Percent of Brokerages by Size

|

|

|

- Denis Brooks

- 5 years ago

- Views:

Transcription

1

2

3

4

5 Percent of Brokerages by Size 80% 70% 60% 58.4% 50% 40% 30% 28.7% 20% 10% 0% #: +23.6% -7.3% +9.9% 0.1% 0.1% 0.2% 0.5% 0.6% 1.8% 2.6% 1, Single Brokers %

6 Percent of Agents by Brokerage Size 16% 14% 12% 14.2% 13.1% 10.9% 12.2% 12.2% 10% 9.6% 8% 6.7% 8.3% 7.5% 6% 5.3% 4% 2% 1, % 1, Single Brokers

7

8 Transacted Dollar Volume: Twin Cities Metro (unadjusted nominal dollars) $18 $16.60 $16 $15.61 $14.89 $14 $13.80 $13.92 $12.64 $12.61 $12 $11.41 Billions $10 $9.43 $9.17 $10.35 $8 $8.15 $8.10 $6 $4 $2 $

9 Annual New Listings Twin Cities Region 120, , , ,000 88, ,039 99,627 93,362 80,000 82,876 81,813 68,851 65,874 72,026 73,650 77,380 60,000 40,000 20, % -0.4% +8.4% -2.8% -11.1% -11.2% -1.3% -15.8% -4.3% +9.3% +2.3% +5.1%

10 Annual Closed Sales Twin Cities Region 70,000 60,000 50,000 40,000 57,457 60,180 60,063 49,419 41,018 39,550 45,775 38,256 41,589 48,791 53,172 49,604 56,390 30,000 20,000 10, % -0.2% -17.7% -17.0% -3.6% +15.7% -16.4% +8.7% +17.3% +9.0% -6.7% +13.7%

11 Annual Inventory Twin Cities Region 30,000 27,609 25,000 24,439 25,585 22,659 20,000 18,711 20,801 20,613 17,453 15,000 15,139 13,034 12,698 12,997 10,000 10,166 5, % +11.2% +17.5% +13.0% -7.3% -19.4% +9.9% -23.0% -25.3% -2.6% +2.4% -21.8%

12 Annual Inventory (April) Twin Cities Region 35,000 33,104 33,290 30,000 30,308 27,763 27,946 25,000 20,000 21,074 23,964 21,644 24,356 18,579 15,000 14,222 15,341 15,930 10,000 5, % -9.7% +40.0% +9.2% +0.6% -16.6% +0.7% -12.8% -23.7% -23.5% +7.9% +3.8%

13 Annual Median Sales Price Twin Cities Region $250,000 $200,000 $199,900 $229,000$230,000 $225,000 $217,000 $195,000 $192,000 $205,600 $220,000 $150,000 $165,100 $169,900 $150,000$167, % below peak 47.0% above valley $100,000 $50, % +5.5% +0.4% -2.2% -13.3% -15.3% +2.9% -11.7% +11.9% +14.4% +7.1% +7.0% $

14 Annual Days on Market Twin Cities Region % +15.0% -5.9% -7.6% +10.5% -20.4% -29.1% -6.0% -2.6%

15 Annual Pct. of List Price Rec'd at Sale Twin Cities Region 100% 98.5% 98.6% 98.1% 98% 96% 94% 96.8% 94.7% 94.0% 96.1% 95.7% 96.6% 92.7% 92.3% 92% 91.8% 90.6% 90% 88% +0.1% -0.5% -1.3% -2.2% -3.1% +1.0% -0.4% -1.8% -0.4% +2.2% -0.4% +0.9% 86%

16 Annual Months Supply of Inventory Twin Cities Region % +8.1% +50.0% +36.7% -6.1% -29.9% +31.5% -29.6% +10.3% -9.4% +10.3% -34.4%

17 Annual Months Supply of Inventory (April) Twin Cities Region % +69.8% +31.0% +22.1% -22.0% -13.0% +16.4% -39.2% -31.8% +6.6% +0.5%

18 Seller s Market (Less than 5 MSI) Buyer s Market (More than 6 MSI) Balanced Market (5-6 MSI) Low supply, high demand Seller at a relative advantage Shorter market times More robust price appreciation Multiple offers more common Sales prices closer to asking prices High supply, low demand Buyer at a relative advantage Longer market times Relatively slower price appreciation or price declines Buyer has more power in negotiation of price Neither side has a market-wide advantage Price growth and market times in line with steady, historical norms

19 Distressed Sales Rate Share of all Closed Sales that are either Foreclosures or Shorts (Twin Cities MSA, ) 70% 65% 60% 55% 61.4% 56.9% 61.6% 56.5% 50% 45% 44.0% 40% 35% 33.9% 30% 25% 28.4% 30.4% 20% 15% 10% 17.8% 15.9% 7.5% 11.2% 5% 0%

20 New Construction Market Share Percentage of all Closed Sales that were New Construction, Twin Cities MSA 18% 16% 14.4% 14.8% 14% 12.9% 13.1% 13.1% 12% 10% 9.9% 8% 6% 7.3% 7.6% 6.1% 6.5% 7.08% 7.14% 6.3% 4% 2% 0%

21 New Construction Market Share Percentage of all Closed Sales that were New Construction, Edina 11% 10% 10.0% 9% 8.5% 8.8% 8% 7% 6% 6.3% 6.6% 5% 4% 3.4% 4.5% 4.9% 4.1% 4.0% 3% 2% 1.3% 1.7% 1.1% 1% 0%

22 Townhouse-Condo Market Share Percentage of all Closed Sales that were Townhomes or Condos, Twin Cities MSA 35% 30% 28.2% 29.7% 28.2% 25% 23.7% 25.7% 23.8% 23.3% 24.3% 24.3% 23.2% 22.9% 24.3% 23.6% 20% 15% 10% 5% 0%

23

24

25

26 Price Comparison - Assuming 5% Annual Growth Recorded ASP 5% Annual Growth $350,000 $310,576 $300,000 $279,153 $250,000 $263,178 $200,000 $150,000 $100,000 $117,

27

28 A renter making the median income in the U.S. spent 30.2 percent of her income on a median-priced apartment in the Q2-2015, compared with 29.5 percent a year earlier. The long-term average, from 1985 to 1999, was 24.4 percent. -Bloomberg 2015

29 Owners' equivalent rent (OER) is a dollar amount published by the U.S. Bureau of Labor Statistics to measure the change in implicit rent, or the amount of rent that could be paid to substitute a currently owned house for an equivalent rental property in a competitive market. This chart shows that assuming the rental stock and owner-occupied housing stock are comparable owners experienced slower cost increases than renters did.

