The end of the macroeconomic adjustment? Economic Department

|

|

|

- Theresa Cole

- 6 years ago

- Views:

Transcription

1 The end of the macroeconomic adjustment? Economic Department

2 Political stress and Government Yield Curve

3 Yield Curve - Brazil 0#DIJ: Yield 15,8 15,655 15,655 15,6 15,4 YC; 0#DIJ:; Trade Price; Realtime; 5Y 4M 19D; 14,428; YC; 0#DIJ:; Trade Price; Rolling(09/03/2016); 5Y 4M 19D; 14,428; YC; 0#DIJ:; Trade Price; Rolling(29/02/2016); 5Y 4M 19D; 15,655; YC; 0#DIJ:; Trade Price; Rolling(29/02/2016); 5Y 4M 19D; 15,655 22D - 5Y 4M 19D Lines: Pink 03/08/2016 Orange 03/09/2019 Blue 02/29/ , ,8 14,6 14,428 14,428 14, ,8 Auto 22D 7M 26D 1Y 4M 2Y 1M 3D 3Y 1M 7D 4Y 1M 13D 5Y 4M 19D 3

4 Structural issues

5 Structural issues - Monetary Real Interest Rate (ex-post) (% YoY) * Brazil 12,31 10,11 6,79 7,85 4,44 4,84 4,5 1,41 4,09 5,34 3,58 3,54 Chile 0,84 2,69-1,83 1,16 1,88 0,28 0,81 3,51 1,56-1,6-0,65-1,26 Mexico 4,92 2,95 3,74 1,78 0,93 0,1 0,68 0,96-0,47-1,08 0,52 0,64 Colombia 1,15 3,02 3,81 1,83 1,5-0,17 1,02 1,81 1,31 0,84-0,89-1,21 Indonesia -4,37 3,15 1,41-1,81 3,72-0,46 2,21 1,45-0,58-0,61 2,61 2,86 China 3,98 3,32 0,97 4,11 3,41 1,21 2,46 3,5 3,5 4,1 3,05 2,55 5

6 jan/08 abr/08 jul/08 out/08 jan/09 abr/09 jul/09 out/09 jan/10 abr/10 jul/10 out/10 jan/11 abr/11 jul/11 out/11 jan/12 abr/12 jul/12 out/12 jan/13 abr/13 jul/13 out/13 jan/14 abr/14 jul/14 out/14 jan/15 abr/15 jul/15 out/15 jan/16 Structural issues - Monetary Sales Value (index) Source: FIPE/ZAP, Gradual Investimentos 230,0 210,0 190,0 170,0 150,0 130,0 110,0 90,0 70,0 50,0 São Paulo Rio de Janeiro 6

7 jan/08 abr/08 jul/08 out/08 jan/09 abr/09 jul/09 out/09 jan/10 abr/10 jul/10 out/10 jan/11 abr/11 jul/11 out/11 jan/12 abr/12 jul/12 out/12 jan/13 abr/13 jul/13 out/13 jan/14 abr/14 jul/14 out/14 jan/15 abr/15 jul/15 out/15 jan/16 Structural issues - Monetary Rental Index (rent / property price) Source: FIPE/ZAP, Gradual Investimentos 0,80% 0,75% 0,70% 0,65% 0,60% 0,55% 0,50% 0,45% 0,40% 0,35% 0,30% Nacional São Paulo Rio de Janeiro 7

8 jul/40 jul/42 jul/44 jul/46 jul/48 jul/50 jul/52 jul/54 jul/56 jul/58 jul/60 jul/62 jul/64 jul/66 jul/68 jul/70 jul/72 jul/74 jul/76 jul/78 jul/80 jul/82 jul/84 jul/86 jul/88 jul/90 jul/92 jul/94 jul/96 jul/98 jul/00 jul/02 jul/04 jul/06 jul/08 jul/10 jul/12 jul/14 Structural issues - Monetary Minimum Real Wage Source: IPEA, Gradual Investimentos R$1.400,00 R$1.200,00 R$1.000,00 R$800,00 R$600,00 R$400,00 R$200,00 R$- 8

9 jul/40 jul/42 jul/44 jul/46 jul/48 jul/50 jul/52 jul/54 jul/56 jul/58 jul/60 jul/62 jul/64 jul/66 jul/68 jul/70 jul/72 jul/74 jul/76 jul/78 jul/80 jul/82 jul/84 jul/86 jul/88 jul/90 jul/92 jul/94 jul/96 jul/98 jul/00 jul/02 jul/04 jul/06 jul/08 jul/10 jul/12 jul/14 Structural issues - Monetary Minimum wage - purchasing power parity (PPP) Source: IPEA, Gradual Investimentos $350,00 $300,00 $250,00 $200,00 $150,00 $100,00 $50,00 $- 9

10 Structural issues - FISCAL Fiscal Result Source: BCB, Gradual Investimento Total revenue (R$ mi) Total expenditure (R$ mi) Primary Fiscal Result (R$ mi) 10

11 Structural issues - FISCAL Tax benefits totaled R$ 400 billion 11

12 Structural issues - FISCAL Primary surplus projected for 2015 (% of GDP) 2 Source: FMI Data Mapper, Gradual Investimentos 1, ,75-1,51-1,19-1, ,83-0,5-0, ,06-2,83-2,58-2, ,

13 Structural issues - FISCAL Gross Debt (% of GDP) (forecast for 2015) Source: FMI, Gradual Investimentos , ,9 65, ,1 50,9 48,4 44,4 43, ,9 32,1 26,5 22,4 20,4 18,1 0 13

14 Structural issues - FISCAL CPI (% YoY) Source: BCB, Gradual Investimentos 20,0% 18,0% 16,0% 14,0% 12,0% 10,0% 8,0% 6,0% 4,0% 2,0% 0,0% CPI Administered Services 14

15 Structural issues - FISCAL Nominal interests - Consolidated Public Sector R$ % 9% R$ % R$ % 6% R$ % 4% R$ % R$ % 1% R$ % Accumulated 12 months - R$ (mi) % GDP 15

16 Signs of Adjustment

17 Signs of Adjustment Industry Confidence Index - FGV Consumer Confidence Index - FGV Commerce Confidence Index - FGV Services Confidence Index - FGV 17

18 mar/03 jul/03 nov/03 mar/04 jul/04 nov/04 mar/05 jul/05 nov/05 mar/06 jul/06 nov/06 mar/07 jul/07 nov/07 mar/08 jul/08 nov/08 mar/09 jul/09 nov/09 mar/10 jul/10 nov/10 mar/11 jul/11 nov/11 mar/12 jul/12 nov/12 mar/13 jul/13 nov/13 mar/14 jul/14 nov/14 mar/15 jul/15 nov/15 Signs of Adjustment Average Real Income (% YoY) Source: IBGE, Gradual Investimentos 20,00% 15,00% 10,00% 5,00% 0,00% -5,00% -10,00% -15,00% -20,00% Rendimento Médio Real Rendimento Médio Real - com carteira Rendimento Médio Real - sem carteira 18

19 Signs of Adjustment Currencies (index) (100=01/01/2004) Yen Euro Mexican Peso Swiss Franc Brazillian Real 19

20 dez/95 jul/96 fev/97 set/97 abr/98 nov/98 jun/99 jan/00 ago/00 mar/01 out/01 mai/02 dez/02 jul/03 fev/04 set/04 abr/05 nov/05 jun/06 jan/07 ago/07 mar/08 out/08 mai/09 dez/09 jul/10 fev/11 set/11 abr/12 nov/12 jun/13 jan/14 ago/14 mar/15 out/15 Signs of Adjustment Direct Investment in Brazil (US $ mi) (12 months) Source: BCB, Gradual Investimentos R$ ,00 R$ ,00 R$ ,00 R$ ,00 R$80.000,00 R$60.000,00 R$40.000,00 R$20.000,00 R$- NET Income Outcome 20

21 Cenário - Internacional Monetary War

22 Monetary War Assets of the central banks (US $ billion) $ $ $8.000 $6.000 $4.000 $2.000 $0 jan-05 jan-06 jan-07 jan-08 jan-09 jan-10 jan-11 jan-12 jan-13 jan-14 jan-15 FED BOJ BCE Total Source: Bloomberg, Gradual Investimentos. 22

23 Monetary War Yield 2 years bonds (%YoY) jan-07 jan-08 jan-09 jan-10 jan-11 jan-12 jan-13 jan-14 jan-15-1 Germany USA Italy Spain Source: Bloomberg, Gradual Investimentos. 23

24 Monetary War Yield 10 years bonds (%YoY) USA Germany Source: Bloomberg, Gradual Investimentos. 24

25 Monetary War PIB chinês (% a.a.) Fonte: Thomson Reuters, Gradual Investimento

26 Monetary War Exportações Chinesas (em US$ bi) Fonte: Thomson Reuters, Gradual Investimentos Exportações (em US$ bi) MM12 26

27 Monetary War Reservas Internacionais - China (em US$ bi) Fonte: Thomson Reuters, Gradual Investimentos

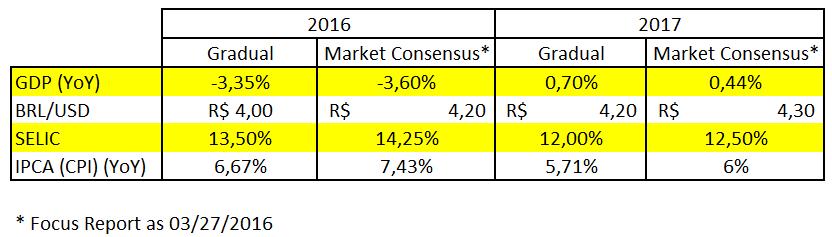

28 Forecasts end of the period

29 29

30 Contacts Economic Department André Perfeito, chief economist Rafael Gonçalves Ouvidoria/SAC:

31 DISCLAIMER This report was prepared by Gradual Investimentos and is distributed free of charge for the sole purpose of providing information to the market. Gradual Investimentos does not have any connection with any person that act in the scope of the analyzed companies or economic scenarios. The company does not receive for the services provided nor has business/commercial relationships with the companies analyzed. Although it has been taken all the necessary care in order to assure all the information at the time, its precision and accuracy are not guaranteed and Gradual Investimentos are not responsible for them. The prices, opinions and forecasts contained in this report are subject to change at any time without prior notice or announcement. This report might not be interpreted as a suggestions to buy or sell any assets or securities. The report may not be reproduced, distributed or published by any person for any purpose.

Market Insights. June 30, 2018

June 30, 2018 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.7% 1.2% 1.3% 2.1% 2.3% 1.7% 2.3%

June 30, 2018 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.7% 1.2% 1.3% 2.1% 2.3% 1.7% 2.3%

Market Insights. March 29, 2019

March 29, 2019 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.2% 1.4% 2.1% 2.3% 1.7% 2.4% 2.3%

March 29, 2019 Economic Overview 2 Global & Regional Growth Forecasts IMF GDP Forecasts (% change YoY) 2010 2011 2012 2013 2014 2015 2016 2017 2018 Advanced Economies 1.2% 1.4% 2.1% 2.3% 1.7% 2.4% 2.3%

BRAZIL MACROECONOMIC OUTLOOK: ECONOMY STABILIZATION AND LOOKING FOR REFORMS

BRAZIL MACROECONOMIC OUTLOOK: ECONOMY STABILIZATION AND LOOKING FOR REFORMS 1 Economic Research Department October, 2016 PRIMARY SURPLUS AS % OF GDP 5,0% 4,0% 3,0% 2,0% 3,7% 3,2% 3,2% 3,3% 1,9% 2,6% 2,9%

BRAZIL MACROECONOMIC OUTLOOK: ECONOMY STABILIZATION AND LOOKING FOR REFORMS 1 Economic Research Department October, 2016 PRIMARY SURPLUS AS % OF GDP 5,0% 4,0% 3,0% 2,0% 3,7% 3,2% 3,2% 3,3% 1,9% 2,6% 2,9%

GLOBAL ECONOMICS, REAL ESTATE PRICING & OUTLOOK FOR 2017 RICHARD BARKHAM GLOBAL CHIEF ECONOMIST

GLOBAL ECONOMICS, REAL ESTATE PRICING & OUTLOOK FOR 2017 RICHARD BARKHAM GLOBAL CHIEF ECONOMIST BREXIT TRUMPISM EURO-TRUMPISM 4 ECONOMICS, PRICING & OUTLOOK FOR 2017 LET S GET GEOPOLITICS IN PERSPECTIVE

GLOBAL ECONOMICS, REAL ESTATE PRICING & OUTLOOK FOR 2017 RICHARD BARKHAM GLOBAL CHIEF ECONOMIST BREXIT TRUMPISM EURO-TRUMPISM 4 ECONOMICS, PRICING & OUTLOOK FOR 2017 LET S GET GEOPOLITICS IN PERSPECTIVE

Airlines, the economy and air transport demand

Airlines, the economy and air transport demand Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 Returns for airlines investors lower this year;

Airlines, the economy and air transport demand Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 Returns for airlines investors lower this year;

BRAZIL MACROECONOMIC OUTLOOK: INCREDIBLE MOMENT OF A POLITICAL CRISIS BUT WE CANNOT JEOPARDIZE THIS CRISIS

BRAZIL MACROECONOMIC OUTLOOK: INCREDIBLE MOMENT OF A POLITICAL CRISIS BUT WE CANNOT JEOPARDIZE THIS CRISIS 1 Economic Research Department April, 2016 WHY IS THE FISCAL POLICY SO CHALLENGING? Political

BRAZIL MACROECONOMIC OUTLOOK: INCREDIBLE MOMENT OF A POLITICAL CRISIS BUT WE CANNOT JEOPARDIZE THIS CRISIS 1 Economic Research Department April, 2016 WHY IS THE FISCAL POLICY SO CHALLENGING? Political

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip?

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Opportunities in a Challenging Global Business Environment: Can the World Avoid a Double-Dip? Ross DeVol Chief Research Officer (310) 570 4615 rdevol@milkeninstitute.org www.milkeninstitute.org Presentation

Economic & Financial Market Outlook

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

Economic & Financial Market Outlook BC Pension Forum March 1, 2013 Chris Lawless, Chief Economist Overview Global forces Recent economic performance ~ US, Europe, Japan, China ~ Other emerging markets

Colombia: Economic Adjustment and Outlook. Andres-Mauricio Velasco Technical Deputy Minister of Finance, Republic of Colombia February 2018

Colombia: Economic Adjustment and Outlook Andres-Mauricio Velasco Technical Deputy Minister of Finance, Republic of Colombia February 2018 What is Colombian Ministry of Finance s outlook and funding strategies

Colombia: Economic Adjustment and Outlook Andres-Mauricio Velasco Technical Deputy Minister of Finance, Republic of Colombia February 2018 What is Colombian Ministry of Finance s outlook and funding strategies

SA economic review Kevin Lings. August 2018

SA economic review Kevin Lings August 2018 South Africa real GDP growth year-on-year %y/y 8 7 6 5 Ave 4.3% 4 Ave 2.5% 3 2 Ave 0.9% 1 0-1 -2-3 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 2

SA economic review Kevin Lings August 2018 South Africa real GDP growth year-on-year %y/y 8 7 6 5 Ave 4.3% 4 Ave 2.5% 3 2 Ave 0.9% 1 0-1 -2-3 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 2

Economic Outlook for Canada: Economy Confronting Capacity Limits

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

Reading the Tea Leaves: Investing for 2010 and Beyond

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

Reading the Tea Leaves: Investing for 2010 and Beyond Wednesday, April 28, 2010; 8:00 AM - 9:15 AM Moderator: Maria Bartiromo, Anchor, CNBC's Closing Bell With Maria Bartiromo Speakers: Nick Calamos, President

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

Outline. Overview of globalization. Global outlook for real economic activity & inflation. Risks to the outlook

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

2017 International Economic Outlook Everett Grant Research Economist Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas October 2017 The views expressed are those of the author and

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States?

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

The Israeli Economy 2009 The Caesarea Center Conference

The Israeli Economy 2009 The Caesarea Center Conference Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

The Israeli Economy 2009 The Caesarea Center Conference Provost, Interdisciplinary Center (IDC) Herzliya The Big Issues The broken crystal ball A crisis that happens once in 100 years From a country oriented

Economic Outlook March Economic Policy Division

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Economic Outlook March 212 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly, Q1 197 to Q4 211 Real

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition May 7 and 8, 2013 İstanbul, Turkey Outline 1 The Financial System 2 Weak Growth 3 4 5 Unprecedented

Financial Stability Implications of Changing Global Finance: Policy Panel Global Finance in Transition May 7 and 8, 2013 İstanbul, Turkey Outline 1 The Financial System 2 Weak Growth 3 4 5 Unprecedented

The outlook: what we know, the known unknowns and the unknown unknowns

The outlook: what we know, the known unknowns and the unknown unknowns 24 April 2017 Seoul Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1

The outlook: what we know, the known unknowns and the unknown unknowns 24 April 2017 Seoul Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1

Muhlenkamp & Company. Webcast August 30, Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President

Muhlenkamp & Company Webcast August 30, 2018 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Muhlenkamp & Company Webcast August 30, 2018 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Canada s economy on track for a solid 2018 although policy uncertainty lingers

Canada s economy on track for a solid 2018 although policy uncertainty lingers Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com March 2018 Canada is facing a challenging

Canada s economy on track for a solid 2018 although policy uncertainty lingers Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com March 2018 Canada is facing a challenging

RBC Economics Financial Update Dawn Desjardins

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

RBC Economics Financial Update Dawn Desjardins CICA/RBC Q4 2011 Business Monitor Economic Results Overview Business and Economic Optimism Begin to Stablize 100 % 80 % 60 % 40 % 20 % 0 % National Optimism

Alloy Production Is Brazil Back Online?

Alloy Production Is Brazil Back Online? Singapore, March 23 rd, 2016 No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means electronic,

Alloy Production Is Brazil Back Online? Singapore, March 23 rd, 2016 No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means electronic,

RISI EUROPEAN CONFERENCE. (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last?

The European Economy Things look good just now. Can this last?") RISI EUROPEAN CONFERENCE (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last? Andrea Boltho Magdalen College University of Oxford and Oxford Economics CONCLUSIONS OF

RISI EUROPEAN CONFERENCE (Barcelona, 6 March 2018) The European Economy Things look good just now. Can this last? Andrea Boltho Magdalen College University of Oxford and Oxford Economics CONCLUSIONS OF

Composition of Federal Spending

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

*For Institutional Use Only* Demographic and Economic Trends: Growth, Debt and Promises Douglas C. Robinson RCM Robinson Capital Management LLC SEC Registered Investment Advisory Firm Advisory services

After the British referendum

Future of Europe After the British referendum Broader issues for the UK and the EU David Marsh, Managing Director, OMFIF 27 October 2016 Nicosia 1 European politics moves against integration A new phase

Future of Europe After the British referendum Broader issues for the UK and the EU David Marsh, Managing Director, OMFIF 27 October 2016 Nicosia 1 European politics moves against integration A new phase

2008 : Global economy and its effects on Brazilian markets

HSBC Investments 2008 : Global economy and its effects on Brazilian markets March, 2007 Scenario Review Summary: Key performance drivers and risks Real improvement in fundamentals: Superior growth prospects

HSBC Investments 2008 : Global economy and its effects on Brazilian markets March, 2007 Scenario Review Summary: Key performance drivers and risks Real improvement in fundamentals: Superior growth prospects

The Global Economy: Sustaining Momentum

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

The Global Economy: Sustaining Momentum David J. Stockton Senior Fellow Peterson Institute for International Economics Chief Economist Monetary Policy Analytics October 5, 2017 What s Driving the Global

BrazilianStatesFiscal Sustainability

BrazilianStatesFiscal Sustainability VII Jornada Iberoamericana de Financiación Local Cartagena, Colombia(Sept-2018) Guilherme Tinoco, Economic Research Department guilherme.tinoco@bndes.gov.br The views

BrazilianStatesFiscal Sustainability VII Jornada Iberoamericana de Financiación Local Cartagena, Colombia(Sept-2018) Guilherme Tinoco, Economic Research Department guilherme.tinoco@bndes.gov.br The views

Global growth forecasts Key countries/regions,

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

Global growth forecasts Key countries/regions, 2014-2018 Percent 7 6 5 4 3 2 1 0 Developing Asia Sub-Saharan Africa Middle East and North Africa Latin America and the Caribbean United States Euro area

MUSTAFA MOHATAREM Chief Economist, General Motors

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

Outlook for growth, traffic and airline profits

Outlook for growth, traffic and airline profits Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 50 = no change in output expected Widespread

Outlook for growth, traffic and airline profits Brian Pearce, Chief Economist, IATA www.iata.org/economics Airline Industry Economics Advisory Workshop 2016 1 50 = no change in output expected Widespread

Macro-economic risk and the outlook for aviation

Macro-economic risk and the outlook for aviation 25 th January 2018, Dublin Brian Pearce, Chief Economist, IATA www.iata.org/economics Macro matters 24% 20% Global GDP and RPK growth 12% 10% 16% 12% 8%

Macro-economic risk and the outlook for aviation 25 th January 2018, Dublin Brian Pearce, Chief Economist, IATA www.iata.org/economics Macro matters 24% 20% Global GDP and RPK growth 12% 10% 16% 12% 8%

Muhlenkamp & Company. Webinar December 1, Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Muhlenkamp & Company Webinar December 1, 2016 Ron Muhlenkamp, Portfolio Manager Jeff Muhlenkamp, Portfolio Manager Tony Muhlenkamp, President Muhlenkamp & Company, Inc. Intelligent Investment Management

Global economy maintaining solid growth momentum. Canada leading the pack

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

sector: recent developments VÍTOR CONSTÂNCIO

The economy and the banking sector: recent developments VÍTOR CONSTÂNCIO January 2006 Recent performance of the economy and prospects Factors behind the period of slow growth Challenges to the Banking

The economy and the banking sector: recent developments VÍTOR CONSTÂNCIO January 2006 Recent performance of the economy and prospects Factors behind the period of slow growth Challenges to the Banking

Global Economic Outlook

Global Economic Outlook Mark A. Wynne Vice President & Associate Director of Research Director, Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas Presentation to Vistas Conference

Global Economic Outlook Mark A. Wynne Vice President & Associate Director of Research Director, Globalization & Monetary Policy Institute Federal Reserve Bank of Dallas Presentation to Vistas Conference

Economic Overview. Melissa K. Peralta Senior Economist April 27, 2017

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

From Recession to Recovery

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

Global trade: how does it look?

