U.S., Texas and North Texas Economic Trends and Forecast. Where are we? Where are we going? And what can we do about it?

|

|

|

- Reginald Lamb

- 5 years ago

- Views:

Transcription

1 U.S., Texas and North Texas Economic Trends and Forecast Where are we? Where are we going? And what can we do about it?

2 The North Texas Perspective: Real Estate Finance Executives Association March 12, 2015 M. Elizabeth Morris CEO / Chief Economist Insight Research Corporation

3 Our Services Land Use Economics Transportation Infrastructure Impact Analysis Investment-Grade Economic, Employment and Tax Revenue Analysis Site Selection Municipal Land Use and Financial Planning Analysis Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

4 Can Your City Afford Its Future? The Impact TRAKKER The Fast TRAKKER The Z-Snap TM The FlexTRAK DSM Insight s MUNICIPAL SUITE: Getting It Together... Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

2 SH 183 3 PGBT Superconnector 8 6 12 4 5 SH 360 PGBT Eastern Extension 15 6 7 8 Dallas North Tollway & Addison Toll Tunnel LBJ Freeway Improvements & Toll Tunnel Lake Lewisville")

5 DFW CMSA Transportation and Toll Improvements Completed or Underway Using Insight Research Corporation s Land Use, Demographic / Employment and Investment-Grade Forecasts 1 Trinity River Parkway (River Corridor) 2 SH PGBT Superconnector SH 360 PGBT Eastern Extension Dallas North Tollway & Addison Toll Tunnel LBJ Freeway Improvements & Toll Tunnel Lake Lewisville Bridge SH 121, SW Pkwy, Chisholm Trail Pkwy 10 Loop 9, SE Segment PGBT I-30 to I SH 121 Denton Collin County 13 SH 161 Extension SH-183 to I20 14 SH 80 Trans Reinvestment Zone 15 I 35E HOV Lane Analysis Blacklands Turnpike/ Northeast Gateway Currently Abandoned Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

6 Today s Topics Community Development and Economic Development A critical perspective U.S. Economy, Texas Comparison Texas to North Texas Economies Current Economic Chatter Leveraging Our State and Regional Advantages Forecast: U.S.-Texas-DFW MSA

7 Real Estate Development: The Primary Economic Development Source Developers and Finance Executives in the Real Estate Industry are key to a region s economic status Working with public and private sector partners, the real estate industry creates and maintains the local tax bases that allow public jurisdictions to function. The innovation, creativity and hard-won stability of property tax values is the bedrock of local revenues supporting any region s quality of life.

8 The Biggest Texas Advantage: Business Friendly Texas gets it! The clear understanding that... All taxes flow from profitable businesses. And all Jobs, too! Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

9 U.S. Economic, Employment and Population Trends

10 HISTORIC PROJECTED.com Bubble Depression 1929 to 1933 WW II 1941 to to 2001 Recent Recession 2007 to U.S. Cycles of Capital Investment 1919 to 2035, Insight s 2015 Forecast to 2035 High Cycle Points Low Cycle Points Total Employment Construction Employment

11 U.S. Cycles of Capital Investment 1919 to 1955.com Bubble Depression 1929 to 1933 WW II 1941 to to Source: U.S. Bureau of Labor Statistics High Cycle Points Low Cycle Points Total Employment Construction Employment Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

12 U.S. Cycles of Capital Investment, 1956 to Forecast to 2021 HISTORIC PROJECTED.com Bubble Depression 1929 to 1933 WW II 1941 to to 2001 High Cycle Points Low Cycle Points Recent Recession 2007 to Total Employment Construction Employment Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

13 HISTORIC PROJECTED.com Bubble Depression 1929 to 1933 WW II 1941 to to 2001 Recent Recession 2007 to LOOKING AGAIN at U.S. Cycles of Capital Investment 1919 to 2035, Insight s 2015 Forecast to 2035 High Cycle Points Low Cycle Points Total Employment Construction Employment

14 10 Real Economic Growth in the Gross Domestic Product (GDP) Percent Change from Previous Quarter at Annual Rate th Qtr 14: +2.2% A Recession: Two consecutive quarters of economic loss -10 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q Source: Bureau of Economic Analysis (Next Update April 30, 2015) Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

15 Components of the GDP Economic Component 2015 Status over 2014 Government Spending Consumer Spending Continued Unprecedented High Measurably More Optimistic Private Capital Investment Cautionary, Marginal Uptick Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

16 Job Job Recovery Time: time Current from Prior to Prior Recessions...from From Peak Peak to Return to Return in Months in Months

17 , , , , , , ,000 U.S. CIVILIAN LABOR FORCE, In Thousands of Workers, Source - U.S. BLS 154, ,899 Boomer retirements and other losses to US workforce 106,974

18 U.S. Unemployment Rate Percent 12 In Percent of Unemployed Persons in the Civilian Labor Force 10 U.S. Unemployment Feb % BLS considers 4% of Labor Force as Permanently Unemployed; 6.5% is Average Unemployment since JFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJF Source: U S BLS

19 120 U.S. Consumer Confidence Index From a Monthly Survey of 5,000 US Households, 1985 = February 15 U.S (p) At 25.3, Feb 09 was lowest since 1967 when index began. A healthy index is considered to be 90% JFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJ FMAMJ J ASONDJ F Source: The Conference Board

20 Economic Performance Comparisons US, Texas and North Texas

21 Texas Job Growth Outpaces US 1970 through 2014 Gray bars reflect US recessions, Year-to-year % change, SAA

22 Annual Average Unemployment Rate US (Blue), Texas (Red), No TX (Green) 12.0% 10.0% BLS considers 4% of Labor Force as Permanently Unemployed - 6.0% is Average Since % 6.0% 4.0% 2.0% December 2014 US: 5.6%, Texas: 4.6%, DFW 4.0% 0.0% Texas US N. Texas Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

23 % Change 5.0% 4.0% Civilian Labor Force Comparison U.S. to Texas to North Texas While the size of the US CLF declined in 2009 for the first time in 30 years, the CLF in Texas and North Texas continue to grow. 3.0% 2.0% 1.0% 0.0% -1.0% US TEXAS N. TEXAS Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

24 U.S. BEA Regional Market Segments

25 Comparisons of Regional Consumer Confidence Dec Dec Dec Dec Dec Dec Dec. Dec The Consumer Confidence Board considers a score of 90 to be a healthy baseline. Dec 2014 Difference from US Pacific Mountain Midwest Northeast Southeast West South Central U.S Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

26 140.0 Consumer Confidence Index West South Central Reg. Compared to U.S = West So Cent Difference From U.S West South Central 80.0 United States December 2014 Consumer Confidence Index West South Central Region: United States: Source: Conference Board JFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASOND Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

27 2014 Median Home Price and Inventory by Texas MSA % Price Increase, 2014 to 2013

28 US Auto Sales, , 2015 Projection Lower Gasoline Prices Boost Auto Sales

29 TEXAS METROPOLITAN STATISTICAL AREAS Ft. Worth-Arlington MD Johnson, Parker, Tarrant and Wise Counties Ft Worth Dallas-Plano-Irving MD Collin, Dallas, Delta, Denton, Ellis, Hunt, Kaufman and Rockwall Counties Dallas EL Paso MSA El Paso Co El Paso Austin Houston Austin-Round Rock MSA Bastrop, Caldwell, Hays, Travis and Williamson Counties San Antonio San Antonio MSA Atascosa, Bandera, Bexar, Comal, Guadalupe, Kendall, Medina and Wilson Counties Houston-Baytown-Sugar Land MSA Austin, Brazoria, Chambers, Fort Bend, Galveston, Harris, Liberty, Montgomery, San Jacinto and Waller Counties

30 ANNUAL AVERAGE UNEMPLOYMENT RATES U.S. Texas Austin Dallas Ft. Worth El Paso Houston San Antonio Source: U.S. Bureau of Labor Statistics Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