30

31

32

33

34 Fed Monetary Policy and Mortgage Rates Federal Funds Rate 30-yr Mortgage Rate

35 Current and Projected Mortgage Rates 30-yr Mortgage Rate 30-yr Mortgage Rate Forecast 5.0% 4.6% 4.5% 4.4% 4.2% 4.0% 4.0% 3.5% 3.0%

36

37

38

39

40 Upper Midwestern Values?

41

42 How Will This Benefit you? Listing Presentations Open Houses Showings Prospecting Lead Generation/Capture Personal Marketing (You vs. Entire Market) Manage Expectations by Showcasing Market Realities Strategic, Informed Decision Making Forecasting, Extrapolation and Business Planning Identifying Growth Opportunities Segment Specialization Geographical Specialization Risk/Reward Management Foreclosures not a growth market, new construction probably is

How long will it take to sell my house? (DOM) How much of my asking price will I get? (PCT) When do I have the most options as a buyer? (INV) What s happening with new construction?")

43 Be the expert you wish to see in the market! Stats Answer Popular Questions: Is it a buyer s or seller s market? (MSI) How do property types compare? (TC vs. SF) Are prices going up or down? (MSP) How long will it take to sell my house? (DOM) How much of my asking price will I get? (PCT) When do I have the most options as a buyer? (INV) What s happening with new construction? (NC) What s happening with foreclosures in my area? (F&SS)

44 Regional Accolades (just 2015) - 1 st most livable city in the U.S. (StP) - 2 nd best state for business conditions (MN) - 1 st lowest unemployment rate of any major metro (TCs 2.9% vs. 5.0% nation) - 2 nd best downtown area in U.S. (Mpls) - 2 nd greenest city in U.S. (TCs) - 3 rd best city for 20-somethings (Mpls) - 1 st most bikable city in U.S. (Mpls) - 2 nd most bikable state in U.S. (MN) - 1 st healthiest city in U.S. (Mpls) - 2 nd highest number of Fortune 500 companies per capita (TCs) - 4 th best city for job seekers (Mpls) - 7 th most recession-recovered city in U.S. (Mpls) - 5 th best state to have a baby (MN) - 1 st best local food scene (TCs) - 2 nd highest number of theater seats per capita (Mpls) - 7 th best state for women s equality (MN) - 1 st most literate city in America (Mpls) - 3 rd best metro area for beer lovers (TCs) - 3 rd most friendly metro area (TCs but #1 nicest) - 8 th best school system school system in U.S. (MN) - 3 rd best domestic airport in U.S. (TCs) - 1 st best metro area on ParkScore Index (TCs) - 2 nd best metro area for recent graduates (TCs) - 5 th best music scene in U.S. (TCs)

45 The Global Context Economics - Energy Prices & New Construction - Threat of a Grexit when is the political theater over - Civil war in Syria harm consumer confidence? - Saudis and Iranians diplomatic crisis - US banks limited exposure to Canadian and Chinese mortgage markets - Slowing Chinese growth and non-existent Japanese growth will they try to collect our debt? - We have a lot of Fortune 500 businesses with the majority of their revenue coming from overseas - Gyrations in corporate earnings, slowing emerging market growth, etc. - Stock Market - Strong dollar U.S. consumers pay less for imports, but the world pays more for U.S. exports - Trade deficit widening - Others? Politics - A timely one: Presidential politics matter! - Interest rates? Verdict - U.S. is a shining star in the world economy - Growth may be more subdued than we d like, but another major crash/impending doom is unlikely - Risk of contagion is low for now

