention 5-14-09 Lawrence Yun, NAR Chief Economist NAR Marketing Tips!Provide Market Data to buyers!forbes Buyer Survey: Now good time to buy home!best Banner Ads: 1. Has Market

NAR Convention 5-14-09 NAR Convention 5-14-09 Lawrence Yun, NAR Chief Economist NAR Marketing Tips!Provide Market Data to buyers!forbes Buyer Survey: Now good time to buy home!best Banner Ads: 1. Has Market

What is the outlook for the prime residential markets?

What is the outlook for the prime residential markets? Katy Warrick Market Update Mat Oakley Commercial View Lucian Cook Residential Forecasts Emily Donovan London Development Living in uncertain times

What is the outlook for the prime residential markets? Katy Warrick Market Update Mat Oakley Commercial View Lucian Cook Residential Forecasts Emily Donovan London Development Living in uncertain times

Regional Spread of Inbound Tourism

Regional Spread of Inbound Tourism Foresight issue 157 VisitBritain Research 1 Contents Introduction Summary Key metrics by UK area Analysis by UK area Summary of growth by UK area Scotland Wales North

Regional Spread of Inbound Tourism Foresight issue 157 VisitBritain Research 1 Contents Introduction Summary Key metrics by UK area Analysis by UK area Summary of growth by UK area Scotland Wales North

Dick Vos Senior Manager Research & Strategy

Dick Vos Senior Manager Research & Strategy! House prices now falling at fastest rate since early 1990s House prices will fall 7% in 'uncertain' market IMF warns on global house prices House prices Through

Dick Vos Senior Manager Research & Strategy! House prices now falling at fastest rate since early 1990s House prices will fall 7% in 'uncertain' market IMF warns on global house prices House prices Through

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States?

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

MARKET AND CAPACITY UPDATE. Matthew Marsh September 2016

MARKET AND CAPACITY UPDATE Matthew Marsh September 2016 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

MARKET AND CAPACITY UPDATE Matthew Marsh September 2016 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

U.S. Property Market Outlook, 2013Q1. Jim Costello, Managing Director CBRE Americas Research Investment Research

U.S. Property Market Outlook, 2013Q1 Jim Costello, Managing Director CBRE Americas Research Investment Research CBRE Page 2 Outlook for the Real Side of the Economy Operationally, what do Research Teams

U.S. Property Market Outlook, 2013Q1 Jim Costello, Managing Director CBRE Americas Research Investment Research CBRE Page 2 Outlook for the Real Side of the Economy Operationally, what do Research Teams

Houston and Tomball Economic and. Housing Outlook. recenter.tamu.edu. Dr. James P. Gaines Research Economist

Houston and Tomball Economic and Dr. James P. Gaines Research Economist Housing Outlook recenter.tamu.edu THE CURRENT SITUATION The Future Just Ain t What It Used to Be! Yogi Berra National Economic Recovery

Houston and Tomball Economic and Dr. James P. Gaines Research Economist Housing Outlook recenter.tamu.edu THE CURRENT SITUATION The Future Just Ain t What It Used to Be! Yogi Berra National Economic Recovery

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Capital Markets Day Ebbsfleet Garden City

Capital Markets Day 2018 Ebbsfleet Garden City Capital Markets Day John Tutte Group Chief Executive Celebrating 100,000 th Redrow home Capital Markets Day 2018: Ebbsfleet Garden City 3 Capital Markets

Capital Markets Day 2018 Ebbsfleet Garden City Capital Markets Day John Tutte Group Chief Executive Celebrating 100,000 th Redrow home Capital Markets Day 2018: Ebbsfleet Garden City 3 Capital Markets

QUARTERLY ANALYSIS : SALES Analysis by Sam Long and Tim Craine, April 2018

QUARTERLY ANALYSIS : SALES Analysis by Sam Long and Tim Craine, April 2018 For residential market experts www.moliorlondon.com MOLIOR. LONDON residential. development. research 2 Sales Report April 2018

QUARTERLY ANALYSIS : SALES Analysis by Sam Long and Tim Craine, April 2018 For residential market experts www.moliorlondon.com MOLIOR. LONDON residential. development. research 2 Sales Report April 2018

Highways England Creative M Welcome. Smart motorway M6 junctions 16 to 19 public information exhibition

Welcome Smart motorway junctions 16 to 19 public information exhibition Smart motorway junctions 16 to 19 Making the motorway better The is also part of the Highways England strategic road network connecting

Welcome Smart motorway junctions 16 to 19 public information exhibition Smart motorway junctions 16 to 19 Making the motorway better The is also part of the Highways England strategic road network connecting

TENDER PRICE INDICATOR 2 ND QUARTER 2016

TENDER PRICE INDICATOR 2 ND QUARTER 2016 As the Brexit vote looms the potential for an unprecedented exit from Europe remains a possibility, uncertainty surrounding this is having an effect on investment

TENDER PRICE INDICATOR 2 ND QUARTER 2016 As the Brexit vote looms the potential for an unprecedented exit from Europe remains a possibility, uncertainty surrounding this is having an effect on investment

U.S. AUTO INDUSTRY UPDATE Federal Reserve Bank of Chicago Automotive Outlook Symposium. Emily Kolinski Morris Chief Economist May 2015

U.S. AUTO INDUSTRY UPDATE Federal Reserve Bank of Chicago Automotive Outlook Symposium Emily Kolinski Morris Chief Economist May 2015 NORTH AMERICA INDUSTRY VOLUME SUMMARY 13.1 Total North America* (Mils.)