Edmonton, December 2018 Global trade: how does it look? Marie-France Paquet The Office of the Chief Economist Global Affairs Canada Overview 1. Canadian economy at a glance 2. Provincial economy at a glance

Edmonton, December 2018 Global trade: how does it look? Marie-France Paquet The Office of the Chief Economist Global Affairs Canada Overview 1. Canadian economy at a glance 2. Provincial economy at a glance

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD?

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD? FROM BUST TO BOOM. AN EPIC BUST After 16 years of growth with a short pause for breath in 2002, the Icelandic economy entered

THE ICELANDIC ECONOMY AN IMPRESSIVE RECOVERY BUT WHAT CHALLENGES LIE AHEAD? FROM BUST TO BOOM. AN EPIC BUST After 16 years of growth with a short pause for breath in 2002, the Icelandic economy entered

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Turkey: Recent Developments and Future Prospects. ISBANK Economic Research Division November 2018

Turkey: Recent Developments and Future Prospects ISBANK Economic Research Division November 2018 Macroeconomic Outlook Strong Economic Growth Cycle GDP of 851 bn USD (2017), 10.6k USD (2017) per capita

Turkey: Recent Developments and Future Prospects ISBANK Economic Research Division November 2018 Macroeconomic Outlook Strong Economic Growth Cycle GDP of 851 bn USD (2017), 10.6k USD (2017) per capita

A Giant Producer, & An Emerging Giant Consumer/Investor. Hong Liang

A Giant Producer, & An Emerging Giant Consumer/Investor China s Role in Global Trade and Investment Hong Liang Chief Economist, Head of Research October, 2016 I China: A global manufacturing power house,

A Giant Producer, & An Emerging Giant Consumer/Investor China s Role in Global Trade and Investment Hong Liang Chief Economist, Head of Research October, 2016 I China: A global manufacturing power house,

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes. Tom Rogers. Lead Economist, Oxford Economics.

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

Global Economic Outlook: From Fiscal Cliff to Rushcliffe in 15 minutes Tom Rogers Lead Economist, Oxford Economics trogers@oxfordeconomics.com 16 th January 2013 Overview External environment showing signs

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

A comment on recent events, and...

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

Airline industry outlook 2019

Airline industry outlook 2019 Brian Pearce Chief Economist 12 December 2018 Million barrels a day US$ per barrel Are the markets signalling recession ahead? 60 55 Business confidence (left scale) FTSE

Airline industry outlook 2019 Brian Pearce Chief Economist 12 December 2018 Million barrels a day US$ per barrel Are the markets signalling recession ahead? 60 55 Business confidence (left scale) FTSE

Seven Lean Years Explaining Persistent Global Economic Weakness

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

Seven Lean Years Explaining Persistent Global Economic Weakness 9 June 2015 Bank of Canada and European Central Bank Conference Tim Lane Deputy Governor Bank of Canada The global economy remains weak and

FY 2017 Results Presentation Q Results Presentation. Milan, 24 th April Milan, 15 th May 2018

FY 2017 Results Presentation Milan, 24 th April 2018 2018 1Q Results Presentation Milan, 15 th May 2018 FY 2017 Results Presentation Milan, 24 th April 2018 Audience & Advertising gen-16 feb-16 mar-16

FY 2017 Results Presentation Milan, 24 th April 2018 2018 1Q Results Presentation Milan, 15 th May 2018 FY 2017 Results Presentation Milan, 24 th April 2018 Audience & Advertising gen-16 feb-16 mar-16

The Mystery of Growing Foreign Exchange Reserve

The Mystery of Growing Foreign Exchange Reserve January - March 2007 Total increase = $136 Billion Trade surplus 34% To be explained 54% Net FDI inflow 12% Source: PBoC Renminbi Pressure Indicator Initial

The Mystery of Growing Foreign Exchange Reserve January - March 2007 Total increase = $136 Billion Trade surplus 34% To be explained 54% Net FDI inflow 12% Source: PBoC Renminbi Pressure Indicator Initial

Capitalizing on the Opportunity in Emerging Markets

Capitalizing on the Opportunity in Emerging Markets Philippe Langham, Head, Emerging Markets Equities & Senior Portfolio Manager January 2017 RBC Global Asset Management (UK) Ltd. Rising Importance of

Capitalizing on the Opportunity in Emerging Markets Philippe Langham, Head, Emerging Markets Equities & Senior Portfolio Manager January 2017 RBC Global Asset Management (UK) Ltd. Rising Importance of

Dick Vos Senior Manager Research & Strategy

Dick Vos Senior Manager Research & Strategy! House prices now falling at fastest rate since early 1990s House prices will fall 7% in 'uncertain' market IMF warns on global house prices House prices Through

Dick Vos Senior Manager Research & Strategy! House prices now falling at fastest rate since early 1990s House prices will fall 7% in 'uncertain' market IMF warns on global house prices House prices Through

Grasshoppers, Ants and Locusts: the future of the world economy

Ralph Miliband Series on the Restructuring of World Power Grasshoppers, Ants and Locusts: the future of the world economy Martin Wolf Associate editor and chief economics commentator, Financial Times Professor

Ralph Miliband Series on the Restructuring of World Power Grasshoppers, Ants and Locusts: the future of the world economy Martin Wolf Associate editor and chief economics commentator, Financial Times Professor

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION

OXYGEN EVENTS CONFERENCE GALA PERFORMANCE 2017 MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION - THE CASE OF ROMANIA - Ph.D. Andrei RĂDULESCU Senior Economist, Banca Transilvania Researcher, Institute

OXYGEN EVENTS CONFERENCE GALA PERFORMANCE 2017 MONETARY AND FISCAL POLICIES DURING THE NEXT RECESSION - THE CASE OF ROMANIA - Ph.D. Andrei RĂDULESCU Senior Economist, Banca Transilvania Researcher, Institute

Car Production. Brazil Mexico. Production in thousands. Source: AMIA Asociacion Mexicana de la industria automotriz.

Car Production Production in thousands 4000 3000 2000 1000 Brazil Mexico 0 2013 2014 2015 Source: AMIA Asociacion Mexicana de la industria automotriz. Mexico s Expanding Middle Class Percent of population

Car Production Production in thousands 4000 3000 2000 1000 Brazil Mexico 0 2013 2014 2015 Source: AMIA Asociacion Mexicana de la industria automotriz. Mexico s Expanding Middle Class Percent of population

Economic Outlook: fear over fundamentals

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

ECONOMICS I RESEARCH Economic Outlook: fear over fundamentals April 2016 Craig Wright (SVP & Chief Economist) (416) 974-7457 craig.wright@rbc.com Volatility index Market volatility index, (VIX) 90 80 70

2016 1H Results Presentation. Milan, 28 th July 2016

2016 1H Results Presentation Milan, 28 th July 2016 Broadcasting & Advertising ITALY 1H 2016 Macro-economic indicators GDP & HH EXPENDITURE y.o.y growth rate, Source: ISTAT GOOD & SERVICE CONSUMPTION y.o.y

2016 1H Results Presentation Milan, 28 th July 2016 Broadcasting & Advertising ITALY 1H 2016 Macro-economic indicators GDP & HH EXPENDITURE y.o.y growth rate, Source: ISTAT GOOD & SERVICE CONSUMPTION y.o.y

Prowess Investment Managers

gathering clouds: South Africa's economic situation and how it affects you Kelebogile Moloko Prowess Investment Managers what to expect ~ how to identify a recession ~ what are the implications for South

gathering clouds: South Africa's economic situation and how it affects you Kelebogile Moloko Prowess Investment Managers what to expect ~ how to identify a recession ~ what are the implications for South

Global economy s strong momentum intact despite elevated level of uncertainty. Canada headed for another year of solid growth

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

ECONOMICS I RESEARCH Global economy s strong momentum intact despite elevated level of uncertainty Canada headed for another year of solid growth Dawn Desjardins (Deputy Chief Economist) (416) 974-6919

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Macroeconomic Research and Statistics Department Vol. XVIl, No.3 March 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02 Table

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Macroeconomic Research and Statistics Department Vol. XVIl, No.3 March 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02 Table

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.9 September 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.9 September 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

DECLINE IN COMMODITY PRICES GCC OUTLOOK NOVEMBER 22 ND, 2015

DECLINE IN COMMODITY PRICES GCC OUTLOOK NOVEMBER 22 ND, 2015 1 EVERYONE HAS A PLAN UNTIL THEY GET PUNCHED IN THE FACE 2 HE WHO IS NOT COURAGEOUS ENOUGH TO TAKE RISKS WILL ACCOMPLISH NOTHING IN LIFE 3 IT

DECLINE IN COMMODITY PRICES GCC OUTLOOK NOVEMBER 22 ND, 2015 1 EVERYONE HAS A PLAN UNTIL THEY GET PUNCHED IN THE FACE 2 HE WHO IS NOT COURAGEOUS ENOUGH TO TAKE RISKS WILL ACCOMPLISH NOTHING IN LIFE 3 IT

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.11 November 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

ROYAL MONETARY AUTHORITY OF BHUTAN MONTHLY STATISTICAL BULLETIN Department of Macroeconomic Research and Statistics Vol. XVIl, No.11 November 2018 CONTENTS Preface....01 Bhutan s Key Economic Indicators..02

Chief Economist s Report

Chief Economist s Report 22 February 2017 IATA Legal Symposium, Washington Brian Pearce Chief Economist, IATA Airline Industry Economics Advisory Workshop 2016 1 Themes 1. World economy still stuck on

Chief Economist s Report 22 February 2017 IATA Legal Symposium, Washington Brian Pearce Chief Economist, IATA Airline Industry Economics Advisory Workshop 2016 1 Themes 1. World economy still stuck on

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks. Business Research Division Leeds School of Business

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks Presented by the Business Research Division Leeds School of Business University of Colorado at Boulder U.S. Economic

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks Presented by the Business Research Division Leeds School of Business University of Colorado at Boulder U.S. Economic

Mexico Stands to Benefit From. With Relative Ease. Jesus Cañas Federal Reserve Bank of Dallas Laredo, Texas May 2014

Mexico Stands to Benefit From With Relative Ease Jesus Cañas Federal Reserve Bank of Dallas Laredo, Texas May 2014 Outline 2013 worst than expected Economy back on growth track in 2014 Why we care about

Mexico Stands to Benefit From With Relative Ease Jesus Cañas Federal Reserve Bank of Dallas Laredo, Texas May 2014 Outline 2013 worst than expected Economy back on growth track in 2014 Why we care about

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

The U.S. & Global Economic Outlook Greg Ip, U.S. Economics Editor, The Economist Remarks to The American Sportfishing Association Hilton Head, S.C. Oct. 9, 2012 How We Got Here Great Moderation = More

The U.S. & World Economy: The Good, the Bad, and the Ugly

The U.S. & World Economy: The Good, the Bad, and the Ugly Michael Strauss Chief Economist and Chief Investment Strategist Commonfund October 16, 2012 The U.S. & World Economy: The Good, the Bad, and the

The U.S. & World Economy: The Good, the Bad, and the Ugly Michael Strauss Chief Economist and Chief Investment Strategist Commonfund October 16, 2012 The U.S. & World Economy: The Good, the Bad, and the

Presentation from the USDA Agricultural Outlook Forum 2017

Presentation from the USDA Agricultural Outlook Forum 2017 United States Department of Agriculture 93 rd Annual Agricultural Outlook Forum A New Horizon: The Future of Agriculture February 23-24, 2017

Presentation from the USDA Agricultural Outlook Forum 2017 United States Department of Agriculture 93 rd Annual Agricultural Outlook Forum A New Horizon: The Future of Agriculture February 23-24, 2017

Big Changes, Unknown Impacts

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H. Parker Willis Lecture in Political Economics

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

The U.S. Economic Outlook Chartspresented by WilliamC Dudley Charts presented by William C. Dudley President and Chief Executive Officer Federal Reserve Bank of New York Washington and Lee University H.

Future Global Trade Trends - Risks & Opportunities. Pulse of the Ports: Peak Season Forecast March 21, 2013

1 Future Global Trade Trends - Risks & Opportunities Pulse of the Ports: Peak Season Forecast March 21, 2013 June 2012 Dr. Walter Kemmsies Chief Economist Summary Higher economic growth in 2013, possible

1 Future Global Trade Trends - Risks & Opportunities Pulse of the Ports: Peak Season Forecast March 21, 2013 June 2012 Dr. Walter Kemmsies Chief Economist Summary Higher economic growth in 2013, possible

Forecast evaluation report Robert Chote Chairman

Forecast evaluation report 2017 Robert Chote Chairman Background to the FER The FER is an annual report looking at the performance of past EFO forecasts against the latest outturn data Rationale Accountability

Forecast evaluation report 2017 Robert Chote Chairman Background to the FER The FER is an annual report looking at the performance of past EFO forecasts against the latest outturn data Rationale Accountability

FINANCIAL ANALYSIS. Stoby

FINANCIAL ANALYSIS Stoby INVESTMENTS AND FINANCING Investments planned over the period : Investments 2018 2019 2020 2021 Intangible assets Company creation 1 500 Web platform development 8 290 Accounting

FINANCIAL ANALYSIS Stoby INVESTMENTS AND FINANCING Investments planned over the period : Investments 2018 2019 2020 2021 Intangible assets Company creation 1 500 Web platform development 8 290 Accounting

Inside Brazil: The Leading Auto Manufacturers and Suppliers. Augusto Amorim

Inside Brazil: The Leading Auto Manufacturers and Suppliers Augusto Amorim Brazil Beyond Soccer and Carnival World Soccer Cup winner five times World s most popular Carnival World s 6th largest light vehicle

Inside Brazil: The Leading Auto Manufacturers and Suppliers Augusto Amorim Brazil Beyond Soccer and Carnival World Soccer Cup winner five times World s most popular Carnival World s 6th largest light vehicle

It Was Never Going To Be Easy

It Was Never Going To Be Easy Stephen Toplis, Head of Research July 2010 Introduction Global power shift sustained Average outlook on the improve Fiscal constraints binding Domestic rebalance under way

It Was Never Going To Be Easy Stephen Toplis, Head of Research July 2010 Introduction Global power shift sustained Average outlook on the improve Fiscal constraints binding Domestic rebalance under way

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Trends. September 10, 2013

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Babson Capital/UNC Charlotte Economic Forecast. May 13, 2014

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

The Shifts and the Shocks Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

The Shifts and the Shocks Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times Peterson Institute for International Economics 9 th October 2014 Washington DC The Shifts and the

The Shifts and the Shocks Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times Peterson Institute for International Economics 9 th October 2014 Washington DC The Shifts and the

National Transfer Accounts in Mexico

National Transfer Accounts in Mexico Policy implications: labor market Iván Mejía Guevara imejiag@stanford.edu Stanford University 12th Global Meeting of the NTA Network, Mexico City, July 23-27, 2018

National Transfer Accounts in Mexico Policy implications: labor market Iván Mejía Guevara imejiag@stanford.edu Stanford University 12th Global Meeting of the NTA Network, Mexico City, July 23-27, 2018

Three-speed economic recovery

Three-speed economic recovery Projection after 2012 GDP growth, percent 10 8 6 4 2 0-2 Euro area -4-6 1992 1996 2000 2004 2008 2012 2016 Source: IMF WEO, April 2013. Emerging market and developing economies

Three-speed economic recovery Projection after 2012 GDP growth, percent 10 8 6 4 2 0-2 Euro area -4-6 1992 1996 2000 2004 2008 2012 2016 Source: IMF WEO, April 2013. Emerging market and developing economies

World real GDP growth in 2010 Annual percent change

World real GDP growth in 2010 Annual percent change 1 or more 6-1 3-6% 0-3% Less than No data Source: International Monetary Fund. World real GDP growth in 2011 Annual percent change 1 or more 6-1 3-6%

World real GDP growth in 2010 Annual percent change 1 or more 6-1 3-6% 0-3% Less than No data Source: International Monetary Fund. World real GDP growth in 2011 Annual percent change 1 or more 6-1 3-6%

The United States: Fiscal Facts and Fantasies. Presented by: Nigel Gault Chief U.S. Economist IHS Global Insight

The United States: Fiscal Facts and Fantasies Presented by: Nigel Gault Chief U.S. Economist IHS Global Insight Subdued Recovery: Tailwinds Battling Headwinds The U.S. Recovery: Tailwinds More sectors

The United States: Fiscal Facts and Fantasies Presented by: Nigel Gault Chief U.S. Economist IHS Global Insight Subdued Recovery: Tailwinds Battling Headwinds The U.S. Recovery: Tailwinds More sectors

FY 2017 Results Presentation H Results Presentation. Milan, 24 th April Milan, 27 th July 2018

FY 2017 Results Presentation Milan, 24 th April 2018 2018 1H Results Presentation Milan, 27 th July 2018 FY 2017 Results Presentation Milan, 24 th April 2018 Audience & Advertising gen-16 feb-16 mar-16

FY 2017 Results Presentation Milan, 24 th April 2018 2018 1H Results Presentation Milan, 27 th July 2018 FY 2017 Results Presentation Milan, 24 th April 2018 Audience & Advertising gen-16 feb-16 mar-16