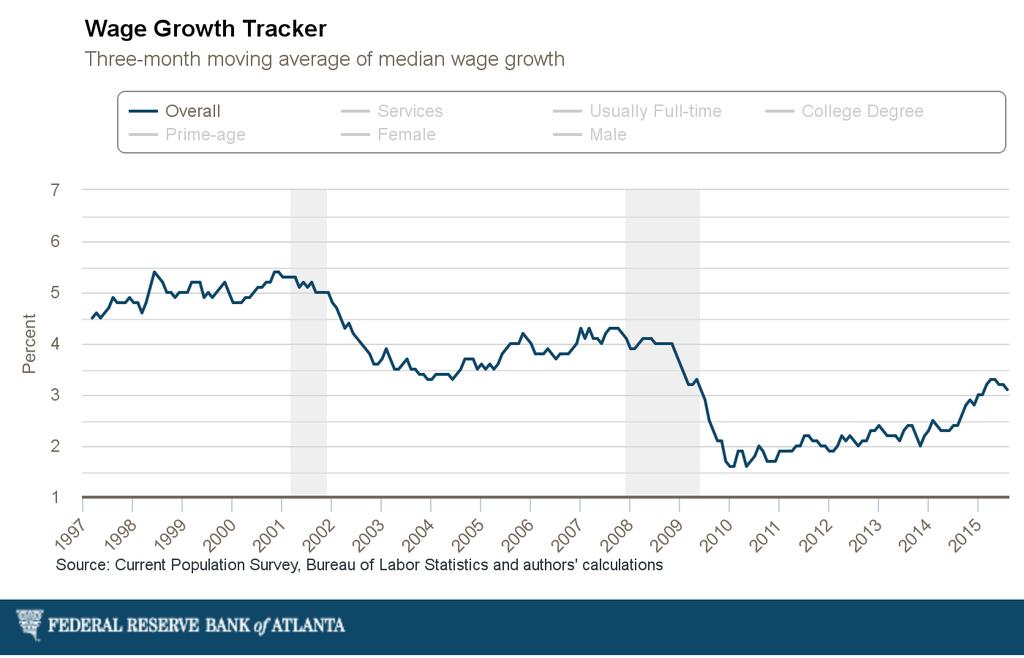

46 What s in store for 2016? 1. Seller activity up 5-7 percent 2. Buyer activity up 7-10 percent 3. For sale inventory up 3-5 percent 4. Home prices up 4-6 percent 5. Housing affordability down 1-2 percent 6. New construction up 8-10 percent 7. Interest rates up to 4.6% by end of 2016 (gradual + incremental) 8. Foreclosures down to 5-7% of Closed Sales 9. Unemployment Twin Cities < 2.3% U.S. < 4.6% 10. Job growth accelerating to 300k+ per mo 11. Wage Growth increasing to ~3-4% per yr (before inflation)

47 You Went Too Far! 10kresearch.com 47

48 Corporate Sector vs. Humans

Big Changes, Unknown Impacts

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Texas Housing Markets: Metropolitan vs. Border Communities. September 22, 2014

Texas Housing Markets: Metropolitan vs. Border Communities Luis Bernardo Torres Ruiz, Ph.D. Research Economist El Paso Branch Dallas Federal Rio Grande Economic Association September 22, 2014 Contents

Texas Housing Markets: Metropolitan vs. Border Communities Luis Bernardo Torres Ruiz, Ph.D. Research Economist El Paso Branch Dallas Federal Rio Grande Economic Association September 22, 2014 Contents

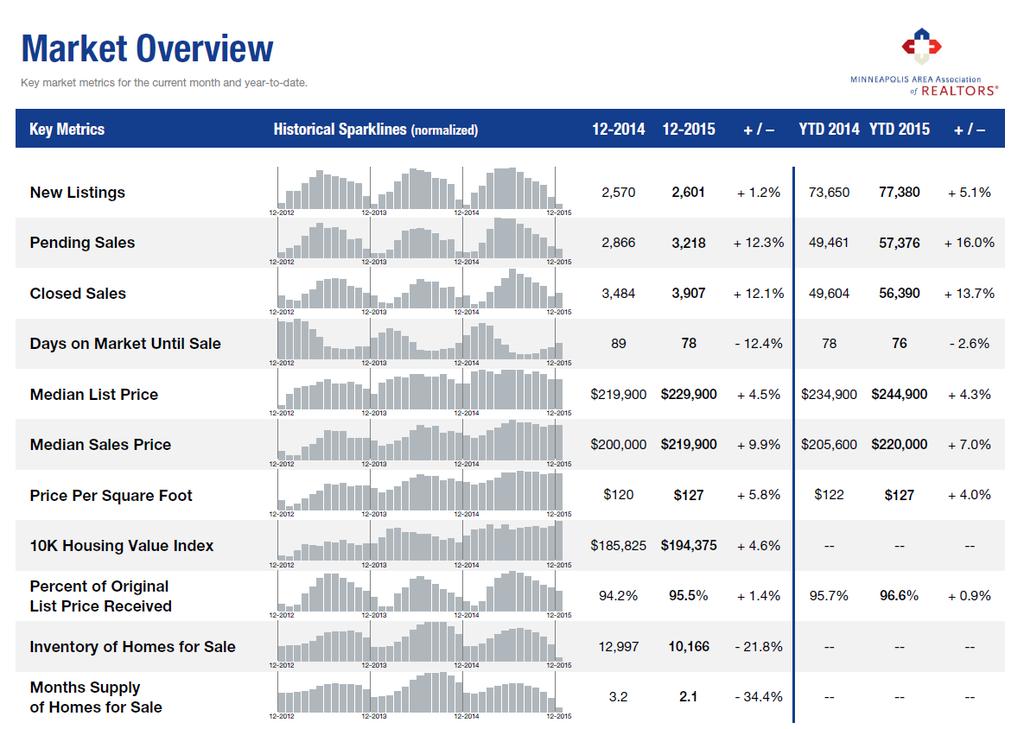

Monthly Indicators - 5.2% % % Activity Overview New Listings Pending Sales. Closed Sales. Days on Market Until Sale. Median Sales Price

Monthly Indicators 2018 Sales and new listings continue to perform well throughout the state of New York largely due to a booming U.S. economy that has increased listing and purchasing confidence. Housing

Monthly Indicators 2018 Sales and new listings continue to perform well throughout the state of New York largely due to a booming U.S. economy that has increased listing and purchasing confidence. Housing

The U.S. Economic Outlook

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

Monthly Indicators. Quick Facts - 4.5% January % + 7.9%

Monthly Indicators 2019 Despite a strong U.S. economy, historically low unemployment and steady wage growth, home sales began to slow across the nation late last year. Blame was given to a combination

Monthly Indicators 2019 Despite a strong U.S. economy, historically low unemployment and steady wage growth, home sales began to slow across the nation late last year. Blame was given to a combination

10 County Conference. Richard Wobbekind. Executive Director Business Research Division & Senior Associate Dean Leeds School of Business

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States?

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

More of the Same; Or now for Something Completely Different?