31 Population, % change, mid-year 2014 US Population Growth 0.9% or greater 0.4% to 0.9% 0.4% or less U.S. = 0.73% Sources: Census Bureau, Moody s Analytics

32 United States Population 1960 through 2014, Source U.S. Census Bureau 350,000, ,000, ,972, ,906, ,000, ,000, ,000, ,000,000 50,000, Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

33 State of Texas Population 1960 through ,000,000 25,000, ,624,000 20,000, ,956,958 15,000,000 10,000,000 5,000, Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

34 ,500,000 6,500,000 5,500,000 4,500,000 3,500,000 2,500,000 1,500, ,000 DFW MSA Population 1960 through ,425, ,097,813 or 26% of the State Dallas MD Ft Worth MD Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

35 AREAS OF PUBLIC UTILITY SERVICE AT TWENTY YEAR INTERVALS Dallas-Fort Worth Population Growth Areas Aqua 1970 Yellow 1990 White 2010 Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

36 Continuing Advantages for Texas, especially North Texas

37 Statewide Advantages Supporting The Competitive Texas Rebound Economic Realities Lower Cost of Living & Housing Employment Diversity Energy s Influence Marketing Support 4A&B Funds Local Incentive Flexibility Special Districts TIF, TIRZ Texas Enterprise Fund Public Policy Benefits Homestead LOC Cap No State Income Tax Speed to Market Right-to-Work State Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

38 TOTAL TAX BURDEN #1 High, # 50 Lowest % of Avg Per Capita Income Paid in State & Local Taxes 2011 Rank Rank Rank 2009 New York % % % New Jersey % % % Connecticut % % % California % % % Wisconsin % % % Minnesota % % % Maryland % % % Rhode Island % % % Vermont % % % Greatest Pennsylvania % % % Least Alabama % % % South Carolina % % % Nevada % % % New Hampshire % % % Tennessee % % % Louisiana % % % Texas % % % South Dakota % % % Alaska % % % Wyoming % % % Source: Bureau of Economic Analysis, Tax Foundation Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

39 The Biggest Texas Advantage: Business Friendly Texas gets it! The clear understanding that... All taxes flow from profitable businesses. And all Jobs, too! Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

40 Hillwood Properties, Corporate Services SPEED TO MARKET July 19 September 16 October 4 October 29 December 2 December 31

41 Texas: A Good Financial Bet Location Central Time Zone Economic Stability Oil/Gas, Defense, Transportation Job Creation and Population Growth Low Cost of Living/ Low Tax Burden Business Friendly Environment Local Control of Zoning, Special District Formation, Incentive Packages and Negotiations Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

42 DFW Real Estate Performance Overview Year End 2014

43 New and Existing Home Sales in the US Home sales continue to be supported by Job Growth, Low Rates

44 2014 Median Home Price and Inventory by TX MSA % Price Increase, 2014 to 2013

45 New Home Construction Flattens

46 Construction Contract Values Up

47 Market Segments Included: Single Family Multi Family Retail Office Industrial Each segment reviews Dallas, Fort Worth and the DFW performance data combined.

48 Single Family

49 50,000 DALLAS MD SINGLE FAMILY PERMITS 45,000 40,000 35,000 30,000 25,000 20,000 15,000 10,000 5, Annual Number of Permits Source: Texas A&M RE Center

50 DALLAS MD SINGLE FAMILY PERMITS BY COUNTY Hunt % Kaufman % Rockwall % Ellis % Denton % Collin % Delta % Dallas % Source: Texas A&M RE Center

51 Annual Number of Permits FORT WORTH MD SINGLE FAMILY PERMITS 50,000 45,000 40,000 35,000 30,000 25,000 20,000 15,000 10,000 5, Source: Texas A&M RE Center

52 FORT WORTH MD SINGLE FAMILY PERMITS BY COUNTY Wise 68 1% Johnson % Parker 376 6% Tarrant % Source: Texas A&M RE Center

53 DFW MSA SINGLE FAMILY PERMITS 50,000 45,000 40,000 35,000 30,000 25,000 20,000 15,000 10,000 5, Annual Number of Permits Source: Texas A&M RE Center

54 Multi-Family

55 65,000 55,000 45,000 35,000 25,000 15,000 5,000 (5,000) Source: CBRE Inc. DALLAS MD MULTI-FAMILY CONSTRUCTION Units ABSORBED DELIVERIES

56 65,000 55,000 45,000 35,000 25,000 15,000 5,000 (5,000) Source: CBRE Inc. FORT WORTH MD MULTI-FAMILY CONSTRUCTION Units ABSORBED DELIVERIES

57 Units DFW MSA MULTI-FAMILY CONSTRUCTION 65,000 55,000 45,000 35,000 25,000 15,000 5,000 (5,000) Source: CBRE Inc. ABSORPTION DELIVERIES

58 Retail

59 (3.0) Source: CBRE Inc. DALLAS MD RETAIL CONSTRUCTION Millions of Square Feet ABSORBED DELIVERIES

60 (3.0) Source: CBRE Inc. FORT WORTH MD RETAIL CONSTRUCTION Millions of Square Feet ABSORBED DELIVERIES

61 (3.0) Source: CBRE Inc. DFW MSA RETAIL CONSTRUCTION ABSORPTION DELIVERIES Millions of Square Feet

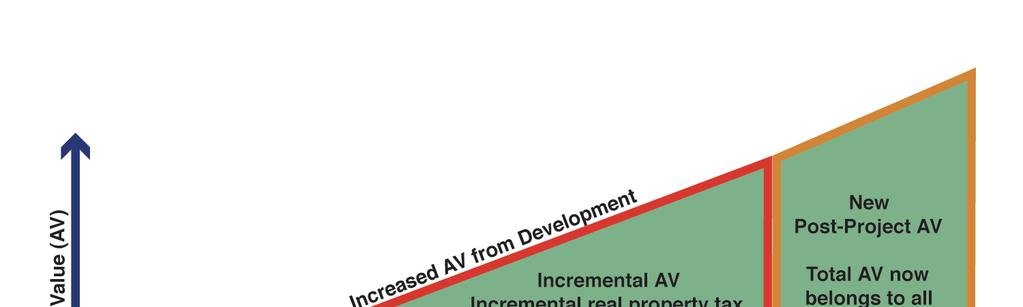

62 Office

63 DALLAS MD OFFICE CONSTRUCTION 25 Millions of Square Feet (5) Source: CBRE Inc. ABSORBED DELIVERIES

64 FORT WORTH MD OFFICE CONSTRUCTION 25 Millions of Square Feet (5) Source: CBRE Inc. ABSORBED DELIVERIES

65 Millions DFW MSA OFFICE CONSTRUCTION (5) Source: CBRE Inc. ABSORBED DELIVERIES

66 Industrial

67 (5) Source: CBRE Inc. DALLAS MD INDUSTRIAL CONSTRUCTION Millions ABSORBED DELIVERIES

68 FORT WORTH MD INDUSTRIAL CONSTRUCTION 30 Millions of Square Feet (5) Source: CBRE Inc. ABSORBED DELIVERIES

69 (5) Source: CBRE Inc. DFW MSA INDUSTRIAL CONSTRUCTION Millions ABSORPTION DELIVERIES

70 Special District Financing Increasingly Used Approaches that can Stabilize and Enable Development Opportunities

71

72 Typical TIF Eligibility Criteria A TIF District can be established if: There is significant potential to stimulate new, private sector, taxable development or redevelopment (regeneration). The public infrastructure is currently insufficient to support the new private sector development, including streets, utilities, water and wastewater treatment, sidewalks, lighting and common area public space. Development will not occur but for the creation of the District.

73 As Used in the US, Tax Increment Financing is NOT: A tax abatement program A direct or uncontrolled subsidy to a developer A tax break for property owners within the TIF District A public sector-initiated enticement -- but rather a response to the expressed infrastructure needs of private sector development commitments Tax increment financing IS an alternative financing tool in which the community decides to participate temporarily to help fund the costs of the district s infrastructure for the ultimate financial benefit of the community s tax base.