RISI LATIN AMERICAN CONFERENCE. (São Paulo, 16 August 2016) The Latin American Economy: Some Successes, Many Disappointments

The Latin American Economy: Some Successes, Many Disappointments") RISI LATIN AMERICAN CONFERENCE (São Paulo, 16 August 2016) The Latin American Economy: Some Successes, Many Disappointments Andrea Boltho Magdalen College University of Oxford and Oxford Economics GDP

RISI LATIN AMERICAN CONFERENCE (São Paulo, 16 August 2016) The Latin American Economy: Some Successes, Many Disappointments Andrea Boltho Magdalen College University of Oxford and Oxford Economics GDP

The U.S. Economic Outlook

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

The US Economic Crisis: Impact on Northeast Asia, Lessons from Japan Richard Katz The Oriental Economist Report rbkatz@ix.netcom.com www.orientaleconomist.com 2008 Japan Watchers LLC. All rights reserved.

The Eurozone integration, des-integration and possible future developments

The Eurozone integration, des-integration and possible future developments 18 th Monetary Policy Workshop at the Berlin School of Economcs and Law, 12 13 October 2017 Overview Position 1: The euro itself

The Eurozone integration, des-integration and possible future developments 18 th Monetary Policy Workshop at the Berlin School of Economcs and Law, 12 13 October 2017 Overview Position 1: The euro itself

Alicorp: A History of Growth: Organic and through Acquisitions

October 2007 1 Alicorp: A History of Growth: Organic and through Acquisitions Merger Acquisition Merger Merger Acquisition Merger Acquisition 1993 Feb 95 Mar 95 Jun 95 Oct 95 Dic 96 Jan 01 Feb 04 Nov 05

October 2007 1 Alicorp: A History of Growth: Organic and through Acquisitions Merger Acquisition Merger Merger Acquisition Merger Acquisition 1993 Feb 95 Mar 95 Jun 95 Oct 95 Dic 96 Jan 01 Feb 04 Nov 05

INDUSTRY IN FIGURES January/2019

INDUSTRY IN FIGURES January/2019 1. Industry performance (short-term indicators) Main industrial indicators Variable Nov18/Oct18 (%) seasonally adjusted Nov18/Nov17 (%) Accumulated rate in the last 12

INDUSTRY IN FIGURES January/2019 1. Industry performance (short-term indicators) Main industrial indicators Variable Nov18/Oct18 (%) seasonally adjusted Nov18/Nov17 (%) Accumulated rate in the last 12

U.S. Oil & Gas Industry Chartbook

U.S. Oil & Gas Industry Chartbook BBVA Research USA Houston, TX August 2015 DISCLAIMER This document was prepared by Banco Bilbao Vizcaya (BBVA) BBVA Research U.S. on behalf of itself and its affiliated

U.S. Oil & Gas Industry Chartbook BBVA Research USA Houston, TX August 2015 DISCLAIMER This document was prepared by Banco Bilbao Vizcaya (BBVA) BBVA Research U.S. on behalf of itself and its affiliated

Agriculture and the Economy: A View from the Chicago Fed

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Agriculture and the Economy: A View from the Chicago Fed March 3, 2016 Riverside, Iowa David Oppedahl Senior Business Economist 312-322-6122 david.oppedahl@chi.frb.org Federal Reserve System Twelve District

Real gross domestic growth

Real gross domestic growth United States, 2000 prices Compound annual growth rate 10 5 0-5 -10 81 83 85 87 89 91 93 95 97 99 01 03 05 07 Sources: BEA, Global Insight. Consumer sentiment University of Michigan,

Real gross domestic growth United States, 2000 prices Compound annual growth rate 10 5 0-5 -10 81 83 85 87 89 91 93 95 97 99 01 03 05 07 Sources: BEA, Global Insight. Consumer sentiment University of Michigan,

INDUSTRY IN FIGURES July/2018

INDUSTRY IN FIGURES July/2018 1. Industry performance (short-term indicators) Main industrial indicators Variable May18/Apr18 (%) seasonally adjusted May18/May17 (%) Accumulated rate in the last 12 months;

INDUSTRY IN FIGURES July/2018 1. Industry performance (short-term indicators) Main industrial indicators Variable May18/Apr18 (%) seasonally adjusted May18/May17 (%) Accumulated rate in the last 12 months;

Montreal Real Estate Forum. Economic Outlooks for March 31, Cooperating in building the future

Montreal Real Estate Forum March 31, 2015 Economic Outlooks for 2015 François Dupuis Vice-President and Chief Economist Desjardins Group Cooperating in building the future Outline The global economy and

Montreal Real Estate Forum March 31, 2015 Economic Outlooks for 2015 François Dupuis Vice-President and Chief Economist Desjardins Group Cooperating in building the future Outline The global economy and

Jordi Prat Principal Economist March, 2018

Jordi Prat Principal Economist March, 2018 Agenda Economic Growth and Human Capital Foreign Banking in CADR and Financial Convergence Effect Favorable External Context Possible Shocks for CADR Favorable

Jordi Prat Principal Economist March, 2018 Agenda Economic Growth and Human Capital Foreign Banking in CADR and Financial Convergence Effect Favorable External Context Possible Shocks for CADR Favorable

Unconventional Monetary Policy: Thoughts on the U.S. and Japanese Experiences

Unconventional Monetary Policy: Thoughts on the U.S. and Japanese Experiences International Conference on Capital Flows and Safe Assets John Rogers Senior Adviser Federal Reserve Board May 27, 2013 The

Unconventional Monetary Policy: Thoughts on the U.S. and Japanese Experiences International Conference on Capital Flows and Safe Assets John Rogers Senior Adviser Federal Reserve Board May 27, 2013 The