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

Economic & Financial Market Outlook

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Trends. September 10, 2013

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Muhlenkamp & Company. Webinar December 1, Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Spring Time for Housing

Spring Time for Housing Arizona State University December 2 nd, 2015 Presented By: Elliott D. Pollack CEO, IN PHOENIX 1 2 The World has Changed Pre-2007 Post-2007 3 Employment Growth From Bottom of Recession

Spring Time for Housing Arizona State University December 2 nd, 2015 Presented By: Elliott D. Pollack CEO, IN PHOENIX 1 2 The World has Changed Pre-2007 Post-2007 3 Employment Growth From Bottom of Recession

Charlotte Region Monthly Indicators

Charlotte Region Monthly Indicators A RESEARCH TOOL PROVIDED BY CHARLOTTE REGIONAL REALTOR ASSOCIATION FOR MORE INFORMATION CONTACT A REALTOR 2019 Despite a strong U.S. economy, historically low unemployment

Charlotte Region Monthly Indicators A RESEARCH TOOL PROVIDED BY CHARLOTTE REGIONAL REALTOR ASSOCIATION FOR MORE INFORMATION CONTACT A REALTOR 2019 Despite a strong U.S. economy, historically low unemployment

Monthly Indicators. Quick Facts 0.0% January % + 3.2%

Monthly Indicators 2019 Despite a strong U.S. economy, historically low unemployment and steady wage growth, home sales began to slow across the nation late last year. Blame was given to a combination

Monthly Indicators 2019 Despite a strong U.S. economy, historically low unemployment and steady wage growth, home sales began to slow across the nation late last year. Blame was given to a combination

As Good as it Gets. The Aging Expansion Powers On... but for How Much Longer? Andrew J. Nelson Chief Economist USA, Colliers International

As Good as it Gets The Aging Expansion Powers On... but for How Much Longer? Andrew J. Nelson Chief Economist USA, Colliers International #NMHCstudent @ApartmentWire Ten Years After: A Full if Imperfect

As Good as it Gets The Aging Expansion Powers On... but for How Much Longer? Andrew J. Nelson Chief Economist USA, Colliers International #NMHCstudent @ApartmentWire Ten Years After: A Full if Imperfect

Monthly Indicators - 6.4% + 8.0% - 5.3% Market Overview New Listings Pending Sales. Closed Sales. Days on Market Until Sale. Median Sales Price

Monthly Indicators 2018 The booming U.S. economy continues to prop up home sales and new listings in much of the nation, although housing affordability remains a concern. Historically, housing is still

Monthly Indicators 2018 The booming U.S. economy continues to prop up home sales and new listings in much of the nation, although housing affordability remains a concern. Historically, housing is still

Economy On The Rebound

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Annual Report on the Charlotte Region Housing Market RESIDENTIAL REAL ESTATE ACTIVITY FROM THE CHARLOTTE REGIONAL REALTOR ASSOCIATION

Annual Report on the Charlotte Region Housing Market RESIDENTIAL REAL ESTATE ACTIVITY FROM THE CHARLOTTE REGIONAL REALTOR ASSOCIATION Annual Report on the Charlotte Region Housing Market RESIDENTIAL REAL

Annual Report on the Charlotte Region Housing Market RESIDENTIAL REAL ESTATE ACTIVITY FROM THE CHARLOTTE REGIONAL REALTOR ASSOCIATION Annual Report on the Charlotte Region Housing Market RESIDENTIAL REAL

Economic Outlook for Canada: Economy Confronting Capacity Limits

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

Charlotte Region Monthly Indicators

Charlotte Region Monthly Indicators A RESEARCH TOOL PROVIDED BY CHARLOTTE REGIONAL REALTOR ASSOCIATION FOR MORE INFORMATION CONTACT A REALTOR 2018 The booming U.S. economy continues to prop up home sales

Charlotte Region Monthly Indicators A RESEARCH TOOL PROVIDED BY CHARLOTTE REGIONAL REALTOR ASSOCIATION FOR MORE INFORMATION CONTACT A REALTOR 2018 The booming U.S. economy continues to prop up home sales

A comment on recent events, and...

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

Curves On The Road Ahead

Curves On The Road Ahead Light Vehicle Market Outlook November 2018 Charles Chesbrough Senior Economist A g e n d a Economic Outlook and New Vehicle Sales Affordability Threat and the Used Vehicle Market

Curves On The Road Ahead Light Vehicle Market Outlook November 2018 Charles Chesbrough Senior Economist A g e n d a Economic Outlook and New Vehicle Sales Affordability Threat and the Used Vehicle Market

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic and Real Estate Outlook

Economic and Real Estate Outlook By Lawrence Yun, Ph.D. Chief Economist, National Association of REALTORS Presentation at Charlottesville Area Association of REALTORS October 13, 2016 1990 1991 1992 1993

Economic and Real Estate Outlook By Lawrence Yun, Ph.D. Chief Economist, National Association of REALTORS Presentation at Charlottesville Area Association of REALTORS October 13, 2016 1990 1991 1992 1993

Global economy s strong momentum intact despite elevated level of uncertainty. Canada headed for another year of solid growth

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

WHERE ARE ARIZONA DEMOGRAPHICS TAKING US? HOW GROWING SLOWER, OLDER AND MORE DIVERSE AFFECTS REAL ESTATE

WHERE ARE ARIZONA DEMOGRAPHICS TAKING US? HOW GROWING SLOWER, OLDER AND MORE DIVERSE AFFECTS REAL ESTATE March 2017 Tom Rex Office of the University Economist and Center for Competitiveness and Prosperity

WHERE ARE ARIZONA DEMOGRAPHICS TAKING US? HOW GROWING SLOWER, OLDER AND MORE DIVERSE AFFECTS REAL ESTATE March 2017 Tom Rex Office of the University Economist and Center for Competitiveness and Prosperity

National and Regional Economic Outlook. Central Southern CAA Conference

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

National and Regional Economic Outlook Central Southern CAA Conference Dr. Mira Farka & Dr. Adrian R. Fleissig California State University, Fullerton April 13, 2011 The Painfully Slow Recovery The Painfully

Monthly Indicators + 1.7% + 7.1% % Market Overview New Listings Pending Sales. Closed Sales. Days on Market Until Sale. Median Sales Price

Monthly Indicators 2018 Home prices were consistently up again in most markets in 2018 but at reduced levels compared to recent years. High demand for few homes for sale fueled price increases, but evidence

Monthly Indicators 2018 Home prices were consistently up again in most markets in 2018 but at reduced levels compared to recent years. High demand for few homes for sale fueled price increases, but evidence

The U. S. Economic Outlook: Robert J. Gordon

The U. S. Economic Outlook: Upside and Risks Robert J. Gordon Ottawa a Economics Association Ottawa, a, September 14, 2017 Immigration Medical Care My Policy Package: Be Like Canada d University Tuition