U.S. AUTO INDUSTRY UPDATE Federal Reserve Bank of Chicago Automotive Outlook Symposium Emily Kolinski Morris Chief Economist May 2015 NORTH AMERICA INDUSTRY VOLUME SUMMARY 13.1 Total North America* (Mils.)

Dr. James P. Gaines Research Economist recenter.tamu.edu

Texas Uncertain Economy in a World of Uncertain Oil Prices Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 U.S. Outlook Expected GDP growth still modest:

Texas Uncertain Economy in a World of Uncertain Oil Prices Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 U.S. Outlook Expected GDP growth still modest:

Real Estate and Economic Outlook

Real Estate and Economic Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation at Inforum Outlook Conference University of Maryland College Park, MD December 12, 2013

Real Estate and Economic Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation at Inforum Outlook Conference University of Maryland College Park, MD December 12, 2013

President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H. Parker Willis Lecture in Political Economics

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

Europe June Craig Menear. Chairman, CEO & President. Diane Dayhoff. Vice President, Investor Relations

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

Europe June 2016 Craig Menear Chairman, CEO & President Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements contained in today

Cargo outlook Brian Pearce Chief Economist. 13 December 2018

Cargo outlook 2019 Brian Pearce Chief Economist 13 December 2018 1 Cargo revenue contribution stabilizing 2 % total revenues 82% 80% 78% 76% 74% 72% 70% 68% 66% 64% 62% 2008 2009 2010 2011 2012 2013 2014

Cargo outlook 2019 Brian Pearce Chief Economist 13 December 2018 1 Cargo revenue contribution stabilizing 2 % total revenues 82% 80% 78% 76% 74% 72% 70% 68% 66% 64% 62% 2008 2009 2010 2011 2012 2013 2014

Economic Outlook: fear over fundamentals

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

DFW MULTIFAMILY TRENDS & OBSERVATIONS Q2 2017

DFW MULTIFAMILY TRENDS & OBSERVATIONS Q2 2017 DALLAS / FORT WORTH The Top US Demand Driven Apartment Market DFW MULTIFAMILY STARTS A HISTORY LESSON!!! The challenge boom or bust perception vs recent history

DFW MULTIFAMILY TRENDS & OBSERVATIONS Q2 2017 DALLAS / FORT WORTH The Top US Demand Driven Apartment Market DFW MULTIFAMILY STARTS A HISTORY LESSON!!! The challenge boom or bust perception vs recent history

PHILADELPHIA HOUSE PRICE INDICES

PHILADELPHIA HOUSE PRICE INDICES February 13, 2017 KEVIN C. GILLEN, Ph.D. Kevin.C.Gillen@Drexel.edu Disclaimers and Acknowledgments: The Lindy Institute for Urban Innovation at Drexel University provides

PHILADELPHIA HOUSE PRICE INDICES February 13, 2017 KEVIN C. GILLEN, Ph.D. Kevin.C.Gillen@Drexel.edu Disclaimers and Acknowledgments: The Lindy Institute for Urban Innovation at Drexel University provides

Dr. James P. Gaines Research Economist. recenter.tamu.edu

Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 National Issues Expected GDP growth still modest: 2015 2.5%; personal consumption 2.5% Inflation not worrisome:

Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 National Issues Expected GDP growth still modest: 2015 2.5%; personal consumption 2.5% Inflation not worrisome:

Domestic Energy Fact File (2006): Owner occupied, Local authority, Private rented and Registered social landlord homes

: Owner occupied, Local authority, Private rented and Registered social landlord homes") Domestic Energy Fact File (2006): Owner occupied, Local authority, Private rented and Registered social landlord homes Domestic Energy Fact File (2006): Owner occupied, Local authority, Private rented

Domestic Energy Fact File (2006): Owner occupied, Local authority, Private rented and Registered social landlord homes Domestic Energy Fact File (2006): Owner occupied, Local authority, Private rented

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

Economic and Real Estate Outlook

Economic and Real Estate Outlook By Lawrence Yun, Ph.D. Chief Economist, National Association of REALTORS Presentation at Charlottesville Area Association of REALTORS October 13, 2016 1990 1991 1992 1993

Economic and Real Estate Outlook By Lawrence Yun, Ph.D. Chief Economist, National Association of REALTORS Presentation at Charlottesville Area Association of REALTORS October 13, 2016 1990 1991 1992 1993

Housing Market Update Greater Moncton. Housing market intelligence you can count on

Housing Market Update Greater Moncton Housing market intelligence you can count on Housing Market Drivers Multi-Residential/Rental Market New Home Market Single Family Homes Resale Market 2013/2014 Outlook

Housing Market Update Greater Moncton Housing market intelligence you can count on Housing Market Drivers Multi-Residential/Rental Market New Home Market Single Family Homes Resale Market 2013/2014 Outlook

21/02/2018. How Far is it Acceptable to Walk? Introduction. How Far is it Acceptable to Walk?