74

75 TEXAS MOTOR SPEEDWAY

76

77

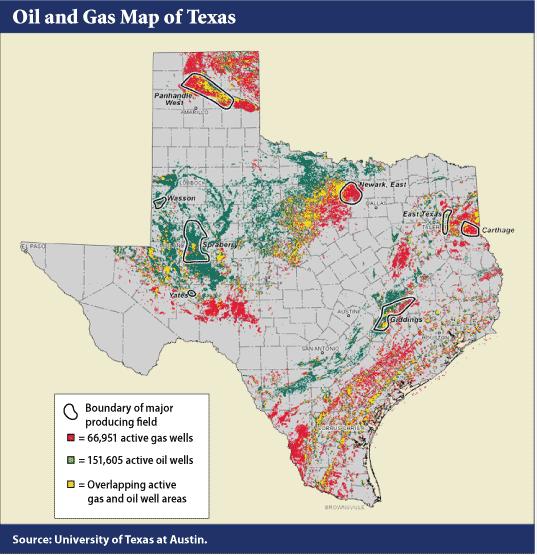

78 CITY OF FORNEY TIF/TRZ AREA (in Gold) Balance of the City s s Tax Base in Red, City Limit in Green TIF area is about 55% of the city s land area, and 18% of its existing tax base.

79 The U.S., Texas and North Texas Economic Forecast from Insight Research Corporation

80 FORECASTS AND FORECASTERS What do the Other Guys have to say about economic performance in Texas in the coming year? Comerica Bank Federal Reserve JPMorgan Chase Like this week s Northeast weather forecast, is the chatter about a poor performance year for 2015 in Texas just another snow job? Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

81 Regional Economic Effects of Higher Energy Prices S S Helped Hurt

82

83 How About Comerica Bank and The Dallas Federal Reserve Bank? The Chief Economist of Comerica Bank expects a 2.0% U.S. GDP growth in 2015, and forecasts a slowing economic outlook for Texas. The Chief Research Economist for the Federal Reserve Bank of Dallas expects slower growth in Texas as well, Texas may not outpace the U.S. economy. Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

84 And JPMorganChase? December 18, 2014: According to U.S. Chief Economist, JPMorgan Chase Michael Feroli, We think Texas will, at least, have a rough 2015 ahead, and is at risk of slipping into a regional recession. As support for his opinion, Feroli points to two months of job count decline statewide for Texas from January to March of Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

85

86 Direct Energy Employment Differences US and Selected Texas MSAs U.S. 0.6% of total employment, or 910,000 direct jobs nationwide Texas Average 2.6% 303,900 jobs statewide Houston MSA 4.0% 113,500 jobs in the region Midland-Odessa 20.0% 30,400 jobs regionally DFW MSA 0.7% 23,800 jobs Given the ripple effect multiplier applicable to employment, the Federal Reserve Bank estimates that approximately 140,000 direct and indirect jobs may be somewhat affected in the State of Texas. Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

87 A 2015 Texas Recession? According to Insight Research Corporation s Chief Economist, that perspective can be summed up in one word: RUBBISH! Shale production of oil & natural gas has been a boost to the Texas economy, helping to jump-start the employment numbers in the state ahead of much of the rest of the nation. However, unlike Feroli s additional citation of the similarities in Texas and North Dakota, the Texas economy is strong and diverse. At year end 2014, the Texas economy and particularly the North Texas economy -- has the bit between it s teeth and is experiencing strong gains in employment and in-migration of both companies and households. Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

88 Oil and Gas Prices Plunge

89

90 How long will lower gas prices last? The U.S. Energy Department projects a price at the pump of 2.16 per gallon during the first quarter of 2015 and $2.33 as an average through the year, down from an average of $3.36 per gallon in It projects an average of $2.72 per gallon for Diesel fuel prices, which averaged $3.83 per gallon in 2014, are expected to fall to $2.85 for 2015, and rise again to $3.25 per gallon in 2016.

91 Dueling Forces for Business Q: What weights the economy down? A. Added expenses to businesses and households. B. Risk Aversion Uncertainty; both businesses and households avoid risk Q: What propels it it forward? A. Lessened business and household expenses B. Risk Taking For both available credit and forecasting stability Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

92 Policy and Regulation Forecast Drivers in the U.S. ANTI-BUSINESS a) Dodd-Frank Act (DFA) b) Affordable Care Act Implementation Uncertainties c) New Taxes, Fewer Exemptions d) Oil, Coal, Gas Restrictions; Cap & Trade PRO-BUSINESS a) Increasing Credit Availability b) Regulatory Revisions to Reduce Business Costs c) Lower Overall Taxes: Local, State & Federal, Capital Gains and Estate d) Lower Energy Cost Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

93 Assumptions for the U.S. Forecast Good: Continued overall economic and housing market recovery Mixed: Fed Action: Slowly increasing interest rates Slowly increasing inflation Reduced oil prices Bad: More domestic terrorism, deteriorating Mid- and Far East... Too important to ignore, too expensive to fix. Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

94 United States Total and Construction Employment 1981 through 2014 Historic; 2015 through 2035 Forecast Annual % of Change Historic EOY 2014 Projected US Total Employment US Construction Employment Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

95 Texas and North Texas Forecasting Assumptions

96 Texas & No. Texas Economic Keys As of 2015, Texas continues to be light years ahead of the U.S. recovery in terms of job change percentages, especially true in North Texas The Texas economy and job creation performance continued to grow steadily Major Texas cities 2014 housing markets continued rapid improvement, making the switch from a buyer s to a seller s market, driven by the State s increasing employment and inmigration. Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

97 Comparison of U.S, Texas and North Texas Construction Employment 1981 through 2014 Historic; 2015 through 2035 Forecast % Change 20 Historic EOY 2014 Projected At year end 2014, Texas is outperforming the U.S. recovery at a remarkable pace: U.S. 3.5%, TX 5.0%, No. Texas 12.6% US Const. Employment Texas Const. Employment N. TX Const. Employment Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

98 State of Texas Total and Construction Employment 1981 through 2014 Historic; 2015 through 2035 Forecast Annual % of Change 15 Historic EOY 2014 Projected Total Employment Construction Employment Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

99 Annual % of Change 25 DFW MSA Total and Construction Employment 1981 through 2014 Historic; 2015 through 2035 Forecast Historic EOY 2014 Projected Regional economic slowdowns can be expected about 2020, and again in Total Employment Construction Employment Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

100 Executive Summary Insight is Upbeat for 2015

101 Executive Summary: Insight is Upbeat for North Texas in 2015 & 2016 While other economists are predicting slower growth and even a recession for Texas, Insight Research is more bullish, citing the demonstrated economic strengths of North Texas. Meeting pent-up demand, the region is poised to continue strong economic development successes. Texas may slow slightly from 2014 in 2015, but Austin and Houston as well as DFW remain strong powerhouses of economic demand and strength. Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

102 Upbeat for North Texas in 2015 & 2016 In 2016, a Presidential election year will likely bring a measurable slowing of activity nationwide as businesses and families postpone major decisions to see what may affect them. This happens almost every Presidential election year as the negative drumbeat of daily media and political ads dominate communications. Notwithstanding, North Texas is poised to continue to outpace the U.S. and Texas averages as well into the next economic cycle.

103 Meeting Looming Challenges Stay ahead of the multiple challenges posed by a rapidly increasing population using all the economic development tools at our disposal: 4A,4B, TIRZ, TIF, and most important, locally controlled incentives. Plan for and provide for Texas future water needs. Manage and finance our transportation, mobility and infrastructure requirements. Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

104

105 Recognize the Importance of and Protect Some Texas Advantages! Keep Texas one of seven states in the U.S. with no state income tax. Protect our right-to-work status. Keep the cost of living down Insist on professional public management and budget practices. Maintain the economic advantages of our 80% homestead cap on home loan debt that protected Texas in the mortgage meltdown as compared to many other parts of the U.S. Copyright Insight Research Corporation, P.O. Box 61, Allen, TX

106 In other words, keep doing the Texas thing!

107 The circulation of confidence is better than the circulation of money. - James Madison -

108 Our Mission Insight Research Corporation clearly defines the economic costs and benefits of project alternatives so that decision makers have fully informed choices.