The U. S. Economic Outlook: Upside and Risks Robert J. Gordon Ottawa a Economics Association Ottawa, a, September 14, 2017 Immigration Medical Care My Policy Package: Be Like Canada d University Tuition

President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H. Parker Willis Lecture in Political Economics

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

ABA Commercial Real Estate Lending Committee

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

Babson Capital/UNC Charlotte Economic Forecast. May 13, 2014

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Wenlin Liu, Senior Economist. Stateof Wyoming. Economic Analysis Division State of Wyoming 1

WYOMING DEMOGRAPHIC AND ECONOMIC TREND LCCC LIFE Program April 7, 2012 Cheyenne, Wyoming Wenlin Liu, Senior Economist Economic Analysis Division Stateof Wyoming Economic Analysis Division State of Wyoming

WYOMING DEMOGRAPHIC AND ECONOMIC TREND LCCC LIFE Program April 7, 2012 Cheyenne, Wyoming Wenlin Liu, Senior Economist Economic Analysis Division Stateof Wyoming Economic Analysis Division State of Wyoming

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee The U.S. economy has now enjoyed 7 years of economic growth since the Great Recession Real GDP grew by 1.2% in

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee The U.S. economy has now enjoyed 7 years of economic growth since the Great Recession Real GDP grew by 1.2% in

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Economic Growth in the Trump Economy

Economic Growth in the Trump Economy Presented to State Data Center Conference William F. Fox, Director November 18, 2016 GDP Grows, Though Slowly 10.0 8.0 Percentage Change, Previous Qtr, SAAR 6.0 4.0

Economic Growth in the Trump Economy Presented to State Data Center Conference William F. Fox, Director November 18, 2016 GDP Grows, Though Slowly 10.0 8.0 Percentage Change, Previous Qtr, SAAR 6.0 4.0

Global economy maintaining solid growth momentum. Canada leading the pack

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip?

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

U.S. REITs have rebounded strongly Dow Jones Equity REIT Total Return Index

U.S. REITs have rebounded strongly Dow Jones Equity REIT Total Return Index Index, 2005 = 100 250 200 150 100 50 0 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Sources: Bloomberg, Dow Jones. Affordability

U.S. REITs have rebounded strongly Dow Jones Equity REIT Total Return Index Index, 2005 = 100 250 200 150 100 50 0 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Sources: Bloomberg, Dow Jones. Affordability

Charlotte Region Monthly Indicators

Charlotte Region Monthly Indicators A RESEARCH TOOL PROVIDED BY CHARLOTTE REGIONAL REALTOR ASSOCIATION FOR MORE INFORMATION CONTACT A REALTOR 2018 Home prices were consistently up again in most markets

Charlotte Region Monthly Indicators A RESEARCH TOOL PROVIDED BY CHARLOTTE REGIONAL REALTOR ASSOCIATION FOR MORE INFORMATION CONTACT A REALTOR 2018 Home prices were consistently up again in most markets

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office The views expressed in this presentation are strictly those of the author and do not necessarily

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office The views expressed in this presentation are strictly those of the author and do not necessarily

The Global Economy: Sustaining Momentum

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

Canada s economy on track for a solid 2018 although policy uncertainty lingers

Canada s economy on track for a solid 2018 although policy uncertainty lingers Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com March 2018 Canada is facing a challenging

Canada s economy on track for a solid 2018 although policy uncertainty lingers Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com March 2018 Canada is facing a challenging

Monthly Indicators - 9.1% + 4.5% + 8.0% Activity Overview New Listings. Closed Sales Median Sales Price

Monthly Indicators 2018 Home prices were consistently up again in most markets in 2018 but at reduced levels compared to recent years. High demand for few homes for sale fueled price increases, but evidence

Monthly Indicators 2018 Home prices were consistently up again in most markets in 2018 but at reduced levels compared to recent years. High demand for few homes for sale fueled price increases, but evidence

Economic Overview. Melissa K. Peralta Senior Economist April 27, 2017

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Old Dominion University 2017 Regional Economic Forecast. Strome College of Business

Old Dominion University 2017 Regional Economic Forecast January 25, 2017 Professor Vinod Agarwal Director, Economic Forecasting Project Strome College of Business www.odu.edu/forecasting The views expressed

Old Dominion University 2017 Regional Economic Forecast January 25, 2017 Professor Vinod Agarwal Director, Economic Forecasting Project Strome College of Business www.odu.edu/forecasting The views expressed

The US Economic Outlook

IHS ECONOMICS US Outlook The US Economic Outlook November 2014 ihs.com Rafael Amiel, Director latin America Economics +1 215 789 7405, rafael.amiel.ihs.com 2014 IHS The US economy is gaining momentum Growth

IHS ECONOMICS US Outlook The US Economic Outlook November 2014 ihs.com Rafael Amiel, Director latin America Economics +1 215 789 7405, rafael.amiel.ihs.com 2014 IHS The US economy is gaining momentum Growth

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

Agriculture and the Economy: A View from the Chicago Fed

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

The Auction Market In 2015 & 2016 Review & Forecast. Dr. Ira Silver NAAA Economist

The Auction Market In 2015 & 2016 Review & Forecast Dr. Ira Silver NAAA Economist silver@naaa.com Agenda Economic conditions Economic outlook Light vehicle sales Light vehicle sales outlook NAAA 2015 Annual

The Auction Market In 2015 & 2016 Review & Forecast Dr. Ira Silver NAAA Economist silver@naaa.com Agenda Economic conditions Economic outlook Light vehicle sales Light vehicle sales outlook NAAA 2015 Annual

Seven Lean Years Explaining Persistent Global Economic Weakness

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Percent

Outline Outline Growth is picking up Percent 6 Advanced economies Emerging and developing economies 5 4 4.9 5.0 4.3 4.4 4.6 4.7 4.7 3.7 3.7 3 2 2.0 2.3 1.6 2.2 2.3 1.9 1.7 1 1.1 1.3 0 2012 2013 2014 2015