21/2/218 Introduction Walking is an important mode of travel. How far people walk is factor in: Accessibility/ Sustainability. Allocating land in Local Plans. Determining planning applications. Previous

21/2/218 Introduction Walking is an important mode of travel. How far people walk is factor in: Accessibility/ Sustainability. Allocating land in Local Plans. Determining planning applications. Previous

Global economy s strong momentum intact despite elevated level of uncertainty. Canada headed for another year of solid growth

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

Shifting International Trade Routes A National Economic Outlook. February 1, 2011

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

PHILADELPHIA HOUSE PRICE INDICES

PHILADELPHIA HOUSE PRICE INDICES July 20, 2017 KEVIN C. GILLEN, Ph.D. Kevin.C.Gillen@Drexel.edu Disclaimers and Acknowledgments: The Lindy Institute for Urban Innovation at Drexel University provides this

PHILADELPHIA HOUSE PRICE INDICES July 20, 2017 KEVIN C. GILLEN, Ph.D. Kevin.C.Gillen@Drexel.edu Disclaimers and Acknowledgments: The Lindy Institute for Urban Innovation at Drexel University provides this

Hotel Industry Update. Stephen Hennis, CHA, ISHC

Hotel Industry Update Stephen Hennis, CHA, ISHC 1 Through Aug 2012: Strong Results Despite Headwinds % Change Room Supply* 1.2 bn 0.4% Room Demand* 741 mm 3.3% Occupancy 63% 2.9% A.D.R. $106 4.3% RevPAR

Hotel Industry Update Stephen Hennis, CHA, ISHC 1 Through Aug 2012: Strong Results Despite Headwinds % Change Room Supply* 1.2 bn 0.4% Room Demand* 741 mm 3.3% Occupancy 63% 2.9% A.D.R. $106 4.3% RevPAR

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes. Tom Rogers. Lead Economist, Oxford Economics.

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

Rochester Area Bike Sharing Program Study

roc bike share Rochester Area Bike Sharing Program Study Executive Summary ~ January 2015 JANUARY 2015 8484 Georgia Avenue, Suite 800 Silver Spring, MD 20910 3495 Winton Pl., Bldg E, Suite 110 Rochester,

roc bike share Rochester Area Bike Sharing Program Study Executive Summary ~ January 2015 JANUARY 2015 8484 Georgia Avenue, Suite 800 Silver Spring, MD 20910 3495 Winton Pl., Bldg E, Suite 110 Rochester,

Demographic change, long-run housing demand and the related challenges for the Irish banking sector

Demographic change, long-run housing demand and the related challenges for the Irish banking sector December 5 th, 2016 esri.ie David Duffy, Daniel Foley, Kieran McQuinn and Niall McInerney Outline: Addresses

Demographic change, long-run housing demand and the related challenges for the Irish banking sector December 5 th, 2016 esri.ie David Duffy, Daniel Foley, Kieran McQuinn and Niall McInerney Outline: Addresses

10 County Conference. Richard Wobbekind. Executive Director Business Research Division & Senior Associate Dean Leeds School of Business

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

Economic Analysis of Farmland Market: An Introduction

Economic Analysis of Farmland Market: An Introduction Dr. Wendong Zhang Assistant Professor of Economics wdzhang@iastate.edu FIN 450X, Feb 17 th, 2017 A Quick Introduction: Dr. Wendong Zhang Grown up in

Economic Analysis of Farmland Market: An Introduction Dr. Wendong Zhang Assistant Professor of Economics wdzhang@iastate.edu FIN 450X, Feb 17 th, 2017 A Quick Introduction: Dr. Wendong Zhang Grown up in

Transport Workshop Dearbhla Lawson Head of Transport & Infrastructure Policy & Funding University of the Third Age.