Partnerships with Purpose: Housing for Texans

Partnerships with Purpose: Housing for Texans 25th Annual TALHFA Educational Conference October 25-27, 2017 Fort Worth, Texas Dr. James P. Gaines Chief Economist 2 Outlook Since November 10, 2017: Rising

Partnerships with Purpose: Housing for Texans 25th Annual TALHFA Educational Conference October 25-27, 2017 Fort Worth, Texas Dr. James P. Gaines Chief Economist 2 Outlook Since November 10, 2017: Rising

Texas Housing Markets: Metropolitan vs. Border Communities. September 22, 2014

Texas Housing Markets: Metropolitan vs. Border Communities Luis Bernardo Torres Ruiz, Ph.D. Research Economist El Paso Branch Dallas Federal Rio Grande Economic Association September 22, 2014 Contents

Texas Housing Markets: Metropolitan vs. Border Communities Luis Bernardo Torres Ruiz, Ph.D. Research Economist El Paso Branch Dallas Federal Rio Grande Economic Association September 22, 2014 Contents

Dr. James P. Gaines Research Economist recenter.tamu.edu

Texas Uncertain Economy in a World of Uncertain Oil Prices Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 U.S. Outlook Expected GDP growth still modest:

Texas Uncertain Economy in a World of Uncertain Oil Prices Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 U.S. Outlook Expected GDP growth still modest:

The 2019 Economic Outlook Forum The Outlook for MS

The 2019 Economic Outlook Forum The Outlook for MS February 2019 Mississippi University Research Center Mississippi Institutions of Higher Learning Darrin Webb, State Economist dwebb@mississippi.edu (601)432-6556

The 2019 Economic Outlook Forum The Outlook for MS February 2019 Mississippi University Research Center Mississippi Institutions of Higher Learning Darrin Webb, State Economist dwebb@mississippi.edu (601)432-6556

Your Texas Economy. Current through: Tuesday, Nov 20, 2018

Your Texas Economy Current through: Tuesday, Nov 20, 2018 Overview of Texas Economy The Texas economy is growing robustly in 2018 2018 job growth through October is 2.9 percent annualized compared to 2.1

Your Texas Economy Current through: Tuesday, Nov 20, 2018 Overview of Texas Economy The Texas economy is growing robustly in 2018 2018 job growth through October is 2.9 percent annualized compared to 2.1

Will 2016 Be the Last Hurrah for Commercial Real Estate? Presented By: John Chang First Vice-President Marcus & Millichap Research Services

Will 2016 Be the Last Hurrah for Commercial Real Estate? Presented By: John Chang First Vice-President Marcus & Millichap Research Services Rising Uncertainty Creating Headwinds for Commercial Real Estate

Will 2016 Be the Last Hurrah for Commercial Real Estate? Presented By: John Chang First Vice-President Marcus & Millichap Research Services Rising Uncertainty Creating Headwinds for Commercial Real Estate

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

The U.S. Economy How Serious A Downturn? Nigel Gault Group Managing Director North American Macroeconomic Services Growth Is Cooling; But a Soft Landing Is Likely (Real GDP, annualized rate of growth)

Economy On The Rebound

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

Economy On The Rebound Robert Johnson Associate Director of Economic Analysis November 17, 2009 robert.johnson@morningstar.com (312) 696-6103 2009, Morningstar, Inc. All rights reserved. Executive

2019 Economic Outlook: Will the Recovery Ever End?

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

2019 Economic Outlook: Will the Recovery Ever End? Advantage Bank Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 15 th, 2018

Dr. James P. Gaines Research Economist. recenter.tamu.edu

Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 National Issues Expected GDP growth still modest: 2015 2.5%; personal consumption 2.5% Inflation not worrisome:

Dr. James P. Gaines Research Economist recenter.tamu.edu National Economic Recovery still Going 2 National Issues Expected GDP growth still modest: 2015 2.5%; personal consumption 2.5% Inflation not worrisome:

Houston and Tomball Economic and. Housing Outlook. recenter.tamu.edu. Dr. James P. Gaines Research Economist

Houston and Tomball Economic and Dr. James P. Gaines Research Economist Housing Outlook recenter.tamu.edu THE CURRENT SITUATION The Future Just Ain t What It Used to Be! Yogi Berra National Economic Recovery

Houston and Tomball Economic and Dr. James P. Gaines Research Economist Housing Outlook recenter.tamu.edu THE CURRENT SITUATION The Future Just Ain t What It Used to Be! Yogi Berra National Economic Recovery

Charting a Path to Lift Off? Understanding the Shifting Economic Winds

Charting a Path to Lift Off? Understanding the Shifting Economic Winds Thomas F. Siems, Ph.D. Assistant Vice President and Senior Economist Federal Reserve Bank of Dallas Government Finance Officers Arlington,

Charting a Path to Lift Off? Understanding the Shifting Economic Winds Thomas F. Siems, Ph.D. Assistant Vice President and Senior Economist Federal Reserve Bank of Dallas Government Finance Officers Arlington,

recenter.tamu.edu Dr. James P. Gaines Research Economist Real Estate Center at Texas A&M University

recenter.tamu.edu Dr. James P. Gaines Research Economist Real Estate Center at Texas A&M University Area Market Reports RECENTER.TAMU.EDU Tierra Grande Economic Review Videos, Audios & Presentations Data,

recenter.tamu.edu Dr. James P. Gaines Research Economist Real Estate Center at Texas A&M University Area Market Reports RECENTER.TAMU.EDU Tierra Grande Economic Review Videos, Audios & Presentations Data,

Your Texas Economy. Last updated: January 30, 2018

Your Texas Economy Last updated: January 30, 2018 Texas economy strong in 2017 2017 job growth was 2.4% Overview 2015/2016 job growth was much weaker due to the oil bust (1.3% and 1.2%, respectively) 2014

Your Texas Economy Last updated: January 30, 2018 Texas economy strong in 2017 2017 job growth was 2.4% Overview 2015/2016 job growth was much weaker due to the oil bust (1.3% and 1.2%, respectively) 2014

Zions Bank Economic Overview

Zions Bank Economic Overview Kenworth National Dealers Conference November 8, 2018 1 National Economic Conditions 2 Volatility Returns to the Stock Market 27,000 Dow Jones Industrial Average October 10,

Zions Bank Economic Overview Kenworth National Dealers Conference November 8, 2018 1 National Economic Conditions 2 Volatility Returns to the Stock Market 27,000 Dow Jones Industrial Average October 10,

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder Member FDIC VectraBank.com Economic Outlook 2015 Richard

Dr. Richard Wobbekind Executive Director, Business Research Division and Senior Associate Dean for Academic Programs University of Colorado Boulder Member FDIC VectraBank.com Economic Outlook 2015 Richard

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States?

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Canadian Teleconference: Can the Canadian Economy Survive the Turmoil in the United States? Nigel Gault Chief U.S. Economist Dale Orr Canadian Macroeconomic Services Copyright 2008 Global Insight, Inc.