Outline Outline Growth is picking up Percent 6 Advanced economies Emerging and developing economies 5 4 4.9 5.0 4.3 4.4 4.6 4.7 4.7 3.7 3.7 3 2 2.0 2.3 1.6 2.2 2.3 1.9 1.7 1 1.1 1.3 0 2012 2013 2014 2015

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder Member FDIC VectraBank.com Economic Outlook 2015 Richard

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder Member FDIC VectraBank.com Economic Outlook 2015 Richard

The Wisconsin and Minnesota Economies: What can we learn from each other? Noah Williams

The Economies: What can we learn from each other? Noah University of Wisconsin - Madison Future Wisconsin Summit 2016 Economies Location, size, demographics, and history make Wisconsin and Minnesota natural

The Economies: What can we learn from each other? Noah University of Wisconsin - Madison Future Wisconsin Summit 2016 Economies Location, size, demographics, and history make Wisconsin and Minnesota natural

A Primer on Factors Affecting Farmland Values

A Primer on Factors Affecting Farmland Values Federal Reserve Bank of Chicago David Oppedahl Business Economist 312-322-6122 david.oppedahl@chi.frb.org The economy hit bottom in June 2009, with hesitant

A Primer on Factors Affecting Farmland Values Federal Reserve Bank of Chicago David Oppedahl Business Economist 312-322-6122 david.oppedahl@chi.frb.org The economy hit bottom in June 2009, with hesitant

Global growth prospects

Global growth prospects Percent 6 Advanced Economies Emerging Markets and Developing Economies 5 4.9 5.0 4.7 4.7 4.5 4 4.3 4.3 3.7 3.7 3 2 2.3 2.3 2.2 2.0 2.0 1.7 1.7 1 1.1 1.3 0 2012 2013 2014 2015 2016

Global growth prospects Percent 6 Advanced Economies Emerging Markets and Developing Economies 5 4.9 5.0 4.7 4.7 4.5 4 4.3 4.3 3.7 3.7 3 2 2.3 2.3 2.2 2.0 2.0 1.7 1.7 1 1.1 1.3 0 2012 2013 2014 2015 2016

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

Will 2016 Be the Last Hurrah for Commercial Real Estate? Presented By: John Chang First Vice-President Marcus & Millichap Research Services

Will 2016 Be the Last Hurrah for Commercial Real Estate? Presented By: John Chang First Vice-President Marcus & Millichap Research Services Rising Uncertainty Creating Headwinds for Commercial Real Estate

Will 2016 Be the Last Hurrah for Commercial Real Estate? Presented By: John Chang First Vice-President Marcus & Millichap Research Services Rising Uncertainty Creating Headwinds for Commercial Real Estate

Dr. Greg Hallman Director, Real Estate Finance and Investment Center (REFIC) McCombs School of Business University of Texas at Austin

McCombs School of Business University of Texas at Austin") Dr. Greg Hallman Director, Real Estate Finance and Investment Center (REFIC) McCombs School of Business University of Texas at Austin POWERPOINT PARTNER The US Economy today, with a close look at jobs

Dr. Greg Hallman Director, Real Estate Finance and Investment Center (REFIC) McCombs School of Business University of Texas at Austin POWERPOINT PARTNER The US Economy today, with a close look at jobs

The World and U.S. Economy and San Pedro Bay Container Trade Outlook Forecast Review

The World and U.S. Economy and San Pedro Bay Container Trade Outlook Forecast Review Michael Keenan Harbor Planning and Economic Analyst Port of Los Angeles October 5, 2009 Review of 2007 Container Trade

The World and U.S. Economy and San Pedro Bay Container Trade Outlook Forecast Review Michael Keenan Harbor Planning and Economic Analyst Port of Los Angeles October 5, 2009 Review of 2007 Container Trade

Economic Outlook: fear over fundamentals

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

PHILADELPHIA HOUSE PRICE INDICES

PHILADELPHIA HOUSE PRICE INDICES April 14, 2014 KEVIN C. GILLEN, Ph.D. gillenk@upenn.edu Disclaimers and Acknowledgments: The Fels Institute of Government at the University of Pennsylvania provides this

PHILADELPHIA HOUSE PRICE INDICES April 14, 2014 KEVIN C. GILLEN, Ph.D. gillenk@upenn.edu Disclaimers and Acknowledgments: The Fels Institute of Government at the University of Pennsylvania provides this

Zions Bank Economic Overview

Zions Bank Economic Overview WIB Education Summit September 19, 2017 National Economic Conditions Dow Breaks 22,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Federal

Zions Bank Economic Overview WIB Education Summit September 19, 2017 National Economic Conditions Dow Breaks 22,000 The Trump Bump Dow Reaches New Heights Following U.S. Presidential Election Source: Federal

Zions Bank Economic Overview

Zions Bank Economic Overview Kenworth National Dealers Conference November 8, 2018 1 National Economic Conditions 2 Volatility Returns to the Stock Market 27,000 Dow Jones Industrial Average October 10,

Zions Bank Economic Overview Kenworth National Dealers Conference November 8, 2018 1 National Economic Conditions 2 Volatility Returns to the Stock Market 27,000 Dow Jones Industrial Average October 10,

Briefing on the State of the State. presented to the. SCAA Schuyler Center for Analysis and Advocacy

Briefing on the State of the State presented to the SCAA Schuyler Center for Analysis and Advocacy Rae D. Rosen Assistant Vice President Federal Reserve Bank of New York November 16, 2006 Key Points: Economic

Briefing on the State of the State presented to the SCAA Schuyler Center for Analysis and Advocacy Rae D. Rosen Assistant Vice President Federal Reserve Bank of New York November 16, 2006 Key Points: Economic

Cement & Construction Outlook

Cement & Construction Outlook Minnesota Concrete Council November 17, 2011 Dave Zwicke, PCA Analytics Manager, Sr. Economist Bottom Line Economy in a slow growth period characterized by tepid job gains.