Transport Workshop Dearbhla Lawson Head of Transport & Infrastructure Policy & Funding University of the Third Age 30 th March 2015 1 Presentation Overview Roles and responsibilities Snapshot of Key Challenges

Transport Workshop Dearbhla Lawson Head of Transport & Infrastructure Policy & Funding University of the Third Age 30 th March 2015 1 Presentation Overview Roles and responsibilities Snapshot of Key Challenges

U.S. REITs have rebounded strongly Dow Jones Equity REIT Total Return Index

U.S. REITs have rebounded strongly Dow Jones Equity REIT Total Return Index Index, 2005 = 100 250 200 150 100 50 0 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Sources: Bloomberg, Dow Jones. Affordability

U.S. REITs have rebounded strongly Dow Jones Equity REIT Total Return Index Index, 2005 = 100 250 200 150 100 50 0 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Sources: Bloomberg, Dow Jones. Affordability

It Was Never Going To Be Easy

It Was Never Going To Be Easy Stephen Toplis, Head of Research July 2010 Introduction Global power shift sustained Average outlook on the improve Fiscal constraints binding Domestic rebalance under way

It Was Never Going To Be Easy Stephen Toplis, Head of Research July 2010 Introduction Global power shift sustained Average outlook on the improve Fiscal constraints binding Domestic rebalance under way

The Importance of Infrastructure and Real Estate for the Future of Brussels, Europe s Capital.

The Importance of Infrastructure and Real Estate for the Future of Brussels, Europe s Capital. ERES INDUSTRY SEMINAR, Brussels Jean-Paul Loozen, March 11, 2016 Academic Director Executive Programme in

The Importance of Infrastructure and Real Estate for the Future of Brussels, Europe s Capital. ERES INDUSTRY SEMINAR, Brussels Jean-Paul Loozen, March 11, 2016 Academic Director Executive Programme in

RISI Housing Report An Update on the Housing Market

RISI Housing Report An Update on the Housing Market North American Conference October 2018 Jennifer Coskren Senior Economist Agenda Current housing demand and demographic conditions Supply and impediments

RISI Housing Report An Update on the Housing Market North American Conference October 2018 Jennifer Coskren Senior Economist Agenda Current housing demand and demographic conditions Supply and impediments

Canada s economy on track for a solid 2018 although policy uncertainty lingers

Canada s economy on track for a solid 2018 although policy uncertainty lingers Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com March 2018 Canada is facing a challenging

Canada s economy on track for a solid 2018 although policy uncertainty lingers Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com March 2018 Canada is facing a challenging

European Commission. Harmonisation of BCS: Aggregation methods (business surveys) and Quality checking (consumer survey)

and Quality checking (consumer survey)") European Commission Directorate General Economic and Financial Affairs Harmonisation of BCS: Aggregation methods (business surveys) and Quality checking (consumer survey) Roberta Friz Business and consumer

European Commission Directorate General Economic and Financial Affairs Harmonisation of BCS: Aggregation methods (business surveys) and Quality checking (consumer survey) Roberta Friz Business and consumer

Iowa Farmland Market Update: What s Ahead?

Iowa Farmland Market Update: What s Ahead? Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 Ag Credit School, June 14 th, 2017 The new Mike Duffy

Iowa Farmland Market Update: What s Ahead? Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 Ag Credit School, June 14 th, 2017 The new Mike Duffy

Clackmannanshire Council. Housing Need and Demand Assessment. 1.0 Introduction

Clackmannanshire Council Housing Need and Demand Assessment 1.0 Introduction Establishing a clear picture of housing need and demand in Clackmannanshire is essential to inform Council policy in relation

Clackmannanshire Council Housing Need and Demand Assessment 1.0 Introduction Establishing a clear picture of housing need and demand in Clackmannanshire is essential to inform Council policy in relation

First Lecture Capitalism: A Brief History

Nitzan / 3270 GPE I I. Capitalism: A Brief History / 1 First Lecture Capitalism: A Brief History Definition Economic system? Private ownership / profit motive / wage labour Beginnings 16 th century: Feudal

Nitzan / 3270 GPE I I. Capitalism: A Brief History / 1 First Lecture Capitalism: A Brief History Definition Economic system? Private ownership / profit motive / wage labour Beginnings 16 th century: Feudal

Economic Outlook for Canada: Economy Confronting Capacity Limits

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

A Primer on Factors Affecting Farmland Values

A Primer on Factors Affecting Farmland Values Federal Reserve Bank of Chicago David Oppedahl Business Economist 312-322-6122 david.oppedahl@chi.frb.org The economy hit bottom in June 2009, with hesitant

A Primer on Factors Affecting Farmland Values Federal Reserve Bank of Chicago David Oppedahl Business Economist 312-322-6122 david.oppedahl@chi.frb.org The economy hit bottom in June 2009, with hesitant

As Good as it Gets. The Aging Expansion Powers On... but for How Much Longer? Andrew J. Nelson Chief Economist USA, Colliers International

As Good as it Gets The Aging Expansion Powers On... but for How Much Longer? Andrew J. Nelson Chief Economist USA, Colliers International #NMHCstudent @ApartmentWire Ten Years After: A Full if Imperfect

As Good as it Gets The Aging Expansion Powers On... but for How Much Longer? Andrew J. Nelson Chief Economist USA, Colliers International #NMHCstudent @ApartmentWire Ten Years After: A Full if Imperfect