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Trends. September 10, 2013

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Trends September 10, 2013 The Freight Economy Washington continues to be a headwind on economic

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME MBA Program in Colorado according to U.S. News & World Report Engage in a collaborative

Big Changes, Unknown Impacts

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

Big Changes, Unknown Impacts Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 2018 Real GDP Growth

The Auction Market In 2015 & 2016 Review & Forecast. Dr. Ira Silver NAAA Economist

The Auction Market In 2015 & 2016 Review & Forecast Dr. Ira Silver NAAA Economist silver@naaa.com Agenda Economic conditions Economic outlook Light vehicle sales Light vehicle sales outlook NAAA 2015 Annual

The Auction Market In 2015 & 2016 Review & Forecast Dr. Ira Silver NAAA Economist silver@naaa.com Agenda Economic conditions Economic outlook Light vehicle sales Light vehicle sales outlook NAAA 2015 Annual

Babson Capital/UNC Charlotte Economic Forecast. May 13, 2014

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Babson Capital/UNC Charlotte Economic Forecast May 13, 2014 Outline for Today Myths and Realities of this Recovery Positive Economic Signs Negative Economic Signs Outlook for 2014 The Employment Picture

Education Committee Economic Background and Issue Review

Education Committee Economic Background and Issue Review Montpelier, Vermont January 22, 2014 Thomas E. Kavet State Economist and Principal Economic Advisor to the Vermont State Legislature Since 1996

Education Committee Economic Background and Issue Review Montpelier, Vermont January 22, 2014 Thomas E. Kavet State Economist and Principal Economic Advisor to the Vermont State Legislature Since 1996

More of the Same; Or now for Something Completely Different?

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

More of the Same; Or now for Something Completely Different? C2ER Place cover image here Richard Wobbekind Chief Economist and Associate Dean for Business and Government Relations June 14, 2017 Real GDP

The Wisconsin and Minnesota Economies: What can we learn from each other? Noah Williams

The Economies: What can we learn from each other? Noah University of Wisconsin - Madison Future Wisconsin Summit 2016 Economies Location, size, demographics, and history make Wisconsin and Minnesota natural

The Economies: What can we learn from each other? Noah University of Wisconsin - Madison Future Wisconsin Summit 2016 Economies Location, size, demographics, and history make Wisconsin and Minnesota natural

Economic Overview. Melissa K. Peralta Senior Economist April 27, 2017

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

Economic Overview Melissa K. Peralta Senior Economist April 27, 2017 TTX Overview TTX functions as the industry s railcar cooperative, operating under pooling authority granted by the Surface Transportation

U.S. Overview. Gathering Steam? Tuesday, October 1, 2013

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

U.S. Overview Gathering Steam? Tuesday, October 1, 2013 Uneven global economic recovery Annual real GDP growth projections (%) Projections 2013 2014 World 3.1 3.1 3.8 United States 2.2 1.7 2.7 Euro Area

Spring Time for Housing

Spring Time for Housing Arizona State University December 2 nd, 2015 Presented By: Elliott D. Pollack CEO, IN PHOENIX 1 2 The World has Changed Pre-2007 Post-2007 3 Employment Growth From Bottom of Recession

Spring Time for Housing Arizona State University December 2 nd, 2015 Presented By: Elliott D. Pollack CEO, IN PHOENIX 1 2 The World has Changed Pre-2007 Post-2007 3 Employment Growth From Bottom of Recession

THE FUTURE OF SALES TAX REVENUE

THE FUTURE OF SALES TAX REVENUE Presented by Adam Fulton, Senior Economic Associate The Outlook for Sales Taxes State governments rely on state sales taxes for more than a fifth of their revenue Economic

THE FUTURE OF SALES TAX REVENUE Presented by Adam Fulton, Senior Economic Associate The Outlook for Sales Taxes State governments rely on state sales taxes for more than a fifth of their revenue Economic

The U.S. Economic Outlook

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

The U.S. Economic Outlook Nigel Gault Chief U.S. Economist, IHS Global Insight FTA Revenue Estimation & Tax Research Conference Charleston, West Virginia October 17, 2011 What Has Happened to the Recovery?

10 County Conference. Richard Wobbekind. Executive Director Business Research Division & Senior Associate Dean Leeds School of Business

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

10 County Conference Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business Hmm... (http://myfallsemester.blogspot.com) Real GDP Growth Percent

WHERE ARE ARIZONA DEMOGRAPHICS TAKING US? HOW GROWING SLOWER, OLDER AND MORE DIVERSE AFFECTS REAL ESTATE

WHERE ARE ARIZONA DEMOGRAPHICS TAKING US? HOW GROWING SLOWER, OLDER AND MORE DIVERSE AFFECTS REAL ESTATE March 2017 Tom Rex Office of the University Economist and Center for Competitiveness and Prosperity

WHERE ARE ARIZONA DEMOGRAPHICS TAKING US? HOW GROWING SLOWER, OLDER AND MORE DIVERSE AFFECTS REAL ESTATE March 2017 Tom Rex Office of the University Economist and Center for Competitiveness and Prosperity

Zions Bank Economic Overview

Zions Bank Economic Overview Intermountain Credit Education League May 10, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around

Zions Bank Economic Overview Intermountain Credit Education League May 10, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around

Bob Costello Chief Economist & Vice President American Trucking Associations. Economic & Motor Carrier Industry Update.

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Update February 26, 2013 The Worst Recession Since the Great Depression 0% Loss from Peak

Bob Costello Chief Economist & Vice President American Trucking Associations Economic & Motor Carrier Industry Update February 26, 2013 The Worst Recession Since the Great Depression 0% Loss from Peak

MARKET AND CAPACITY UPDATE. Matthew Marsh September 2016

MARKET AND CAPACITY UPDATE Matthew Marsh September 2016 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

MARKET AND CAPACITY UPDATE Matthew Marsh September 2016 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

ABA Commercial Real Estate Lending Committee

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

ABA Commercial Real Estate Lending Committee Commercial Real Estate Outlook The Good, the Bad and the Ugly January 16, 2019 Rob Strand Senior Economist American Bankers Association aba.com 1-800-BANKERS

U.S. Economy in a Snapshot

U.S. Economy in a Snapshot Economic Press Briefing: May 19, 2016 The views expressed here are those of the presenter and do not necessarily represent the views of the Federal Reserve Bank of New York or

U.S. Economy in a Snapshot Economic Press Briefing: May 19, 2016 The views expressed here are those of the presenter and do not necessarily represent the views of the Federal Reserve Bank of New York or

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch June 2016

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch June 2016 Image from http://peoplesguidetohouston.wordpress.com/category/uncategorized/

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch June 2016 Image from http://peoplesguidetohouston.wordpress.com/category/uncategorized/

2014 Economic Forecast: Boulder & Beyond. Keynote Presentation

2014 Economic Forecast: Boulder & Beyond Keynote Presentation Business Research Division Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business

2014 Economic Forecast: Boulder & Beyond Keynote Presentation Business Research Division Richard Wobbekind Executive Director Business Research Division & Senior Associate Dean Leeds School of Business

How Much Wind Is in the Sails?

How Much Wind Is in the Sails? Erie Chamber of Commerce Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations September 20, 2017 Real GDP Growth

How Much Wind Is in the Sails? Erie Chamber of Commerce Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations September 20, 2017 Real GDP Growth

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Economic Update and Outlook NAIOP Vancouver Chapter November 15, 2012 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global, U.S., and Canadian economic conditions Canada economic and

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office The views expressed in this presentation are strictly those of the author and do not necessarily

Texas Economic Outlook: Recovery in 2010 Keith Phillips Federal Reserve Bank of Dallas San Antonio Office The views expressed in this presentation are strictly those of the author and do not necessarily

Economic Growth in the Trump Economy

Economic Growth in the Trump Economy Presented to State Data Center Conference William F. Fox, Director November 18, 2016 GDP Grows, Though Slowly 10.0 8.0 Percentage Change, Previous Qtr, SAAR 6.0 4.0

Economic Growth in the Trump Economy Presented to State Data Center Conference William F. Fox, Director November 18, 2016 GDP Grows, Though Slowly 10.0 8.0 Percentage Change, Previous Qtr, SAAR 6.0 4.0

Zions Bank Economic Overview

Zions Bank Economic Overview Veteran Owned Business Conference May 11, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around Correction

Zions Bank Economic Overview Veteran Owned Business Conference May 11, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around Correction

The Economy: A View from the (Atlanta) Fed (Staff)