Cement & Construction Outlook Minnesota Concrete Council November 17, 2011 Dave Zwicke, PCA Analytics Manager, Sr. Economist Bottom Line Economy in a slow growth period characterized by tepid job gains.

Monthly Indicators - 5.7% - 6.3% - 2.6% Activity Overview New Listings Pending Sales. Closed Sales. Days on Market Until Sale. Median Sales Price

Monthly Indicators 2019 Despite a strong U.S. economy, historically low unemployment and steady wage growth, home sales began to slow across the nation late last year. Blame was given to a combination

Monthly Indicators 2019 Despite a strong U.S. economy, historically low unemployment and steady wage growth, home sales began to slow across the nation late last year. Blame was given to a combination

MUSTAFA MOHATAREM Chief Economist, General Motors

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Update.

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Update February 26, 2013 The Worst Recession Since the Great Depression 0% Loss from Peak

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Update February 26, 2013 The Worst Recession Since the Great Depression 0% Loss from Peak

Frederick Ross. Real Estate Market Overview. Presented by: Kevin Thomas Senior Vice President. Frederick Ross. Company.

Frederick Ross Real Estate Market Overview Presented by: Kevin Thomas Senior Vice President Frederick Ross Company January 2003 Business Consumers Source: BEA, Ross Research Housing...Bust or Rust? 2001

Frederick Ross Real Estate Market Overview Presented by: Kevin Thomas Senior Vice President Frederick Ross Company January 2003 Business Consumers Source: BEA, Ross Research Housing...Bust or Rust? 2001

RBC Economics Financial Update Dawn Desjardins

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

The Economic Outlook. Economic Policy Division

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

The Economic Outlook Economic Policy Division Glass Half Full Six plus years of moderate growth Real GDP Outlook Percent Change, Annual Rate 10 5 0-5 -10 1980 1985 1990 1995 2000 2005 2010 2015 Glass Half

Charlotte Region Monthly Indicators

Charlotte Region Monthly Indicators A RESEARCH TOOL PROVIDED BY CHARLOTTE REGIONAL REALTOR ASSOCIATION FOR MORE INFORMATION CONTACT A REALTOR 2018 If the last few months are an indication of the temperature

Charlotte Region Monthly Indicators A RESEARCH TOOL PROVIDED BY CHARLOTTE REGIONAL REALTOR ASSOCIATION FOR MORE INFORMATION CONTACT A REALTOR 2018 If the last few months are an indication of the temperature

Charting a Path to Lift Off? Understanding the Shifting Economic Winds

Charting a Path to Lift Off? Understanding the Shifting Economic Winds Thomas F. Siems, Ph.D. Assistant Vice President and Senior Economist Federal Reserve Bank of Dallas Government Finance Officers Arlington,

Charting a Path to Lift Off? Understanding the Shifting Economic Winds Thomas F. Siems, Ph.D. Assistant Vice President and Senior Economist Federal Reserve Bank of Dallas Government Finance Officers Arlington,

Dr. James P. Gaines Research Economist recenter.tamu.edu

Texas Uncertain Economy in a World of Uncertain Oil Prices Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 U.S. Outlook Expected GDP growth still modest:

Texas Uncertain Economy in a World of Uncertain Oil Prices Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 U.S. Outlook Expected GDP growth still modest:

US imports from emerging economies have grown rapidly

US imports from emerging economies have grown rapidly Ratio to GDP (current dollars) 0.07 US merchandise imports, 1978 2008 0.06 0.05 0.04 0.03 0.02 Industrial Non-OPEC other 0.01 0 OPEC = Organization

US imports from emerging economies have grown rapidly Ratio to GDP (current dollars) 0.07 US merchandise imports, 1978 2008 0.06 0.05 0.04 0.03 0.02 Industrial Non-OPEC other 0.01 0 OPEC = Organization

U.S Cement Outlook IEEE. Ed Sullivan Group VP, Chief Economist

U.S Cement Outlook IEEE Ed Sullivan Group VP, Chief Economist 1 Construction Activity Billion Real $ 1,400 1,200 1,000 2014 = 2.5% 2015 = 5.6% 800 600 400 200 0 12 Year Peak-to- Peak Recovery 1998 2000

U.S Cement Outlook IEEE Ed Sullivan Group VP, Chief Economist 1 Construction Activity Billion Real $ 1,400 1,200 1,000 2014 = 2.5% 2015 = 5.6% 800 600 400 200 0 12 Year Peak-to- Peak Recovery 1998 2000

U.S. Economic and Apartment Market Overview and Outlook. July 15, 2014

2014 U.S. Economic and Apartment Market Overview and Outlook July 15, 2014 U.S. Economic Overview U.S. GDP Growth Persistent Despite 1Q Polar Vortex Annualized Quarterly Percent Change 10% 5% 0% -5% -10%

2014 U.S. Economic and Apartment Market Overview and Outlook July 15, 2014 U.S. Economic Overview U.S. GDP Growth Persistent Despite 1Q Polar Vortex Annualized Quarterly Percent Change 10% 5% 0% -5% -10%

PHILADELPHIA HOUSE PRICE INDICES

PHILADELPHIA HOUSE PRICE INDICES February 13, 2017 KEVIN C. GILLEN, Ph.D. Kevin.C.Gillen@Drexel.edu Disclaimers and Acknowledgments: The Lindy Institute for Urban Innovation at Drexel University provides

PHILADELPHIA HOUSE PRICE INDICES February 13, 2017 KEVIN C. GILLEN, Ph.D. Kevin.C.Gillen@Drexel.edu Disclaimers and Acknowledgments: The Lindy Institute for Urban Innovation at Drexel University provides

Trade Growth - Fundamental Driver of Port Operations and Development Strategies

Trade Growth - Fundamental Driver of Port Operations and Development Strategies Marine Terminal Management Training Program October 15, 2007 Long Beach, CA Paul Bingham Global Insight, Inc. 1 Agenda Economic

Trade Growth - Fundamental Driver of Port Operations and Development Strategies Marine Terminal Management Training Program October 15, 2007 Long Beach, CA Paul Bingham Global Insight, Inc. 1 Agenda Economic