32 nd Annual CanaData Construction Forecasts Conference

32 nd Annual CanaData Construction Forecasts Conference Economic Intelligence September 21 st, 2017 Toronto Peter Norman, VP & Chief Economist, Economic Consulting Our Company Structure at a Glance ARGUS

32 nd Annual CanaData Construction Forecasts Conference Economic Intelligence September 21 st, 2017 Toronto Peter Norman, VP & Chief Economist, Economic Consulting Our Company Structure at a Glance ARGUS

Further Opening Up and Reform of China s Capital Market

Further Opening Up and Reform of China s Capital Market Haizhou Huang January 7, 2016 China economy and capital market: Finding new normal 1 Macro: We expect China GDP to grow 6.9% in 2015 and 6.8% in

Further Opening Up and Reform of China s Capital Market Haizhou Huang January 7, 2016 China economy and capital market: Finding new normal 1 Macro: We expect China GDP to grow 6.9% in 2015 and 6.8% in

Agriculture and the Economy: A View from the Chicago Fed

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

BC Pension Forum. Economic Outlook. Presented by: Ben Homsy, CFA Portfolio Manager

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

BC Pension Forum Economic Outlook Presented by: Ben Homsy, CFA Portfolio Manager 1694 1704 1713 1723 1732 1741 1751 1760 1770 1779 1788 1798 1807 1817 1826 1836 1845 1854 1864 1873 1883 1892 1901 1911

A Financial Systems Resilience Index for South Africa: Joining the Twin Peaks

A Financial Systems Resilience Index for South Africa: Joining the Twin Peaks Professor Christine Oughton SOAS University of London co12@soas.ac.uk KEY ISSUES FOR EFFECTIVE MACROPRUDENTIAL POLICYMAKING

A Financial Systems Resilience Index for South Africa: Joining the Twin Peaks Professor Christine Oughton SOAS University of London co12@soas.ac.uk KEY ISSUES FOR EFFECTIVE MACROPRUDENTIAL POLICYMAKING

MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION

OXYGEN EVENTS CONFERENCE GALA PERFORMANCE 2017 MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION - THE CASE OF ROMANIA - Ph.D. Andrei RĂDULESCU Senior Economist, Banca Transilvania Researcher, Institute

OXYGEN EVENTS CONFERENCE GALA PERFORMANCE 2017 MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION - THE CASE OF ROMANIA - Ph.D. Andrei RĂDULESCU Senior Economist, Banca Transilvania Researcher, Institute

UK Integrated Behaviour Change Programmes

UK Integrated Behaviour Change Programmes 17 th November 2009 ACT TDM Summit Conference Daniel Johnson, Transport for London Nicky Ward, Steer Davies Gleave Structure 1. UK travel behaviour change 2. An

UK Integrated Behaviour Change Programmes 17 th November 2009 ACT TDM Summit Conference Daniel Johnson, Transport for London Nicky Ward, Steer Davies Gleave Structure 1. UK travel behaviour change 2. An

PHILADELPHIA HOUSE PRICE INDICES

PHILADELPHIA HOUSE PRICE INDICES January 15, 2015 KEVIN C. GILLEN, Ph.D. Kevin.C.Gillen@Drexel.edu Disclaimers and Acknowledgments: The Lindy Institute for Urban Innovation at Drexel University provides

PHILADELPHIA HOUSE PRICE INDICES January 15, 2015 KEVIN C. GILLEN, Ph.D. Kevin.C.Gillen@Drexel.edu Disclaimers and Acknowledgments: The Lindy Institute for Urban Innovation at Drexel University provides

PHILADELPHIA HOUSE PRICE INDICES

PHILADELPHIA HOUSE PRICE INDICES April 14, 2014 KEVIN C. GILLEN, Ph.D. gillenk@upenn.edu Disclaimers and Acknowledgments: The Fels Institute of Government at the University of Pennsylvania provides this

PHILADELPHIA HOUSE PRICE INDICES April 14, 2014 KEVIN C. GILLEN, Ph.D. gillenk@upenn.edu Disclaimers and Acknowledgments: The Fels Institute of Government at the University of Pennsylvania provides this

The global economic climate and impact on SA Mining during a downward phase in the commodity cycle.

The global economic climate and impact on SA Mining during a downward phase in the commodity cycle. World Economy Real Long term commodity and employment data. Vanity sanity and reality of mining and investment

The global economic climate and impact on SA Mining during a downward phase in the commodity cycle. World Economy Real Long term commodity and employment data. Vanity sanity and reality of mining and investment

Will 2016 Be the Last Hurrah for Commercial Real Estate? Presented By: John Chang First Vice-President Marcus & Millichap Research Services

Will 2016 Be the Last Hurrah for Commercial Real Estate? Presented By: John Chang First Vice-President Marcus & Millichap Research Services Rising Uncertainty Creating Headwinds for Commercial Real Estate

Will 2016 Be the Last Hurrah for Commercial Real Estate? Presented By: John Chang First Vice-President Marcus & Millichap Research Services Rising Uncertainty Creating Headwinds for Commercial Real Estate

2009 California & Bay Area Real Estate Market Outlook

2009 California & Bay Area Real Estate Market Outlook November 24, 2008 Fairmont Hotel Leslie Appleton-Young C.A.R. Vice President and Chief Economist California Real Estate Market: 2008 California s Housing

2009 California & Bay Area Real Estate Market Outlook November 24, 2008 Fairmont Hotel Leslie Appleton-Young C.A.R. Vice President and Chief Economist California Real Estate Market: 2008 California s Housing

Child Road Safety in Great Britain,

Child Road Safety in Great Britain, 21-214 Bhavin Makwana March 216 Summary This short report looks at child road casualties in Great Britain between 21 and 214. It looks at how children travel, the geographical

Child Road Safety in Great Britain, 21-214 Bhavin Makwana March 216 Summary This short report looks at child road casualties in Great Britain between 21 and 214. It looks at how children travel, the geographical

Philadelphia Housing s Recovery Becomes More Equitable in Q3 Sales surge citywide; house value appreciation strongest in low-priced neighborhoods.

Philadelphia Housing s Recovery Becomes More Equitable in Q3 Sales surge citywide; house value appreciation strongest in low-priced neighborhoods. October 13, 2014: After a brisk spring which saw widespread

Philadelphia Housing s Recovery Becomes More Equitable in Q3 Sales surge citywide; house value appreciation strongest in low-priced neighborhoods. October 13, 2014: After a brisk spring which saw widespread

Economy On The Rebound

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Spring Time for Housing

Spring Time for Housing Arizona State University December 2 nd, 2015 Presented By: Elliott D. Pollack CEO, IN PHOENIX 1 2 The World has Changed Pre-2007 Post-2007 3 Employment Growth From Bottom of Recession

Spring Time for Housing Arizona State University December 2 nd, 2015 Presented By: Elliott D. Pollack CEO, IN PHOENIX 1 2 The World has Changed Pre-2007 Post-2007 3 Employment Growth From Bottom of Recession

CALIFORNIA STATE UNIVERSITY LONG BEACH. Southern California Regional Economic Forecast

CALIFORNIA STATE UNIVERSITY LONG BEACH Southern California Regional Economic Forecast Lisa M. Grobar, Ph.D. Director, CSULB Economic Forecast Project Office of Economic Research 2009: A terrible year for

CALIFORNIA STATE UNIVERSITY LONG BEACH Southern California Regional Economic Forecast Lisa M. Grobar, Ph.D. Director, CSULB Economic Forecast Project Office of Economic Research 2009: A terrible year for

Seven Lean Years Explaining Persistent Global Economic Weakness

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

The Cairns Economy Recent Trends and Prospects

MINING, AGRICULTURE, TOURISM, TRANSPORT, CONSTRUCTION, MANUFACTURING, DEFENCE, EDUCATION, ADMINISTRATION, SERVICES The Cairns Economy Recent Trends and Prospects WS (Bill) Cummings PRESENTATION TO Ref:

MINING, AGRICULTURE, TOURISM, TRANSPORT, CONSTRUCTION, MANUFACTURING, DEFENCE, EDUCATION, ADMINISTRATION, SERVICES The Cairns Economy Recent Trends and Prospects WS (Bill) Cummings PRESENTATION TO Ref:

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Alternative Measures of Economic Activity. Jan J. J. Groen, Officer Research and Statistics Group

Alternative Measures of Economic Activity Jan J. J. Groen, Officer Research and Statistics Group High School Fed Challenge Student Orientation: February 1 and 2, 217 Outline Alternative indicators: data

Alternative Measures of Economic Activity Jan J. J. Groen, Officer Research and Statistics Group High School Fed Challenge Student Orientation: February 1 and 2, 217 Outline Alternative indicators: data

2017 Nebraska Profile

2017 Nebraska Profile State, 9 NEW Regions, 93 Counties, plus 31 Cities Three Volumes Demographic Change in the State Economic Influences at Work Housing Statistics and Trends Summary of Findings Discuss

2017 Nebraska Profile State, 9 NEW Regions, 93 Counties, plus 31 Cities Three Volumes Demographic Change in the State Economic Influences at Work Housing Statistics and Trends Summary of Findings Discuss

Partnerships with Purpose: Housing for Texans

Partnerships with Purpose: Housing for Texans 25th Annual TALHFA Educational Conference October 25-27, 2017 Fort Worth, Texas Dr. James P. Gaines Chief Economist 2 Outlook Since November 10, 2017: Rising

Partnerships with Purpose: Housing for Texans 25th Annual TALHFA Educational Conference October 25-27, 2017 Fort Worth, Texas Dr. James P. Gaines Chief Economist 2 Outlook Since November 10, 2017: Rising

Company A Company A. Company A Board Meeting Presentation 12 th May 20XX

Board Meeting Presentation 12 th May 20XX Table of Contents CEO Overview Business Dashboard Quarterly Financials & forecasts Sales and Marketing Quarter specific items Strategic update: D2C Risk and Underwriting

Board Meeting Presentation 12 th May 20XX Table of Contents CEO Overview Business Dashboard Quarterly Financials & forecasts Sales and Marketing Quarter specific items Strategic update: D2C Risk and Underwriting

Iowa Farmland Market Update: What s Ahead?

Iowa Farmland Market Update: What s Ahead? Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 April 4 th, 2017 The new Mike Duffy since Aug 2015 30

Iowa Farmland Market Update: What s Ahead? Wendong Zhang Assistant Professor of Economics and Extension Economist wdzhang@iastate.edu 515-294-2536 April 4 th, 2017 The new Mike Duffy since Aug 2015 30

THE HOCKEY STRATEGY. UPDATED March 2012

THE HOCKEY STRATEGY UPDATED March 2012 1 CURRENT SITUATION SWOT Hockey has great potential with some unique strengths and competitive advantages...we must play to our strengths SWOT Strengths Global sport,

THE HOCKEY STRATEGY UPDATED March 2012 1 CURRENT SITUATION SWOT Hockey has great potential with some unique strengths and competitive advantages...we must play to our strengths SWOT Strengths Global sport,

The new normal. Mortgage holders are also taking advantage of low interest rates to pay down the principal with P&I loans sitting at 81%.

19 July 2018 The new normal Today s quarterly AFG Mortgage Index figures (ASX:AFG) show it is business as usual as a vibrant mortgage broking industry delivering choice and competition to the market continues

19 July 2018 The new normal Today s quarterly AFG Mortgage Index figures (ASX:AFG) show it is business as usual as a vibrant mortgage broking industry delivering choice and competition to the market continues

BRC/Springboard Footfall Monitor September 2014 Covering the five weeks 31 August October 2014

Strictly Embargoed until 00.01 hrs Monday 20 October 2014 OUT-OF-TOWN FOOTFALL CONTINUES POSITIVE TREND UK Total Retail Footfall* % change year-on-year High Street Out-of- Town Shopping Centre Summary

Strictly Embargoed until 00.01 hrs Monday 20 October 2014 OUT-OF-TOWN FOOTFALL CONTINUES POSITIVE TREND UK Total Retail Footfall* % change year-on-year High Street Out-of- Town Shopping Centre Summary

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office The views expressed in this presentation are strictly those of the author and do not necessarily

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office The views expressed in this presentation are strictly those of the author and do not necessarily

Colorado Economic Update

Colorado Economic Update Steamboat Economic Summit Place cover image here Brian Lewandowski Associate Director, Business Research Division October 21, 2016 Recession 8 Months Recession 18 Months Real GDP

Colorado Economic Update Steamboat Economic Summit Place cover image here Brian Lewandowski Associate Director, Business Research Division October 21, 2016 Recession 8 Months Recession 18 Months Real GDP

2018 Full Year Results Presentation. 31 August 2018

2018 Full Year Results Presentation 31 August 2018 Disclaimer Important Notice and Disclaimer Disclaimer The material in this presentation has been prepared by Reece Limited (ABN 49 004 313 133) ( Reece")

2018 Full Year Results Presentation 31 August 2018 Disclaimer Important Notice and Disclaimer Disclaimer The material in this presentation has been prepared by Reece Limited (ABN 49 004 313 133) ( Reece")

Future of Housing Trends and the Housing Market Demographic Waves in the Region and Future of Housing. Illinois Finance Forum January 25, 2019

Future of Housing Trends and the Housing Market Demographic Waves in the Region and Future of Housing Illinois Finance Forum January 25, 2019 Millions OUR STATE S POPULATION 2000-2017 13.0 12.4 M 12.9

Future of Housing Trends and the Housing Market Demographic Waves in the Region and Future of Housing Illinois Finance Forum January 25, 2019 Millions OUR STATE S POPULATION 2000-2017 13.0 12.4 M 12.9

The structure of the euro area recovery

The structure of the euro area recovery Rolf Strauch, Chief Economist JPMorgan Investor Seminar, IMF Annual Meetings Washington, October 2017 The euro area: a systemic player in global trade Trade openness

The structure of the euro area recovery Rolf Strauch, Chief Economist JPMorgan Investor Seminar, IMF Annual Meetings Washington, October 2017 The euro area: a systemic player in global trade Trade openness

Oakmont: Who are we?

Oakmont: Who are we? A Snapshot of our community from the April 2010 US Census Contents Age and Gender... 1 Marital Status... 2 Home Ownership and Tenure... 3 Past Demographic Characteristics... 5 Income

Oakmont: Who are we? A Snapshot of our community from the April 2010 US Census Contents Age and Gender... 1 Marital Status... 2 Home Ownership and Tenure... 3 Past Demographic Characteristics... 5 Income

Southwest Ohio Regional Economy in Context. Richard Stock, PhD. Business Research Group

Southwest Ohio Regional Economy in Context Richard Stock, PhD. Business Research Group State of the Metro Area (in January Each Year) Total Employment has slowly increased in the last three years after

Southwest Ohio Regional Economy in Context Richard Stock, PhD. Business Research Group State of the Metro Area (in January Each Year) Total Employment has slowly increased in the last three years after

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Global economy maintaining solid growth momentum. Canada leading the pack

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Cargo outlook Brian Pearce Chief Economist. 13 December 2018

Cargo outlook 2019 Brian Pearce Chief Economist 13 December 2018 % total revenues % total revenues Cargo revenue contribution stabilizing 2 82% 80% 78% 76% 74% 72% 70% 68% 66% 64% 62% Share of airlines'

Cargo outlook 2019 Brian Pearce Chief Economist 13 December 2018 % total revenues % total revenues Cargo revenue contribution stabilizing 2 82% 80% 78% 76% 74% 72% 70% 68% 66% 64% 62% Share of airlines'

Greater Portland Office Market Survey {Presented by James D. Harnden

Greater Portland Office Market Survey {Presented by James D. Harnden {Topical Agenda 2013 Office Market Highlights Downtown Sector Vacancy, significant leases/vacancies Suburban Sector Vacancy, significant

Greater Portland Office Market Survey {Presented by James D. Harnden {Topical Agenda 2013 Office Market Highlights Downtown Sector Vacancy, significant leases/vacancies Suburban Sector Vacancy, significant

Airlines, the economy and air transport demand

Airlines, the economy and air transport demand Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 Returns for airlines investors lower this year;

Airlines, the economy and air transport demand Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 Returns for airlines investors lower this year;

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

Ask a question Go to slido.com, enter #london

Ask a question Go to slido.com, enter #london THE BIG PICTURE Kevin McCauley EXECUTIVE DIRECTOR HEAD OF LONDON RESEARCH MARKET BACKGROUND LOW GROWTH, UNCERTAINTY BUT STRONG GLOBAL ECONOMY Slowing UK economic

Ask a question Go to slido.com, enter #london THE BIG PICTURE Kevin McCauley EXECUTIVE DIRECTOR HEAD OF LONDON RESEARCH MARKET BACKGROUND LOW GROWTH, UNCERTAINTY BUT STRONG GLOBAL ECONOMY Slowing UK economic

Curves On The Road Ahead

Curves On The Road Ahead Light Vehicle Market Outlook November 2018 Charles Chesbrough Senior Economist A g e n d a Economic Outlook and New Vehicle Sales Affordability Threat and the Used Vehicle Market

Curves On The Road Ahead Light Vehicle Market Outlook November 2018 Charles Chesbrough Senior Economist A g e n d a Economic Outlook and New Vehicle Sales Affordability Threat and the Used Vehicle Market

2016 Texas Prosperity Conference The Barnhill Center Brenham, Texas August 26, Dr. James P. Gaines Chief Economist. recenter.tamu.

2016 Texas Prosperity Conference The Barnhill Center Brenham, Texas August 26, 2016 Dr. James P. Gaines Chief Economist recenter.tamu.edu Housing and People 2 Texas Population 1910-2050 60,000,000 50,000,000

2016 Texas Prosperity Conference The Barnhill Center Brenham, Texas August 26, 2016 Dr. James P. Gaines Chief Economist recenter.tamu.edu Housing and People 2 Texas Population 1910-2050 60,000,000 50,000,000

FY 2017 Results Presentation Q Results Presentation. Milan, 24 th April Milan, 15 th May 2018

FY 2017 Results Presentation Milan, 24 th April 2018 2018 1Q Results Presentation Milan, 15 th May 2018 FY 2017 Results Presentation Milan, 24 th April 2018 Audience & Advertising gen-16 feb-16 mar-16

FY 2017 Results Presentation Milan, 24 th April 2018 2018 1Q Results Presentation Milan, 15 th May 2018 FY 2017 Results Presentation Milan, 24 th April 2018 Audience & Advertising gen-16 feb-16 mar-16

MUSTAFA MOHATAREM Chief Economist, General Motors

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

Aegon ISA transfer application form

For customers Aegon Platform Aegon ISA transfer application form In this form, Aegon means Cofunds Limited and I, me, my, you and your refer to the applicant named in section 1. Use this form to transfer

For customers Aegon Platform Aegon ISA transfer application form In this form, Aegon means Cofunds Limited and I, me, my, you and your refer to the applicant named in section 1. Use this form to transfer