Fed (Staff)") The Economy: A View from the (Atlanta) Fed (Staff) 2018 Alabama Economic Outlook Montgomery, AL January 11, 2018 2 The new supply-side economics? In their discussion of monetary policy, participants saw

The Economy: A View from the (Atlanta) Fed (Staff) 2018 Alabama Economic Outlook Montgomery, AL January 11, 2018 2 The new supply-side economics? In their discussion of monetary policy, participants saw

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

2019 ECONOMIC FORECAST AND FINANCIAL MARKET UPDATE January 14, 2019 Scott Colbert, CFA Executive Vice President Director of Fixed Income & Chief Economist scott.colbert@commercebank.com GLOBAL GROWTH EXPECTATIONS

Future Global Trade Trends - Risks & Opportunities. Pulse of the Ports: Peak Season Forecast March 21, 2013

1 Future Global Trade Trends - Risks & Opportunities Pulse of the Ports: Peak Season Forecast March 21, 2013 June 2012 Dr. Walter Kemmsies Chief Economist Summary Higher economic growth in 2013, possible

1 Future Global Trade Trends - Risks & Opportunities Pulse of the Ports: Peak Season Forecast March 21, 2013 June 2012 Dr. Walter Kemmsies Chief Economist Summary Higher economic growth in 2013, possible

Legislative Economic Briefing

Legislative Economic Briefing February 16, 2017 Mississippi University Research Center Mississippi Institutions of Higher Learning Darrin Webb, State Economist dwebb@mississippi.edu (601)432-6556 To subscribe

Legislative Economic Briefing February 16, 2017 Mississippi University Research Center Mississippi Institutions of Higher Learning Darrin Webb, State Economist dwebb@mississippi.edu (601)432-6556 To subscribe

Colorado Economic Update

Colorado Economic Update Steamboat Economic Summit Place cover image here Brian Lewandowski Associate Director, Business Research Division October 21, 2016 Recession 8 Months Recession 18 Months Real GDP

Colorado Economic Update Steamboat Economic Summit Place cover image here Brian Lewandowski Associate Director, Business Research Division October 21, 2016 Recession 8 Months Recession 18 Months Real GDP

Understanding the. Dr. Christopher Waller. Federal Reserve Bank of St. Louis

Understanding the Unemployment Picture Dr. Christopher Waller Senior Vice President and Director of fresearch Federal Reserve Bank of St. Louis By David Andolfatto and Marcela Williams A Look at Unemployment

Understanding the Unemployment Picture Dr. Christopher Waller Senior Vice President and Director of fresearch Federal Reserve Bank of St. Louis By David Andolfatto and Marcela Williams A Look at Unemployment

Curves On The Road Ahead

Curves On The Road Ahead Light Vehicle Market Outlook November 2018 Charles Chesbrough Senior Economist A g e n d a Economic Outlook and New Vehicle Sales Affordability Threat and the Used Vehicle Market

Curves On The Road Ahead Light Vehicle Market Outlook November 2018 Charles Chesbrough Senior Economist A g e n d a Economic Outlook and New Vehicle Sales Affordability Threat and the Used Vehicle Market

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

2018 Annual Economic Forecast Dragas Center for Economic Analysis and Policy PRESENTING SPONSOR EVENT PARTNERS 2 The forecasts and commentary do not constitute an official viewpoint of Old Dominion University,

The U.S. Economic Outlook

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

The U.S. Economic Outlook Presented to: Maquiladora Industry Outlook Conference September 29 2006 Presented by: Patrick Newport Principal, U.S. Macroeconomic Service 781-301-9125 patrick.newport@globalinsight.com

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

Deficit Reduction and Economic Growth: Are They Mutually Exclusive Goals? Tuesday, May 1, 2012; 2:30 PM - 3:45 PM Moderator: Gillian Tett, U.S. Managing Editor, Financial Times Speakers: Jared Bernstein,

Demographic Characteristics and Trends of Bexar County and San Antonio, TX

Demographic Characteristics and Trends of Bexar County and San Antonio, TX Leadership San Antonio Understand Infrastructure. Prepare for Growth. May 2, 2012 San Antonio, TX Select Growing States, 2000-2010

Demographic Characteristics and Trends of Bexar County and San Antonio, TX Leadership San Antonio Understand Infrastructure. Prepare for Growth. May 2, 2012 San Antonio, TX Select Growing States, 2000-2010

Investing in Real Estate. The smart choice for today s investor

Investing in Real Estate The smart choice for today s investor Real Estate is preferred over stocks Real estate out performs stocks http://blog.863katy.com/category/national-housing-news/page/2/ Real Estate

Investing in Real Estate The smart choice for today s investor Real Estate is preferred over stocks Real estate out performs stocks http://blog.863katy.com/category/national-housing-news/page/2/ Real Estate

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

National and Virginia Economic Outlook Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business October 24, 2018 The forecasts and commentary do not constitute

A comment on recent events, and...

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

A comment on recent events, and... where we are in the current economic cycle November 15, 2016 Mark Schniepp Director Likely Trump Policies $4 to $5 Trillion in tax cuts over 10 years to corporations,

MUSTAFA MOHATAREM Chief Economist, General Motors

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

MUSTAFA MOHATAREM Chief Economist, General Motors INTRODUCTION The U.S. economy continues to grow at a gradual but also erratic pace The current recovery is one of the slowest in the post-wwii U.S. history.

RISI Housing Report An Update on the Housing Market

RISI Housing Report An Update on the Housing Market North American Conference October 2018 Jennifer Coskren Senior Economist Agenda Current housing demand and demographic conditions Supply and impediments

RISI Housing Report An Update on the Housing Market North American Conference October 2018 Jennifer Coskren Senior Economist Agenda Current housing demand and demographic conditions Supply and impediments

Transitions: 2019 Economic Forecast for Metro Denver February 6, 2019

Transitions: 2019 Economic Forecast for Metro Denver February 6, 2019 Prepared by: Can Stock Photo / jkirsh In Partnership with: Consumer Changes and Influences Slowing population growth Aging of the population

Transitions: 2019 Economic Forecast for Metro Denver February 6, 2019 Prepared by: Can Stock Photo / jkirsh In Partnership with: Consumer Changes and Influences Slowing population growth Aging of the population

U.S. Property Market Outlook, 2013Q1. Jim Costello, Managing Director CBRE Americas Research Investment Research

U.S. Property Market Outlook, 2013Q1 Jim Costello, Managing Director CBRE Americas Research Investment Research CBRE Page 2 Outlook for the Real Side of the Economy Operationally, what do Research Teams

U.S. Property Market Outlook, 2013Q1 Jim Costello, Managing Director CBRE Americas Research Investment Research CBRE Page 2 Outlook for the Real Side of the Economy Operationally, what do Research Teams

colorado.edu/business/brd

colorado.edu/business/brd Big Changes, Unknown Impacts Southwest Business Forum Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January

colorado.edu/business/brd Big Changes, Unknown Impacts Southwest Business Forum Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January

PROVINCE OF SASKATCHEWAN INVESTOR PRESENTATION

PROVINCE OF SASKATCHEWAN INVESTOR PRESENTATION May 2018 THE SASKATCHEWAN DIFFERENCE Economic Stability Diversified economy balances cyclicality of resources Growing population Majority government with

PROVINCE OF SASKATCHEWAN INVESTOR PRESENTATION May 2018 THE SASKATCHEWAN DIFFERENCE Economic Stability Diversified economy balances cyclicality of resources Growing population Majority government with

U.S. AUTO INDUSTRY UPDATE Federal Reserve Bank of Chicago Automotive Outlook Symposium. Emily Kolinski Morris Chief Economist May 2015

U.S. AUTO INDUSTRY UPDATE Federal Reserve Bank of Chicago Automotive Outlook Symposium Emily Kolinski Morris Chief Economist May 2015 NORTH AMERICA INDUSTRY VOLUME SUMMARY 13.1 Total North America* (Mils.)

U.S. AUTO INDUSTRY UPDATE Federal Reserve Bank of Chicago Automotive Outlook Symposium Emily Kolinski Morris Chief Economist May 2015 NORTH AMERICA INDUSTRY VOLUME SUMMARY 13.1 Total North America* (Mils.)

North American Forging Shipment Forecast (Using FIA bookings information through December 2013)

") North American Forging Shipment Forecast 2014-2018 (Using FIA bookings information through December 2013) Percent Change Year Ago Best leading indicator combination for impression die bookings used to

North American Forging Shipment Forecast 2014-2018 (Using FIA bookings information through December 2013) Percent Change Year Ago Best leading indicator combination for impression die bookings used to

The Chamber of Commerce for Greater Philadelphia Economic Outlook Survey Results

The Chamber of Commerce for Greater Philadelphia Economic Outlook Survey Results January 19, 2018 Elif Sen Senior Economic Analyst FEDERAL RESERVE BANK OF PHILADELPHIA * The views expressed today are my

The Chamber of Commerce for Greater Philadelphia Economic Outlook Survey Results January 19, 2018 Elif Sen Senior Economic Analyst FEDERAL RESERVE BANK OF PHILADELPHIA * The views expressed today are my

2016 Texas Prosperity Conference The Barnhill Center Brenham, Texas August 26, Dr. James P. Gaines Chief Economist. recenter.tamu.

2016 Texas Prosperity Conference The Barnhill Center Brenham, Texas August 26, 2016 Dr. James P. Gaines Chief Economist recenter.tamu.edu Housing and People 2 Texas Population 1910-2050 60,000,000 50,000,000

2016 Texas Prosperity Conference The Barnhill Center Brenham, Texas August 26, 2016 Dr. James P. Gaines Chief Economist recenter.tamu.edu Housing and People 2 Texas Population 1910-2050 60,000,000 50,000,000

Kevin Thorpe Financial Economist & Principal Cassidy Turley

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

Kevin Thorpe Financial Economist & Principal Cassidy Turley Economic & Commercial Real Estate Outlook Kevin Thorpe, Chief Economist 2012 Another Year Of Modest Improvement 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1

From Recession to Recovery

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

From Recession to Recovery Monday, April 26, 2010 8:00 AM - 9:15 AM Moderator Michael Klowden, President and CEO, Milken Institute Speakers Mohamed El-Erian, CEO and Co-Chief Investment Officer, Pacific

Global economy maintaining solid growth momentum. Canada leading the pack

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

Global economy maintaining solid growth momentum Canada leading the pack Dawn Desjardins (Deputy Chief Economist) (416) 974-6919 dawn.desjardins@rbc.com September 2017 Brighter global outlook gains traction

U.S. Economic and Apartment Market Overview and Outlook. July 15, 2014

2014 U.S. Economic and Apartment Market Overview and Outlook July 15, 2014 U.S. Economic Overview U.S. GDP Growth Persistent Despite 1Q Polar Vortex Annualized Quarterly Percent Change 10% 5% 0% -5% -10%

2014 U.S. Economic and Apartment Market Overview and Outlook July 15, 2014 U.S. Economic Overview U.S. GDP Growth Persistent Despite 1Q Polar Vortex Annualized Quarterly Percent Change 10% 5% 0% -5% -10%

THE MOST INFORMATIVE EVENT COVERING REAL ESTATE INVESTMENTS

THE MOST INFORMATIVE EVENT COVERING REAL ESTATE INVESTMENTS 2014 U.S. Economic, Capital Markets, and Retail Market Overview and Outlook Retail Trends 2014 U.S. Economic Overview and Outlook Total Employment

THE MOST INFORMATIVE EVENT COVERING REAL ESTATE INVESTMENTS 2014 U.S. Economic, Capital Markets, and Retail Market Overview and Outlook Retail Trends 2014 U.S. Economic Overview and Outlook Total Employment

Northwest Economic Research Center College of Urban and Public Affairs Forecast Breakfast Economic Outlook

Northwest Economic Research Center College of Urban and Public Affairs 2019 Forecast Breakfast Economic Outlook 1/10/2019 2 U.S. ECONOMY 1/10/2019 3 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Northwest Economic Research Center College of Urban and Public Affairs 2019 Forecast Breakfast Economic Outlook 1/10/2019 2 U.S. ECONOMY 1/10/2019 3 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Real Estate and Economic Outlook

Real Estate and Economic Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation at Inforum Outlook Conference University of Maryland College Park, MD December 12, 2013

Real Estate and Economic Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation at Inforum Outlook Conference University of Maryland College Park, MD December 12, 2013

Briefing on the State of the State. presented to the. SCAA Schuyler Center for Analysis and Advocacy

Briefing on the State of the State presented to the SCAA Schuyler Center for Analysis and Advocacy Rae D. Rosen Assistant Vice President Federal Reserve Bank of New York November 16, 2006 Key Points: Economic

Briefing on the State of the State presented to the SCAA Schuyler Center for Analysis and Advocacy Rae D. Rosen Assistant Vice President Federal Reserve Bank of New York November 16, 2006 Key Points: Economic

Wenlin Liu, Senior Economist. Stateof Wyoming. Economic Analysis Division State of Wyoming 1

WYOMING DEMOGRAPHIC AND ECONOMIC TREND LCCC LIFE Program April 7, 2012 Cheyenne, Wyoming Wenlin Liu, Senior Economist Economic Analysis Division Stateof Wyoming Economic Analysis Division State of Wyoming

WYOMING DEMOGRAPHIC AND ECONOMIC TREND LCCC LIFE Program April 7, 2012 Cheyenne, Wyoming Wenlin Liu, Senior Economist Economic Analysis Division Stateof Wyoming Economic Analysis Division State of Wyoming

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks. Business Research Division Leeds School of Business

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks Presented by the Business Research Division Leeds School of Business University of Colorado at Boulder U.S. Economic

U.S. and Colorado Economic Outlook National Association of Industrial and Office Parks Presented by the Business Research Division Leeds School of Business University of Colorado at Boulder U.S. Economic

Frederick Ross. Real Estate Market Overview. Presented by: Kevin Thomas Senior Vice President. Frederick Ross. Company.

Frederick Ross Real Estate Market Overview Presented by: Kevin Thomas Senior Vice President Frederick Ross Company January 2003 Business Consumers Source: BEA, Ross Research Housing...Bust or Rust? 2001

Frederick Ross Real Estate Market Overview Presented by: Kevin Thomas Senior Vice President Frederick Ross Company January 2003 Business Consumers Source: BEA, Ross Research Housing...Bust or Rust? 2001

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch January 2017

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch January 2017 Image from http://peoplesguidetohouston.wordpress.com/category/uncategorized/

The Houston Economy Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch January 2017 Image from http://peoplesguidetohouston.wordpress.com/category/uncategorized/

Zions Bank Economic Overview

Zions Bank Economic Overview Logan Rotary Club June 28, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around Correction Territory

Zions Bank Economic Overview Logan Rotary Club June 28, 2018 Dow Tops 26,000 Up 48% Since 2016 Election Jan 26, 2018 26,616 Oct 30, 2016 17,888 Source: Wall Street Journal Dow Around Correction Territory

The ABA Advantage: Economic Issues Update & ABA Resources

The ABA Advantage: Economic Issues Update & ABA Resources aba.com 1-800-BANKERS Meet the team Jim Chessen Chief Economist Curtis Dubay Senior Economist Brittany Kleinpaste Vice President of Economic Policy

The ABA Advantage: Economic Issues Update & ABA Resources aba.com 1-800-BANKERS Meet the team Jim Chessen Chief Economist Curtis Dubay Senior Economist Brittany Kleinpaste Vice President of Economic Policy

DFW MULTIFAMILY TRENDS & OBSERVATIONS Q2 2017

DFW MULTIFAMILY TRENDS & OBSERVATIONS Q2 2017 DALLAS / FORT WORTH The Top US Demand Driven Apartment Market DFW MULTIFAMILY STARTS A HISTORY LESSON!!! The challenge boom or bust perception vs recent history

DFW MULTIFAMILY TRENDS & OBSERVATIONS Q2 2017 DALLAS / FORT WORTH The Top US Demand Driven Apartment Market DFW MULTIFAMILY STARTS A HISTORY LESSON!!! The challenge boom or bust perception vs recent history

Telling Canada s story in numbers Elizabeth Richards Analytical Studies Branch April 20, 2017

Recent Developments in the Canadian Economy: How have the decline in oil prices and a weaker Canadian dollar affected Canada s economy? www.statcan.gc.ca Telling Canada s story in numbers Elizabeth Richards

Recent Developments in the Canadian Economy: How have the decline in oil prices and a weaker Canadian dollar affected Canada s economy? www.statcan.gc.ca Telling Canada s story in numbers Elizabeth Richards

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

Economic Update and Prospects for 2019 Professor Robert M. McNab Dragas Center for Economic Analysis and Policy Strome College of Business January 3, 2019 The forecasts and commentary do not constitute

As Good as it Gets. The Aging Expansion Powers On... but for How Much Longer? Andrew J. Nelson Chief Economist USA, Colliers International

As Good as it Gets The Aging Expansion Powers On... but for How Much Longer? Andrew J. Nelson Chief Economist USA, Colliers International #NMHCstudent @ApartmentWire Ten Years After: A Full if Imperfect

As Good as it Gets The Aging Expansion Powers On... but for How Much Longer? Andrew J. Nelson Chief Economist USA, Colliers International #NMHCstudent @ApartmentWire Ten Years After: A Full if Imperfect

Shifting International Trade Routes A National Economic Outlook. February 1, 2011

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

Shifting International Trade Routes A National Economic Outlook February 1, 2011 Today s Objectives Endeavor to provide a broad context for today s program by briefly touching on: Some good news Some not

What s Ahead for The Colorado Economy?

What s Ahead for The Colorado Economy? Colorado Counties Inc. Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 28, 2017 Real GDP

What s Ahead for The Colorado Economy? Colorado Counties Inc. Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations November 28, 2017 Real GDP

The Outlook for Real Estate and Residential Construction. Patrick M. Barkey, Director Bureau of Business and Economic Research University of Montana

The Outlook for Real Estate and Residential Construction Patrick M. Barkey, Director Bureau of Business and Economic Research University of Montana Montana s Real Estate Performance: Getting Back to Boom

The Outlook for Real Estate and Residential Construction Patrick M. Barkey, Director Bureau of Business and Economic Research University of Montana Montana s Real Estate Performance: Getting Back to Boom

Noah Williams. University of Wisconsin-Madison Center for Research On the Wisconsin Economy (CROWE) Outlook for the Wisconsin Economy

Outlook for the Wisconsin Economy") An Noah University of Wisconsin-Madison Center for Research On the Wisconsin Economy (CROWE) CROWE: Brief Introduction Center for Research on the Wisconsin Economy (CROWE) recently established in the Department

An Noah University of Wisconsin-Madison Center for Research On the Wisconsin Economy (CROWE) CROWE: Brief Introduction Center for Research on the Wisconsin Economy (CROWE) recently established in the Department

Nevada County Population Projections 2013 to 2032 Based On The Last Estimate Year of 2012

Nevada County Population Projections 2013 to 2032 Based On The Last Estimate Year of 2012 Prepared By: The Nevada State Demographer s Office Jeff Hardcastle, AICP NV State Demographer University of NV

Nevada County Population Projections 2013 to 2032 Based On The Last Estimate Year of 2012 Prepared By: The Nevada State Demographer s Office Jeff Hardcastle, AICP NV State Demographer University of NV

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee The U.S. economy has now enjoyed 7 years of economic growth since the Great Recession Real GDP grew by 1.2% in

Larry Kessler, Ph.D. Boyd Center for Business & Economic Research University of Tennessee The U.S. economy has now enjoyed 7 years of economic growth since the Great Recession Real GDP grew by 1.2% in

Southwest Ohio Regional Economy in Context. Richard Stock, PhD. Business Research Group

Southwest Ohio Regional Economy in Context Richard Stock, PhD. Business Research Group State of the Metro Area (in January Each Year) Total Employment has slowly increased in the last three years after

Southwest Ohio Regional Economy in Context Richard Stock, PhD. Business Research Group State of the Metro Area (in January Each Year) Total Employment has slowly increased in the last three years after

By making use of SAFRIM (South African Inter-Industry Macro-Economic Model) By Jeaunes Viljoen, Conningarth Economists, 1

By Jeaunes Viljoen, Conningarth Economists, 1") By making use of SAFRIM (South African Inter-Industry Macro-Economic Model) By Jeaunes Viljoen, Conningarth Economists, South Africa 10/13/2011 1 1960: The economy experienced high growth rates mining

By making use of SAFRIM (South African Inter-Industry Macro-Economic Model) By Jeaunes Viljoen, Conningarth Economists, South Africa 10/13/2011 1 1960: The economy experienced high growth rates mining

U.S Cement Outlook IEEE. Ed Sullivan Group VP, Chief Economist

U.S Cement Outlook IEEE Ed Sullivan Group VP, Chief Economist 1 Construction Activity Billion Real $ 1,400 1,200 1,000 2014 = 2.5% 2015 = 5.6% 800 600 400 200 0 12 Year Peak-to- Peak Recovery 1998 2000

U.S Cement Outlook IEEE Ed Sullivan Group VP, Chief Economist 1 Construction Activity Billion Real $ 1,400 1,200 1,000 2014 = 2.5% 2015 = 5.6% 800 600 400 200 0 12 Year Peak-to- Peak Recovery 1998 2000

Economic Analysis What s happening with U.S. potential GDP growth?

Economic Analysis What s happening with U.S. potential GDP growth? Kan Chen Capital stock, labor, and productivity do not show a significant increase following the recent fiscal stimulus According to our

Economic Analysis What s happening with U.S. potential GDP growth? Kan Chen Capital stock, labor, and productivity do not show a significant increase following the recent fiscal stimulus According to our

The Texas Gulf Coast Overview and Outlook

The Texas Gulf Coast Overview and Outlook Jesse Thompson Federal Reserve Bank of Dallas Houston Branch 06/2018 The views expressed in this presentation are strictly those of the presenter and do not necessarily

The Texas Gulf Coast Overview and Outlook Jesse Thompson Federal Reserve Bank of Dallas Houston Branch 06/2018 The views expressed in this presentation are strictly those of the presenter and do not necessarily

11 th Annual Oregon Economic Forum!

11 th Annual Oregon Economic Forum! (almost) Beyond! Macroeconomics Portland, OR! October 16, 2014! Expansion Continues! Five Years and More!! Recession Indicators Nonfarm Payrolls Real Personal Income

11 th Annual Oregon Economic Forum! (almost) Beyond! Macroeconomics Portland, OR! October 16, 2014! Expansion Continues! Five Years and More!! Recession Indicators Nonfarm Payrolls Real Personal Income

Economic Outlook for Canada: Economy Confronting Capacity Limits

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

ECONOMICS I RESEARCH Economic Outlook for Canada: Economy Confronting Capacity Limits Presentation to the Responsible Distribution Canada 32 nd Annual General Meeting May 29, 2018 Paul Ferley (Assistant

Southern California Economic Forecast & Industry Outlook

2016-17 Southern California Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Sr. VP/Chief Economist, LAEDC February 17, 2016 Outline U.S. Economy California Economy Southern California Economy

2016-17 Southern California Economic Forecast & Industry Outlook Robert A. Kleinhenz, Ph.D. Sr. VP/Chief Economist, LAEDC February 17, 2016 Outline U.S. Economy California Economy Southern California Economy