Shifting International Trade Routes A National Economic Outlook. February 1, 2011

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

Steel: A Buyer s Market for the Worst of Reasons. John Anton Director, IHS Global Insight Steel Service August 2009

Steel: A Buyer s Market for the Worst of Reasons John Anton Director, IHS Global Insight Steel Service August 2009 The U.S. Recession Is Bottoming Out This recession has been the most severe of the postwar

Steel: A Buyer s Market for the Worst of Reasons John Anton Director, IHS Global Insight Steel Service August 2009 The U.S. Recession Is Bottoming Out This recession has been the most severe of the postwar

US Economic Outlook IHS ECONOMICS. Paul Edelstein, Director NA Financial Economics, ,

IHS ECONOMICS US Outlook US Economic Outlook How long will the ride last? September 2014 ihs.com Paul Edelstein, Director NA Financial Economics, +1 781 301 9014, paul.edelstein@ihs.com The US economy

IHS ECONOMICS US Outlook US Economic Outlook How long will the ride last? September 2014 ihs.com Paul Edelstein, Director NA Financial Economics, +1 781 301 9014, paul.edelstein@ihs.com The US economy

Carol Tomé CFO and Executive Vice President, Corporate Services

Carol Tomé CFO and Executive Vice President, Corporate Services Financial Overview December 6, 2017 1 Discussion Overview Fiscal 2017 Financial Guidance Our View of the Economy and State of the U.S. Housing

Carol Tomé CFO and Executive Vice President, Corporate Services Financial Overview December 6, 2017 1 Discussion Overview Fiscal 2017 Financial Guidance Our View of the Economy and State of the U.S. Housing

The Fed and the Economic Outlook

The Fed and the Economic Outlook Mark L. J. Wright Research Director Federal Reserve Bank of Minneapolis March 28, 2018 Disclaimer The views expressed are my own and not necessarily those of the Federal

The Fed and the Economic Outlook Mark L. J. Wright Research Director Federal Reserve Bank of Minneapolis March 28, 2018 Disclaimer The views expressed are my own and not necessarily those of the Federal

Your Texas Economy. Last updated: January 30, 2018

Your Texas Economy Last updated: January 30, 2018 Texas economy strong in 2017 2017 job growth was 2.4% Overview 2015/2016 job growth was much weaker due to the oil bust (1.3% and 1.2%, respectively) 2014

Your Texas Economy Last updated: January 30, 2018 Texas economy strong in 2017 2017 job growth was 2.4% Overview 2015/2016 job growth was much weaker due to the oil bust (1.3% and 1.2%, respectively) 2014

Alternative Measures of Economic Activity. Jan J. J. Groen, Officer Research and Statistics Group

Alternative Measures of Economic Activity Jan J. J. Groen, Officer Research and Statistics Group High School Fed Challenge Student Orientation: February 1 and 2, 217 Outline Alternative indicators: data

Alternative Measures of Economic Activity Jan J. J. Groen, Officer Research and Statistics Group High School Fed Challenge Student Orientation: February 1 and 2, 217 Outline Alternative indicators: data

Economic Outlook. Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project

Economic Outlook Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project League of California Cities Monterey, CA December 3, 2014 Economic Update economic

Economic Outlook Peter Rupert Professor and Chair Department of Economics, UCSB Director, UCSB Economic Forecast Project League of California Cities Monterey, CA December 3, 2014 Economic Update economic

The U.S. Economic Recovery: Why so weak and what should be done? William J. Crowder Ph.D.

The U.S. Economic Recovery: Why so weak and what should be done? William J. Crowder Ph.D. Weak Recovery? It s no secret that the U.S. economy has still not fully recovered from the financial crisis and

The U.S. Economic Recovery: Why so weak and what should be done? William J. Crowder Ph.D. Weak Recovery? It s no secret that the U.S. economy has still not fully recovered from the financial crisis and

2017 PNG Economic Survey. Rohan Fox (ANU), Stephen Howes (ANU), Nelson Atip Nema (UPNG), Marcel Schröder (UPNG and ANU)

, Stephen Howes (ANU), Nelson Atip Nema (UPNG), Marcel Schröder (UPNG and ANU)") 2017 PNG Economic Survey Rohan Fox (ANU), Stephen Howes (ANU), Nelson Atip Nema (UPNG), Marcel Schröder (UPNG and ANU) Introduction New government, new plan Short-term challenges: recession, falling government

2017 PNG Economic Survey Rohan Fox (ANU), Stephen Howes (ANU), Nelson Atip Nema (UPNG), Marcel Schröder (UPNG and ANU) Introduction New government, new plan Short-term challenges: recession, falling government

The Outlook for Real Estate and Residential Construction. Patrick M. Barkey, Director Bureau of Business and Economic Research University of Montana

The Outlook for Real Estate and Residential Construction Patrick M. Barkey, Director Bureau of Business and Economic Research University of Montana Montana s Real Estate Performance: Getting Back to Boom

The Outlook for Real Estate and Residential Construction Patrick M. Barkey, Director Bureau of Business and Economic Research University of Montana Montana s Real Estate Performance: Getting Back to Boom

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

Oil Prices: Past, Present, & Future

Oil Prices: Past, Present, & Future Gulf Research Center November 23, 2005 A. F. Alhajji*, PhD Gulf Energy Program - Moderator Gulf Research Center Dubai, UAE *A. F. Alhajji, PhD is also George Patten

Oil Prices: Past, Present, & Future Gulf Research Center November 23, 2005 A. F. Alhajji*, PhD Gulf Energy Program - Moderator Gulf Research Center Dubai, UAE *A. F. Alhajji, PhD is also George Patten

Dr. James P. Gaines Research Economist. recenter.tamu.edu

Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 National Issues Expected GDP growth still modest: 2015 2.5%; personal consumption 2.5% Inflation not worrisome:

Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 National Issues Expected GDP growth still modest: 2015 2.5%; personal consumption 2.5% Inflation not worrisome: